eclipse_images

Funding Thesis

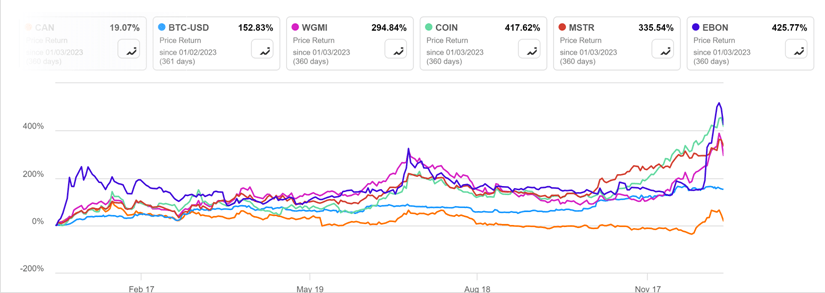

In concept, Canaan Inc. (NASDAQ:CAN) ought to be an incredible buying and selling inventory to play Bitcoin’s bull cycle as a result of the corporate is likely one of the high three producers of bitcoin mining machines on the planet (the opposite two are Bitmain and MicroBT) and its inventory ought to correlate intently with the Bitcoin value. Nonetheless, the fact was sadly fairly the alternative: Canaan had considerably underperformed and basically decoupled from the complete Bitcoin associated inventory universe in 2023. Satirically, its a lot smaller and weaker business peer, Ebang Worldwide Holdings Inc. (EBON), had an unbelievably stellar 12 months with its top off 425% in 2023, handily beating not solely Canaan however Bitcoin, Valkyrie Bitcoin Miners ETF (WGMI), the crypto change Coinbase (COIN) and the Bitcoin hodler MicroStrategy (MSTR) (see chart under).

In search of Alpha.

Given the upcoming tailwind in 2024 and the continued restoration of the business fundamentals, this disconnection between Canaan and Bitcoin value may very well be reversed in full power probably as early as January 2024. Really, we now have already seen some encouraging indicators of the recoupling momentum between the 2 in December 2023, throughout which Canaan inventory lastly wakened and rose 44%.

Our base case situation for Canaan in 2024 is that the correlation between its inventory value and Bitcoin is reestablished with the present vast efficiency hole lastly closed. Throughout 2023, Canaan lagged Bitcoin by roughly 135 proportion factors and an eventual value convergence of the 2 would suggest a goal value of Canaan at $4.95, i.e. 2.6x of the shut value of $1.94 on January 12, 2024.

We additionally in contrast Canaan’s valuation with its Bitcoin-related friends through the use of Value to Gross sales ratio. The desk under summarizes the market capitalization, 2024 gross sales forecast, and P/S multiples of its friends with a market capitalization of lower than $1 billion. Not surprisingly, Canaan has the bottom P/S ratio of 1.5x whereas the ratio of its friends was in a spread of two.5x to six.0x. If Canaan have been to commerce in that vary, the worth ought to be between $3.24 and $7.76. If Bitcoin continues its bull run in 2024, Canaan inventory might have additional upsides assuming it tracks intently with the Bitcoin value through the 12 months. It’s price noting that Canaan as soon as traded above $36 per share again in March 2021 when its correlation with Bitcoin was nonetheless on.

|

Market Cap * |

2024 Gross sales** |

Value/Gross sales |

|

|

Iris Vitality Restricted (IREN) |

$391 MM |

$162 MM |

2.5x |

|

HIVE Digital Applied sciences (HIVE) |

$336 MM |

$107 MM |

3.1x |

|

Cipher Mining (CIFR) |

$838 MM |

$145 MM |

5.8x |

|

Bitfarms (BITF) |

$808 MM |

$263 MM |

3.1x |

|

Canaan |

$332 MM |

$221 MM |

1.5x |

*Market capitalization as of January 12, 2024.

**Based mostly on In search of Alpha estimates.

Supply: In search of Alpha.

For individuals who missed the Bitcoin rally in 2023, Canaan, on the present degree, may very well be catchup play throughout 2024. Nonetheless, please remember that the commerce of being lengthy Canaan may be very speculative and its inventory value may very well be extraordinarily risky regardless of all of the constructive business catalysts. When it comes to risk-reward profile, with the upside goal at $4.95, Canaan’s draw back ground may very well be $1.13 which is its all-time low since its IPO in November 2019.

Canaan Hibernation

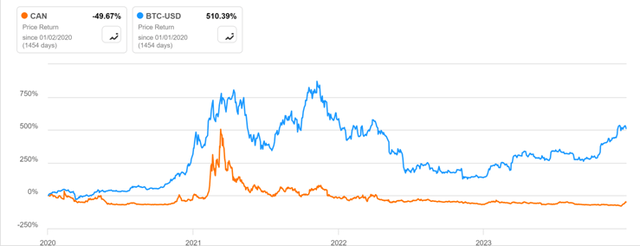

Theoretically the inventory value of Canaan, one of many largest crypto mining rig producers on the planet, ought to observe intently with Bitcoin value as a result of the upper the Bitcoin value, the upper the typical promoting value of the Bitcoin mining rigs, and the upper the inventory value of Canaan. Additionally, Canaan ought to profit from some shortage worth as among the many world’s high three Bitcoin mining rig producers, it’s the solely publicly listed one. The truth, nonetheless, could not be additional away from the idea over the previous 4 years (see chart under).

