valiantsin suprunovich

Overview

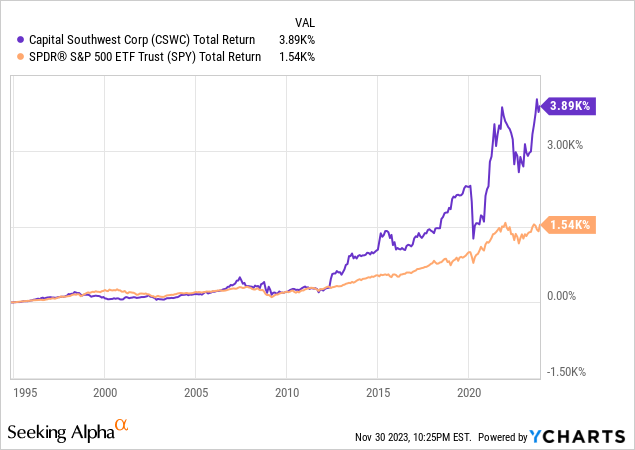

Relating to BDCs (Enterprise Growth Corporations) and double-digit dividend yields, individuals typically assume these firms sacrifice progress in trade for distribution. Within the case of Capital Southwest (NASDAQ:CSWC), you would be extremely mistaken with that assumption. Since inception, CSWC has managed to ship exceptionally constant excessive distributions in addition to present traders with a complete return that outperforms the S&P 500 (SPY). The one remorse I’ve with CSWC shouldn’t be beginning a bigger place dimension in 2020.

Capital Southwest Company is a enterprise growth firm that makes a speciality of investing in middle-market firms by credit score, personal fairness, and enterprise capital. The corporate has a technique that usually avoids startups, publicly traded firms, actual property, or troubled companies. The agency prefers industries equivalent to industrial manufacturing, healthcare, enterprise companies, specialty chemical substances, and tech-enabled companies.

This BDC seeks investments primarily in the USA. The standard funding ranges from $5 to $25 million, with a deal with firms with revenues above $10 million and worthwhile operations. I actually like this CSWC as a result of the construction and threat profile right here that has been applied permits the place to be a stress-free holding that continues to generate excessive ranges of earnings.

Construction

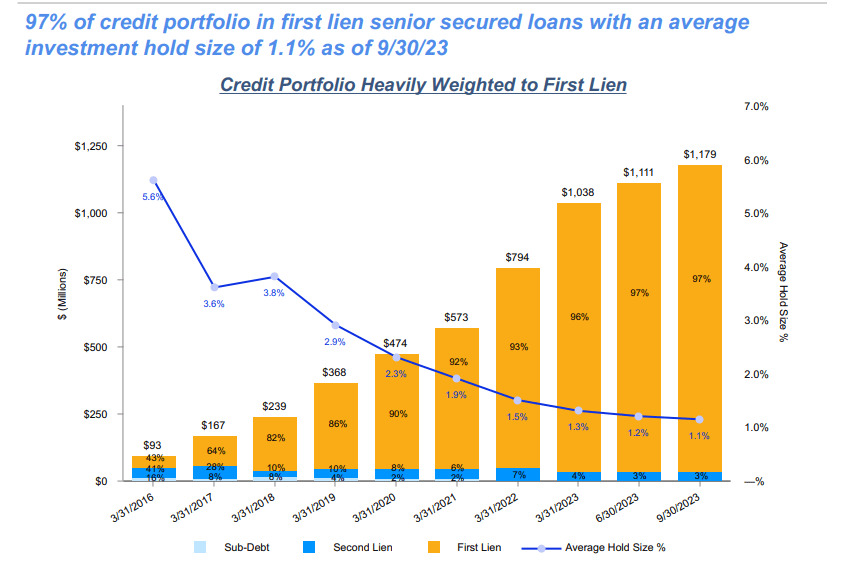

CSWC employs a two-tiered investment strategy to reinforce shareholder worth. Within the core side, targeted on the decrease center market firms, CSWC creates offers involving firms with EBITDA starting from $3 million to $20 million. The standard leverage is between 2.0x and 4.0x Debt to EBITDA, facilitated by CSWC’s debt place. Commitments can go as much as $50 million, with maintain sizes usually starting from $5 million to $35 million. CSWC engages primarily in floating charge first lien debt securities, which provides a layer of reassurance for me. As we are able to see, on their newest earnings report, their credit score portfolio closely leans towards first lien loans making up 97% of publicity.

