Brandon Bell

Introduction

Carvana’s (NYSE:CVNA) “hot days” appear to be over, or aren’t they? Nicely, the latest rise within the share worth is actually one thing to notice.

What I like about Carvana is that they use Carlypso to do knowledge evaluation of their automobiles. This might give them a powerful benefit over others within the business. Nevertheless, Carvana has not satisfied me that it may well proceed to develop and be worthwhile on the similar time.

There are additionally many speculators available in the market who’re going brief in Carvana’s inventory. I see this as a short-term catalyst. However I need to purchase long-term. I’m searching for catalysts and long-term features whereas attempting to know the dangers of investing in Carvana.

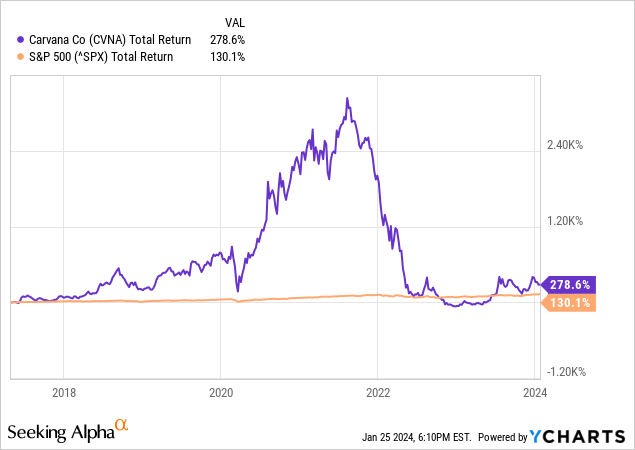

Traders have been enthusiastic about Carvana shortly after the COVID-19 interval. The inventory worth skyrocketed from $35 in 2020 to a document $360 in 2021.

However what has risen sharply also can fall sharply. The share worth has undergone a pointy correction and is now buying and selling at $40.

Excessive volatility is actually not for everybody.

There are two development catalyst that may elevate the inventory worth:

- Robust value discount, enchancment in GPU and adjusted EBITDA.

- Dovish Fed coverage which might cut back rates of interest sooner than anticipated.

In my article I talk about its development catalysts, however I additionally talk about different components that prevented me from shopping for the inventory. I concluded that there are higher alternatives in the marketplace that even have Carvana’s development issue, however with much less danger.

Aggressive Benefits of Carlypso

Carvana is an e-commerce platform and primarily generates income from the acquisition and sale of used vehicles. A aggressive benefit of Carvana is contactless supply and pickup. Clients can decide up their automobile with out the intervention of an worker.

One other aggressive benefit of Carvana is Carlypso. Carlypso is an analytics software that integrates knowledge analytics and machine studying into the shopping for and promoting course of. This offers Carvana a extra detailed image of the upkeep the automobile wants, what it prices, and what it finally pays for.

Shopping for and promoting used vehicles entails monetary dangers which might be tough to manually estimate upfront.

Automobile depreciation is a monetary danger that varies by automobile model and kind. Automobile depreciation will depend on each the age of the automobile and its mileage. The mileage of their gross sales fashions doesn’t enhance of their showroom. However annual depreciation is a crucial consider figuring out the gross sales worth.

Liquidity danger may also be recognized. For Carvana, it is very important discover a good combine between automobile mannequin depreciation and marketability. The depreciation of unpopular automobile fashions could be larger than that of in style automobile fashions. It is very important maintain observe on this. These are very complicated points that require intensive market analysis. Carlypso can conduct this market analysis that provides Carvana a aggressive benefit.