In search of Alpha.

Canaan was monitoring intently with Bitcoin in early 2020 however that correlation broke down in the course of Might 2020 primarily as a result of expiration of its IPO lockup interval and a unfavorable on-line analysis report. Through the first wave of a robust Bitcoin value rally in early 2021, the correlation was considerably re-established and Canaan inventory value hit a historic excessive in late March 2021. Since then, a persistent decoupling kicked in and Canaan inventory value basically flatlined right into a deep hibernation, now not reacting to any Bitcoin value motion in any respect.

One potential rationalization for this lengthy hibernation is the China issue. The background was that the US Congress handed the

Holding Foreign Companies Accountable Act (HFCA) in December 2020, and the SEC issued implementing rules in March 2021. Underneath the brand new regulation, if the Public Firm Accounting Oversight Board (PCAOB) certifies it has not been in a position to evaluation an organization’s audits for 3 consecutive years, the SEC should delist it. Impulsively, all of the US-listed Chinese language ADRs may very well be probably delisted three years from March 2021. Invesco Golden Dragon China ETF (PGJ) declined 42% throughout 2021 and Canaan was additionally dragged down 23% even if it generated traditionally excessive income with Bitcoin up 48% that 12 months (see chart under).

In search of Alpha.

Quick ahead to 2023, Bitcoin ended the 12 months up 155% whereas WGMI rallied 295% (see chart under). Per this media article, the outperformance of WGMI may very well be as a result of interaction of rising costs and excessive quick curiosity of the underlying shares, or a probable quick squeeze.

In search of Alpha.

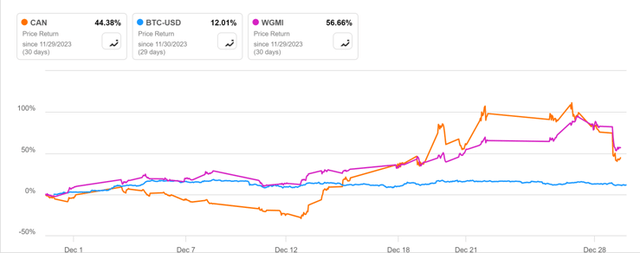

Canaan, then again, was up solely 19% throughout 2023, even decrease than the 25% return of S&P 500 Index (SPY). That mentioned, we did see some silver lining – Canaan appeared to immediately get up from its lengthy hibernation in December and bounced 44% throughout that month alone whereas Bitcoin was solely up 12%. At one level in December, Canaan even outperformed WGMI earlier than giving again a part of the acquire on the 12 months’s finish (see chart under). If this re-coupling momentum continues into 2024, Canaan may very well be nicely positioned not solely to shut the efficiency hole with Bitcoin but in addition to additional profit from the probably begin of a brand new Bitcoin bull cycle.

In search of Alpha.

Canaan Fundamentals

Given the extremely cyclical nature of Bitcoin mining enterprise, Canaan’s administration has carried out a fairly good job navigating the corporate by means of the business down cycles and ongoing regulatory modifications. Beneath are our key observations.

1) Canaan’s high line and revenue margin have been dictated by the Bitcoin value.

Canaan’s income was largely decided by the overall computing energy bought and their common promoting value (ASP). ASP was pushed by three elements, the Bitcoin value, anticipated mining returns, and the efficiency of the mining rigs. Increased Bitcoin costs and anticipated mining returns sometimes will result in increased demand for mining rigs and in flip, drive up the ASP. In a down cycle, these two elements will depress the demand and ASP of mining rigs. The efficiency of the mining rigs is a crucial issue, however not as decisive as the opposite two, as a result of a mining rig with higher options might generally have a decrease ASP than an older model if it was launched in much less optimum time throughout a downcycle or proper after a pointy Bitcoin value correction.

Because it employs a fabless mannequin, Canaan’s value of revenues is primarily pushed by the uncooked supplies and the price of contract manufacturing. Sometimes, a newly launched mining machine mannequin tends to have increased manufacturing prices per Thash early in its product life on account of preliminary setup prices which is able to degree down because the manufacturing course of turns into mature and extra optimized over the next years. Given this, Canaan’s gross margin is due to this fact extra dictated by ASP (in the end by Bitcoin value) than the manufacturing prices per Thash. So long as ASP holds fixed or developments increased, the gross margin will enhance over time. Nonetheless, if ASP falls considerably in a downturn, gross margin will undergo severely as each the manufacturing prices and stock write-down can add as much as be increased than ASP.

