Kirpal Kooner

Expensive readers,

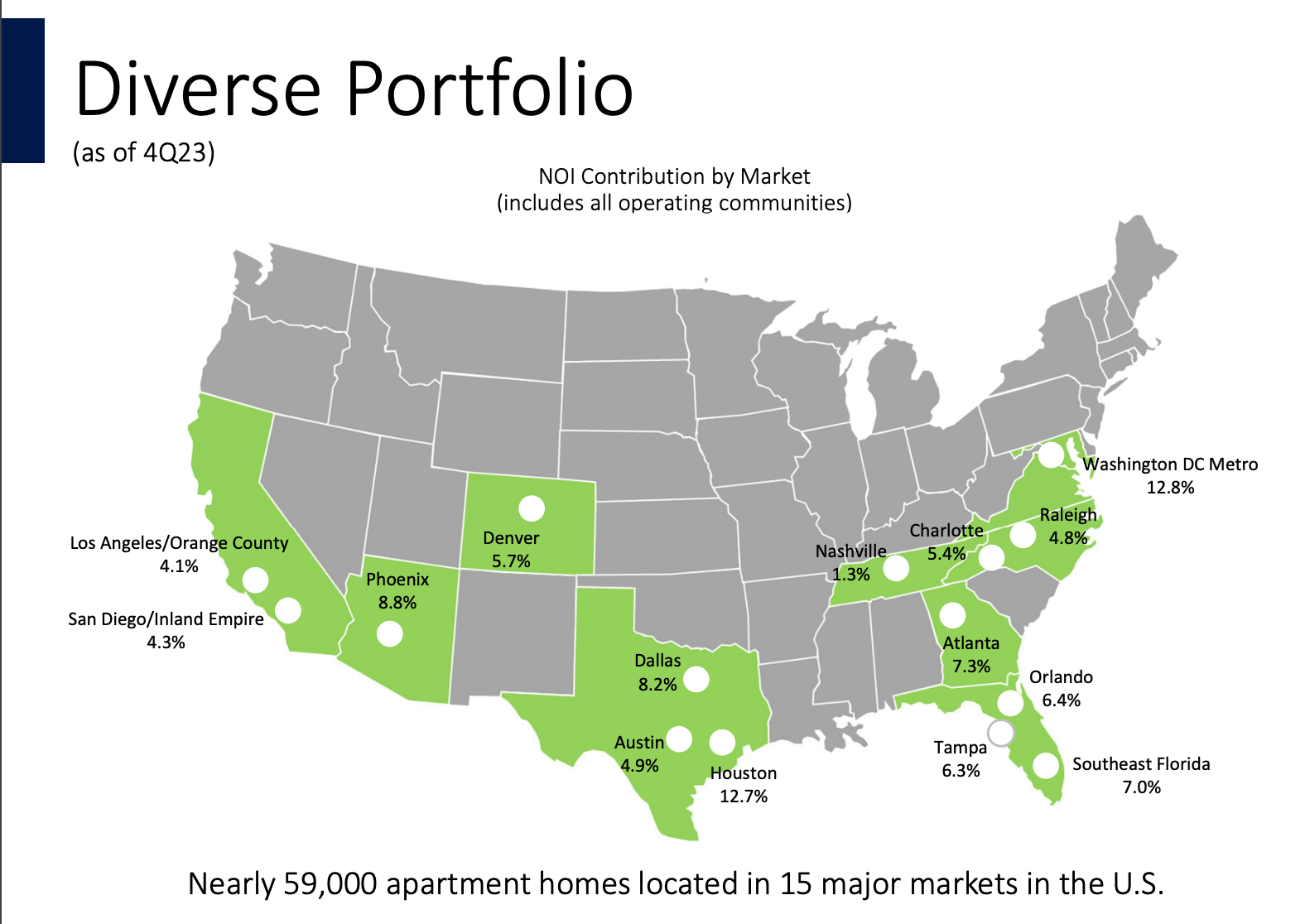

Camden Property Belief (NYSE:CPT) is a significant house REIT with almost 60,000 models positioned throughout the Sunbelt (together with California). Notably, a big portion of models are low-rise (59%) and B-Class (62%) which brings an a variety of benefits. I’ve written extensively about why I see B-Class within the Sunbelt as effectively positioned, particularly relative to A-Class. When you’re , you possibly can learn up on this matter in my article on BSR REIT (OTCPK:BSRTF) titled BSR REIT: Why B-Class Apartments Could Outperform.

