Jacek_Sopotnicki

A number of the finest funding alternatives, about throughout mergers and acquisitions actions. When one agency agrees to purchase out one other, there may be usually a ramification of some type between the worth at which shares are buying and selling and the worth at which the acquirer has agreed to buy them within the close to future.

This unfold exists for 2 causes. First, there’s a time worth of cash piece of the pie. Briefly, the market is accounting for the truth that, when you have your cash within the agency, you possibly can have it in one thing like a risk-free asset. That necessitates a reduction, with the dimensions various primarily based on rates of interest and the way lengthy it is anticipated till the deal goes by. Second, you’ve gotten a threat part related to the deal falling by. Once you see a big unfold in worth, that’s definitely as a result of the market believes that the prospect of the deal falling by is larger than you may usually count on.

One firm that’s speculated to be purchased out in an all-cash transaction that occurs to be sporting a large unfold is Capri Holdings Restricted (NYSE:CPRI), the luxurious style group that owns Michael Kors, Versace, and Jimmy Choo. As of this writing, shares of the corporate are buying and selling at $38.93. That suggests a 46.4% upside ought to it in the end be acquired, as deliberate, by rival Tapestry, Inc. (TPR) in change for $57 per share. It is also solely marginally larger than the roughly $35 that shares had been buying and selling at instantly earlier than the purchase was announced in August of final yr.

Right now, which means the market is forecasting a close to 100% probability of the deal falling by. This creates an attention-grabbing alternative whereby buyers may be capable to get important short-term upside. And in some circumstances the place I’ve seen this type of unfold prior to now, I’ve seen the image in a really constructive mild. It is because I seen the scenario as a positive risk-to-reward situation.

However that solely is smart when both you suppose the deal will undergo otherwise you imagine that shares are attractively priced, or at the least no worse than pretty valued if the transaction is just not accomplished. And whereas the market could be underestimating the prospect of the deal going by, there may be undoubtedly threat right here from a basic perspective that provides me pause.

An attention-grabbing image proper now

To be completely trustworthy with you, I want I might inform you that I knew whether or not, past any doubt, regulators would approve or shoot down the merger between Capri Holdings and Tapestry. However the reality of the matter is that no person is aware of for certain what is going to transpire. What I do know, and what the market appears to be reflecting, is that there’s some threat of the deal falling by. Again in early November of final yr, the FTC sent requests to each firms searching for extra data. However this wasn’t its first request for data. It was truly its second. This does occur sometimes, nevertheless it’s not terribly widespread.

Not a lot has transpired since then. We do know that, not too long ago, Henry Liu, Director of the FTC Bureau of Competitors, made some comments on the 2024 American Bar Affiliation Antitrust Spring assembly in regards to the FTC needing to focus extra on “head-to-head competition” when evaluating offers. However he didn’t say something about this specific transaction.

In its February eighth second quarter earnings name for the 2024 fiscal yr, the administration crew at Tapestry assured investors that they’re continuing ahead with the deal as deliberate, with the newest statement from that finish confirming that they’re on observe to finish the merger by the tip of this yr. As well as, they highlighted how, in November, they issued $6.1 billion in debt to make use of on this buy. They notified buyers that they acquired approval from the Chinese language Regulatory Authority for the deal, they usually simply acquired approval from their European counterpart. Moreover, in addition they detailed that they count on to seize over $200 million of synergies inside three years of the deal closing, they usually mentioned that they nonetheless count on to shut the transaction this calendar yr.

This does not imply there will not be any challenges of it. The newest news that got here out is that the FTC is “leaning” towards submitting a lawsuit to dam the deal. That would definitely cut back the prospect of it going by, however it will in the end come right down to what the courts imagine is suitable at that time. The FTC doesn’t win each case. Final yr, as an example, they ended up being defeated in courtroom when making an attempt to forestall the merger between online game writer Activision Blizzard and Microsoft Company (MSFT).

Creator – SEC EDGAR Knowledge

If I had a gun held to my head and was pressured to guess which route this transaction would go, I’d say that it will probably be accredited and accomplished. But when it would not work out, there might be some extra draw back for shareholders of Capri Holdings.

