tadamichi

Welcome to a different installment of our CEF Market Weekly Evaluate, the place we focus on closed-end fund (“CEF”) market exercise from each the bottom-up – highlighting particular person fund information and occasions – in addition to the top-down – offering an summary of the broader market. We additionally attempt to present some historic context in addition to the related themes that look to be driving markets or that traders must be aware of.

This replace covers the interval via the final week of March. You should definitely take a look at our different weekly updates protecting the enterprise improvement firm (“BDC”) in addition to the preferreds/child bond markets for views throughout the broader earnings area.

Market Motion

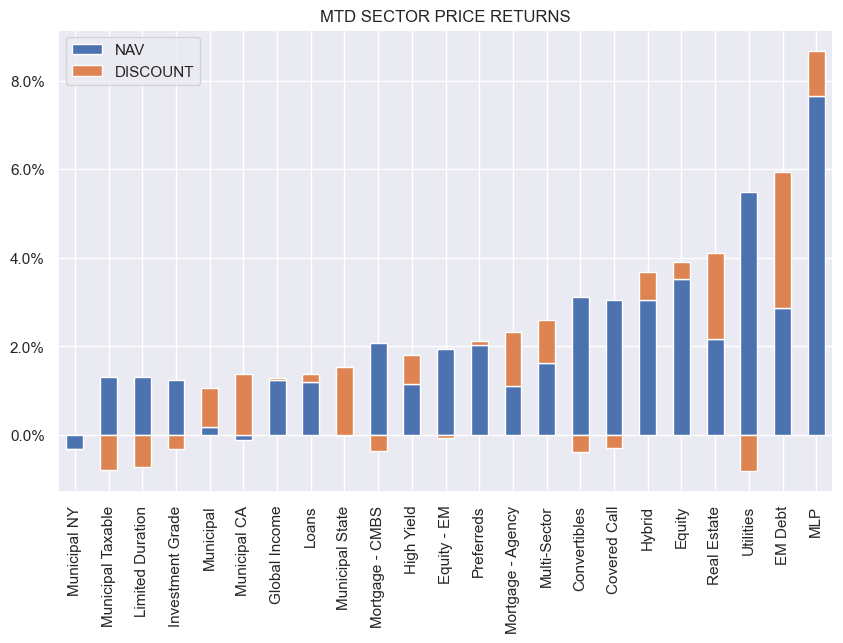

Most CEF sectors had been up on the week as soon as once more. Over March, all however one sector completed within the inexperienced with EM Debt and MLPs main the method.

Systematic Earnings

It was the fifth straight month of positive factors with March coming in because the best-returning sector up to now this yr.

