Artyom_Anikeev

In August 2023, I covered Cargojet (OTCPK:CGJTF) (TSX:CJT:CA) and put a Hold rating but with significant upside. I even pointed out the possibility to buy Cargojet stock as we saw more than 40% upside, but the risk profile was a daring one due to weakness in the air cargo market. Since publishing that report, the stock has gained more than 30% and outperformed the 26.2% return of the broader market. In this report, I will be revisiting Cargojet stock and provide an updated assessment on the stock’s price target and rating.

Optimizing The Business For Freight Recession

The reality for many logistics providers is that more capacity coming online as international air travel recovered has significantly weakened freight rates. If you add inflation to that, we see high-cost structures for businesses and a weaker e-commerce, which is one of the driving powers of logistics and express deliveries. Putting it very simple, lower discretionary spending pressures demand for freight services while more capacity is coming online, and that ultimately pressures the top line while costs are also increasing. So, this is the time for freight service providers to right-size their operations and optimize costs and operational efficiency. Looking at FedEx, we are seeing how much excess cost there is in the system that is being cut now, and companies like Cargojet can also manage costs. Not to the same degree, but that is in part driven by the fact that Cargojet has a more shielded business set up.

Cargojet operates under minimum volume guarantees for Amazon (AMZN) and DHL (OTCPK:DHLGY), which provides some shielding. Apart from that, the company is seeing some demand increases to offset supply chain disruptions due to the situation in the Red Sea for ocean freight. All of that provides some stability in a very rough market, while cost optimizations and lower CapEx can drive financial results or at least offset cost inflation. While Cargojet is not fully immune to the freight recession, its business model is more shielded. Next to the minimum guarantees, the company also has CPI escalators and fuel cost pass through. Not all CPI escalators provide a full offset to rising costs as some escalators kick in after a certain threshold is being reached and when that is not, the cost has to be absorbed by Cargojet.

Cargojet Business Is Extremely Stable In A Depressed Market

Cargojet

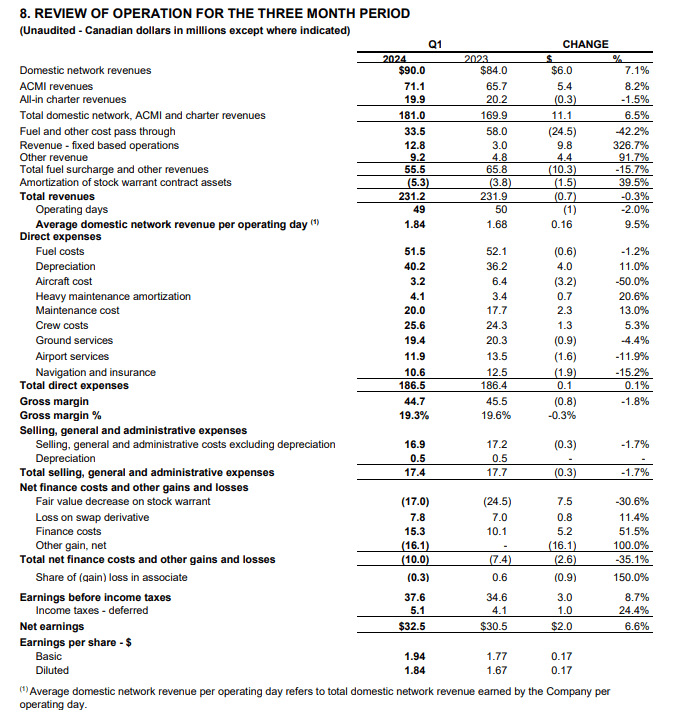

Looking at the results, we can only conclude that the company has managed and is managing the freight recession rather well. Domestic network revenues climbed 7.1% to CAD $90 million, driven by a combination of higher volumes in e-commerce and business-to-business volume, as well as CPI escalators. ACMI revenues increased 8.2% to $71.1 million, driven by one operating airplane more in the ACMI fleet and more ad hoc flights. All-in charter revenues declined modestly to $19.9 million and while this is a decline, this was driven by charter non-recurring revenues last year for flights from JFK. All in all, revenues for domestic, ACMI and charter flights increased 6.5 percent on a 2.9 percent reduction in block hours and having one operational day less in the quarter. This already provides some indication that Cargojet’s revenues are shielded well, and the company is being more efficient.

Fuel and other cost pass through declined due to lower fuel costs, while fixed based operations revenues increased significantly due to fuel sales to third parties. Other revenues such as lease revenues, hangar rental revenue and maintenance revenues improved strong, jumping $4.4 million. All revenue items included, we saw the stable revenues on lower block hours.

The cost side of the business also saw stability. Fuel costs decreased 1.2% driven by lower fuel prices and less block hours operated. The fuel costs decrease is not huge, but that is because differences in the fuel costs are settled in the form of fuel surcharges. Depreciation and amortization increased driven by a bigger asset base, while aircraft costs decreased due to a decrease in sub charter costs. Maintenance costs saw in increase driven by timing and additional higher for maintenance activities, while fleet growth and timing drove heavy maintenance amortization. Cargojet saw a 5.3% growth in crew costs driven by increased crew hiring, but it is enjoying a tailwind by bringing training activities in-house. The decision to use their own simulators reduces travel expenses and brings down downtime for pilots. While the cost reduction achieved, there is not directly obvious from the crew cost component, it is there, and it is an example of optimizing the cost structure.

