LauriPatterson/E+ via Getty Images

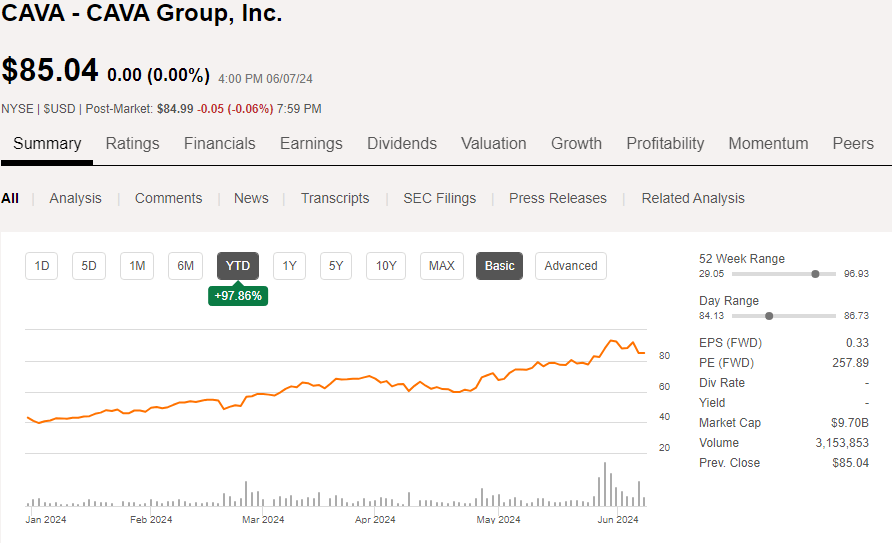

The fast-casual Mediterranean restaurant, CAVA Group (NYSE:CAVA), has had an exceptional run-up in its stock price YTD and is up over 100% from its January lows; the momentum behind this ticker has been incredible over the past few months as investors have been piling into the growth story.

CAVA YTD Chart and Metrics (Seeking Alpha)

Fundamentally, this appreciation is due to a handful of drivers:

- 30%+ YoY sales growth over the past couple of earnings reports

- High average unit volume with potential for strong same store sales growth moving forward

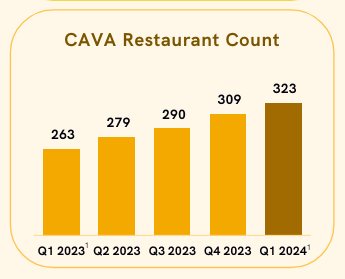

- Completion of Zoës Kitchen conversions to CAVA storefronts following the 2018 acquisition, bringing total footprint to 330+ locations

- A general sentiment that CAVA could be the “next” Chipotle (CMG)

- Prevalence of momentum-based trading in 2024 markets

Coming out of their Q1 FY24 earnings report where the company posted a top and bottom-line beat with a raise in full-year guidance, the stock has traded up as high as +20%. However, we are seeing extreme price volatility as traders take profits while the market tries to make sense of the valuation.

As of writing this article, CAVA is trading in the range of 12+ TTM price/sales, or 10+ forward price/sales, based on 2024 full-year guidance at the mid-point.

CAVA 10-Q

I personally think that the current valuation is quite pricey for a restaurant, and may be stretching thin. However, if CAVA can continue executing at this level and employ their long-term growth strategy, they may be worth the investment at current levels with outsized returns over the next decade.

CAVA Fundamentals and Growth Story

When looking at the growth case for CAVA, we can hone in on three of management’s primary objectives that the business operates around; (1) continued expansion into new regions and locations, (2) maintaining strong restaurant-level profit margins, and (3) grow same restaurant sales growth to maximize existing stores.

Restaurant Growth

CAVA FY24 Q1 Presentation

As of the end of FY23 Q4, CAVA had finished converting all acquired Zoës Kitchen locations into CAVA storefronts. These conversions provided a relatively easy expansion plan since many of them were well established and could provide semi-seamless transitions into “new” CAVA revenue streams.

However, the company must now fully rely on their own internal scouts and real estate teams to build out an expansion pipeline. This is in contrast to converting existing Mediterranean serving storefronts (Zoës Kitchens) as a method of boosting CAVA sales. It is more difficult to successfully implement a sales and marketing plan to bring a new cuisine to a neighborhood versus converting an existing Mediterranean restaurant. There is likely substantial customer carryover in the latter of the two.

With that said, during FY24 Q1, CAVA did open a new store in Chicago (among others), which was their entry into the upper Midwest market. CEO Brett Schulman had the following to say about the new opening in this large market:

The restaurant is delivering exceptional results and generating significant buzz. Our team once again showed the power of our category defining brand, and how we are amplifying the passion of existing fans, engaging new consumers, and rapidly converting them to customers. Our Chicago launches a microcosm of what we see across the country. As CAVA grows, so does the passion for our brand, and we are increasingly becoming part of the cultural conversation.