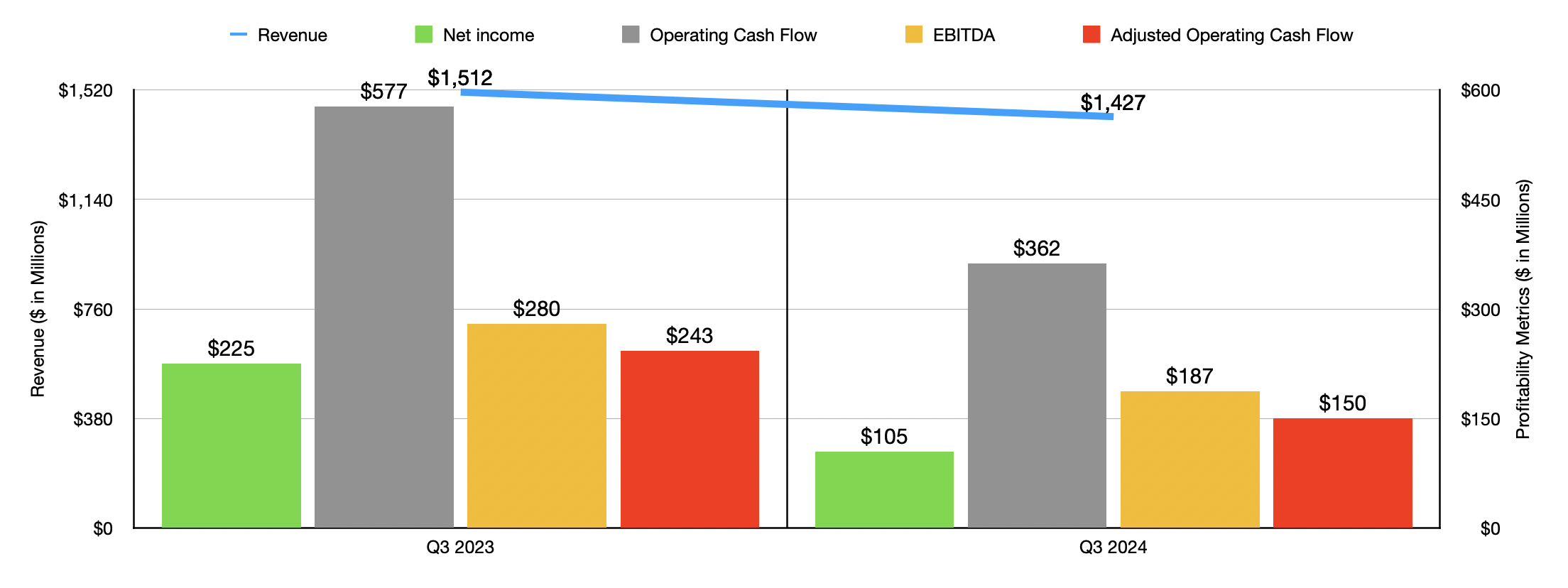

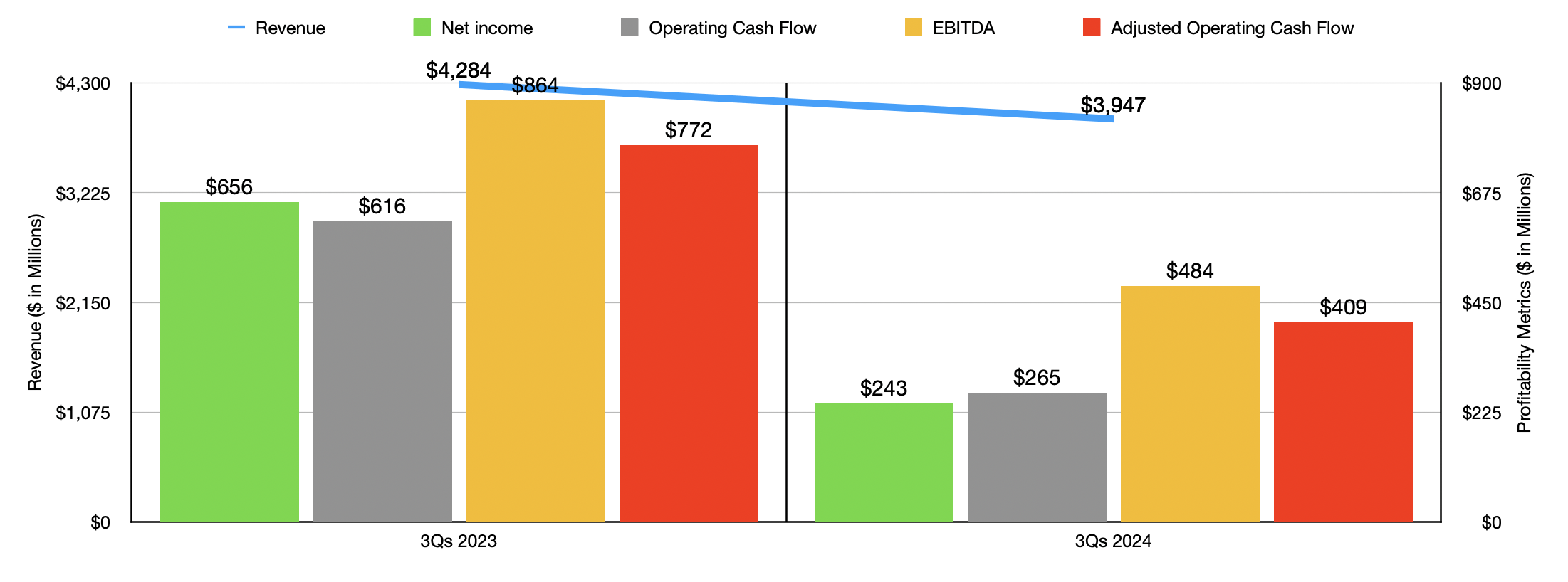

I say this as a result of basic efficiency as of late has been fairly miserable. Within the chart above, you’ll be able to see monetary outcomes for the third quarter of the 2024 fiscal year in comparison with the identical time in 2023. And within the chart under, you’ll be able to see outcomes for the primary 9 months of the 2024 fiscal yr in comparison with the primary 9 months of final yr.

Creator – SEC EDGAR Knowledge

Income has taken a success. However much more problematic has been a decline in earnings. Within the first 9 months of this yr, as an example, the corporate generated earnings of solely $243 million. That is 63% decrease than the $650 million reported one yr earlier. Working money stream, adjusted working money stream, and even EBITDA have all taken a beating throughout this window of time.

Clearly, a few of that ache could be chalked as much as the decline in income. There are a number of ache factors right here. The corporate’s gross revenue margin, as an example, worsened barely, and its depreciation and amortization prices grew. However essentially the most painful factor from a profitability perspective has been a surge in promoting, normal, and administrative prices from 46.3% of income to 53.3%. That decline, based on administration, was largely due to larger retailer prices, elevated advertising investments, and the deleveraging of working bills brought on by decrease income.

