Justin Sullivan

Carvana Co. (NYSE:CVNA) inventory is up a mind-boggling 660% YTD, totally on the again of higher than anticipated Q2 earnings and fixed fears/hope of a short-squeeze. The short-squeeze argument does have some deserves as practically 38% of the float has been shorted in accordance with Searching for Alpha information. However, chasing the inventory right here is prone to find yourself harming the common investor (or dealer). I’m presenting 5 causes right here to sway the common investor or dealer from this inventory. Allow us to get into the main points.

CVNA Inventory (Seekingalpha.com)

Trade Challenges

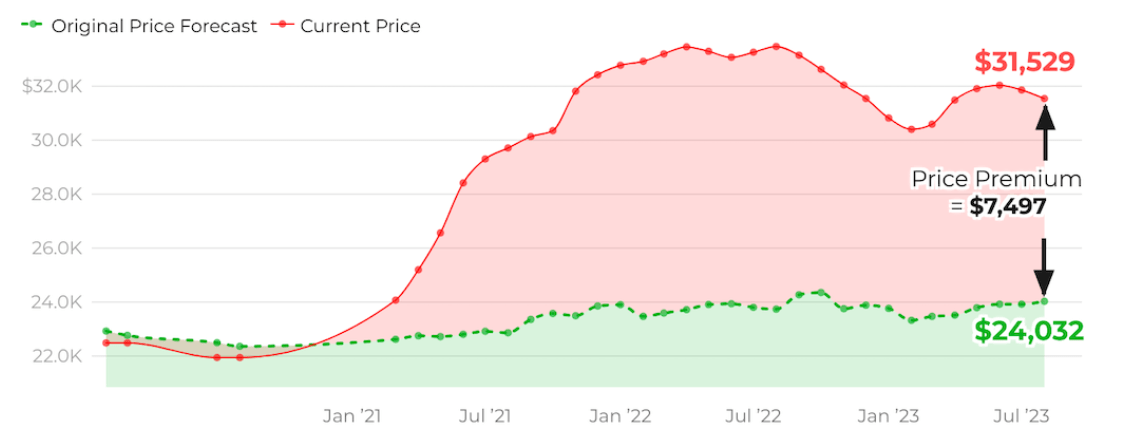

Whereas Carvana lately reported a slight headline beat in its Q3, the reported web earnings of $49 million loses its shine while you issue within the curiosity expense (coated beneath). As well as, whereas used automobile costs have fallen a bit lately, they’re nonetheless buying and selling fairly near their peak than their trough. Used vehicles are nonetheless trading at 30% greater than their historic regular and I’m not getting a rosy image in my thoughts about Carvana’s operations when costs do return to regular.

Used Automobile Premium (ktvz.com)

Let’s not neglect aggressive threats from present or new, stronger gamers. For instance, I imagine Amazon.com (AMZN) is a menace for anybody and everybody with their distribution system and basic ecosystem energy. Therefore, it was not shocking when information broke out that Amazon had partnered with Hyundai Motor Firm (OTCPK:HYMTF) to promote vehicles on-line.

