tadamichi

Introduction

Buyers looking for earnings over the previous couple of a long time have had a restricted toolbox to work with. Dividend yields on U.S. equities have averaged lower than 2% over the previous 20 years, whereas yields on 10-year U.S. Treasuries have averaged lower than 3%.

Two massive levers that may be pulled within the seek for larger yields are length threat and credit score threat. The better the length and/or credit score threat an investor is prepared to imagine, the upper the yields needs to be.

After all, since mid-2022 the yield curve has been inverted, leading to a comparatively uncommon scenario the place rising length threat has resulted in decrease yields.

However is extending length and/or credit score threat the optimum strategy to generate larger earnings? Whereas there are market environments that certainly favor extending length or taking up better credit score threat, there are drawbacks as effectively.

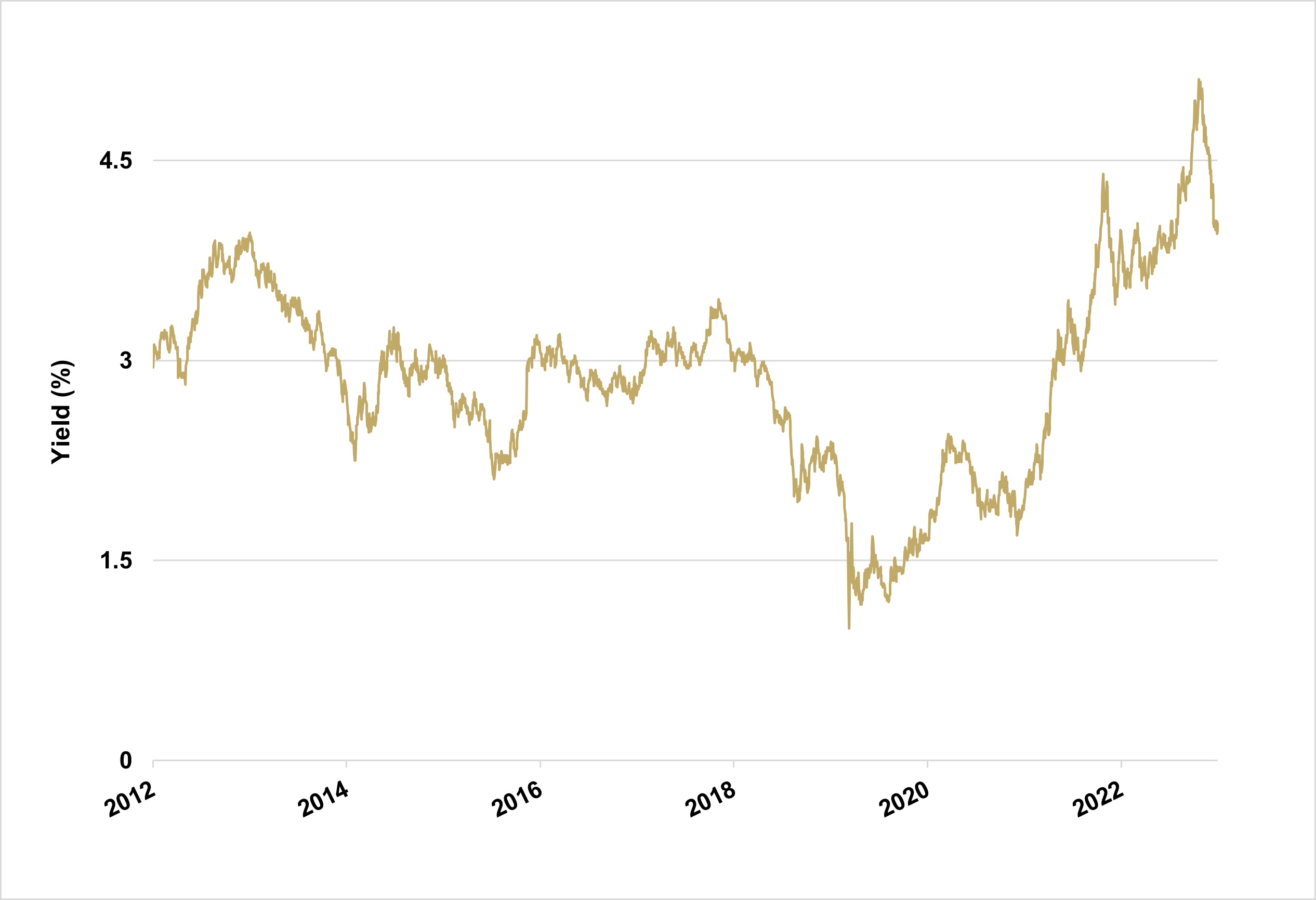

Let’s begin with length threat by taking a look at lengthy length (30-year) U.S. Treasury bonds. Determine 1 exhibits the yield on 30-year U.S. Treasury bonds for the ten years ended 2023. As of January 2024, the yield is about 4%, and has averaged 2.87% for the total interval.

Determine 1

Regardless of the big enhance in yields over the previous two years, the 30-year Treasury yield nonetheless solely hovers round 4%. That’s a fairly modest reward when contemplating the quantity of length threat the investor should assume.