CSWC Earnings Presentation

Floating charge debt has helped CSWC keep excessive ranges of profitability all through the rising rate of interest atmosphere. Moreover, these floating charges are first lien debt, which is generally thought-about “safer”. Floating charge first lien debt is deemed safer for a number of causes. Its rates of interest regulate periodically, offering safety in opposition to rate of interest fluctuations like we have seen during the last 12 months. One of these debt holds a senior place in an organization’s capital construction, providing increased precedence for reimbursement in case of monetary misery. Lastly, it typically comes with collateral, offering an additional layer of safety for traders.

Within the different a part of CSWC’s construction, they aim the higher center market. CSWC invests in each first and second lien positions on this house. Corporations on this class typically have EBITDA exceeding $20 million, with typical leverage starting from 3.5x to five.0x Debt to EBITDA by CSWC’s debt place. Maintain sizes on this class are often between $5 million and $20 million, specializing in floating charge first and second lien debt securities.

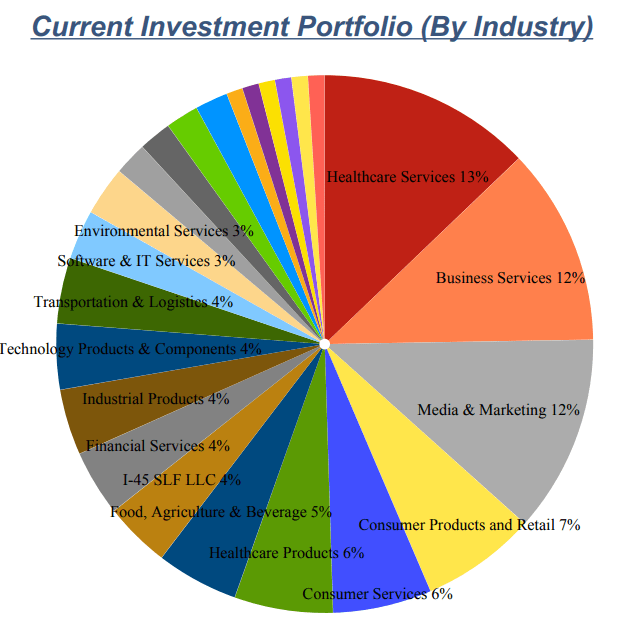

CSWC has 94 firms of their portfolio and the whole price of the portfolio elevated from $1,206,225 to $1,280,155. The weighted common yield on debt investments elevated to 13.5%, and the weighted common yield on complete investments ranged from 12.6% to 13.0%. The portfolio variety additionally stands out to me, with no particular sector accounting for greater than 13% of their complete publicity. Much like my previous analysis on Welltower (WELL), I consider the massive publicity to healthcare shall be helpful as we’ve a rising ageing inhabitants that may proceed to have longer common life spans. This construction has lots to love and has confirmed profitable over time.