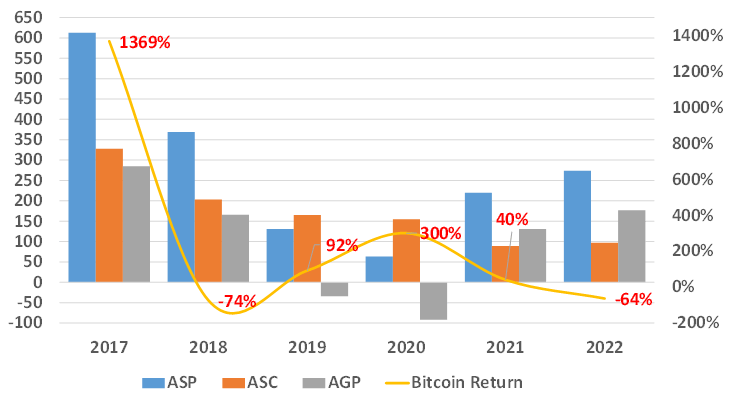

Canaan went public in 2019, so we solely have its annual financials up till 2017. Between 2017 and 2023, Canaan skilled two Bitcoin cycles and Bitcoin hit its peak value of every cycle in 2017 and 2021 respectively (see chart under). 2024 is probably going 12 months 2 of the third cycle Canaan is navigating by means of.

Bitcoin Value Cycles

Yahoo Finance.

Within the following chart, we in contrast Canaan’s ASP, common promoting value per Thash (ASC) and common gross revenue per Thash (AGP) with yearly return of Bitcoin value in order to evaluate the connection between the Bitcoin cycle and the corporate’s revenue cycle. It is extremely clear that the Bitcoin value had a direct and important impression on Canaan’s gross margin. Additionally, Bitcoin cycle led Canaan’s revenue cycle by roughly one 12 months, most probably as a result of manufacturing and supply course of for the mining rigs. For instance, Bitcoin value tanked 74% in 2018 however Canaan nonetheless generated 166 Yuan gross revenue per Thash with a forty five% gross margin per Thash that 12 months. In 2019 the corporate began to really feel the delayed unfavorable impression of Bitcoin selloff and reported 34 Yuan gross loss per Thash. Satirically, Bitcoin was already on its means up through the interval. Canaan additionally reported a gross loss per Thash in 2020, however that was primarily on account of COVID 19 disruption and shouldn’t be counted as a part of the cycle.

Canaan’s Gross Margin vs Bitcoin Return

Firm filings.

