John M Lund Photography Inc/DigitalVision via Getty Images

Investment case for preferred shares Canadian companies due for dividend resets over the next 6 months

I expect preferred shares of Canadian utilities and infrastructure companies to perform strongly over the next 6 to 12 months, as the Bank of Canada (BOC) will likely cut interest rates. Like in October of last year, the Fear Of Missing Out (FOMO) is likely for Canadian investors in preferreds. High interest rates provide a unique opportunity to invest in fixed dividend preferred shares that are due for a reset over the next 6 months and will pay much higher fixed dividends over the next five years. Low-risk business models, stable cash flows and solid dividend track records characterize Canadian utilities and infrastructure companies.

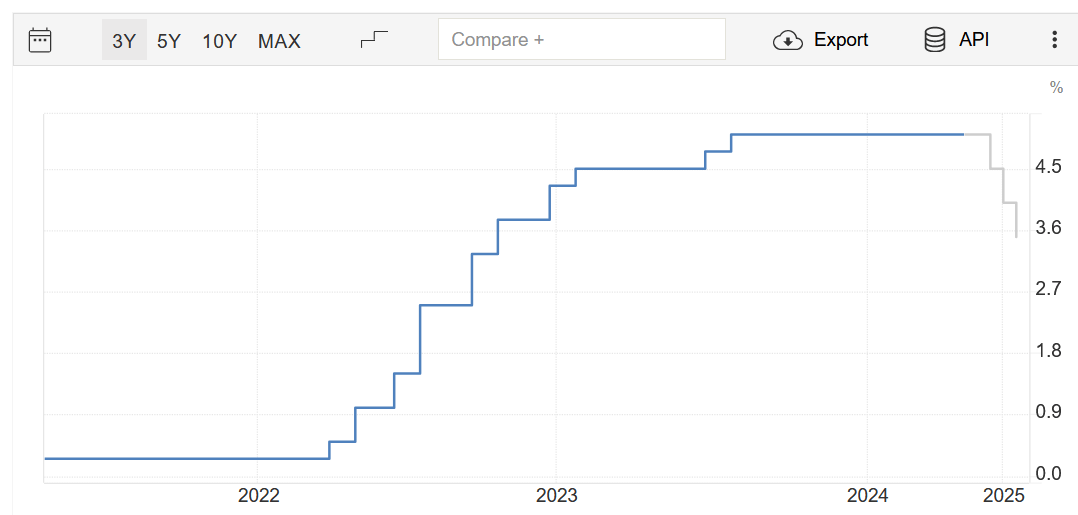

Economic developments point that BOC will start cutting interest rates soon

Weak economic growth and relatively low inflation support monetary easing in Canada. At the same time, the US economy and inflation signal that higher for longer rates are more likely.

According to the projections by Trading Economics, the BOC will cut rates this year twice, each time by 0.5%. There is a high probability that the first cut will be 0.25%. It is likely that the cuts will not be as dramatic as projected by Trading Economics. I believe that the BOC will cut key rates three times this year, 0.25% each time.

Trading Economics

If the first rate cut of 0.25% is implemented on June 5th or July 24th, the second on October 23rd and the last on December 11th, the key rate will decrease to 4.25%. More aggressive monetary easing may follow in 2025.

In these circumstances, the unique window of opportunities to invest in the preferred shares of low-risk Canadian utilities and infrastructure companies might close by the end of this year. As the markets often act based on sentiment ahead of the news, I believe there is a limited time left for investing in Canadian preferred shares. The list of preferred shares that we compiled consists of the stocks that will have their 5-year fixed yields reset over the next 6 months.

Timing

Assuming that the first rate cut in Canada will happen in June or July this year and another one will follow at the end of October, I split the fixed-rate preferred shares that are due for their rates to be reset over the next six months into two groups. While calculating the post-reset yield for the first group, I added to the fixed spread 5-year GOC yield minus 0.25%. I deducted 0.5% from the 5-year GOC yield for the second group.