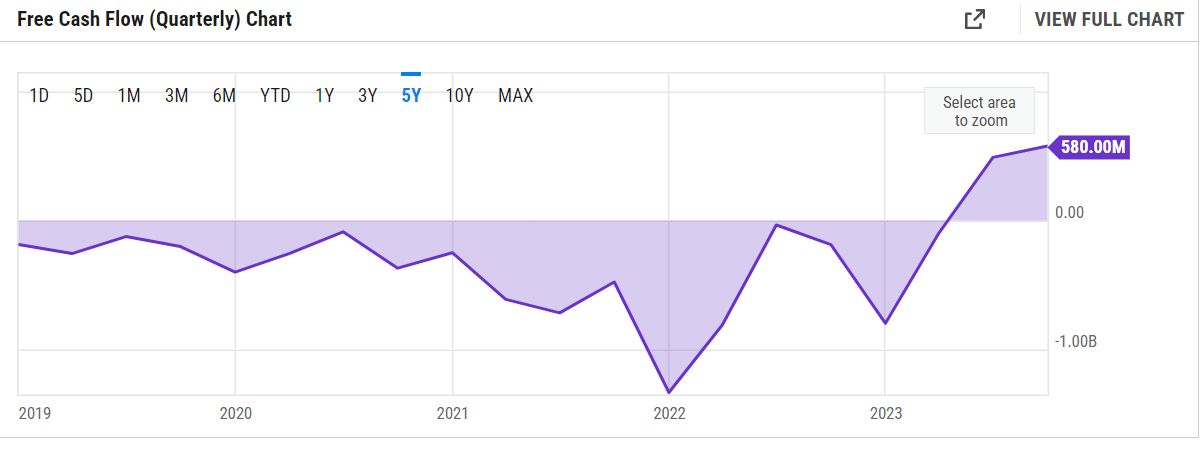

Free (of) Money Movement

It might shock you to listen to now in hindsight that Carvana was not Free Money Movement [FCF] optimistic even on the top of inventory optimism in 2021. Certain, I get that they provide loans and therefore FCF will not be a great metric right here like it’s not for Banks however Carvana’s working earnings shouldn’t be an image of consistency both with solely the final two quarters displaying optimistic working earnings. And let’s not neglect that working earnings excludes taxes and curiosity expense and including these to the equation make issues worse for Carvana. However let’s neglect about taxes and focus simply on curiosity expense on debt beneath.

CVNA FCF (Ycharts.com)

CVNA Working Revenue (Seekingalpha.com)

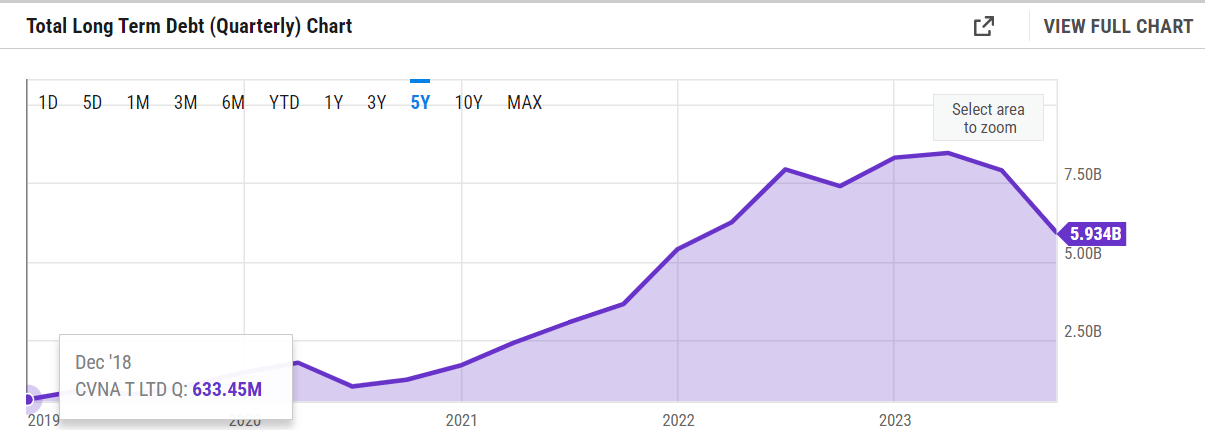

Mounting Debt

Carvana’s long-term debt has grown practically 10 folds within the final 5 years, reaching practically $6 billion on the finish of the latest quarter. Clearly, this isn’t a recipe for fulfillment within the present high-interest fee atmosphere as the corporate is constantly shelling out greater than $150 million/quarter in the direction of curiosity expense on debt. This quantity (curiosity expense on debt) has grown 5 folds since March 2021.

One other option to perceive the enormity of the debt scenario is by wanting on the firm’s market capitalization. With a market cap of $7 billion, Carvana carries a debt load that’s 85% as huge as its general price.