CPT IR

I’ve covered Camden earlier than, final February, and got here to a conclusion that the inventory was a BUY at $120 per share. My thesis, which known as for an OKish 9% complete return, was primarily based on CPT’s spectacular A- score and a valuation of 18x FFO and an implied cap charge of 5.5%. I used to be effectively conscious of the over-supply threat in Camden’s markets, spent a substantial a part of my final article on the anticipated supply-demand dynamics, and got here to a conclusion that the file provide in 2024 and 2025 (particularly in Texas) was prone to get (principally) absorbed.

It turned out, nonetheless, that I used to be fallacious. Sunbelt house markets have softened and in consequence, my name has underperformed with an RoR of -16% in comparison with a shocking return of the S&P 500 (SPX) of 26%.

Market positioning

Dallas, Austin and Atlanta account for 20% of Camden’s ABR and are all amongst the top 5 cities within the U.S. with the best anticipated enhance in stock in 2024. Furthermore, new provide is predicted to be even increased subsequent yr.

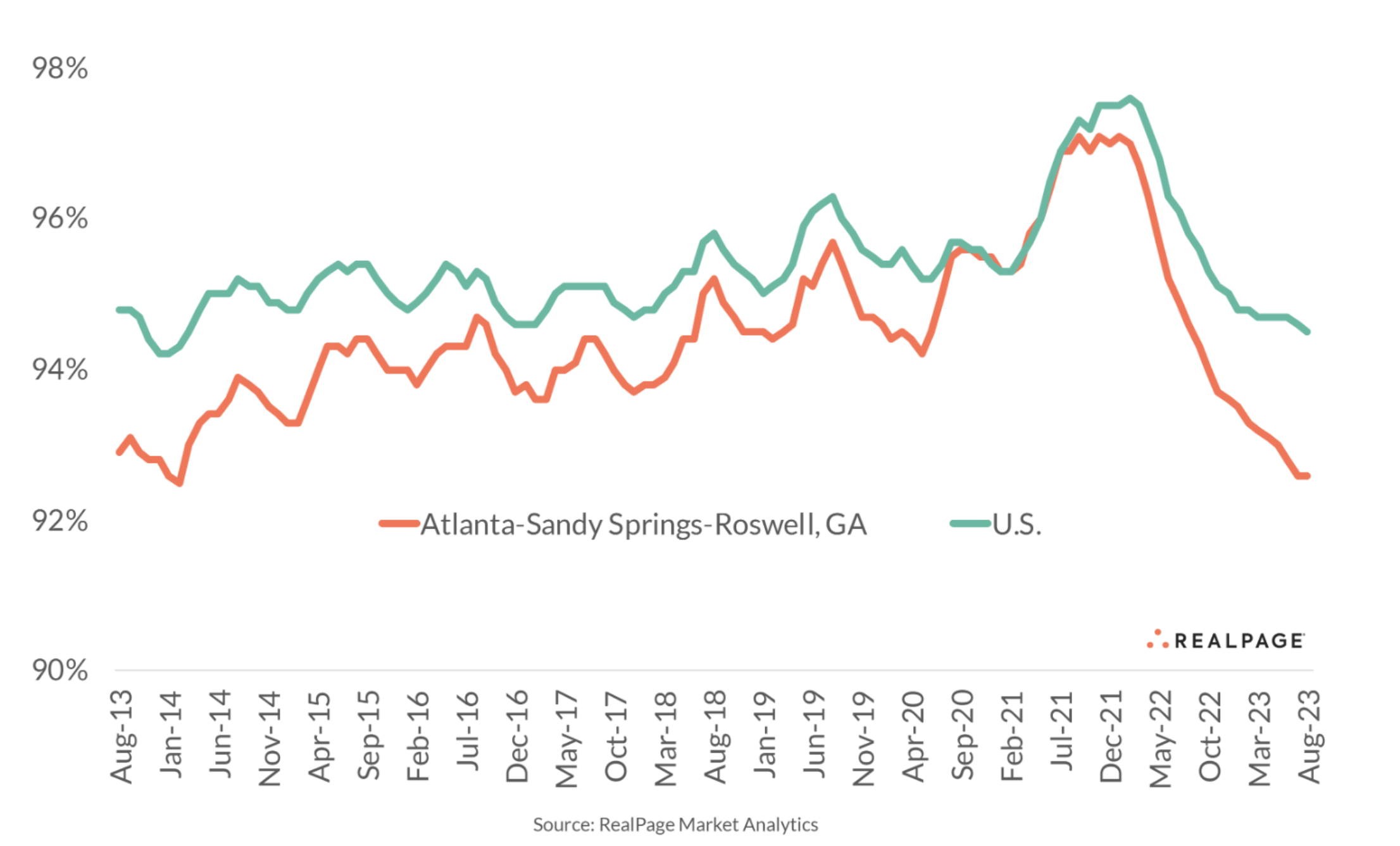

In consequence, these markets are already seeing important will increase in emptiness. In Atlanta, the common emptiness elevated to eight% and vacancies for brand new models in Dallas are as excessive as 10%.