Enbridge Inc. is a low-risk investment

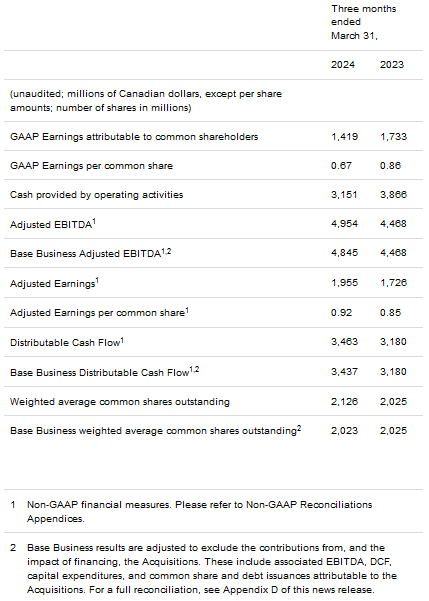

Solid Q1 2024 results

In its Q1 financial results, the company reported an 11% increase in EBITDA year over year (from $4.5 billion to $5 billion) and a 4% rise in DCF per share (from $1.57 to $1.63). At the same time, it reported a decrease in GAAP Earnings per share, which dropped by $0.19 from $0.86 in Q1 2023 to $0.67 in Q1 2024. This decrease resulted from non-operating factors. The company reiterated its guidance for 2024 and its medium-term outlook.

Enbridge News Release

While reporting the Q1 results, the company’s management underlined:

“Enbridge remains committed to delivering long-term shareholder returns supported by stable, diversified, utility-like earnings. We have a strong balance sheet and credible track record of returning capital to shareholders, with approximately $34 billion paid out through common dividends over the past five years and more than $40 billion expected to be returned over the next five years. Looking forward, we believe our disciplined approach to capital allocation and low-risk growth profile will support continued strong shareholder returns and position us as a first-choice investment opportunity” (all the figures are in CAD unless otherwise stated).

Strong Balance sheet and reliable dividends

The company has a BBB+ (or similar) rating from major rating agencies. Enbridge’s strong balance sheet is based on fixed-rate debt (only 5% of the total debt is floating rates). In addition, 80% of the company’s EBITDA is based on contracts with inflation protection, with 95% of the customers having investment-grade credit ratings. Enbridge completed Q1 with a debt-to-EBITDA ratio of 4.7x, which is in the target range of between 4.5x and 5.0x. The range indicates that the company’s business risk is somewhat higher than that of US Midstream companies but lower than that of utilities. It maintained a 60-70% payout range of Distributable Cash Flows (DCF).

Enbridge preferred shares have a strong upside potential even after the BOC rate cuts