Creator – SEC EDGAR Knowledge

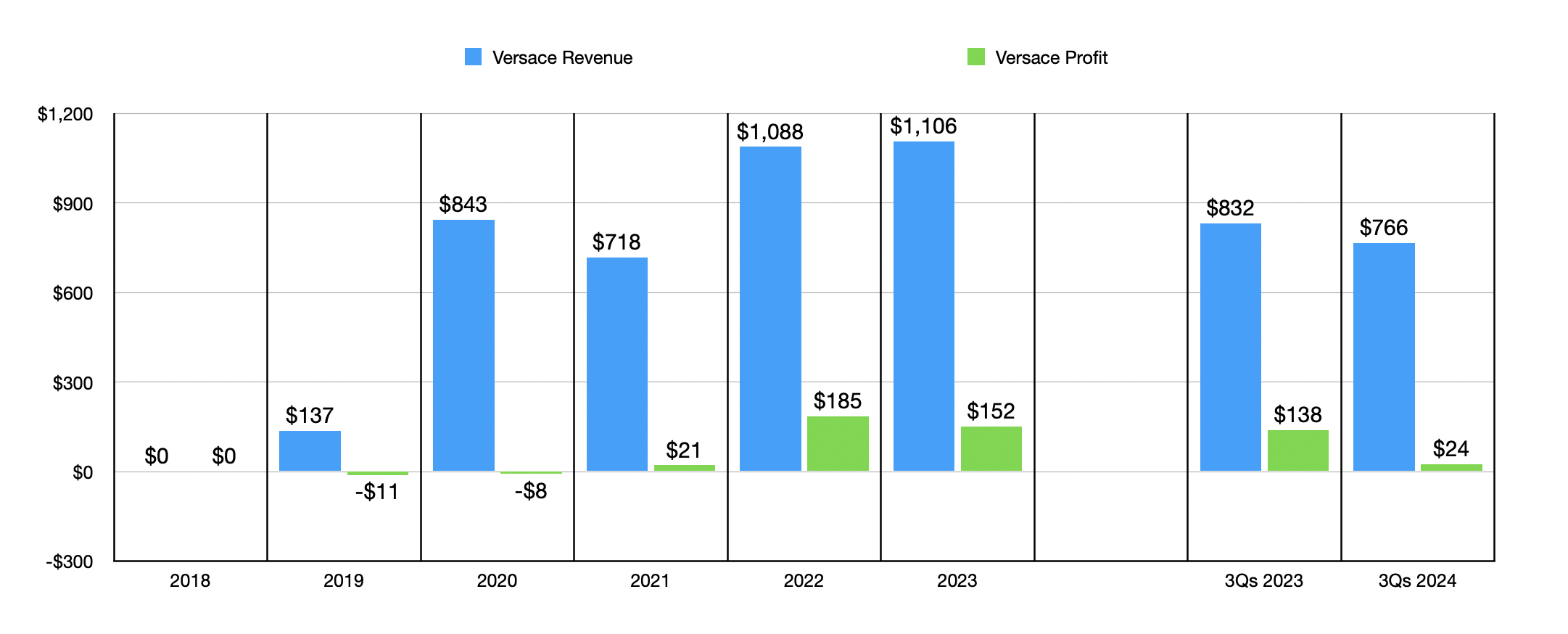

Whereas it could be tempting to view this as a short-term blip on the radar, buyers could be sensible to grasp that the previous has not been notably nice for Capri Holdings. For years now, the corporate’s financials have been worsening year-over-year. Up by 2023, the enterprise had performed nicely with its Versace line. Revenue went from $843 million in 2020 to only below $1.11 billion in 2023. Income for that line in the end peaked at $185 million in 2022 earlier than pulling again to $152 million final yr.

However again in 2020, that line truly misplaced $8 million. Within the first 9 months of 2024, nevertheless, the model reported income of $766 million. That is down 7.9% from the $832 million generated one yr earlier.