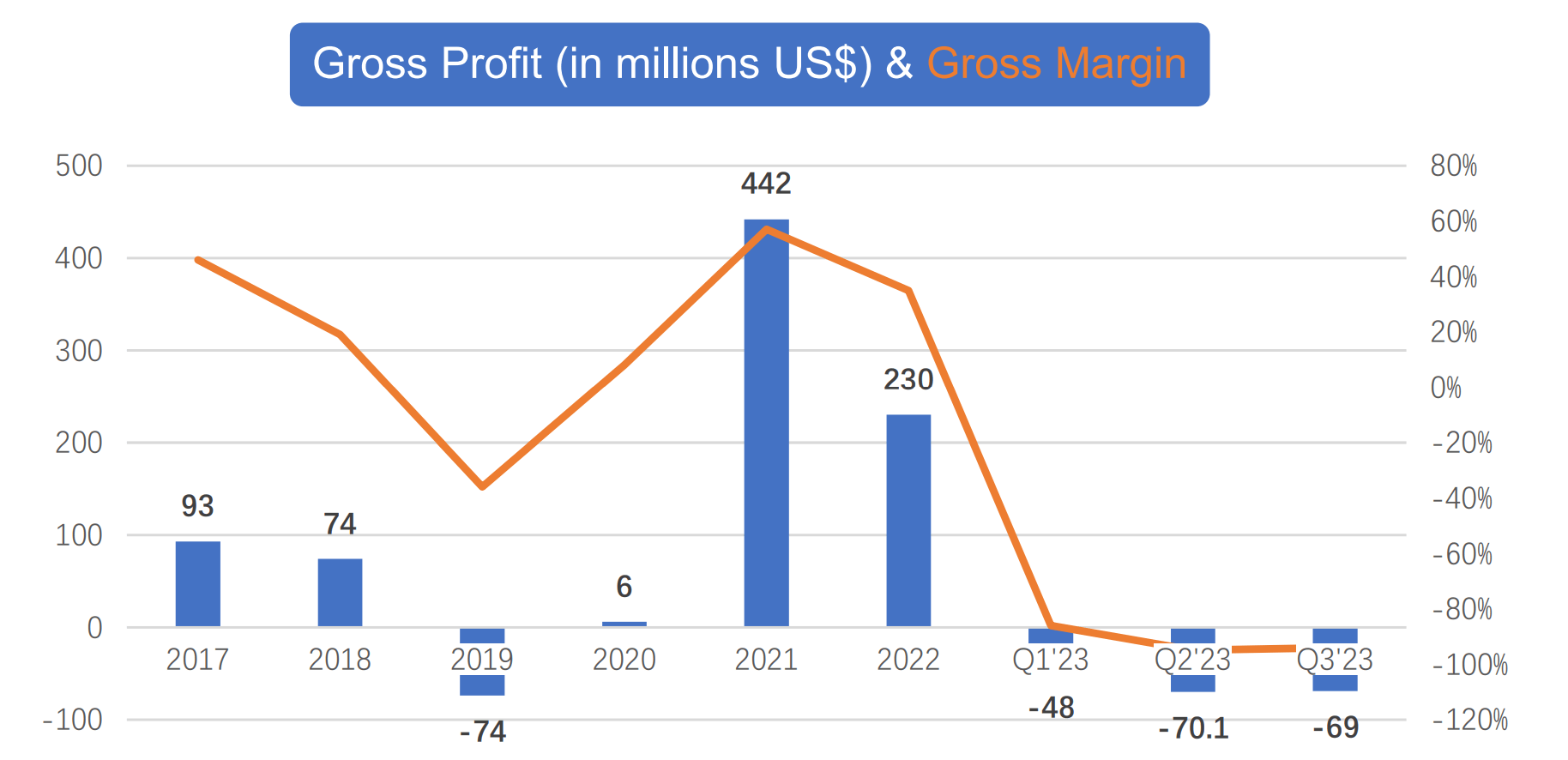

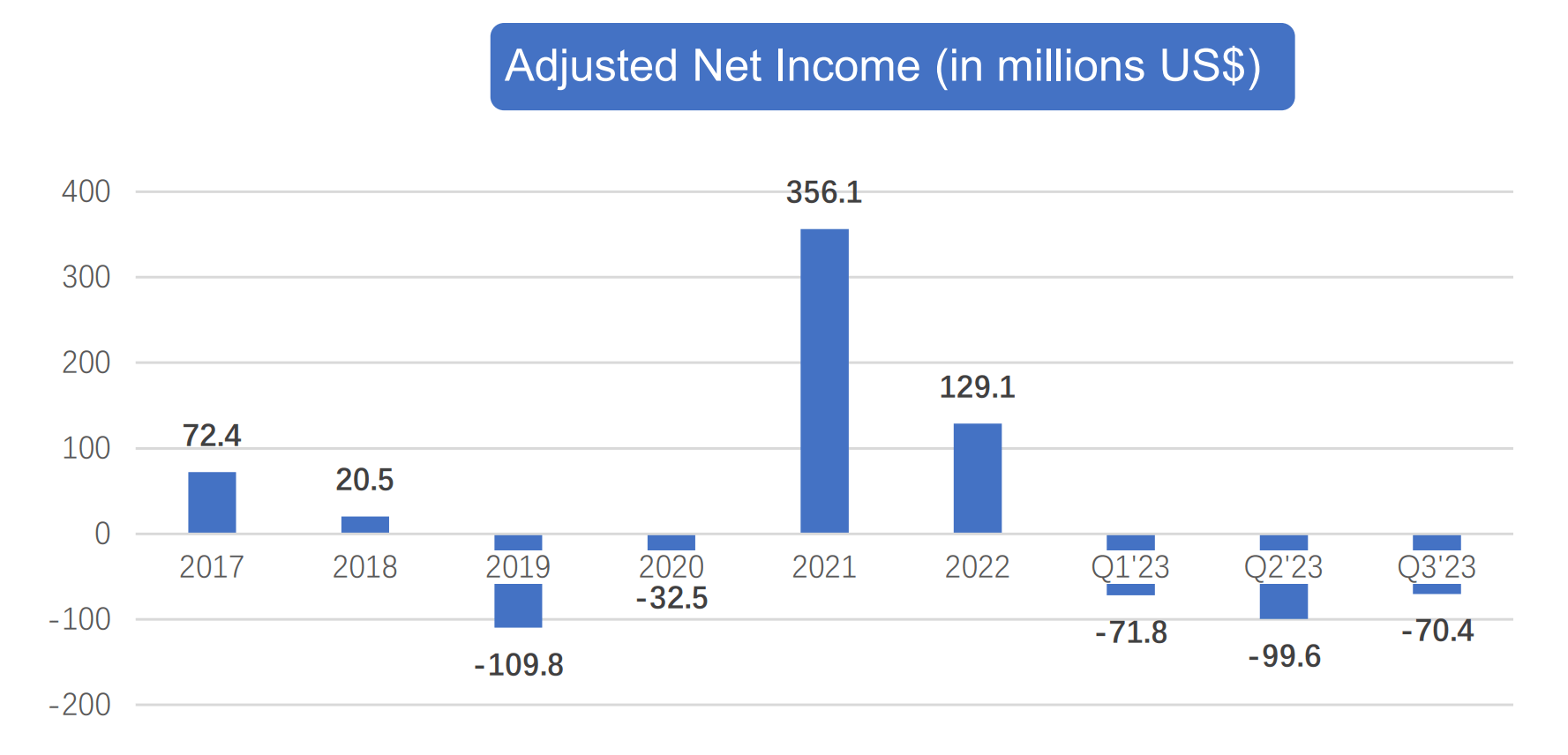

Through the second cycle, Bitcoin value nosedived 64% in 2022, however Canaan didn’t obtain the shockwave till 2023 and reported a gross lack of $167 million and web lack of $242 million respectively within the first 9 months, the very best in previous six years (see charts under). Nonetheless, with Bitcoin value up 155% in 2023 and certain extra rally in 2024. Given the place we’re on this cycle, we might anticipate Canaan to swing to a gross revenue and web revenue once more over the following two years.