Carvana Is Nonetheless On The Studying Curve

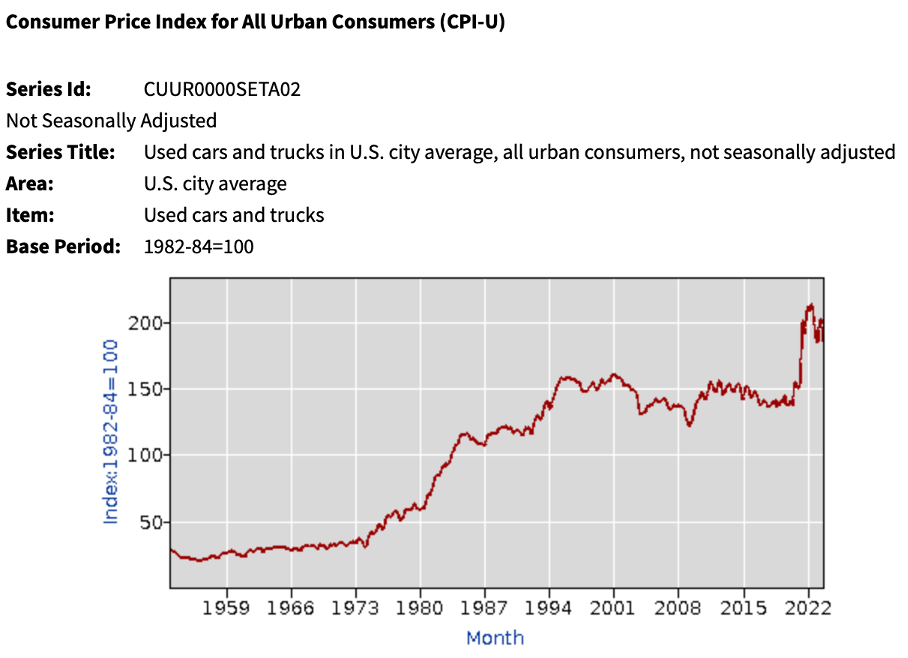

The worth of vehicles decreases as they’re used and as they age. Nevertheless, the massive image exhibits that used automobile costs have risen sharply over the previous 70 years. This is because of inflation, demand, but additionally as a result of vehicles are actually outfitted with technological devices that add extra worth.

The used automobile worth pattern exhibits that used automobile costs have modified little between 1994 and 2020. The massive worth enhance after 2020 might point out sturdy demand for used automobile fashions. Low rates of interest made it fascinating to get low-cost financing, which increase gross sales.

Now that rates of interest are so much larger, the image could look completely different in a couple of years.

CPI-U (U.S. Bureau of Labor Statistics)

Carvana made good use of the engaging rates of interest on the time and elevated inventories considerably. Because of this, their money owed elevated from $1.7 billion to $5.4 billion between 2020 and 2021, whereas their money place elevated by solely $100 million.

General, inventories elevated by $2.7 billion throughout this era. Demand for used automobile fashions by these automotive sellers was considerably excessive throughout this era. The elevated demand could clarify why used automobile costs rose a lot.

Complete Inventories (Personal evaluation)

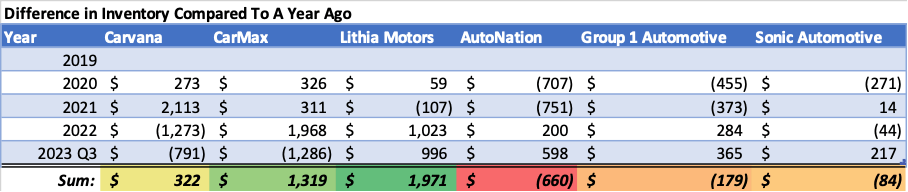

My query is whether or not the elevated demand was additionally felt by customers, or solely by automotive sellers? The stock to income ratio could give me some perception into this.

Distinction in Stock Ranges (Personal Evaluation)

The typical stock to income ratio exhibits how effectively automotive sellers handle their stock. An excessive amount of stock prices pointless storage and financing.

We see that the typical stock to income ratio remained virtually the identical for Carvana through the interval and truly decreased for different automotive sellers. The sturdy demand for used vehicles was additionally felt by customers and Carvana was in a position to make good use of the engaging financing phrases on the time.

However the ratio was barely larger in 2022 than in different years. Different automotive sellers noticed their inventories fall sharply.

This makes me marvel if Carvana adequately anticipated a potential drop in gross sales throughout that interval of rising rates of interest. For my part, their analytical software Carlypso ought to be capable to correctly assess this danger.

Carlypso ought to have recognized these dangers and recommended much less inventory in intervals of low demand (throughout sturdy rate of interest rises). I do not assume it has achieved this effectively. Both manner, I believe that Carvana remains to be on the training curve whereas making nice leaps ahead.

Common stock/income ratio (Personal calculations)

Carvana Has Its Prices Nicely Below Management

Carlypso ought to give Carvana aggressive benefits, which I believe ought to enhance profitability. However for a few years, profitability has lagged behind opponents.

Nevertheless, gross margin for the latest third quarter got here in surprisingly excessive at 17%. The cost control program contributed to this outcome.