Creator – SEC EDGAR Knowledge

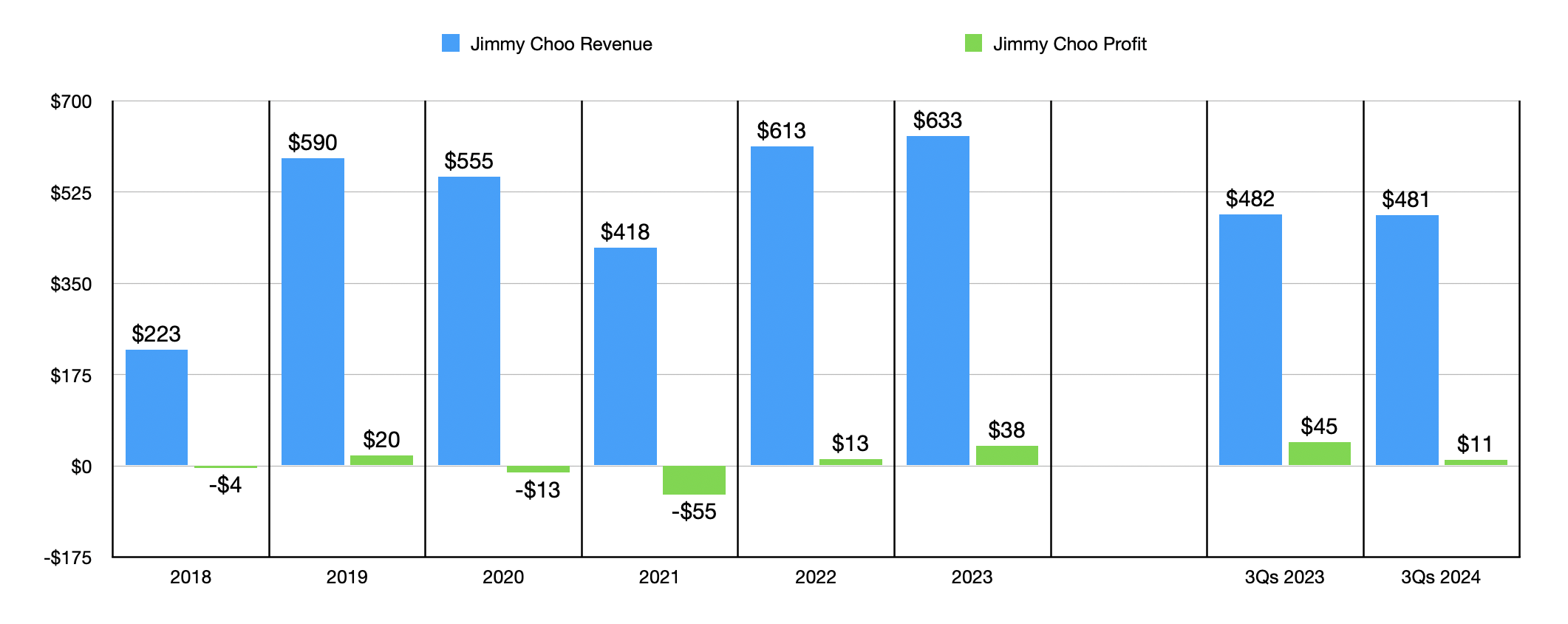

However Versace was the star of the present, within the sense that it has been the perfect performer these days. Additionally, a progress story has been the Jimmy Choo line, with income climbing from $468 million in 2021 to $633 million in 2023. This improve adopted a two-year decline in income for the model.

Nonetheless, earnings from it have by no means actually been that strong. The most effective yr on document relationship again to at the least 2018 confirmed earnings of solely $38 million. And whereas income dipped by solely $1 million from $482 million within the third quarter of 2023 to $481 million on the identical time of the 2024 fiscal yr, earnings plunged from $45 million to $11 million. Increased retailer prices, in addition to advertising investments that appear to not be paying off for now, could be blamed for this weak spot.