Actual Web page

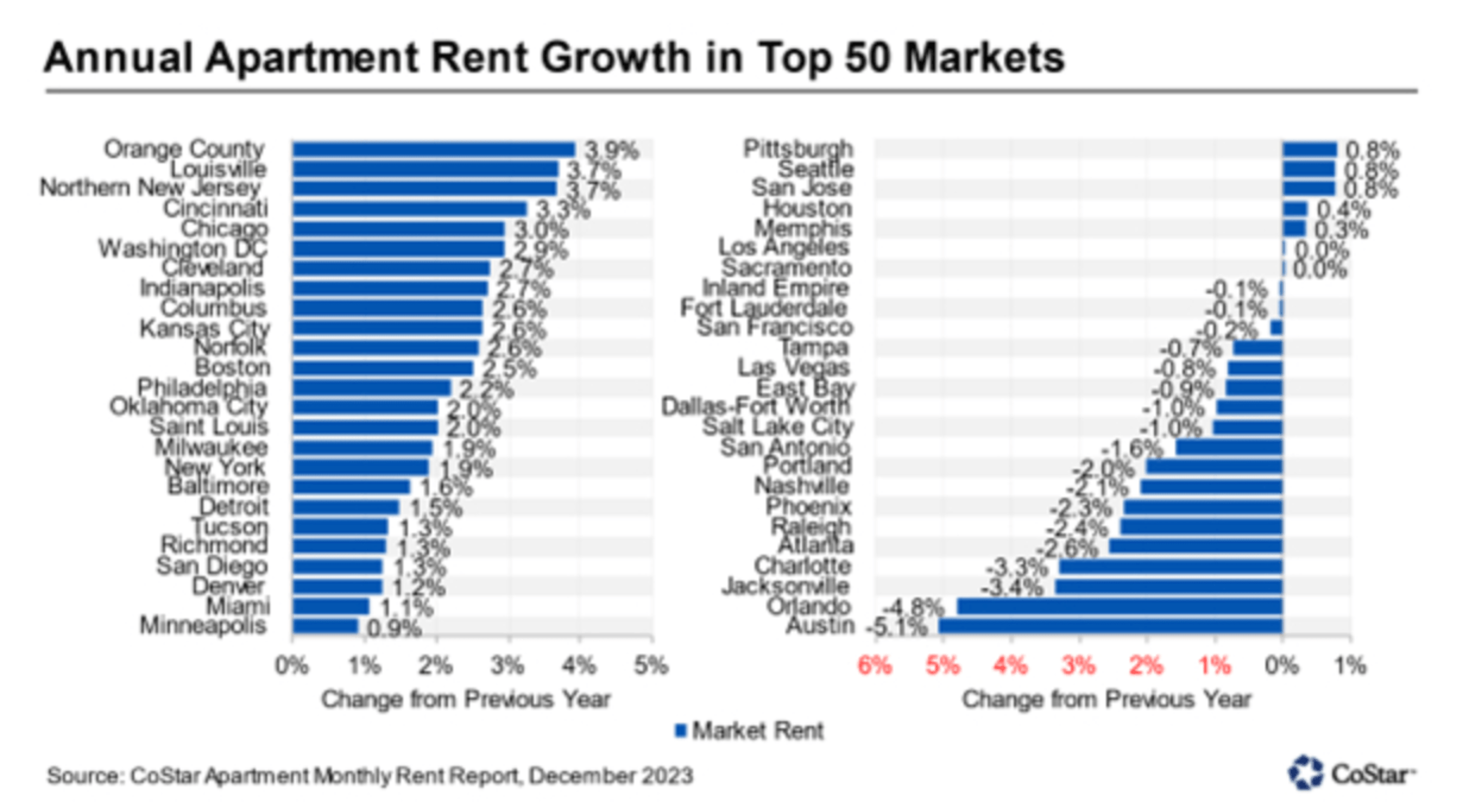

In consequence, rents have come beneath strain. To call a number of of Camden’s largest markets, Austin is down 5.1% YoY, Orlando is down 4.6%, and Atlanta is down 2.6% YoY. And that is earlier than the height in provide subsequent yr.

CoStar

So what’s the take away right here?

It is fairly clear to me that rents within the Sunbelt are prone to decline additional this yr and in 2025. However just for A-Class house. You see, the brand new provide that we have mentioned to date is solely A-Class. B-Class would not get construct, slightly residences change into B-Class with time as they age. In consequence, Camden, which has a big portion of B-Class residences, might be comparatively proof against declining rents. Moreover, the California publicity would possibly really assist stabilize the portfolio, as California is not seeing a lot new provide in any respect and rents are anticipated to be regular.

In both case, I just like the prospects of house REITs within the Sunbelt past 2025. Development begins are down by 27% nation-wide over the past two years and rather more within the Sunbelt because of rising development, vitality and financing prices. This implies much less provide publish 2025. Mixed with the ever growing unaffordability of housing which leads to extra renters by necessity and subsequently extra demand, rents might in a short time rebound, maybe even explode in 2025 and past.