Gros margin of business friends (Personal calculations)

Carvana made sturdy progress in chopping prices in lots of areas:

- Over the previous 12 months, $900 per unit has been saved on non-vehicle retail prices.

- Since 2021, $1,400 per unit has been saved on wholesale automobiles and prices.

- Carvana has saved $400 per unit in promoting prices by eliminating spending in decrease efficiency channels since 2021.

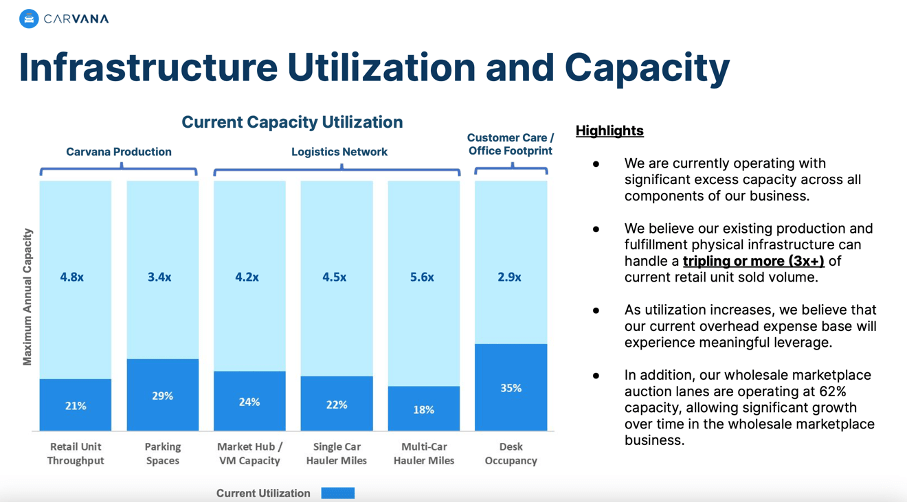

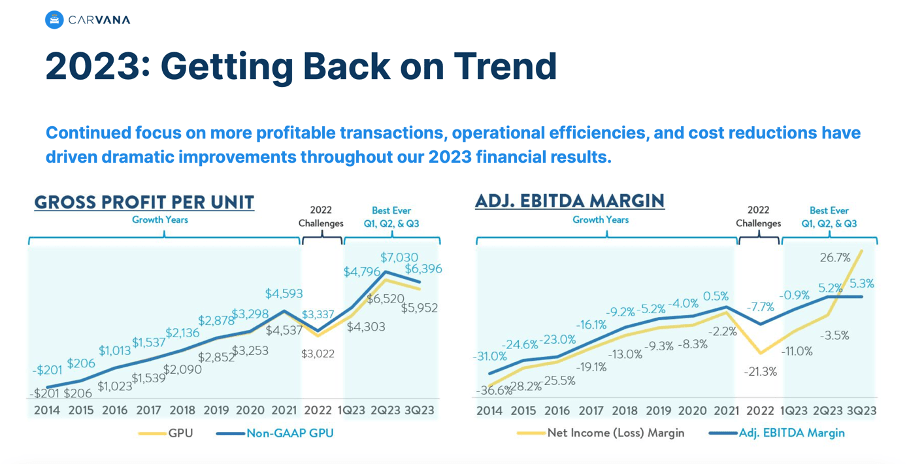

Their value financial savings resulted in development of their gross revenue per unit, which has improved considerably through the years and is now about $6,400 per unit.

Infrastructure Utilization and Capability (November 2023 Value Construction Particulars.)

Carvana expects additional financial savings on non-vehicle and wholesale automobile prices within the coming quarters. Carvana focuses on the following objectives:

- Drive the enterprise to optimistic Adjusted EBITDA.

- Drive the enterprise to vital optimistic unit economics.

- After finishing steps 1 and a couple of, return to development.

These objectives will present additional development fueled by earnings and also will cut back their debt. Carvana is presently on the inflection level to refocus on development. As talked about earlier, GPU has improved considerably and is now round $6,400 per unit. The adjusted EBITDA margin has additionally improved to five.3%. These are optimistic developments for the close to future.

Non permanent Headwinds

2023: Getting Again on Development (2023 RBC Capital Markets International Expertise, Web, Media and Telecommunications Convention)

Traders have been smitten by Carvana’s third-quarter results. Internet revenue was $741 million and adjusted EBITDA was $148 million. Carvana achieved objective one, as described in my earlier paragraph. The achieve in web revenue was primarily on account of features from debt discount.