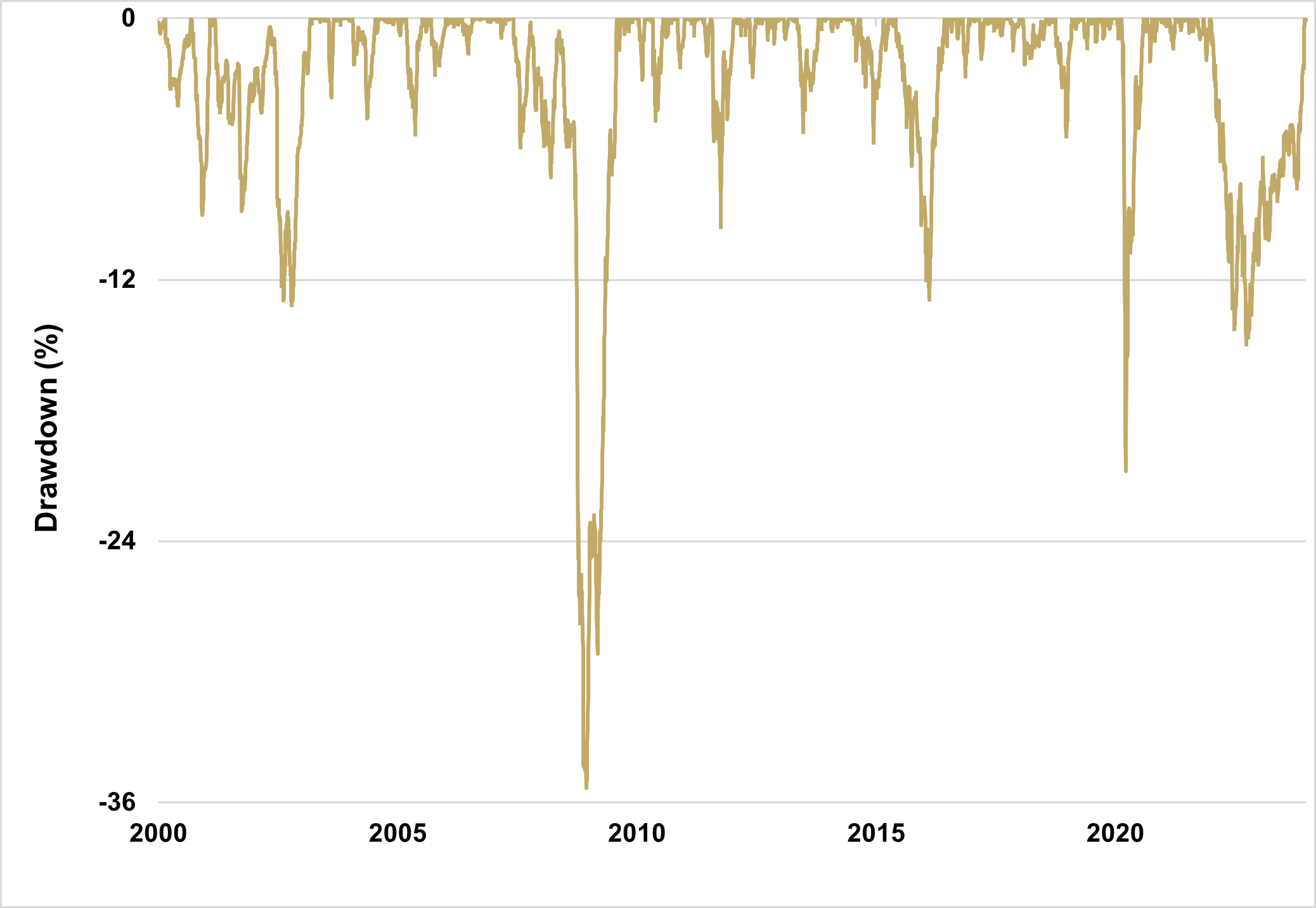

The ICE U.S. Treasury 20+ Years Bond Index has a length of about 17 years, which means {that a} 1% transfer in rates of interest implies a 17% change in worth. Actually, over the previous decade, long-term U.S. Treasury bonds have been almost as unstable because the S&P 500 Index with a bigger most drawdown of almost 50%.

Turning to credit score, company bonds with credit score scores beneath funding grade (excessive yield bonds), take pleasure in larger yields than lengthy length treasuries. However the credit score threat related to excessive yield bonds can rear its ugly head in dramatic vogue, significantly throughout recessionary durations.

Throughout the International Monetary Disaster, the Bloomberg U.S. Company Excessive Yield index endured a 36% drawdown (see Determine 2).

Determine 2

Throughout recessionary durations, companies with low credit score scores might battle to service their debt or roll over their debt because it matures. That is very true if recessionary durations are mixed with larger rates of interest.

It’s this financing stress which causes the yield spreads versus Treasuries to widen throughout recessions, leading to drawdowns for prime yield buyers.

At the moment, income-seeking buyers have extra options. With the modernization of the regulatory framework relating to derivatives similar to choices inside ETFs, new instruments will be utilized to generate important ranges of earnings with out taking up elevated length or credit score threat.

Introducing the Simplify Enhanced Earnings ETF (HIGH)

HIGH is designed to supply a excessive degree of month-to-month earnings with out taking up important length or credit score threat. It does this by combining short-term U.S. Treasury Payments with a risk-managed choices promoting technique.

The HIGH Funding Course of