Creator – SEC EDGAR Knowledge

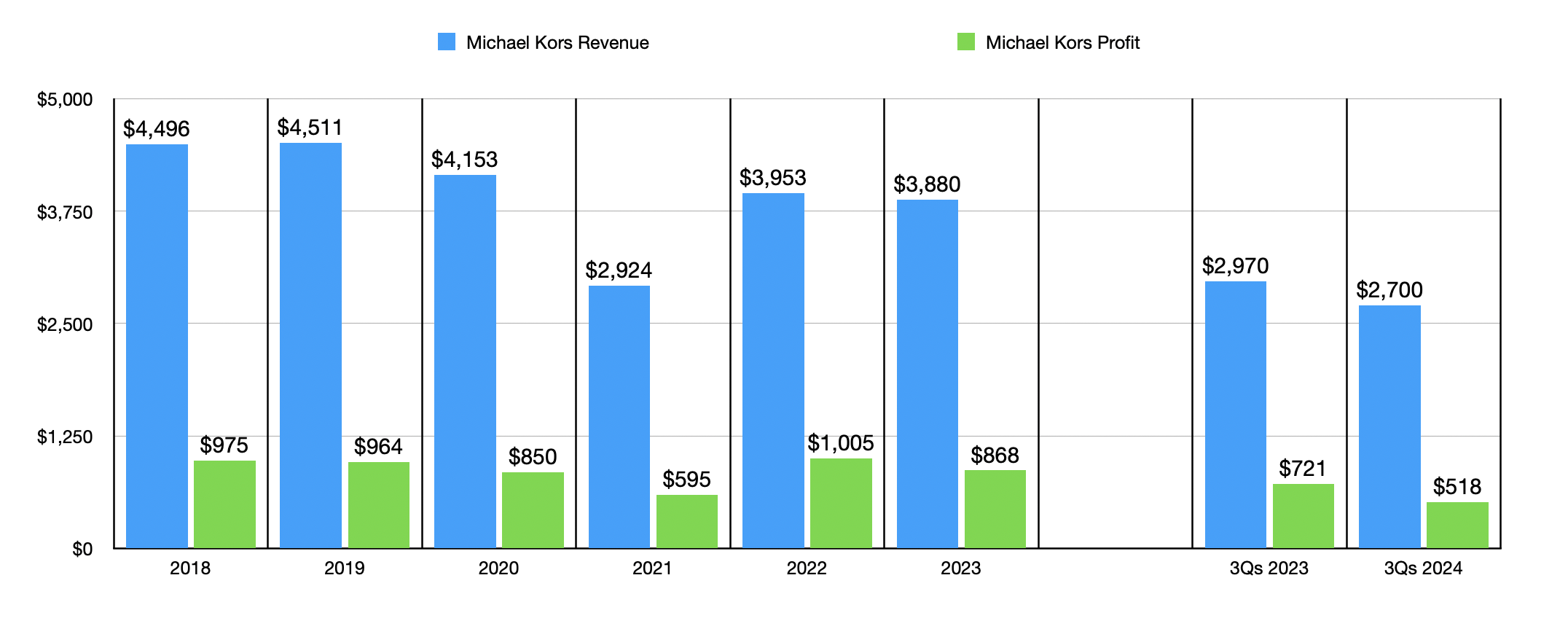

However the actual drawback youngster has been Michael Kors. Ever since hitting $4.51 billion in 2019, the model has been on the decline. By 2023, it had plunged to $3.88 billion. And within the first 9 months of 2024, it got here in at $2.70 billion in comparison with the $2.97 billion generated one yr earlier. Income have additionally taken a success, dropping to $518 million within the first 9 months of 2024 in comparison with the $721 million reported for a similar interval of 2023.

You’d suppose that, given the ache that these items are going by, your complete luxurious style market is struggling. However that does not look like the case. In line with one respected source, the worldwide market is anticipated to climb by between 3% and 5% this yr. That’s worse than the 5% to 7% rise beforehand anticipated. However progress is progress all the identical.