Author analysis; Company data Author analysis; Company data

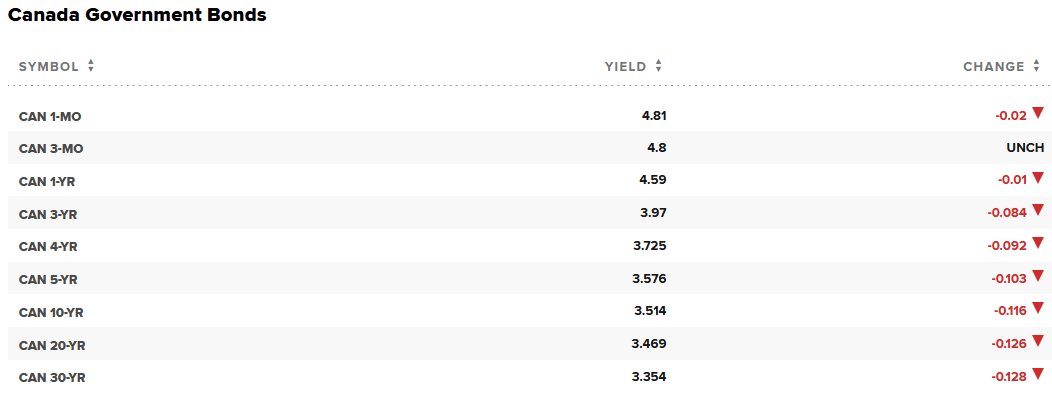

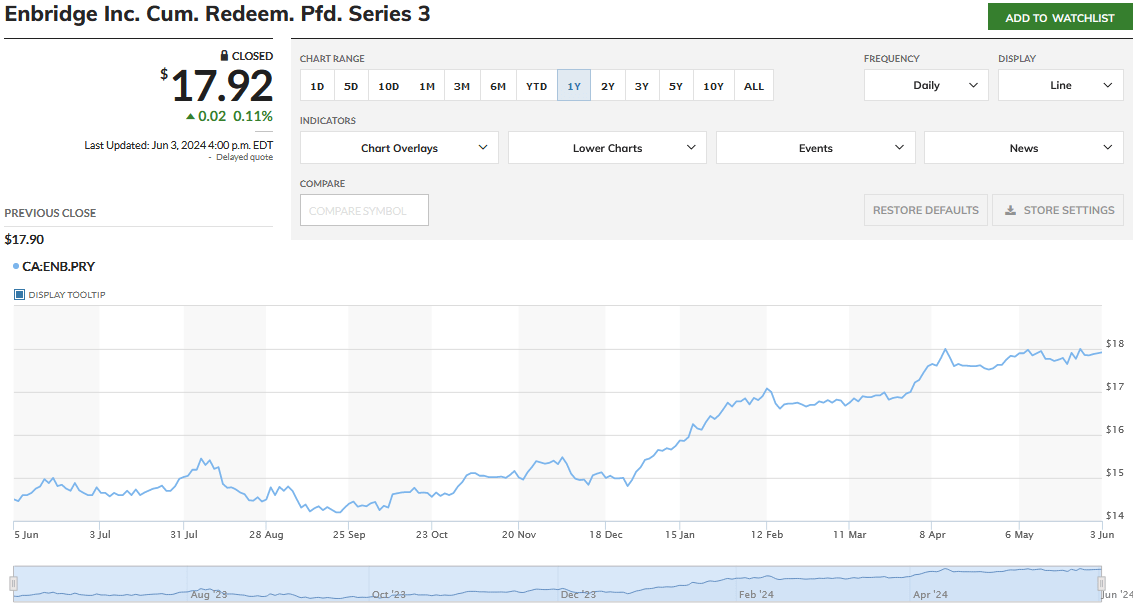

According to the prospectus, Preferred Shares Series 3 (ENB.PR.Y:CA) were issued at $25. The dividend for these preferred shares is calculated as a sum of 5-year Government of Canada bond yield “on the Fixed Rate Calculation Date plus a spread of 2.38%.” The annual dividend was set at $0.93 per share for the current 5-year period. This implies a 5-year GOC rate of 1.34% at the time. As of June 3rd, 2024, the 5-year GOC rate was around 3.6% or approximately 2.26% higher.

CNBC

After applying a 0.25% discount (expected first interest rate cut by the BOC) to the current 5-year GOC yield of 3.6%, I calculated the dividend for the next 5 years to be $1.43 annually. This represents a 54% upside to the current dividend payment and results in a new yield of 8.0%.

MarketWatch

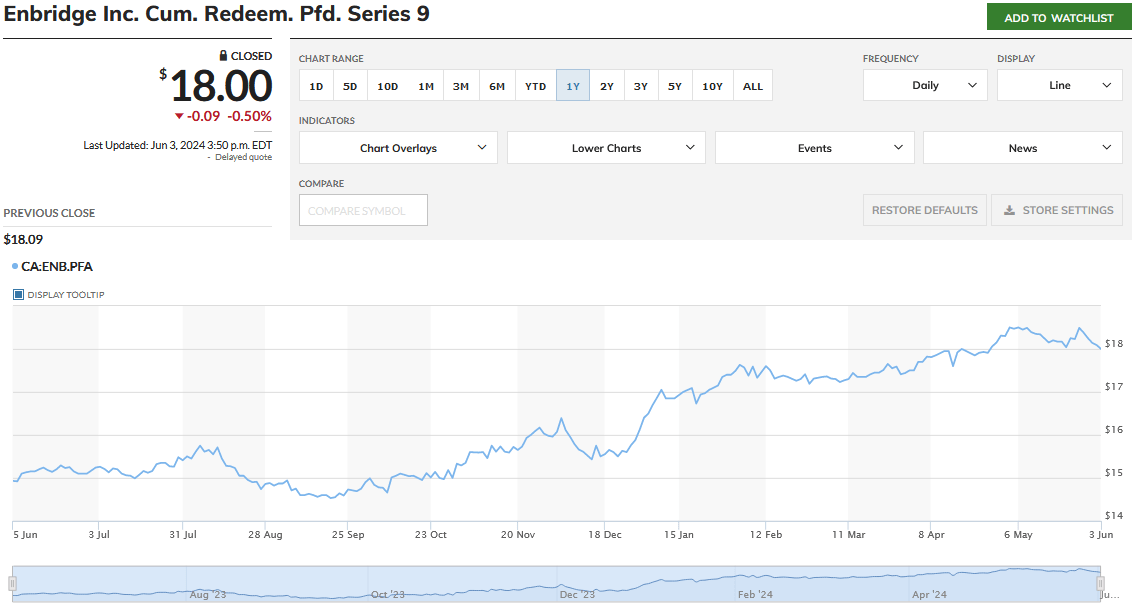

A similar calculation was performed for the Enbridge Series 9 (ENB.PF.A:CA) preferred shares. However, as the reset date for these preferreds is December 1st and the recalculation date is November 1st, which comes after the potential interest rate cut on October 23rd, I lowered the current 5-year GOC yield by 0.5%. This resulted in the new fixed annual dividend of $1.44, representing a 41.2% upside to the current dividend and a yield of 8.0% for the next five years. As discussed in my previous article, ‘Enbridge Preferred Shares: Prime Investment Opportunity,’ investing in preferred shares one month before the recalculation date provided a meaningful upside.