The funding course of begins by investing almost all of HIGH’s belongings in short-term U.S. Treasury Payments. The T-Payments present security, stability, and a base degree of earnings.

As of January 2024, T-Payments are yielding over 5%. Whereas T-Payments haven’t any alternative for capital appreciation, they at the moment yield 25% greater than 30-year Treasury bonds, all whereas assuming zero rate of interest threat.

Subsequent, HIGH employs a risk-managed choices promoting technique to supply extra earnings above that of T-Payments. This choices technique comes within the type of writing a diversified basket of credit score spreads.

Credit score Unfold Fundamentals

A credit score unfold is when the investor sells an out-of-the-money (OTM) possibility after which buys a good additional OTM possibility. Each choices are of equivalent portions and have the identical expiration date.

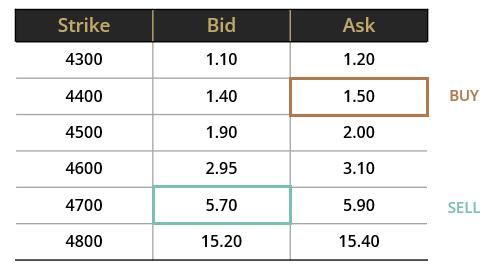

Determine 3 exhibits a hypothetical put possibility credit score unfold for an asset with a present worth of about $4900. The investor may promote an OTM put possibility with a strike of 4700, which might lead to proceeds of $5.70.

Subsequent, the investor buys a put possibility even additional OTM, say, at 4400, leading to a money outlay of $1.50. On this instance, the online proceeds of those two trades are +$4.20, which is credited to the investor’s account – therefore the identify “credit spread”.

Determine 3

Why would the investor promote a credit score unfold as a substitute of simply promoting the put possibility? Doesn’t shopping for the additional OTM possibility scale back the profitability of the commerce?

Shopping for the put possibility controls the danger of the commerce. It units a “floor” beneath which the investor is protected within the occasion the asset worth drops beneath the strike worth of the lengthy possibility. For the reason that additional OTM possibility is less expensive than the choice that’s being offered, it’s a cheap type of insurance coverage.