CFO Tricia Tolivar then had the following to say about their new Q1 openings, in general:

So in fact, our new units are performing very well. One thing to keep in mind as you think about the first quarter, much of the new restaurant openings that we had were in the beginning of the quarter. So that has some impact when you’re factoring in new unit productivity. But when you actually look at restaurant operating weeks themselves and looking on that basis.

Their tone and verbiage sounds promising regarding the success of their newly opened operations. However, I look forward to seeing more data on how these locations are performing and how CAVA greenfield average unit volumes (AUVs) develop throughout the year. If we see some new locations or regions lagging the AUVs of their existing stores, we will want to make a note of this.

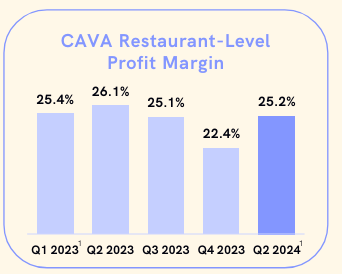

Restaurant-Level Margins

CAVA FY24 Q1 Presentation

Another key performance indicator in the restaurant business is store-level profit margins which includes things like food and beverage, labor, utilities, and occupancy costs. If the restaurants themselves are operating efficiently, then other corporate level expenses such as G&A, pre-opening, and so on should diminish, relatively, with scale.

In general, the CAVA restaurant-level margins are acceptable, but must continuously be monitored. There are constant forces that tend to contract these operating margins, including food, packaging and input inflation along with labor (wage) increases. For instance, AB 1228 in California recently set the new minimum wage for fast food restaurant employees to $20/hr.

According to CAVA, their average wage costs increased 8% year-over-year in FY24 Q1. There is a fine line to tread when it comes to employee retention in hourly work; maintaining skilled and trained workers while simultaneously protecting margins. CAVA is in the process of deploying a labor improvement initiative, which is meant to reallocate working hours in a more efficient manner. Here is CEO Brett Schulman on the progress:

This initiative is net-neutral from a labor dollars and labor hours standpoint. The focus of this test, is on reallocating hours to deliver better food, better hospitality, and more efficient speed of service. Early results are promising, and we are hearing excellent feedback from the team, such as more time to coach and train, more time to interact with guests, and an even more positive work environment.

Otherwise, the company does see some pricing inflation headwinds in their chicken inputs, along with the new steak launch which is being rolled out now. They’ve said in the past that they are hesitant to pass on too many costs to the consumer, so we will need to keep an eye on pricing and how it impacts their operating margins.

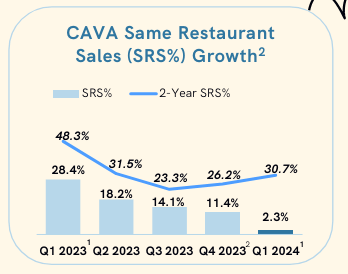

Same-Store Sales Growth

CAVA FY24 Q1 Presentation

The third and final primary CAVA growth pillar is their same restaurant sales growth. This is the area that introduced many question marks in their most recent quarterly earnings report and will be the most important driver towards overall company growth.

As can be seen in the above chart, their same-restaurant sales (SRS) growth is on a downward trend, year-over-year. They most recently reported 2.3% growth, comparing Q1 FY24 to the quarter a year earlier. Here is an excerpt from CFO Tricia Tolivar during their earnings call:

CAVA’s same restaurant sales increased 2.3%, driven by a 3.5% increase from menu price and product mix, partially offset by a decline in traffic of 1.2%.

So they actually saw a traffic decrease during the quarter, and made up for it via menu price increases. As an investor, this is a troubling sign, as we’d obviously prefer to see the trend going in the opposite direction.

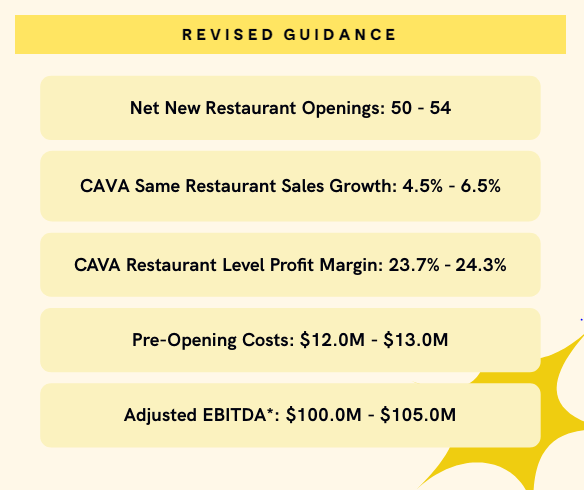

They did note that they expect SRS% to be 5.5% for the year at the midpoint in their updated guidance:

CAVA F24 Q1 Presentation

This implies a high single-digit growth rate for the remainder of the year, which is good news. However, in this incredibly unsure macro-environment, we will have to keep a very close eye on this. If we go another quarter or two with diminished store traffic, it will throw a big wrench into their short-term growth story.