Trying forward, Carvana expects some headwinds from the difficult automotive market. The corporate additionally expects a sequential decline in unit gross sales for the fourth quarter of 2023. Nevertheless, gross revenue per unit remains to be anticipated to exceed $5,000 per unit plus optimistic adjusted EBITDA for the corporate. For the total 12 months 2024, the corporate expects development in GPU and adjusted EBITDA.

And for my part, the dovish fed is a powerful catalyst for Carvana. The Fed goals to chop rates of interest sooner than anticipated. This might increase Carvana gross sales as extra customers take out (cheaper) loans to finance their automobile.

Debt Devices

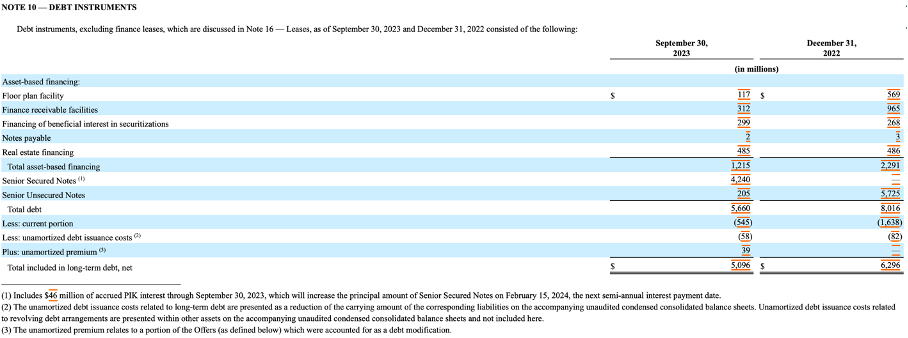

Whereas Carvana is investing closely in development, debt has additionally risen to worrisome ranges. Complete debt stands at $5.9 billion, however the firm has $544 million in money and marketable securities on its stability sheet.

The excessive debt degree might grow to be problematic if Carvana can’t enhance its profitability. Twelve-month curiosity expense is $620 million, whereas working margin remains to be on the verge of profitability.

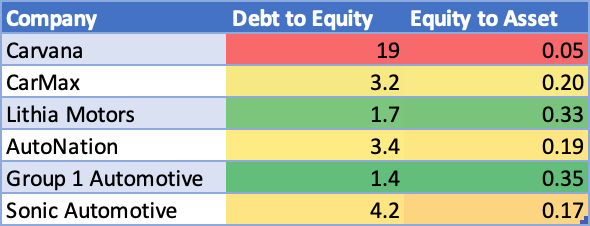

Taking a look at different debt ratios, similar to debt-to-equity and equity-to-assets, Carvana seems overleveraged. The extremely leveraged place might have a powerful development impact if executed favorably. For my part, the dangers do not outweigh potential return however should be too excessive for extra conservative traders.

Debt to Fairness, and Fairness to Asset ratios (Personal calculations)

Not too long ago, Carvana lowered its single line of credit score to $1.5 billion by way of April 30, 2025. This additionally reduced the rate of interest to the bottom fee + 0.1% when quantities drawn beneath the ability are lower than 50% of the then present stock stability (base fee + 0.5% when withdrawn quantities exceed 50%.

Carvana’s debt devices (3Q23 Outcomes)

The brand new phrases are way more favorable as a result of the rate of interest was beforehand larger (the prime fee + 1%). The outlook can be in Carvana’s favor as a result of the Fed goals to cut interest rates within the coming years.

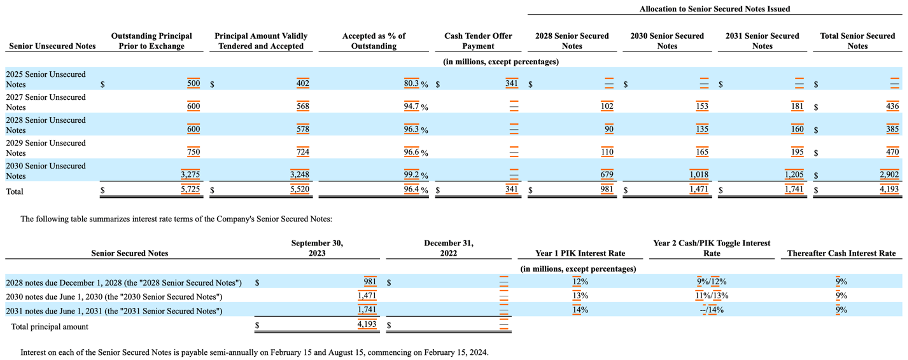

One factor to contemplate are the extra dangers because of the maturity dates of their unsecured bonds. These have been refinanced and can cost a major money rate of interest of 9% after 2 years.