Ideally, the choices all expire out-of-the-money. In that case, your complete internet proceeds of the unfold turn out to be the investor’s revenue.

Managing Threat

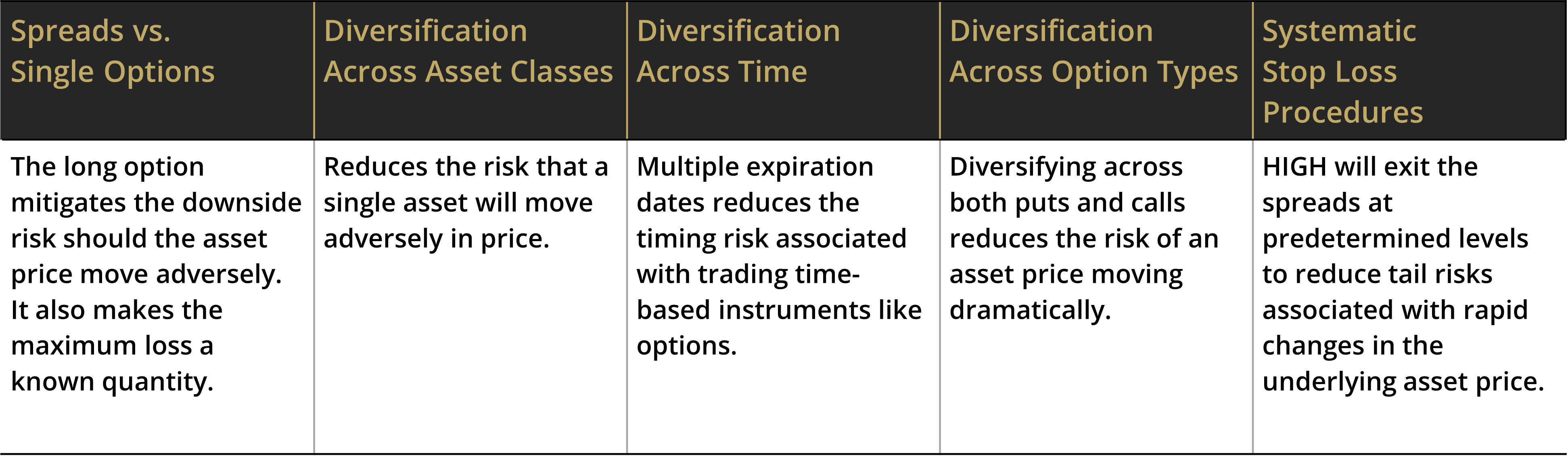

Except for delivering enticing earnings, a further purpose of the fund is to keep up low ranges of volatility and drawdowns. HIGH employs quite a lot of methods to handle threat, as proven in Determine 4.

Determine 4

The first threat administration device is to promote spreads as a substitute of single choices. This limits the utmost potential loss for the commerce within the occasion of an antagonistic transfer in opposition to the underlier.

Diversification is one other key driver of HIGH’s threat administration. HIGH will promote credit score spreads on a wide range of underlying devices, together with fairness ETFs, mounted earnings ETFs, commodity ETFs, and even particular person shares. By diversifying throughout a number of underlying devices, the general threat of the technique is diminished.

A second layer of diversification will be gained by participating in each put spreads in addition to name spreads. Most of the time, on the fairness aspect, HIGH shall be biased in direction of put spreads for 2 causes:

(1) for a similar moneyness, put spreads often lead to a better revenue and (2) shares go up barely extra usually than they go down, making put spreads the upper share play.

On the mounted earnings aspect, HIGH will usually have interaction in name spreads along with put spreads, and generally each on the identical time.

The third degree of diversification is diversifying throughout time. HIGH will usually promote 2-week spreads, however on a rolling 1-week foundation. It will scale back a number of the timing threat inherent in devices that carry an expiration date.

Lastly, draw back dangers are additionally managed through a stop-loss system that closes positions at preset underlier ranges. This threat mitigation method kicks in manner earlier than the lengthy put or name are near being on the cash, considerably slicing the doable loss for the technique.

Portfolio Implementation

Changing present mounted earnings holdings with HIGH will probably scale back length, scale back credit score threat, and enhance earnings. It shouldn’t be utilized by buyers who want to prolong length or credit score threat.