Firm filings. |

Firm filings. |

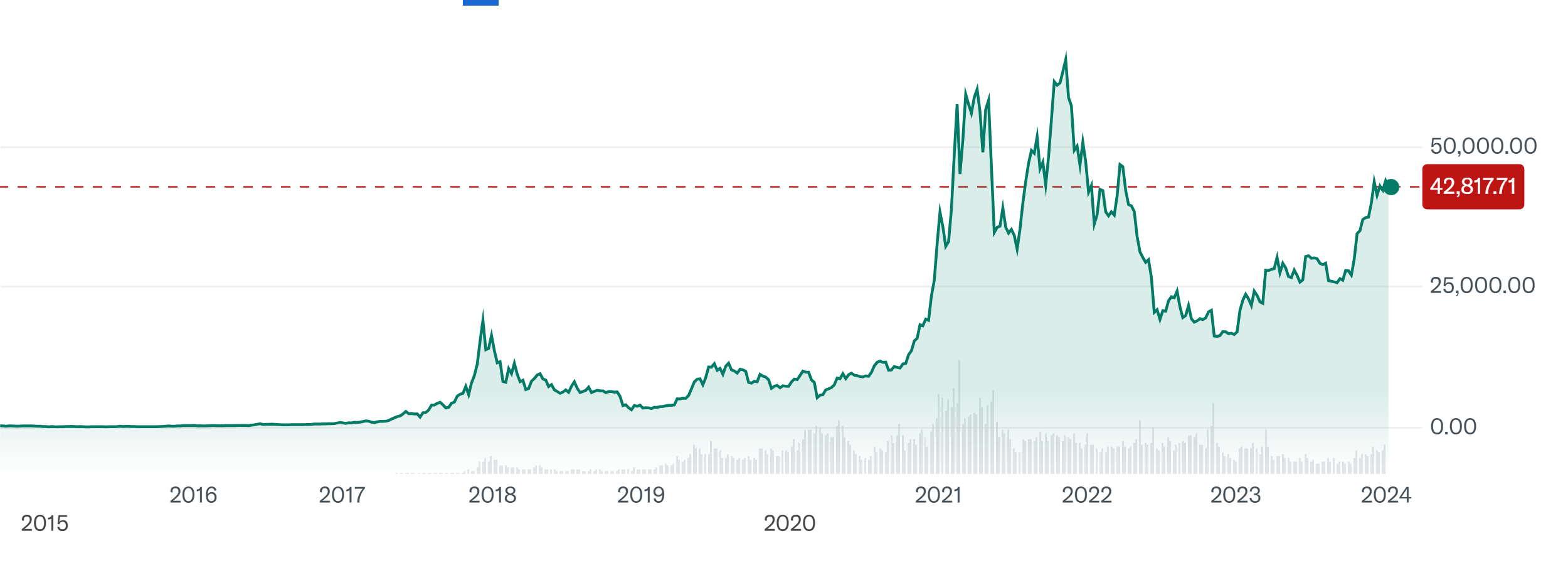

One constructive improvement within the present cycle is that Canaan’s core merchandise, together with Avalon A1346, A1366 and A1466 mining rigs have all been in a position to generate revenue on the present Bitcoin value ($42,313 as of January 14, 2024) primarily based on the estimates of whattomine.com (see desk under). These three fashions ought to be the primary sources of Canaan’s revenues in 2024 earlier than a brand new mannequin is launched through the 12 months.

|

Mining Rig |

Hash Fee/Vitality Consumption |

Revenue/Loss* |

Value** |

|

A1346 |

110.00 Th/s @ 3300W |

$1.24/Per Day/Unit |

$1,729 |

|

A1366 |

130.00 Th/s @ 3250W |

$3.20/Per Day/Unit |

$3,049 |

|

A1466 |

150.00 Th/s @ 3230W |

$4.92/Per Day/Unit |

$3,399 |

*https://www.whattomine.com/

**https://www.cryptominerbros.com/

This revenue development was additional verified by two latest product orders. Per the company press release on January 3, 2024, Canaan had secured two main buy orders late December 2023, embody 16,700 A1466 mining rigs from Cipher’s JV entities and 1,100 A1346 mining rigs from Stronghold who additionally had the choice to buy an extra 2,500 A1466 mining rigs. Based mostly on the promoting value within the above desk, these orders are price roughly $59 million or $67 million, if together with Stronghold’s buy possibility. To maintain these orders in perspective, Canaan’s income in 3Q 2023 was solely $33 million.

