ryasick

Article Thesis

Capital Southwest (NASDAQ:CSWC) has been a powerful performer during the last 12 months. Nonetheless, even following good features, shares usually are not costly, and Capital Southwest additionally nonetheless gives a reasonably good dividend yield of near 10%. Whereas ready for a pullback might enable for an excellent higher entry level, buyers ought to do effectively in the long term in the event that they purchase at present costs.

Previous Protection

I’ve coated Capital Southwest thrice previously, with the most recent article being launched final June. I gave the corporate a Purchase ranking then, and to date, that thesis has performed out effectively — Capital Southwest has returned 28% since then, quadrupling the broad market’s 7% return over the identical time-frame.

Now, a bit greater than half a 12 months later, it is time to replace my thesis on Capital Southwest — what has modified, what has remained the identical, and the way good does Capital Southwest look right this moment?

Capital Southwest: Robust Execution

As a enterprise improvement firm, or BDC, Capital Southwest is influenced by a number of macro objects. The primary vital macro issue to contemplate is the rate of interest atmosphere. Most of Capital Southwest’s loans are floating-rate loans, which means that the corporate advantages from rising rates of interest. When the Fed ups its essential rate of interest, then Capital Southwest earns increased curiosity on most of its loans, all else equal. Whereas the corporate borrows cash as effectively, with the intention to finance a few of its loans, it typically borrows at fastened charges. Finally, it must refinance its personal debt and can expertise increased rates of interest there as effectively, which is able to lead to increased bills, all else equal, however that occurs with a time lag, whereas the profit from increased charges on the curiosity the corporate earns materializes instantly. In a better fee atmosphere, Capital Southwest will thus not essentially earn extra money eternally, however no less than till all its borrowings have been rolled.

We see the optimistic affect of upper rates of interest on Capital Southwest’s profitability within the firm’s latest outcomes. Whereas Capital Southwest continues to originate new loans, which leads to progress in its portfolio, revenues additionally noticed an enormous increase from a better web curiosity margin, which is why complete funding earnings soared by virtually 60% in the course of the most recent quarter in comparison with one 12 months earlier.

The robust income improve did lead to an enormous web funding earnings improve as effectively, which is Capital Southwest’s earnings equal. Nonetheless, you will need to observe that Capital Southwest, like many different enterprise improvement corporations, points new shares usually with the intention to finance a few of its new investments with fairness. This share issuance ends in a climbing share rely, which is why the corporate’s web funding earnings doesn’t develop as quick as its company-wide web funding earnings. Throughout the newest quarter, web funding earnings rose from $14.4 million one 12 months in the past to $27.2 million, which made for a hefty 89% improve. On a per-share foundation, nonetheless, web funding earnings grew from $0.52 to $0.69, which pencils out to a progress fee of 33%. That’s nonetheless very robust, however not as excellent because the company-wide web funding earnings progress fee would possibly counsel. Finally, earnings per share progress is most vital for the trajectory of an organization’s share worth, thus the online funding earnings per share quantity is the one buyers ought to concentrate on. The outcome, right here, remains to be fairly robust, at a bit greater than 30%, which is particularly good once we contemplate that Capital Southwest is an earnings funding primarily, not a progress firm.

Whereas rates of interest play an vital function for Capital Southwest and different BDCs, different macro objects are vital as effectively. Financial progress impacts mortgage demand and thus influences what number of funding alternatives materialize, whereas lack of financial progress may end up in increased credit score losses — when corporations are hurting, the danger of them changing into unable to pay their debt rises.