Camden’s money movement – outcomes and steering

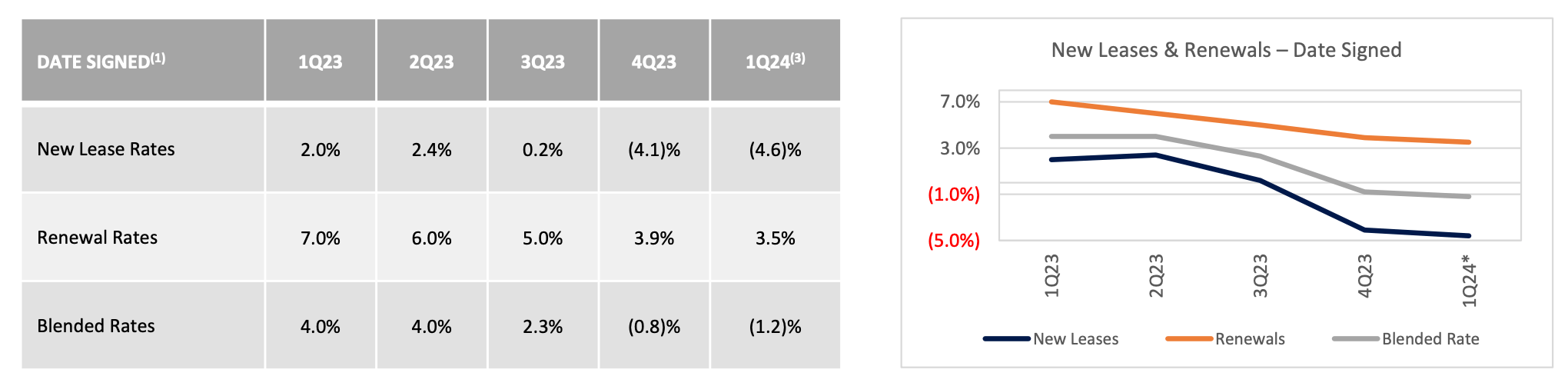

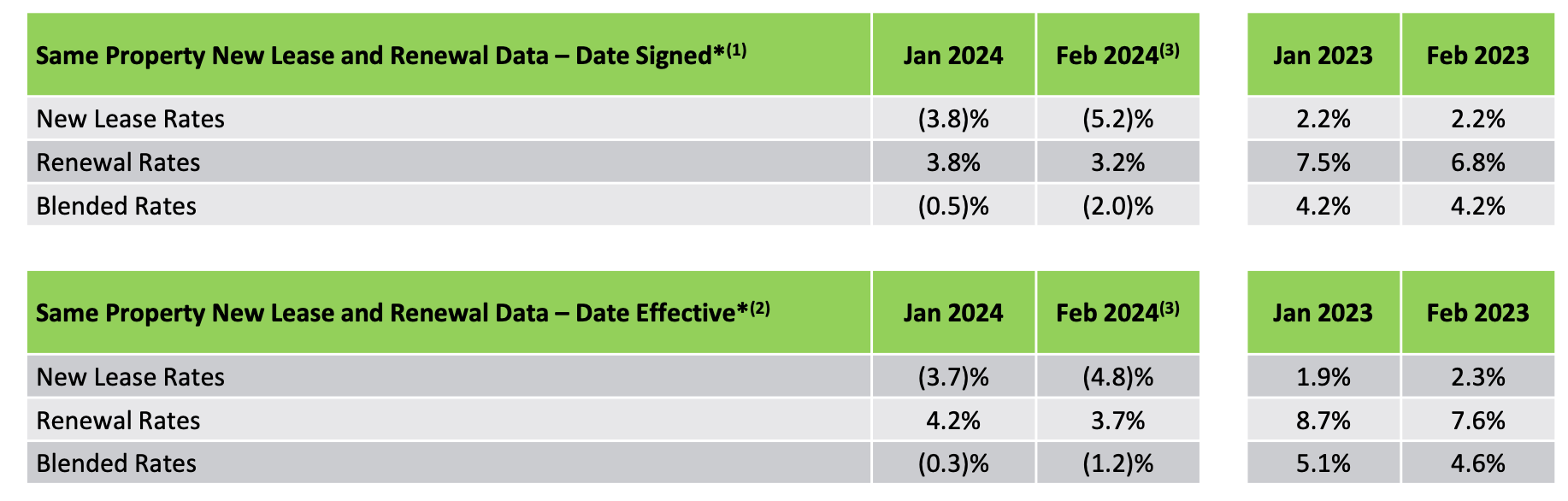

Camden managed to publish strong full year 2023 results with 3% annual FFO development. However slowing lease development has been evident. All year long, lease will increase on renewals have declined from 7% in Q1 to three.9% in This autumn and on new leases the decline has been much more pronounced as lease development dipped into damaging territory in This autumn at -4.1%.

Camden IR

To fight this, administration has carried out a advertising and marketing marketing campaign to spice up occupancy forward of the same old peak leasing season (Q2). The marketing campaign focuses totally on communities with occupancy beneath 95% and on models which were vacant for 30 days or extra. The aim is to deliver occupancy above the present 94.9%.