CSWC Earnings Presentation

Earnings

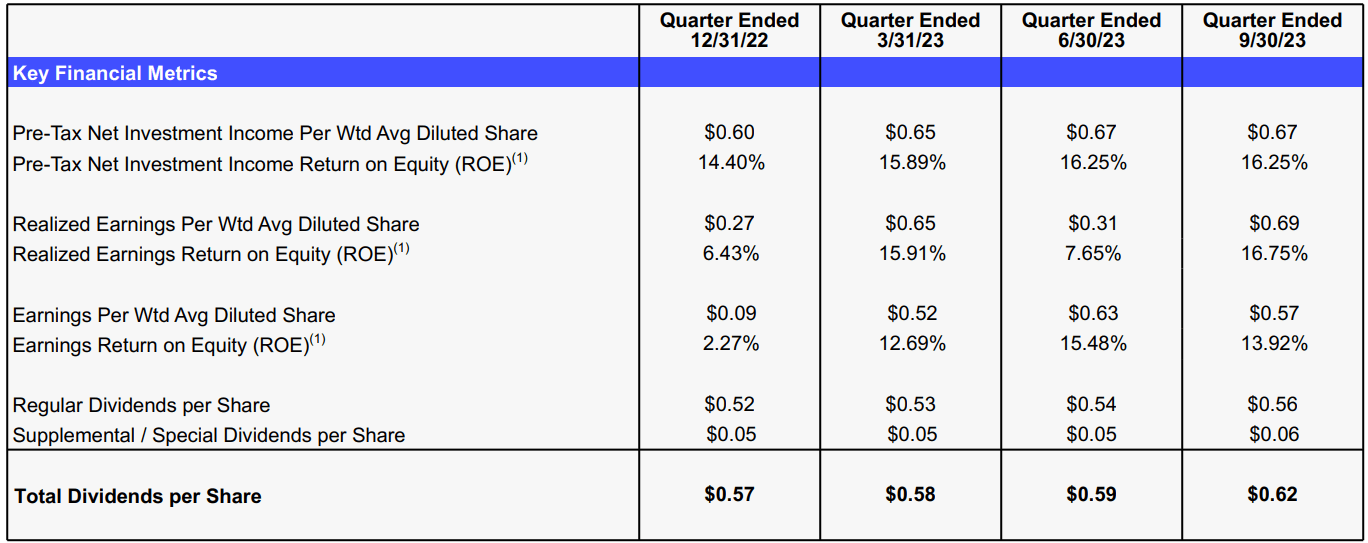

Capital Southwest reported a robust efficiency of their most recent earnings report. Administration procured $110 million in originations throughout 5 new and 6 current portfolio firms. Notably, the agency’s complete funding earnings reached $42.78 million, surpassing consensus by $0.82 million and marking a $2.38 million enhance from the earlier quarter.

For my part, mortgage originations for a BDC is at all times a very good sign for a number of causes. Elevated mortgage originations are inclined to contribute to additional earnings technology by serving to the corporate increase the funding portfolio and diversify threat throughout extra sectors. By structuring aggressive offers, BDCs can improve general portfolio yield, resulting in elevated returns just like what we have seen with all the current supplemental funds from CSWC.

This progress was attributed to an increase in common debt investments excellent and a rise within the weighted common yield on debt investments, climbing to 13.5%. The Internet Asset Worth per share additionally exhibited optimistic motion, reaching $16.46 as of September 30, in comparison with $16.38 at June 30.

The money circulate produced additionally reinforces the corporate’s robust portfolio efficiency, producing $0.67 of pre-tax web funding earnings for the quarter. This earnings comfortably coated each the $0.56 per share common dividend and the $0.06 per share supplemental dividend paid through the interval.

Dividend

As of the newest declared dividend of $0.57/share, the present dividend yield sits round 9.7%. This declared dividend additionally represents a elevate of 1.8% from the prior payout of $0.56/share. Along with the elevate, CSWC additionally declared a supplemental dividend of $0.06/share to be paid out in December.

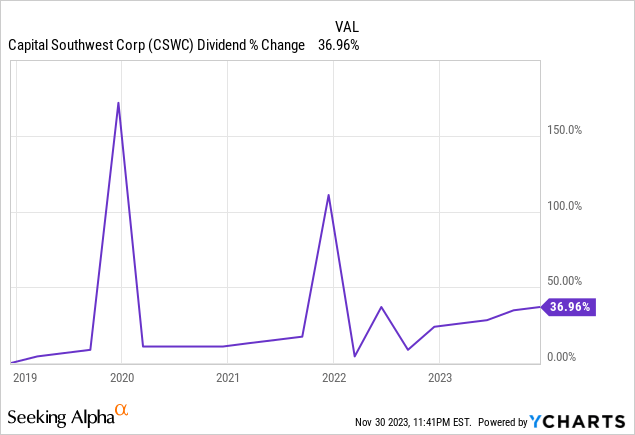

As you’ll be able to see, the dividend has grown 37% during the last 5 years and I believe that we are going to proceed seeing this grown as profitability stays robust. We are able to ignore the 2 massive spikes within the information above, as these have been particular dividends paid out. In response to Portfolio Visualizer, for those who invested $10,000 in 2016, did not reinvest any dividends, and simply held, your earnings would have gone from a measly $274 to a powerful $1,300 yearly in 2023.

