hapabapa/iStock Editorial by way of Getty Photographs

Factors to notice:

1) All values are in CAD until famous in any other case.

2) Previous to June 17, 2021, Canadian Web operated underneath the title of Fronsac Actual Property Funding Belief (FRO.UN).

Earlier Protection

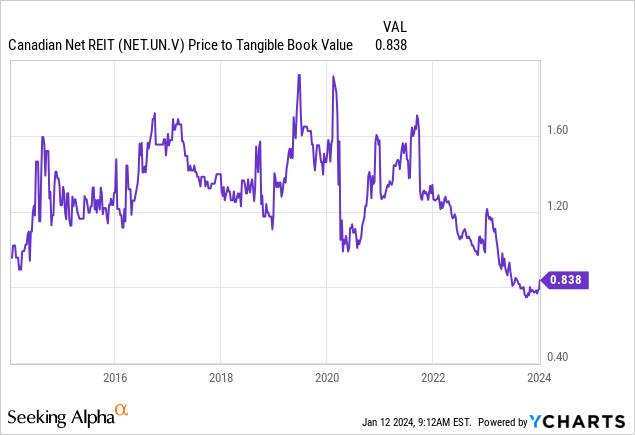

We lined the 2023-Q1 outcomes of Canadian Web Actual Property Funding Belief (TSXV:NET.UN:CA) and got here away impressed with this internally managed, retail landlord. This triple web enterprise was buying and selling at a reduction to its web asset worth or NAV on the time, which was at odds with majority of its buying and selling historical past. Sure, its 8.0X debt to EBITDA was a bit lofty for our style, however its debt construction (primarily property degree) and minimal capital expenditures, made it a no brainer purchase in our books. The icing on the cake was said in our concluding remarks for that piece.

At current, you’re getting a close to 7% yield with a 50% payout ratio. That’s fairly a formidable deal in triple-net land.

Supply: Canadian Net REIT: 6.9% Yield From This Triple Net Landlord

Word: Readers searching for an in depth introduction to this REIT can consult with our earlier piece (hyperlink supplied above). We is not going to rehash the main points in the present day.

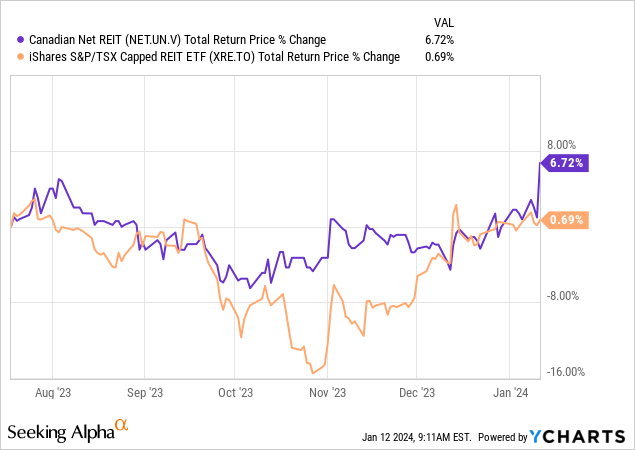

We began accumulating a place thereafter, and in the present day it dwarfs all different REIT positions in our portfolio. It has handily crushed the Canadian REIT Index throughout this timeframe. Although the majority of the outperformance has actually come within the final two days.

The market remains to be not awarding this the proper a number of and it continues to commerce across the identical low cost as final July.

It yields 6.7% at present (2.88 cents/month-to-month distribution, $5.18 value), and has a 55% payout ratio. At present, we assessment the final printed outcomes and clarify our present stance on this Canadian retail REIT entity.