Going ahead, administration is guiding for income development of 1.5% in 2024, down considerably from 2023. However charges on leases signed in January and February present that even this decrease goal is perhaps onerous to realize. It’s regular that leasing is gradual in Q1, however a slowdown from a blended lease enhance of 4-5% final yr to damaging 1-2% this yr is hardly a optimistic. Notably, the slowdown has primarily been a results of round a 4% drop in rents in a few of Camden’s largest and most overbuild markets similar to Austin and Atlanta.

Camden IR

In consequence, administration’s steering and the overall consensus for FFO development has declined since my final article from 4-5% in 2024 and 2025 to -1.5% this yr and three% subsequent yr.

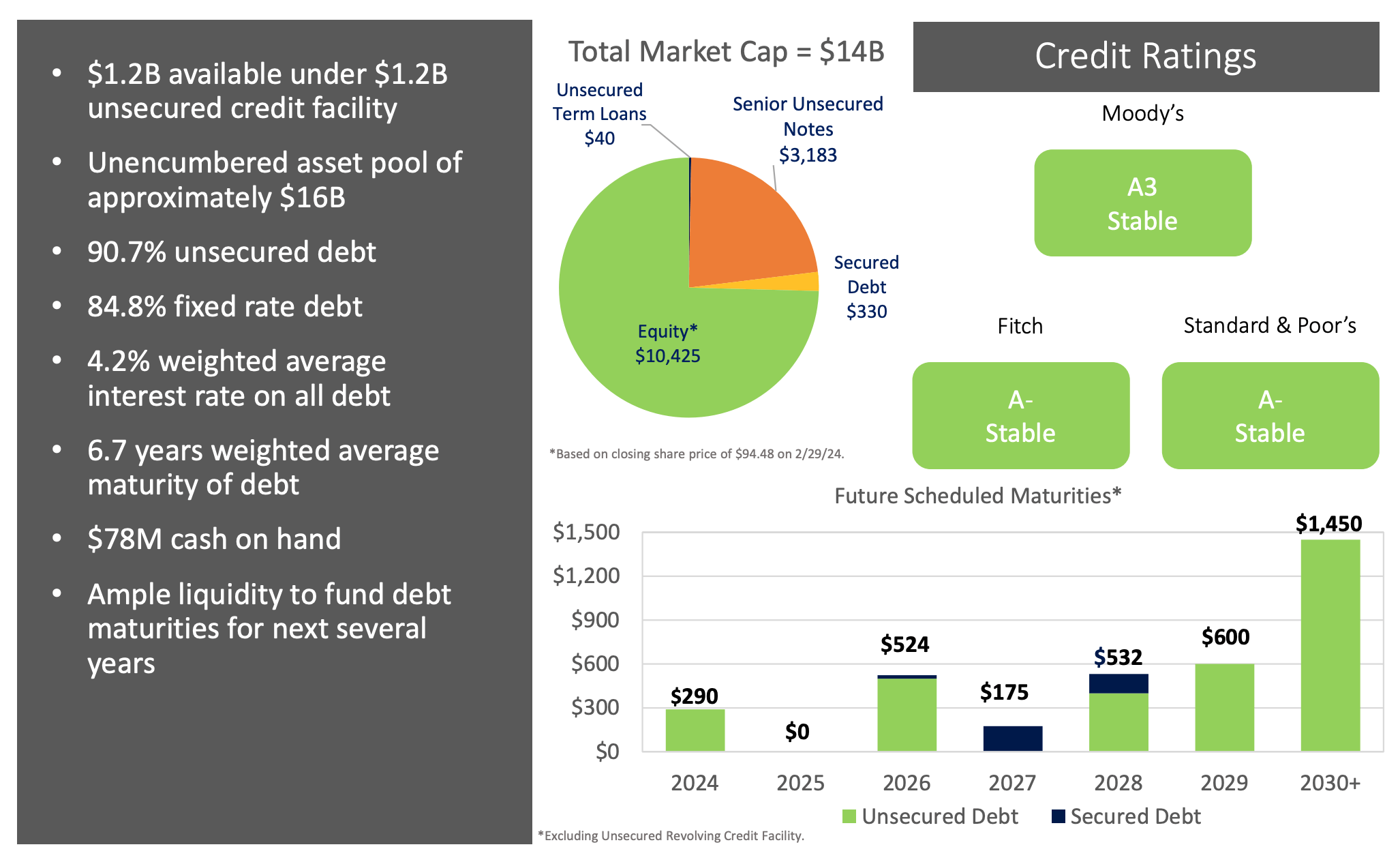

With a secure A- rated steadiness sheet with a big portion (85%) of fastened charge debt and low close to time period maturities, Camden’s money movement (and FFO) is prone to be fairly secure and predictable.

Camden IR

Having mentioned the house market outlook, I consider that Camden is prone to see flat FFO per share till 2025, adopted by a rebound in development post-2025, as soon as rents enhance because of a low provide, to round 5% per yr.

However one query stays.

What’s the money movement value?

Camden pays a 4.3% dividend yield which could be very effectively lined with a payout ratio of simply 59%. The corporate has a 5-year dividend development CAGR of 5.3% which is especially a results of steep will increase in 2021 and 2022 attributable to a booming Sunbelt rental market. Because the market softens, nonetheless, I count on no additional dividend development this yr and subsequent yr.

In search of Alpha

The inventory trades at 14x FFO which is truthful relative to Mid-America Residences (MAA) which commerce at 15x, however have increased high quality A-Class properties, and to BSR REIT which trades at 13x FOO, however focuses solely on Texan markets which can be prone to see probably the most new provide within the coming quarters.

The inventory trades at an implied cap charge of 6.5%, which is about 190 bps above the 10-year treasury yield. Whereas I take into account the unfold truthful, there’s definitely potential for upside if rates of interest and yields decline from as we speak’s ranges.