Ground and airport services as well as navigation costs decreased, which is a function of network optimization. So, overall, we saw stable revenues and operating costs leading to stable gross margins and pre-tax income actually increased by 8.7% driven by $18.5 million in disposals partially offset by higher debt financing costs and lower gains on revaluation of stock warrants.

Cargojet Stock Is Still A Hold

The Aerospace Forum

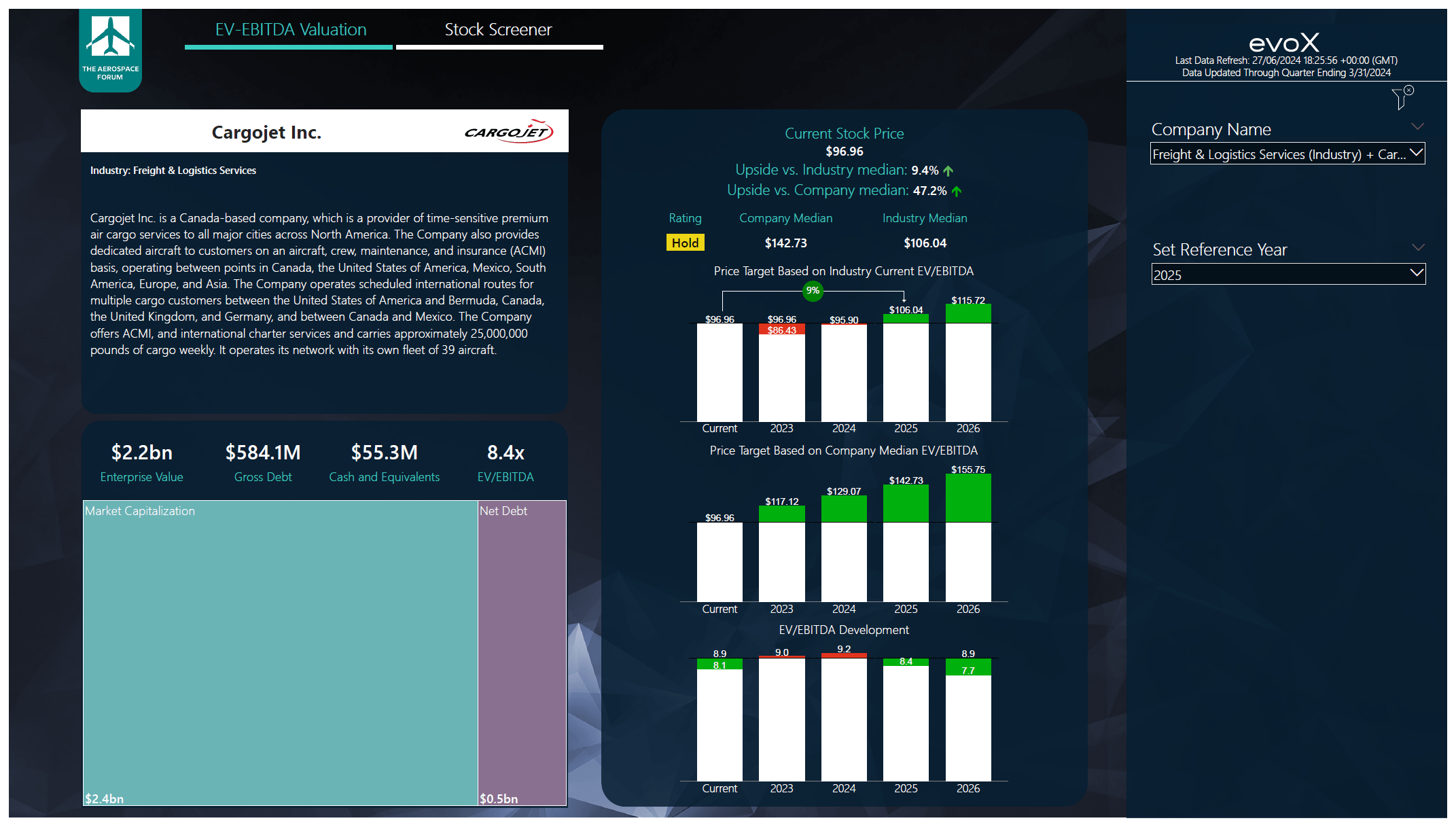

After reviewing the most recent earnings, I do see some upside. The company is executing well on its cost reduction and optimization efforts. However, EBITDA projections have come down by around 7% and 4% for free cash flow. Using an industry valuation, which, I believe, is fair at this point, there remains 9% upside for Cargojet stock, but I feel comfortable with the Hold rating.

Conclusion: Cargojet Is A Nice Stock To Hold

Cargojet has a nice business model with revenue protection in the form of fuel pass through, minimum guaranteed volumes and CPI-driven revenue adjustments. In times like these, with pressure on freight rates and some demand softness persists, we see that Cargojet is seeing quite strong protection on revenues while it is also managing to keep cost stable, neutralizing cost inflation. That all shows that the business model is resilient and, as a result, I am maintaining my hold rating for the stock as I also recognize that forward projections have come down a bit.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.