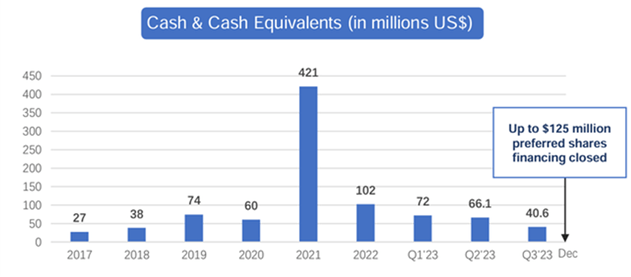

2) The stability sheet had been prudently managed.

Canaan’s stability sheet was debt free as of 3Q 2023. Because the firm incurred web loss in every of the primary three quarters in 2023, its money on the stability sheet had been depleted to solely $41 million. Canaan administration had preemptively addressed the problem throughout 3Q 2023 with a $125 million convertible most well-liked share deal. Moreover, the Firm entered into an At Market Issuance Sales Agreement with B. Riley Securities because the gross sales agent, underneath which Canaan might increase as much as $68 million by promoting its strange shares. These two offers definitely bolstered the liquidity place of the corporate through the business downturn.

Firm filings.

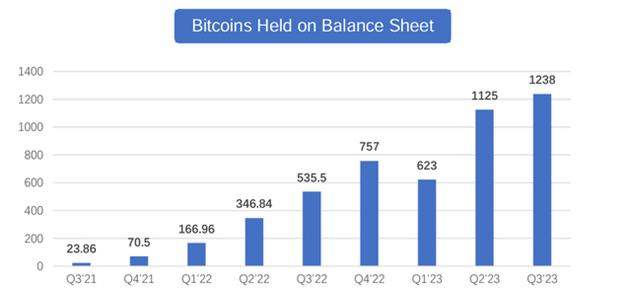

Canaan’s stability sheet was additionally supported by its Bitcoin holdings which had elevated steadily over the previous two years for the reason that firm began its self-mining enterprise. By the top of 3Q 2023, the corporate held 860 Bitcoins (excluding 378 prospects’ deposits) on its stability sheet which on the present Bitcoin market value are price over $36 million (see charts under).

Firm filings.

3) R&D dedication remained intact.

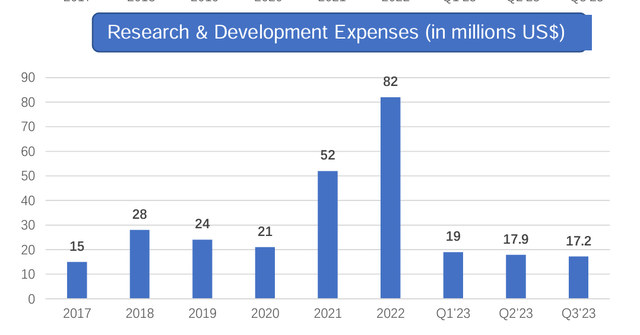

Canaan’s R&D group has near 300 members, or over 50% of the corporate’s whole staff. The group is split into two teams, one for growing the mining machines and the opposite for its AI merchandise. Regardless of the business downtown, the corporate had dedicated to its R&D funding. Through the first 9 months of 2023, the corporate spent over $54 million in R&D, on par with the extent of full 12 months 2021 when the business was at its peak of the final Bitcoin cycle.

Firm filings.

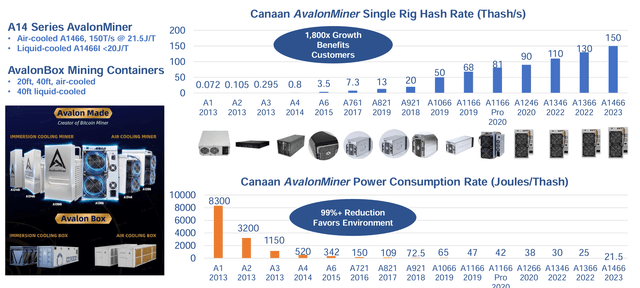

This constant R&D technique by means of the business cycles definitely paid off for Canaan as evidenced by its mining rig’s hash price and power effectivity enhancements over the past 10 years (see chart under).

Firm filings.