CSWC Earnings Presentation

As beforehand said, we are able to see that the web funding earnings per share of $0.67 totally covers the common dividend of $0.56/share in addition to the supplemental dividend of $0.06/share. On this excessive rate of interest atmosphere, I do assume we are going to proceed to see slight raises of the dividend since CSWC has been benefitting from the floating charge loans. Plainly managed confirms that they are going to proceed to additionally distribute quarterly supplemental dividends into the longer term as charges stay above historic averages. The CEO confirmed this on the final earnings call:

As well as, because of the extra earnings being generated by our floating charge debt funding portfolio on this excessive rate of interest atmosphere, our board has once more declared a supplemental dividend of $0.06 per share from the December ’23 quarter, bringing complete dividends declared for the December ’23 quarter to $0.63 per share, which in complete symbolize 11% progress over complete dividends paid out a yr in the past quarter. – Bowen Diehl, CEO

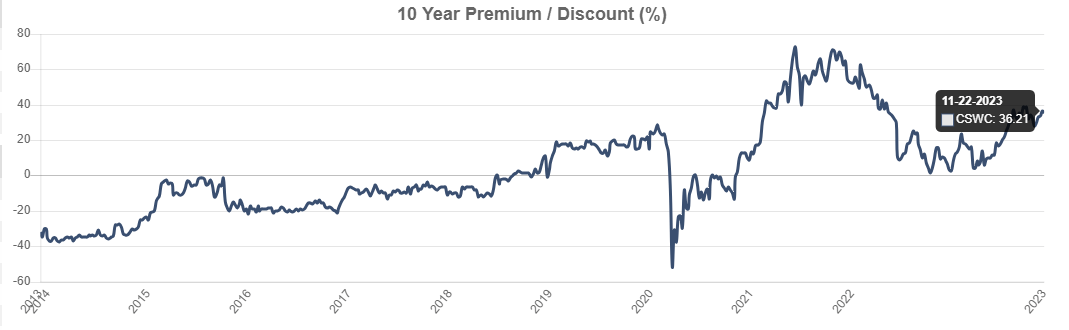

Valuation

The value to NAV (web asset worth) relationship of CSWC is a bit difficult to get down. To at least one finish, the value stays to commerce at a big premium valuation over its NAV of 36.21%. Though, buying and selling at a premium would not essentially imply you need to keep away from shopping for in proper now. Particularly when this premium appears to be for good purpose, given the index beating complete returns. On the identical time, nevertheless, the P/E of 8.35x at present sits beneath the 5-year common of 11.3x, which may point out undervaluation. Nevertheless, I believe the principle factor right here could be to deal with the sustainability and future progress of the dividend.

CEF Knowledge

I used to be fortunate sufficient to choose up shares of CSWC in Might 2020 when the low cost to NAV was roughly -20%. At these ranges, nevertheless, I’m hesitant so as to add to my place due to the news that charges have a chance to be lower as quickly as Q1 of 2024. I haven’t got a magic crystal ball, however I do assume there’s a chance that BDCs like CSWC drop in worth following any future charge cuts. I’m positive they are going to nonetheless be worthwhile in the long run and proceed to ship distinctive returns, however I want to await a greater entry.

Since CSWC is comprised of floating charge loans, I believe there’s a probability that this BDC would react far more dramatically in worth motion. As soon as once more, although, I do consider that CSWC will proceed to develop their enterprise and provide long run worth.

Takeaway

Capital Southwest Company (CSWC) stands out as a resilient and high-performing enterprise growth firm that defies the frequent false impression of sacrificing progress for dividends. CSWC has persistently delivered substantial distributions and outperformed the S&P 500 since its inception.

The corporate’s strategic strategy, with a deal with middle-market firms, a diversified portfolio, and a meticulous funding construction, has confirmed profitable over time. Notably, CSWC’s emphasis on floating charge first lien debt has enhanced profitability. The corporate’s capacity to cowl dividends by strong pre-tax web funding earnings reinforces its monetary energy.

Whereas CSWC’s premium valuation might elevate eyebrows, the P/E ratio beneath the 5-year common and the deal with sustainable dividend progress present reassurance. Regardless of potential challenges with future rate of interest cuts, CSWC’s distinctive place with floating charge loans and a historical past of remarkable returns make it a compelling long-term funding.