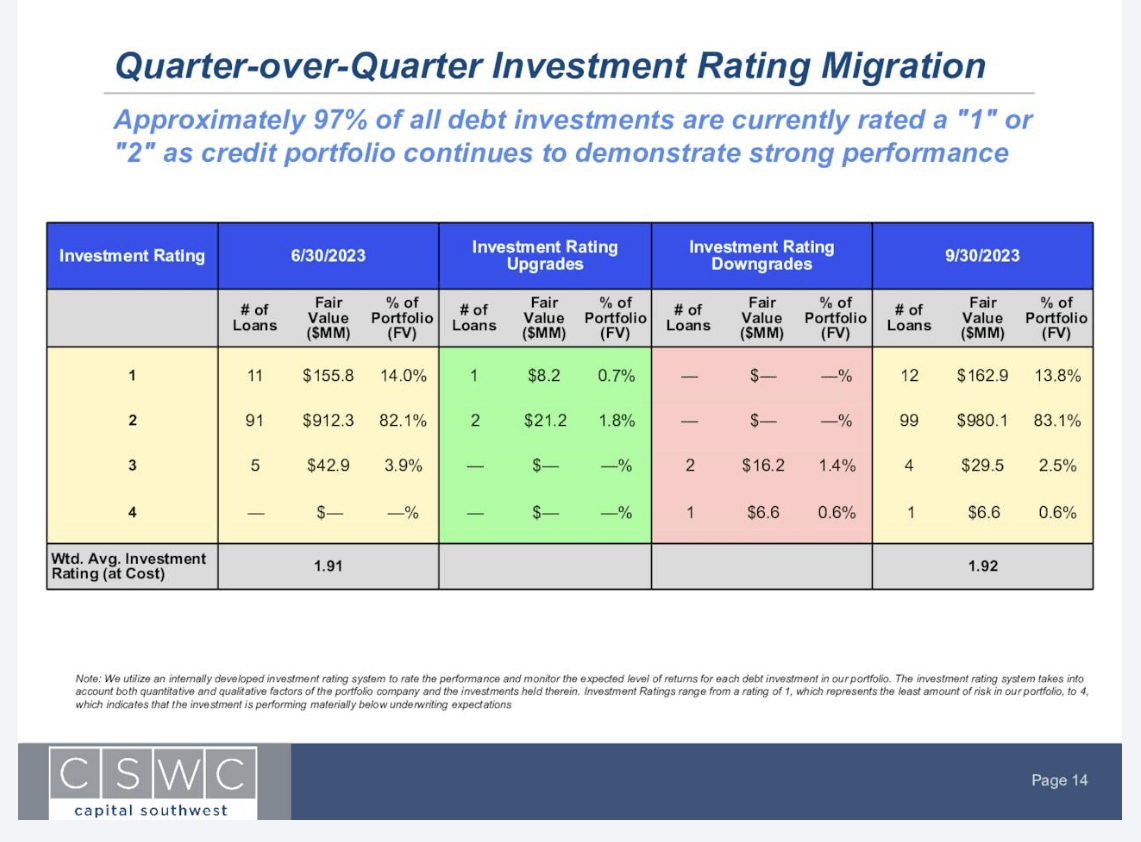

Capital Southwest makes first lien secured debt investments primarily, nevertheless it additionally makes some second lien debt investments and extra fairness investments in some circumstances. Whereas the danger of losses within the first lien secured debt portfolio, which makes up 97% of CSWC’s total credit score portfolio, is relatively small, the second lien loans and the fairness investments are riskier, on common. Throughout the newest quarter, Capital Southwest’s loans had been wanting fairly good normally, as we are able to see within the following presentation slide from the corporate’s most up-to-date earnings launch:

CSWC credit score high quality (Capital Southwest earnings presentation)

The four-tier funding ranking, the place “1” means the bottom threat and highest high quality, whereas “4” means the best threat and lowest high quality, sees 97% of debt investments in one of many higher two ranking classes. Whereas the ratio of loans within the lowest high quality class, “4”, has risen from zero to 0.6% throughout the newest quarter, the ratio of loans within the decrease two ranking classes has declined from 3.9% to three.1%. We are able to thus say that among the many weaker high quality loans with a “3” or “4” ranking, some obtained higher and do now have a ranking within the higher half, whereas some obtained even weaker and had been downgraded from “3” to “4”. I total see this improvement as comparatively impartial and the vital factor is that the very overwhelming majority of loans stay within the higher two funding ranking classes.

Financial progress has remained solidly optimistic over the past couple of quarters, however there isn’t any assure that this may stay the case going ahead. Some analysts and buyers count on a recession in the course of the present 12 months, triggered, no less than partially, by the Fed’s tightening during the last two years. If that had been to occur, buyers ought to count on that some further credit score points materialize in Capital Southwest’s portfolio. Losses won’t essentially soar, however extra credit standing downgrades and no less than some losses in CSWC’s credit score portfolio must be anticipated in case we get right into a recession. A recession might additionally damage the worth of the fairness investments Capital Southwest has made previously. That being stated, I don’t imagine {that a} reasonable recession can be a catastrophe — Capital Southwest ought to be capable to abdomen some credit score losses with out an excessive amount of hassle. Supplemental and particular dividends may very well be minimize in case increased funding losses lead to quickly weaker earnings, nonetheless. This will get us to the subsequent level and some of the vital ones for CSWC’s shareholder base — the corporate’s dividend funds.

CSWC: Nonetheless A Very Good Yield

Capital Southwest has, like many different BDCs, skilled good features during the last 12 months. In comparison with one 12 months in the past, Capital Southwest has gained virtually precisely 40%. A share worth return this excessive is nice information for buyers who held CSWC over that time-frame, nevertheless it additionally signifies that the dividend yield shares are buying and selling at declines meaningfully, all else equal.

Nonetheless, regardless of the dividend yield compression that was brought on by CSWC’s share worth features, the dividend yield stays fairly engaging, at 9.5% once we solely account for CSWC’s common dividend funds, and at 10.5% once we additionally account for the corporate’s supplemental dividend funds of $0.06 per quarter (within the latest previous). There is no such thing as a assure that the dividend can be maintained at this degree eternally, neither for the common dividend nor for the supplemental dividends. However the dividend progress monitor report could be very optimistic, and I imagine that no less than the common dividend is secure until we get right into a deep recession. For the reason that yield on the common dividend alone is near 10% already, buyers would probably not fall right into a panic even when the supplemental dividend had been to be minimize or lowered — in any case, CSWC would nonetheless be a really good income-generating funding on this situation.

Takeaway

Capital Southwest has been a really robust performer during the last 12 months. Whereas web funding earnings soared, share rely dilution offset a few of that progress, however even on a per-share foundation, CSWC’s web funding earnings has appreciated properly during the last 12 months. Web asset worth per share has risen as effectively, however not as drastically, which is why CSWC has develop into dearer. Once we add the truth that CSWC’s dividend yield has compressed, one can argue that buyers ought to watch for a greater shopping for alternative earlier than investing further cash into CSWC, however I imagine that long-term oriented buyers will do effectively with a CSWC funding at present costs, although the corporate is just not as low-cost because it was a 12 months in the past any longer. I thus am reasonably bullish on CSWC however acknowledge the truth that Capital Southwest was a greater funding final 12 months.