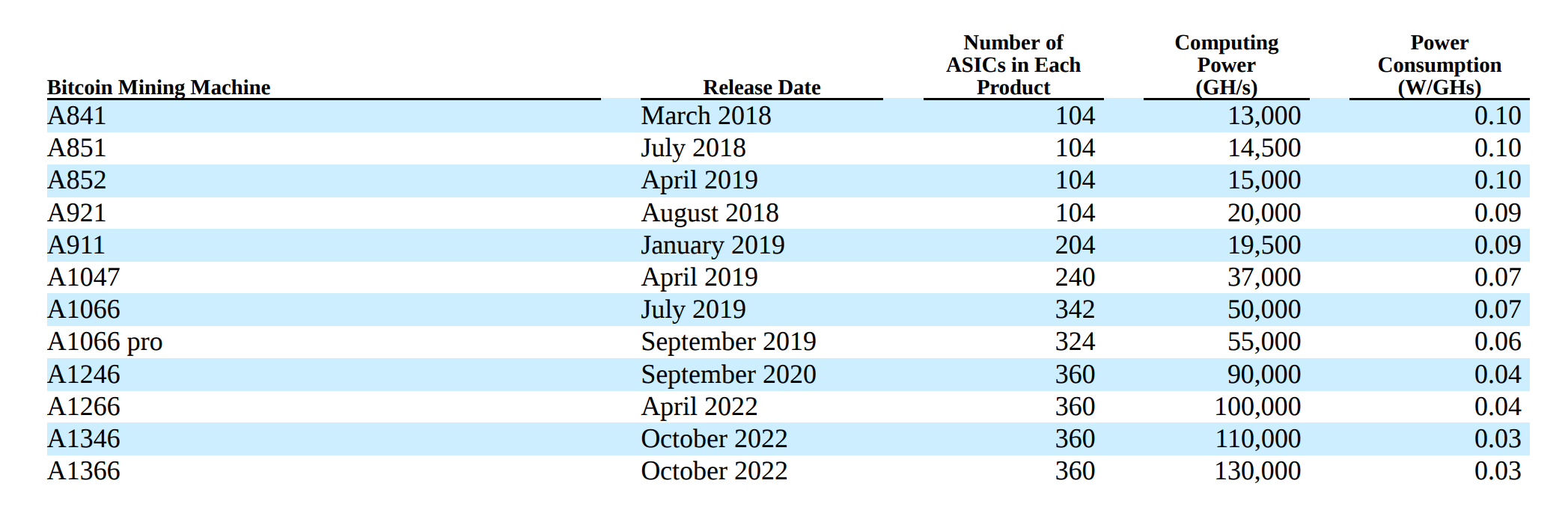

Over the previous six 12 months, Canaan sometimes launched three new fashions per 12 months (see desk under) besides in 2020/2021 (COVID disruption) and 2023 (business downtown). This tempo of latest product launch, supported by R&D funding, is crucial for the corporate to stay aggressive towards the opposite two main business gamers and to additionally keep nicely ready for the following business upcycle which most probably can be round nook in 2024.

Firm filings.

Key Favorable Catalysts

In 2024, Canaan might probably profit from a number of business and firm particular catalysts which are organising Bitcoin for a continued upward trajectory. The important thing business catalysts will most probably occur through the first 4 months of 2024, i.e. SEC approval of spot Bitcoin ETFs and Bitcoin halving.

1) January 10, 2024 – the SEC approval deadline of spot Bitcoin ETFs.

As anticipated, SEC accredited the spot Bitcoin ETFs by the January deadline. The overall market consensus is that the launch of those ETFs would have long-ranging constructive impression for Bitcoin value for 2 causes. Firstly, the shopping for energy of those new ETFs will create incremental and chronic demand for Bitcoin. Secondly, the brand new ETFs will basically change the construction of Bitcoin buyers base as they make the Bitcoin, as an asset class, instantly extra accessible to the institutional buyers. In a submit on The Pomp Letter, Matt Hougan, CIO of Bitwise Investments, analyzed the potential value impression of the brand new Bitcoin ETFs by trying on the gold ETF launched again in November 2004:

The value of gold rose for 9 straight calendar years after the primary gold ETF launched within the U.S. on November 18, 2004. It’s the longest streak of consecutive constructive years in gold’s recorded historical past.

There have been many causes for this historic run other than the ETF launch. However the ETF performed an enormous position. Over this time interval, gold ETFs attracted $89 billion in inflows worldwide, vacuuming up 2,667 metric tons of gold. That is 86 million ounces-more gold than the international locations of China, Switzerland, and Russia maintain mixed.

This basically altered the demand stability for gold. Based on the World Gold Council, investment-related demand for gold rose from 4% of whole demand in 2000 to 45% in 2009, “driven mainly by an increase in demand for ETF and related products.” Given gold’s rigid provide, this probably contributed to rising costs.”

If history repeats itself, the price impacts of the new Bitcoin ETFs will play out surely but gradually as it will take time for those ETFs to build up their AUM and to slowly push up Bitcoin price. Actually, the prices for both Bitcoin and related stocks all traded down right after the ETFs’ launch as the traders took profit by “promoting the information”, however, this short-term volatility shall not alter the long-term tailwind created by these new ETFs.

2) April 2024 – Bitcoin Halving.

The next halving event will likely happen in April 2024 which is expected to reduce the Bitcoin mining reward from 6.25 BTC to 3.125 BTC per block. The halving essentially will lead to a reduced supply of Bitcoin and historically has driven up the Bitcoin price as the demand remained constant or higher.