Systematic Earnings

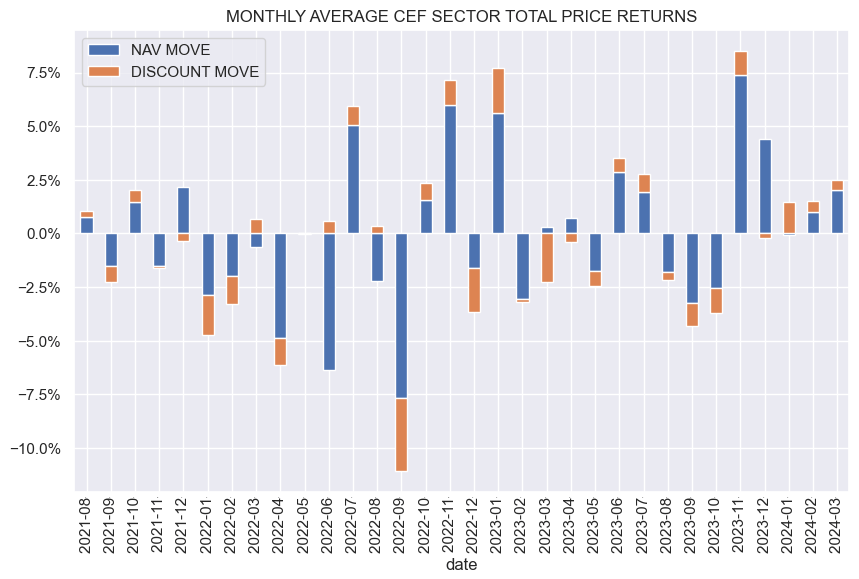

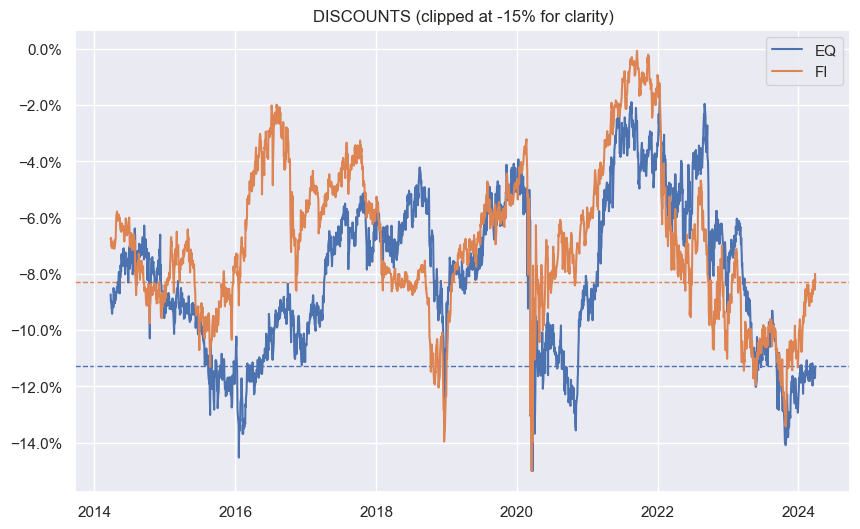

Fairness CEF sector reductions stay extensive at the same time as fixed-income CEF sector reductions have tightened nearer to their historic averages.

Systematic Earnings

Market Themes

One component of CEF investing that may sometimes disappoint traders is the lower than stellar longer-term NAV trajectory of many funds. We check out this dynamic within the context of the preferreds CEF sector during the last couple of years.

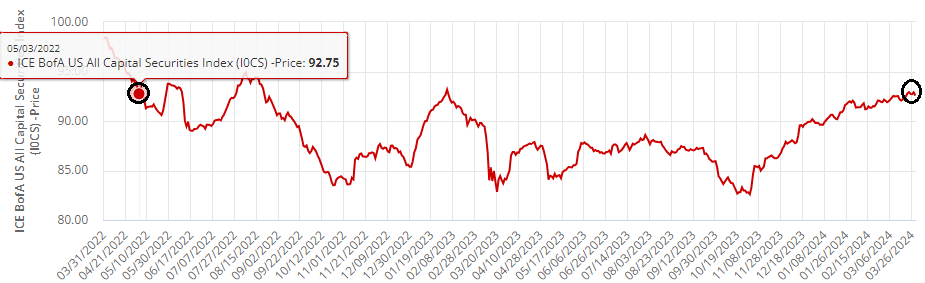

We begin with the broad-based preferreds index – the ICE BofA All US Capital Securities Index. To make issues easy, we determine a interval the place the worth of the index is unchanged. One such interval is 3-Could-2022 to 28-Mar-2024 as proven under.