Buyers who search to keep up their length and credit score publicity, however want to enhance their yield, can take into account changing a few of their money publicity with HIGH. It will, nevertheless, increase their portfolio’s general degree of volatility.

Abstract

The normal playbook of extending length or reducing credit score high quality in the hunt for yield has its limitations. Not solely does extending length not add a lot yield, it comes with equity-like volatility and drawdown threat.

Equally, excessive yield bonds provide extra enticing yields, however on the expense of excessive drawdown threat, particularly throughout financial contractions.

Latest regulatory readability round derivatives has opened the door for options-based earnings methods like HIGH. By following a risk-managed credit score unfold technique, alongside investing in T-bills, HIGH has the potential to generate enticing yields whereas sustaining minimal publicity to length and credit score threat.

Glossary:

Length: A measure of the sensitivity of an asset worth to actions in yields.

Moneyness: Describes the intrinsic worth of an possibility’s premium available in the market. A contract is both “in the money”, “out of the money”, or “at the money”. A name possibility is claimed to be “in the money” when the long run contract worth is above the strike worth. A name possibility is “out of the money” when the long run contract worth is beneath the strike worth.

Choice: An possibility is a contract that offers the client the correct to both purchase (within the case of a name possibility) or promote (within the case of a put possibility) an underlying asset at a pre-determined worth (“strike”) by a selected date (“expiry”). An “outright” is one other identify for a single possibility leg. A “spread” is when choices are purchased at one strike and an equal quantity of choices are offered at a distinct strike, all on the identical expiry.

Out-of-the-Cash: An possibility has no intrinsic worth, solely extrinsic or time worth.

Buyers ought to fastidiously take into account the funding aims, dangers, costs, and bills of Change Traded Funds (ETFs) earlier than investing. To acquire an ETF’s prospectus containing this and different necessary info, please name (855) 772-8488, or go to SimplifyETFs.com. Please learn the prospectus fastidiously earlier than you make investments.

An funding within the fund includes threat, together with doable lack of principal.

The fund is actively-managed is topic to the danger that the technique might not produce the supposed outcomes. The fund is new and has a restricted working historical past to judge. The Fund invests in ETFs (Change-Traded Funds) and entails larger bills than if invested into the underlying ETF instantly. The decrease the credit score high quality, the extra unstable efficiency shall be. When junk bonds dump, the lowest-rated bonds are usually hit hardest often known as blow up threat. Likewise, the riskiest bonds usually rise quickest in a bull market nevertheless these investments that do not have a credit standing are usually essentially the most unstable, laborious to cost and the least liquid.

Using spinoff devices includes dangers completely different from, or probably better than, the dangers related to investing instantly in securities and different conventional investments. These dangers embody (i) the danger that the counterparty to a spinoff transaction might not fulfill its contractual obligations; (ii) threat of mispricing or improper valuation; and (iii) the danger that modifications within the worth of the spinoff might not correlate completely with the underlying asset, fee, or index. By-product costs are extremely unstable and should fluctuate considerably throughout a brief time period. Using leverage by the Fund, similar to borrowing cash to buy securities or using choices, will trigger the Fund to incur extra bills and amplify the Fund’s beneficial properties or losses. The Fund’s funding in mounted earnings securities is topic to credit score threat (the debtor might default) and prepayment threat (an obligation paid early) which might trigger its share worth and complete return to be diminished. Sometimes, as rates of interest rise the worth of bond costs will decline and the fund might lose worth.

Whereas the choice overlay is meant to enhance the Fund’s efficiency, there isn’t any assure that it’ll achieve this. Using an possibility overlay technique includes the danger that as the client of a put or name possibility, the Fund dangers dropping your complete premium invested within the possibility if the Fund doesn’t train the choice. Additionally, securities and choices traded in over-the-counter markets might commerce much less ceaselessly and in restricted volumes and thus exhibit extra volatility and liquidity threat.

Diversification doesn’t guarantee a revenue or assure in opposition to a loss.

Simplify ETFs are distributed by Foreside Monetary Providers, LLC. Simplify and Foreside are usually not associated.

Editor’s Notice: The abstract bullets for this text had been chosen by Looking for Alpha editors.