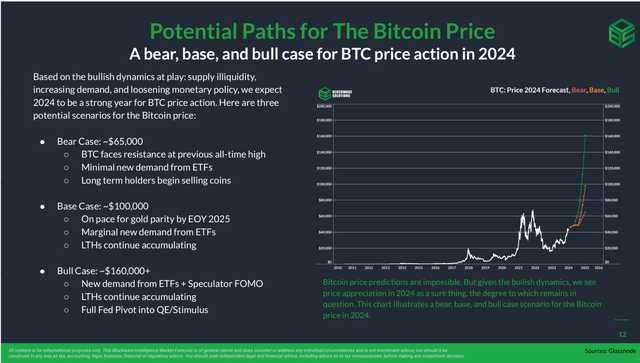

Present market expectation is that the halving and different constructive catalysts might make 2024 a 12 months of Bitcoin bull run. One of many analysis newsletters we intently observe is from Blockware Options, a number one mining rigs market. In its 2024 outlook, the bottom case goal for the Bitcoin value is $100,000 whereas the bear case is $65,000 (see screenshot under). Even in its bear case, the Bitcoin value will nonetheless be up greater than 50% from year-end 2023 which definitely bodes nicely for Canaan.

Blockware Solutions.

Besides these two industry developments, Canaan will potentially benefit from three company specific catalysts:

1) March 2024 – Earnings release.

Canaan will report its 4Q 2023 earnings likely in March 2024, in which the management should update their outlook on the company’s order book based on their observation in 1Q 2024. If Bitcoin indeed started a bull run in early 2024, both the average selling price of the mining rigs and the forward orders for Canaan’s products would rise significantly.

2) Independent funding of Canaan’s AI business.

In its 3Q 2023 earnings call, Canaan mentioned that it was going through an internal restructuring with the goal to clearly separate the mining machine business from its AI business. The two businesses will operate independently and potentially AI business will raise financing separately. This is exciting progress that the market might have totally missed. Just like in the US, AI frenzy swept China in 2023 as the institutional investors were rushing into the space and pushing up the valuation of AI projects. Per a Reuters report, one recent example is 01.AI, an AI startup launched by Lee Kai-fu (ex-Google China Chief and a venture capitalist) in July 2023 after a three-month incubation period, already hit a valuation of $1 billion early in November 2023. If Canaan’s AI business chose to raise fund independently, it would certainly benefit from this market trend and command a market valuation (hopefully higher) without being “tainted” by the highly cyclical Bitcoin mining business. If that is the case, the intrinsic value of Canaan could also be elevated based on the sum of parts valuation.

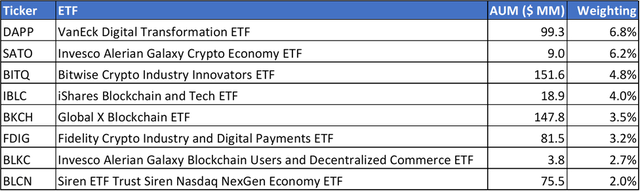

3) Extra ETF inclusion.

Per inventory ETF exposure tool of etfdb.com, Canaan is currently included in 31 ETFs, of which only 8 have Canaan within their top 15 holdings (see table below). It is also worth noting that the AUM of those ETFs is quite small with the largest one being $152 million.

etfdb.com.

By comparability, Riot Platforms (RIOT) is currently in 70 ETFs of which 12 have it within their top 15 holdings. Marathon Digital Holdings (MARA) is currently included 71 ETFs, of which 17 have it within their top 15 holdings. Besides the fact that they are included in more ETFs, they are also included in the ETFs with much larger AUM, e.g. Amplify Transformational Data Sharing ETF (BLOK) with $1.1 billion AUM and SPDR S&P Kensho New Economies Composite ETF (KOMP) with $1.9 billion AUM.

ETF inclusion will be a positive technical catalyst for Canaan and will most likely happen when the stock price of Canaan is on a rising trajectory in 2024. The marginal purchase from the Bitcoin themed ETFs could further amplify the upward momentum. As a catalyst, this one could be a long shot, but we do not want to rule out the odds of it happening in an industry upcycle in 2024.

Key Risks

1) Lack of investors’ interest in the approved spot Bitcoin ETFs. If the investors are not enthusiastic about the spot Bitcoin ETFs, there will not be sufficient support for Bitcoin price for a sustainable rally in 2024. Both Canaan’s stock price and business will suffer in this case.

2) Continued decoupling between Canaan stock and Bitcoin price. Investors could continue to shy away from Chinese ADRs, including Canaan. Under this scenario, Canaan stock could remain flatlined despite all the positive catalysts in 2024, e.g. approval of spot Bitcoin ETF, post halving Bitcoin price rally or improved financials of Canaan.

Conclusion

As one of many high three Bitcoin mining machine producers on the planet, Canaan is a good buying and selling inventory to play the potential bitcoin upcycle. Regardless of being visibly absent from the sturdy business restoration in 2023, the corporate is presently nicely poised for a bull run in 2024 given the sturdy lineup of constructive business catalysts, such because the launch of a number of spot Bitcoin ETFs and imminent halving occasion. On the present value, Canaan inventory gives an uneven risk-reward profile that may very well be achieved by merely closing the valuation hole with Bitcoin and different business friends. The important thing danger of being lengthy Canaan is the persistent decoupling between its inventory and the Bitcoin value.