MarketWatch

Other Canadian infrastructure and utilities preferreds with fixed dividends that will reset over the next six months

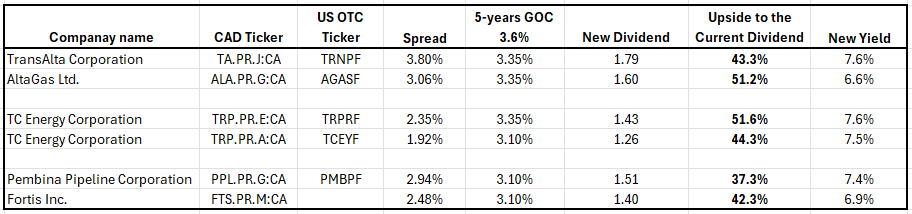

The table below includes preferred shares of TransAlta, AltaGas, TC Energy, Pembina Pipelines, and Fortis. The 5-year fixed dividends for all of these preferreds are due to reset over the next six months. Their recalculation dates come after the first expected rate cut, whether the BOC will announce it on June 5th or July 24th.

(OTCPK:TA.PR.J:CA) (OTC:TRNPF), (ALA.PR.G:CA) (OTCPK:AGASF) and (TRP.PR.E:CA) (OTC:TRPRF) have their yields recalculated before the October 23rd key rates announcement by the BOC. To calculate new dividends for these shares, I reduced the 5-year GOC yield by 0.25%. Assuming a second 0.25% rate cut on October 23, 2024, I reduced the projected 5-year GOC for the remaining three preferreds (TRP.PR.A:CA) (OTCPK:TCEYF), (PPL.PR.G:CA) (OTCPK:PMBPF), (FTS.PR.M:CA) by another 0.25%.

The tables below show that even after the Bank of Canada’s two rate cuts, these preferred shares will pay significantly higher fixed dividends than before the reset. According to my calculations, the new yields will range between 6.6% and 7.6%.

Author analysis; Company data Author analysis; Company data

Major risks to investing in Canadian infrastructure and utilities preferreds

Operating and business interruption risks could undermine the production and financial results of utilities and infrastructure companies. Accidents, logistics disruption, equipment breakdown, etc., could result in lower capacity output, business delays and disruption, and increased repair and maintenance costs.

Risks related to growth through M&As include lower-than-expected returns on new deals, higher-than-planned additional capital requirements, hidden regulatory problems and changes in market conditions resulting in demand deterioration.

Utilities and infrastructure companies, especially those with internationally diversified business models, are vulnerable to regulatory risks. These risks include changes in government regulations, legal problems with local communities, changes in taxes, limitation of market prices, failure to obtain required approvals and licenses, etc.

Interest rate risks could be both upside and downside. The current environment, when the Bank of Canada is widely expected to cut rates, provides a potential tailwind for Canadian common and preferred shares that pay stable and meaningful dividends. However, the higher-for-longer approach to interest rates by central banks could result in refinancing risks and lower profitability.

Conclusion

As the Bank of Canada will likely announce its first rate cut on June 5th or July 24th, I expect increased investor interest in dividend-paying common and preferred shares. The current high-interest rate environment provides a unique opportunity to invest in preferred shares that are due to reset their fixed dividends over the next six months. As monetary easing gets on track, demand for these investments will likely trigger irrational behavior among investors, potentially leading to the FOMO.

Our list of preferred shares includes 2 Enbridge, 2 TC Energy, Pembina Pipeline, TransAlta, AltaGas, and Fortis. These preferred shares are from low-risk utilities and infrastructure companies. Even though interest rate cuts will lower their post-reset yields, these preferred shares will likely perform strongly over the next 6 to 12 months.

In addition to the significant increase in fixed dividend payments, share prices are also likely to appreciate. This expectation is supported by the strong upward movement of the preferred shares that started last October. During this period, the market expected 5 rate cuts in 2024. This is also confirmed by the meaningful appreciation of preferred share prices one month prior to the recalculation date.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.