CVNA Debt (YCharts.com) CVNA Curiosity Expense (Seekingalpha.com)

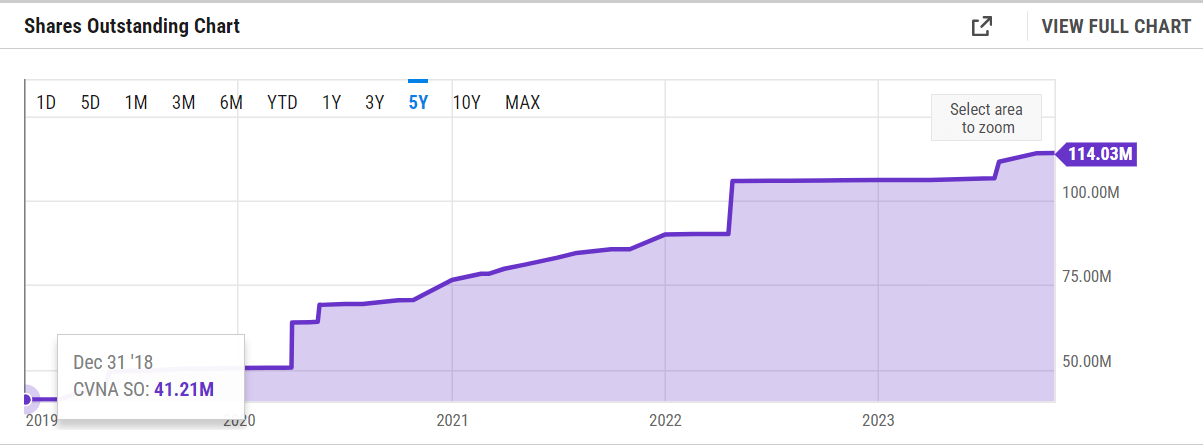

Diluting Away

When firms run into difficulties producing money on their very own and are already leveraged sufficient, the subsequent logical avenue is the market or new buyers. Carvana’s whole shares excellent has nearly tripled within the final 5 years, reaching a excessive of 114 million shares on the finish of the latest quarter. I count on additional dilution as the corporate is prone to wrestle given the macro and basic challenges defined above.

CVNA Shares Excellent (YCharts.com)

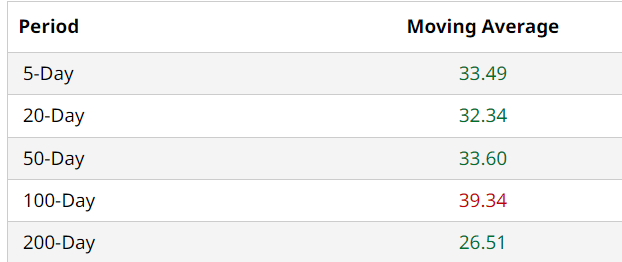

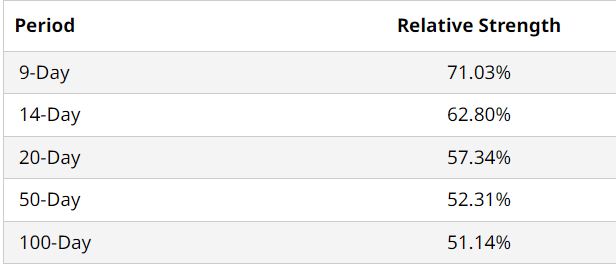

Technical Setup

The current energy proven by the inventory has pushed its Relative Power Index [RSI] near the overbought stage of 70. Curiously, regardless of that, the inventory is buying and selling about 10% beneath its 100-Day shifting common. I’m extra intrigued by the truth that the 200-Day shifting common is greater than 20% beneath the present market worth and that means the inventory has methods to fall earlier than getting long run assist ought to it fail to clear the 100-Day common.

CVNA Transferring Avgs (barchart.com) CVNA RSI (barchart.com)

Conclusion

Certainly one of my favourite adages concerning the market goes one thing like “The market can stay irrational longer than one can stay solvent“. Shopping for Carvana right here within the hope of a short-squeeze is insanity. Shorting the inventory based mostly on fundamentals may very well be madness. The prudent factor to do is to remain away you probably have no place and to promote in case you maintain it. Certain, you could be down fairly a bit in case you obtained caught up within the 2021 shopping for frenzy however at the very least you’re 6 folds higher now than originally of the yr. I firmly imagine this firm is unlikely to exist in its present kind 5 years from now. Coping with such shares shouldn’t be investing and never even buying and selling. It’s speculating. Don’t speculate.