Particularly, I estimate {that a} drop within the 10-year yield to 4% would result in a 25% upside and correspond to a worth goal of $120 per share. The maths behind that is comparatively easy. Utilizing the implied cap charge formulation the place:

Implied cap charge = NOI / (market cap + internet debt)

we are able to change the implied cap charge and work out a corresponding change in market cap. My assumption in regards to the 10-year yield declining to 4% (and holding the unfold of 190-200 bps fixed) implies that the implied cap charge would decline to about 6%. Holding NOI fixed at roughly $900 Million per yr, as a result of we’re assuming little to no development over the following two years and holding internet debt fixed at $3.65 Billion, we are able to work out that the market cap will enhance by roughly 25%.

Dangers

The only largest threat to CPT’s money movement isn’t rising rates of interest, however slightly the uncertainty concerning rents, particularly in gentle of a excessive tenant turnover which tends to common 2-3 years for all house REITs. As (quick) lease contracts expire and tenants go away, CPT’s common lease is prone to mirror market lease fairly intently.

Furthermore, whereas rates of interest solely have a small impression on the REIT’s money movement, they do have an effect on the valuation and consequently inventory worth rather a lot. In consequence, an increase in rates of interest and even rates of interest staying elevated for longer than is now anticipated would most undoubtedly end in a decline within the inventory worth.

Backside Line

We have identified for some time that offer of recent A-Class house house within the Sunbelt would peak in 2024 and 2025. Now we’re beginning to see the impression of this within the type of rising vacancies and falling rents. In consequence, administration has decreased its steering and the overall consensus for FFO per share development has declined from 4-5% to zero. I count on Camden’s FFO per share to be flat till 2025, however to proceed to develop by 4-5% post-2025.

Whereas Camden can’t be thought of a smoking deal at an implied cap charge of 6.5%, I do like its excessive credit standing, comfortably dividend and potential for upside if rates of interest decline. Camden is, in essence, a comparatively secure method to play rates of interest whereas incomes a strong yield. Subsequently I reiterate my BUY score right here at $95 per share.