Q3-2023 Outcomes

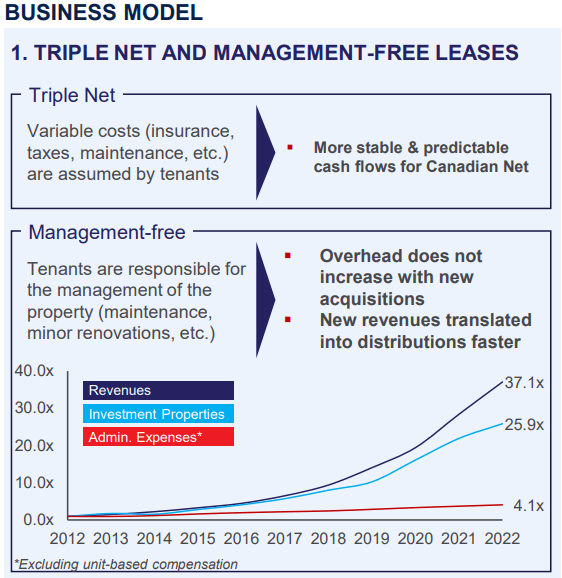

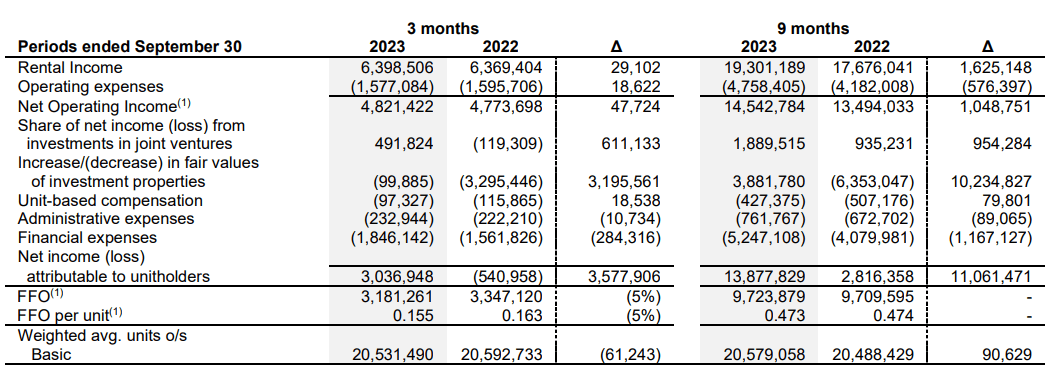

The Canadian Web portfolio contains properties that primarily home retailers, nationwide service stations, comfort shops, and quick-service restaurant chains. The REIT had 99 funding properties to its title on the finish of Q3-2023, bulk of which resided in Quebec (82), with the stability in Ontario (8), Nova Scotia (8), and New Brunswick (1). The portfolio was 101 sturdy on the finish of Q1-2023. Two properties had been subsequently disposed, one in April and the opposite in September. Regardless of the hit to the rental revenue from these inclinations, the Q3-2023 top-line inflows nonetheless confirmed a nominal uptick relative to the Q2-2023 numbers.

Q3-2023 MD&A

This outperformance was as a result of hire will increase on among the current properties. The 9-month interval, then again, confirmed a sturdy 9% enhance within the rental revenues as a result of web acquisitions since This autumn-2021, together with contractual hire step-ups. Administration supplied colour on the hire will increase anticipated for the 2024 renewals in the course of the earnings name.

Patrick Kealey

Excellent. After which simply final query right here. I do not need to hog the decision an excessive amount of. Simply waiting for 2024, might you present any colour perception as to what you are seeing thus far, simply form of respect to leasing spreads and possibly contractual escalators for these expiries?

Kevin Henley

Sure. So 2024, thus far, what we have seen is, I’d say, between 10% and 15% on principally leases in place. On new leases, we’re at present underneath negotiation, so very laborious to inform. However nothing that isn’t contractual can be leased at a variety decrease than 10%, for positive.

Supply: Q3-2023 Earnings Name Transcript – Tikr

The portfolio continues to be absolutely occupied on the finish of Q3-2023, with a weighted common lease time period of 6.6 years. Being a lessor of triple web properties, this REIT’s working bills are steady for probably the most half. It incurs neither the overhead on its rental properties, nor the hassles that include managing them. Each the tasks lie solely on the top of its tenants.

Q2-2023 Reality Sheet

We are able to see the working expense stability in motion within the web working revenue or NOI numbers for the previous few quarters, which persistently are available at round 75% of the rental revenue.

Q3-2023 MD&A

Because of the shut monitoring between the rental revenue and NOI, the sub-nominal enhance in rental income was matched by sub 1% enhance within the year-over-year NOI. Whereas the REIT is shielded from the working prices of the rental properties, it feels the influence of the upper rates of interest on its mortgage renewals, variable charge mortgages, and credit score services. The weighted common rate of interest on its mortgages elevated from 3.63% on September 30, 2022 to three.80% on the finish of Q3-2023 and the year-over-year curiosity protection diminished from 2.9X to 2.6X. We must always add that the curiosity protection has been 2.6X since Q1-2023, so it has not been a latest drop. The upper curiosity bills simply outpaced the modest NOI enhance and the funds from operations got here in round 5% decrease than the comparative quarter in 2022.