Just for a point of comparison, over the past 5 years, primary competitor Chipotle has posted an average SRS growth of 9.64%. In their most recent quarter, they reported 7% comp growth.

If CAVA is going to be the “next Chipotle”, we need to see some improvements here.

Valuation

Taking all of this and applying it to a valuation, I want to map out their sales growth over the coming years, and then decide how much I’m willing to pay for those sales as a multiple. I’m going to provide a straightforward opportunity-cost based valuation to the company by building a 10-year revenue model and then applying a few price/sales ratios depending on execution and growth sentiment.

My revenue model will be built on just two metrics as a simplified way to forecast top-line growth:

- Comps growth (same store sales growth)

- Annual net new store openings growth

With these two metrics, we can chart out the number of CAVA locations over the next decade, and then apply an AUV to each location, bearing in mind that new openings during the year will not reach full AUV.

One caveat to this approach is the large assumption that CAVA will maintain strong restaurant-level profit margins, which will eventually trickle down to the bottom-line as they scale operations. This will chip away at the outlandish 200+ P/E they are currently trading at. The above caveat should not be understated, as it requires strong execution to grow earnings in the incredibly competitive restaurant industry.

Revenue Model

Below are the assumptions I’m using for different revenue and valuation cases. Please note that I’m not referring to any of these as “bear” cases because they are all bullish in nature. There is the distinct possibility that CAVA sees short or long-term negative growth rates across any number of metrics due to shifting consumer appetites, regulatory or legal issues, expansion difficulties, unforeseen challenges (i.e., Chipotle E.coli issue) and so forth.

In each of my cases, you’ll see the annual comp growth, growth of net new openings, and the price/sales I’ll apply to the valuation which typically is larger for companies with high growth and execution, and lower for more mature or slower growing enterprises.

Case Assumptions (Self-made)

The base case is predicated on management’s target of 1,000 locations by 2032, and mid to high single-digit comp growth as guided. The high and low cases add and subtract a premium from the base case metrics. In general, a revenue model like this should be treated as a guideline. Some years may be higher, some may be lower, but on average, it can give you a good sense of what the growth trajectory might be.

Base Case Model

Base Case Revenue Model (Self-made)

High Case Model

High Case Revenue Model (Self-made)

Low Case Model

Low Case Revenue Model (Self-made)

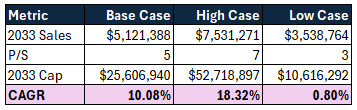

Each model forecasts annual revenue through 2033 based on the number of restaurants and average unit volume. Here are the 2033 sales results, and the 10-year CAGR based on an investment today versus implied 2033 market capitalization:

Self-made

When investing in individual stocks, it should be your goal to produce excess returns over an index, such as the S&P 500 Index (SP500) which has historically returned ~10% annually on average.

Under the base case assumption, we essentially forecast matching the index, and on the low case, substantially underperforming even risk-free assets. The high case model does show potential for outperformance, and thus should be viewed as the true bull case. This will require the company to get back towards double-digit comp growth and exceeding their expansion goals.

Risks and Takeaways

Based on what we are currently seeing from the company, I find it too risky to invest in CAVA at its current valuation based on forecasted sales growth. Even taking on a bullish sentiment during modeling yields questionable return on investment opportunity.

We could invest in the S&P500 for similar returns with far less risk.

Here is a gentle reminder that the above cases imply continued execution and positive growth. These models would completely break down if the company starts running into expansion problems, contracting margins, or shrinking AUVs. These are all very real threats that plague this industry!

I’ll continue monitoring and listening into their quarterly calls; here are a few of the primary points I’ll be monitoring:

- How is their expansion strategy going, and how are new locations performing as compared to their developed markets?

- Are they maintaining strong restaurant-level profit margins (bottom-line growth will come as they scale)?

- Can they drive comp growth back up towards the double-digit level in the coming years?

Personally, I’m a big fan of CAVA and have been long up until recently when I sold my position just before their Q1 earnings call. However, I believe that their valuation has come too far too fast this year, and the numbers just do not make any sense to me based on my models and common sense.

Next Steps

All-in-all, I would not be surprised if we see a sizeable pull-back over the coming months leading up to the next earnings report. I think that CAVA has incredible potential as a fast-casual growth story, and I do love their food. However, they still have a ton to prove and, in my opinion, are overextended at current prices. I’ll continue following their story and will look for a better entry point assuming management and operations continue executing at high levels.