Senior Secured Notes (3Q23 Outcomes)

Excessive Brief Curiosity As A Catalyst

The rise in Carvana’s share worth within the brief time period could be attributed to the closing of brief positions. Greater than 44% of the shares have been bought brief, which is so much. These positions ought to finally be closed by shopping for the shares, which I believe is a major catalyst. However it’s dangerous to purchase the shares solely due to the excessive brief curiosity.

The inventory is fascinating if the long-term prospects are additionally good. However I believe the chance is simply too excessive due to the excessive degree of debt.

Traders with a excessive danger tolerance could be excited by Carvana’s improved profitability and brief curiosity. However I’m ready on the sidelines till the debt is extra manageable.

Worthwhile Alternatives

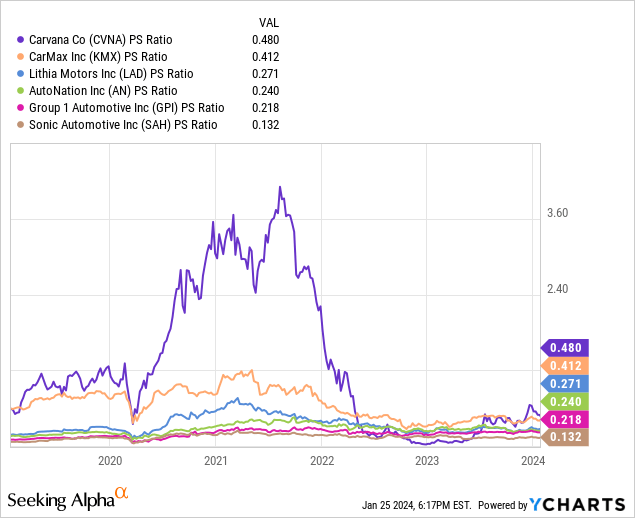

A closing perception into the inventory’s valuation tells us that Carvana is expensively valued if we examine its price-to-sales ratio to others within the sector.

Nevertheless, Carvana’s valuation is much more favorable than earlier than 2022. Traders then had wealthy prospects. However objectively talking, the inventory valuation was far too costly on the time.

For those who have a look at the basics, I believe there are higher alternatives in the marketplace. Though I have not dived deep into the sector comparisons, I observe that Lithia Motors (LAD) and Group 1 Automotive (GPI) are each low leveraged in comparison with the opposite corporations within the sector. The latter can be on a budget aspect given its valuation. An added plus is that they’re already very worthwhile.

Conclusion

Carvana makes use of Carlypso, giving it a aggressive benefit within the business. But Carvana remains to be struggling to be worthwhile. Due to this fact, this makes me query the effectiveness of their revolutionary developments.

Carvana is a development firm that achieves its development by way of vital leverage. Though the leverage is likely one of the highest within the business, it has resulted in Carvana’s income rising to $13.6B by 2022 (in comparison with simply $2B in 2018).

The risky automotive market mixed with excessive leverage can imply huge features or huge losses. Carvana’s gross sales development has stagnated considerably and its share worth has fallen sharply. However latest quarterly figures present confidence in improved profitability.

The expansion catalysts are improved profitability and the Fed trying to minimize rates of interest beginning in 2024. Nevertheless, there are higher alternatives in the marketplace which might be a lot much less dangerous and may present good returns.

Traders ought to check out Lithia Motors and Group 1 Automotive. Each have the benefit of a low debt degree and a good inventory valuation. Their gross sales are usually not rising as quick as Carvana’s, however the dangers and returns appear extra favorable than Carvana’s.

The underside line is that Carvana is a superb inventory for traders who can deal with lots of volatility. Carvana has Carlypso that provides it a aggressive benefit over business friends. Nevertheless, placing them into observe appears difficult for my part. Carvana’s sturdy development has been accompanied by a wealthy inventory valuation. Brief sellers could get nervous as Carvana will get its prices beneath management and improves its profitability. This might trigger the inventory worth to rise sharply on the brief time period.

However, I believe there are a lot of different alternatives which might be a lot much less dangerous and may supply first rate returns. Carvana is due to this fact a maintain.