Creator – SEC EDGAR Knowledge

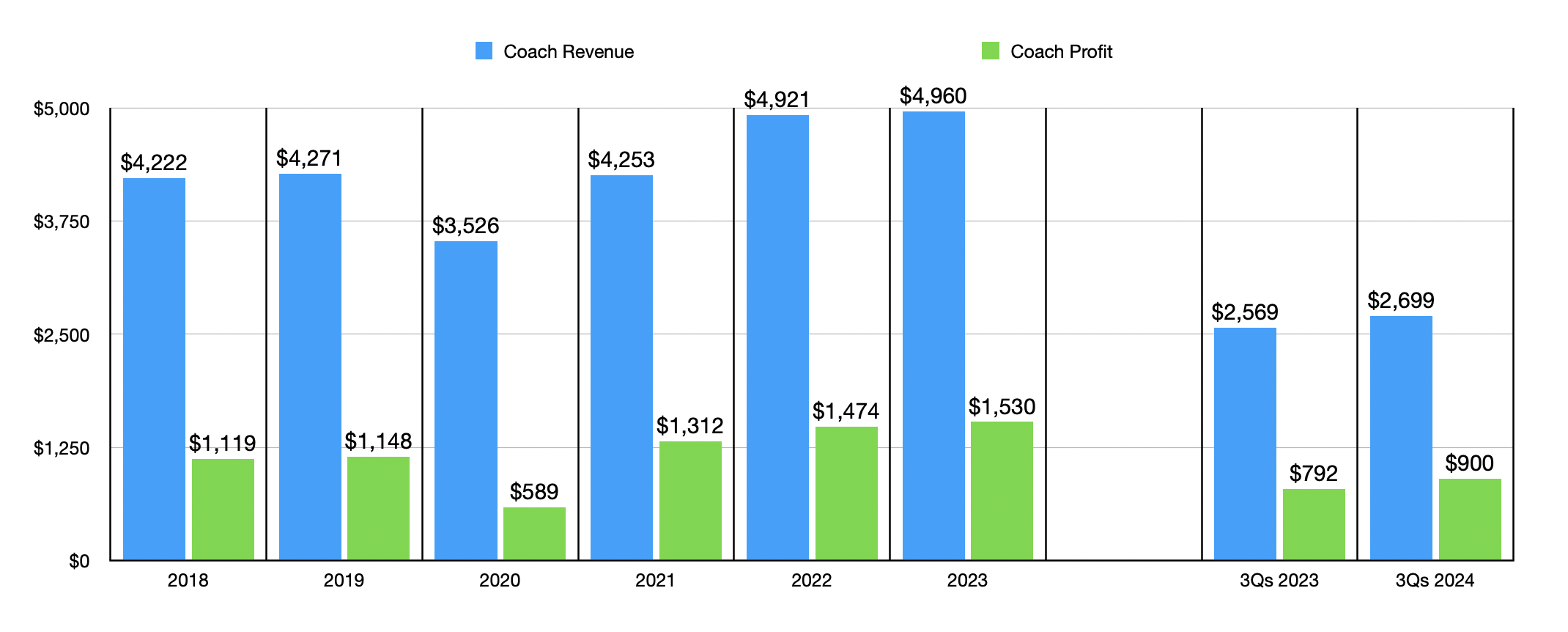

There’s a silver lining right here. And that’s the proven fact that traditionally talking, Tapestry has established a reasonably good observe document of serving to manufacturers get better. Notably, we have now the Coach model that it owns. After seeing income plunge from $4.27 billion in 2019 to $3.53 billion in 2020, with earnings declining from $1.15 billion to $589.4 million, the corporate was in a position to return the model to full well being after which some. By 2023, income had hit $4.96 billion, with earnings virtually tripling to $1.53 billion. And as illustrated by the chart above, outcomes for the primary two quarters of the 2024 fiscal yr present continued enchancment relative to the identical time in 2023.