Q3-2023 MD&A

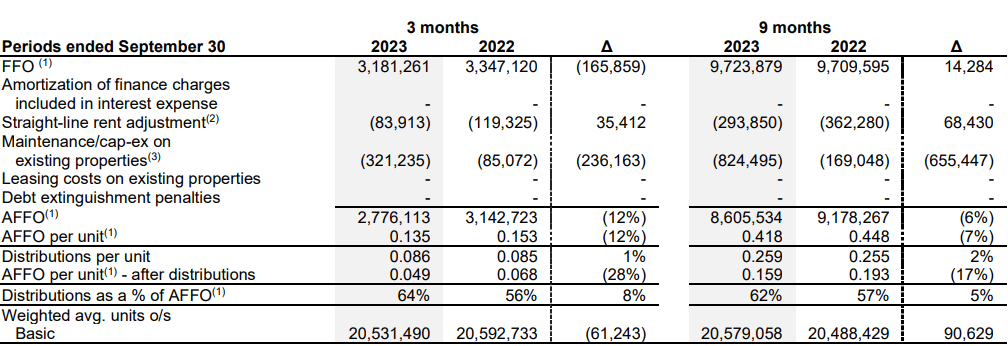

The year-over-year adjusted funds from operations or AFFO declined by 11%, over twice that of the FFO lower.

Q3-2023 MD&A

The primary contributor of this double-digit decline was the upkeep/cap-ex, and the REIT expects to get better the $800 thousand and alter, plus 9% from its tenants.

Patrick Kealey

Acquired it. After which simply shifting ahead on the upkeep CapEx aspect. Assuming that the bump this quarter is just a bit little bit of carryover from, I consider, it is the roof upkeep from — that you simply mentioned final quarter?

Kevin Henley

Precisely. So this 12 months was large, simply we had the $805,000 that was spent on the roof alternative on our [ Kirby ] Lake property. This can be recovered with a 9% charge of return. So that is actually — we began the work in Q2, completed in Q3, and that is why you see an uptick there.

Supply: Q3-2023 Earnings Name Transcript – Tikr

Excluding this short-term influence, the AFFO nonetheless declined, however by 1.4%, which is extra in step with the FFO decline.

Whereas 2022 had the REIT making several acquisitions, 2023 was about inclinations. The sale value on these exceeded their respective IFRS valuations i.e., they had been accretive. Sure, these too got here up in the course of the earnings name.

We’re completely satisfied to report that along with the Timmins property sale in Q2, we additionally bought a restaurant property operated underneath the Mikes banner in Trois-Rivières, Quebec, for $1.3 million in the course of the third quarter and a Pizza Hut property in Dartmouth, Nova Scotia for $1.65 million in October. These transactions exceeding our IFRS values proceed to indicate our capacity to create worth whereas enhancing our capital construction.

Supply: Supply: Q3-2023 Earnings Name Transcript – Tikr

The September sale was at a capitalization charge of 5.6%. Regardless of with the ability to dispose a number of properties at greater than their reported valuations, Canadian Web maintained the portfolio degree capitalization charge at 6.41%, and this has been unchanged since December 2022.

Liquidity and Debt

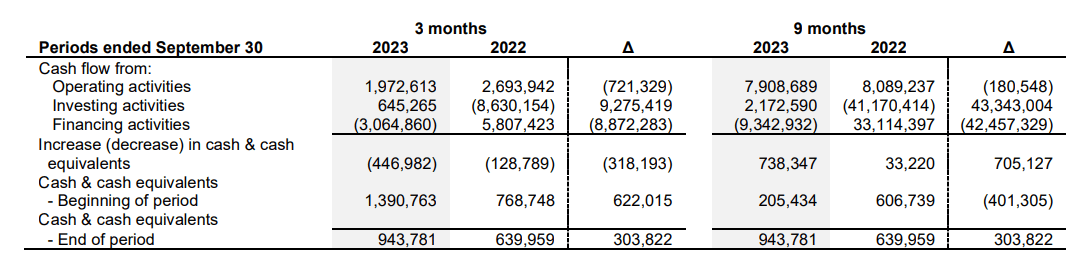

The REIT had round $944 thousand in money and money equivalents on the finish of Q3.