Creator – SEC EDGAR Knowledge

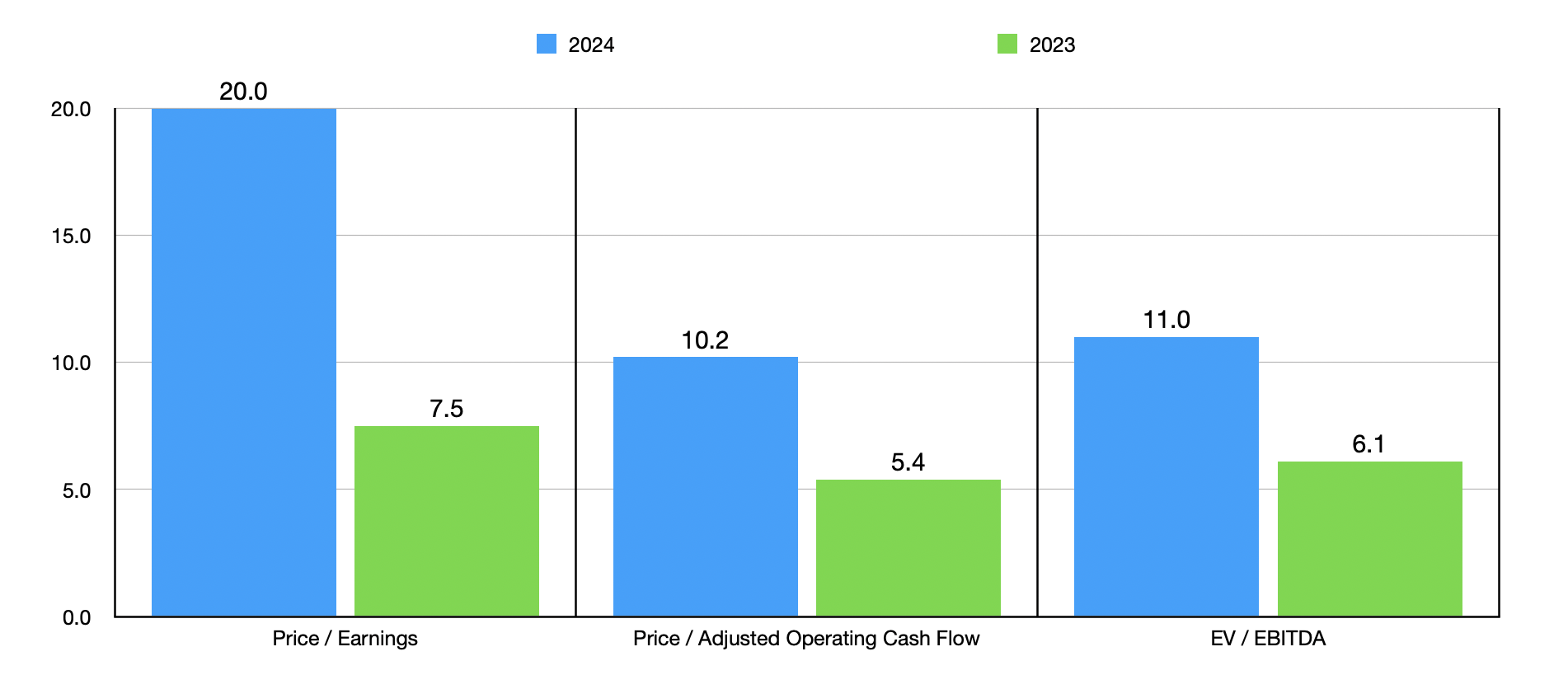

Between administration rhetoric and its skill to show issues round relating to a struggling model, I’d argue that Tapestry would very very like this transaction to nonetheless be accomplished. But when one thing occurs to make it not be accomplished, I might see some extra draw back. Along with issues that basic efficiency will proceed to weaken and not using a new proprietor, there’s the truth that present efficiency signifies that shares are fairly expensive, particularly relative to related companies.

Within the chart above, you’ll be able to see how shares are priced utilizing knowledge from 2023 and estimates for 2024. And within the desk under, you’ll be able to see how they stack up towards 5 different style manufacturers. With regards to each the worth to earnings method and the EV to EBITDA method, our prospect ended up being the costliest of the group. And when it includes the worth to working money stream method, three of the 5 companies ended up being cheaper than it.

| Firm | Worth / Earnings | Worth / Working Money Circulate | EV / EBITDA |

| Capri Holdings Restricted | 20.0 | 10.2 | 11.0 |

| Columbia Sportswear Firm (COLM) | 18.1 | 7.2 | 8.1 |

| Below Armour, Inc. (UAA) | 7.3 | 7.2 | 6.5 |

| PVH Corp. (PVH) | 9.9 | 6.8 | 6.2 |

| Gildan Activewear Inc. (GIL) | 11.7 | 11.4 | 9.4 |

| Ralph Lauren Company (RL) | 18.3 | 11.2 | 9.9 |

Takeaway

At this level, I view Capri Holdings as a really binary prospect. If the transaction between it and Tapestry will get accredited as at the moment structured, buyers can seize great upside in a brief window of time. However, the market has issues in regards to the chance of the deal going by. In some circumstances, buyers can take solace in understanding that the draw back is restricted. However that is not precisely the case right here. It would not be stunning to see the inventory drop 20% or 30% ought to issues fall by.

Due to this uncertainty, buyers who’re extra cautious ought to undoubtedly avoid the image. However for many who do not thoughts taking some threat, I’d say that Capri Holdings Restricted inventory makes for an attention-grabbing, however probably nerve-wracking, “buy” candidate.