Q3-2023 MD&A

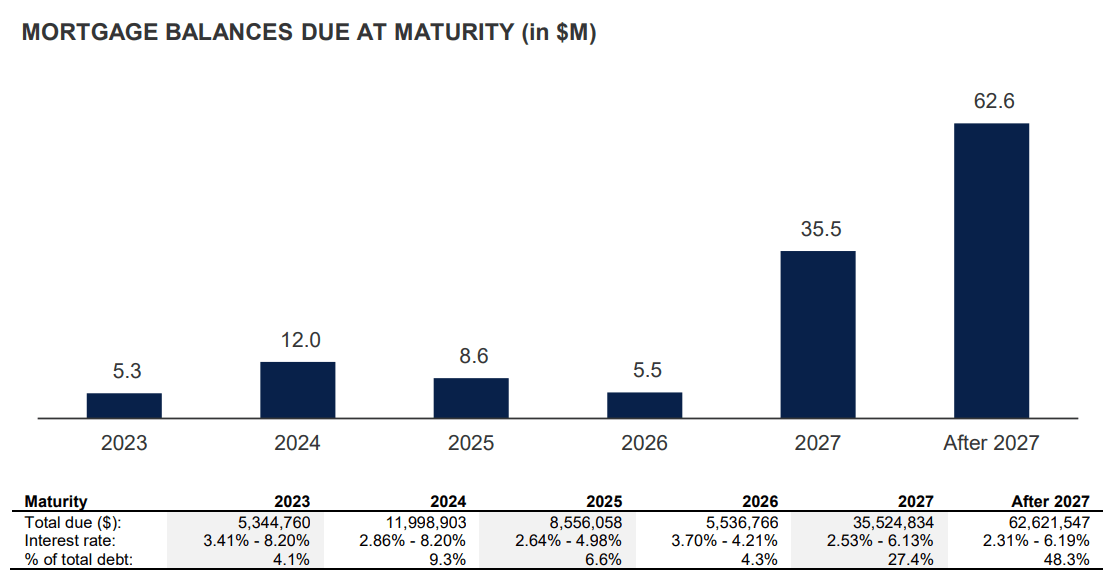

Moreover, it has 3 secured traces of credit score, which had a cumulative $3.1 million that was out there to attract on the finish of the reporting interval. Each the credit score services limits, in addition to the utilization have elevated since Q1-2023, the reporting interval we lined beforehand. The full restrict on the services was round $19.6 million then, with $15.4 million drawn on the time. On the finish of Q3, the 2 quantities stood at $20.6 million and $7.3 million, respectively. Whereas the majority of their mortgages don’t come up for renewal till 2027, the REIT nonetheless has to navigate the present rate of interest setting for round 13% of its $152 million mortgages maturing within the 15 months subsequent to Q3-2023.

Q3-2023 MD&A

Administration anticipated to get the 2023 renewals going within the weeks following the earnings name.

About $8.5 million of mortgages, together with these in three way partnership, stays to be renewed in 2023, with completion anticipated within the coming weeks. Following mortgage renewals, we anticipate producing round $1.5 million in web proceeds to repay credit score services.

Supply: Q3-2023 Earnings Name Transcript – Tikr

With the rates of interest cooling in This autumn, administration anticipates locking in charges of round 6.25% – 6.5% for the refinancings developing shortly after the earnings name.

Verdict

We nonetheless prefer it and are sustaining a Purchase. It stays a really undervalued state of affairs that’s comparatively immune from even modest financial weak point or credit score stresses. Sure, if we get a extreme recession, this may commerce right down to $4.00 and sure you must double down then. The important thing function right here is that the worst case is a number of properties do not get refinancing executed. In that case, the REIT might require a small money infusion for these properties, altering the mortgage to worth ratios. Even when that money was absent, it’d forfeit a few properties in a GFC-like setup. However the REIT will survive and your odds of constructing 10% complete annualized returns from right here stay terribly excessive. Purchase.

Please be aware that this isn’t monetary recommendation. It might look like it, sound prefer it, however surprisingly, it’s not. Buyers are anticipated to do their very own due diligence and seek the advice of with knowledgeable who is aware of their targets and constraints.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.