ICE

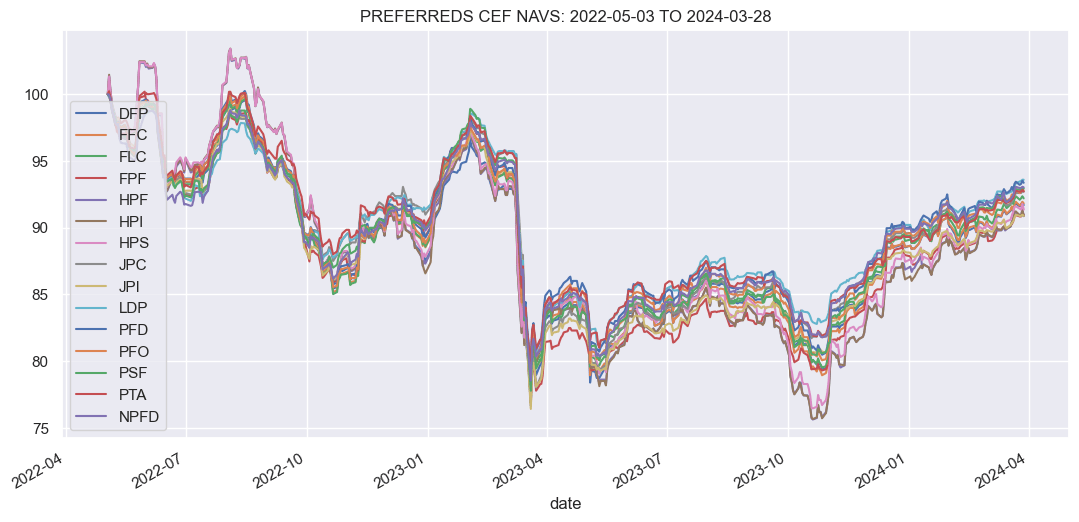

Now we take a look at the normalized (i.e. ranging from $100) most popular CEF NAVs throughout the identical interval and we see that, not like the flat value of the index, all fund NAVs had damaging returns, starting from -6% to -9%.

Systematic Earnings

Why is it that the index was flat whereas all CEF sector NAVs had been down?

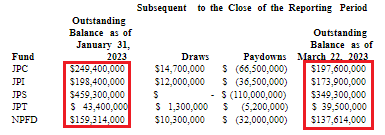

There are doubtless a few causes. One is deleveraging. When asset costs fall, CEF leverage rises. This makes it harder for the fund to keep up its stage of leverage, notably if the fund has a leverage cap. For instance, we see that between January and 22-March of 2023 – a interval that noticed a pointy drop in financial institution preferreds – Nuveen most popular CEFs shed financial institution borrowings. And though a deleveraging doesn’t assure a everlasting loss within the NAV, it usually leads to simply that because the funds usually wait to purchase again belongings when costs rise above the extent at which they had been offered (which lowers the funds’ leverage, creating extra room for added belongings). This “sell low, buy back higher” technique is a headwind to NAVs.

Nuveen

A probable second motive for the NAV drop in a flat index setting is the distinction between the funds’ portfolios and the broader index. Clearly, every fund will not be going to copy the index even when it had been doable – managers have their very own views and targets. Nonetheless, it does imply that fund efficiency can usually deviate from the index.

For instance, most popular CEFs had been obese contingent convertible securities and nonetheless are. These securities struggled within the aftermath of the Credit score Suisse failure when the Swiss regulator wrote down the CS CoCos to zero. CoCo and AT1 securities are lower than 20% of the broader market however many most popular CEFs maintain considerably in extra of that of their portfolios which triggered some ache final yr. This isn’t to say that over the longer-term this was a improper name nevertheless it doubtless ties into the deleveraging mechanism described above.

Nuveen

A probable third motive is overdistribution. Most credit score funds are likely to distribute greater than their web earnings stage and that is true of many most popular CEFs as nicely. This isn’t a giant deal from a complete return perspective nevertheless it does imply that the NAV can drop greater than anticipated.

First Belief

A fourth motive is just buying and selling slippage. Indices are primarily based off mid asset values and ignore any turnover prices which might add up over the longer-term. Hopefully, the alpha that managers generate can override this value nevertheless it doesn’t all the time.

Finally, there are a variety of mechanisms that may create headwinds to the NAVs of credit score funds relative to the underlying benchmarks. That does not imply that traders ought to keep away from CEFs. It does imply, nevertheless, that traders must spend time figuring out sectors the place benchmark underperformance can occur in addition to the funds within the sector which are able to outperformance for varied structural causes.

Market Commentary

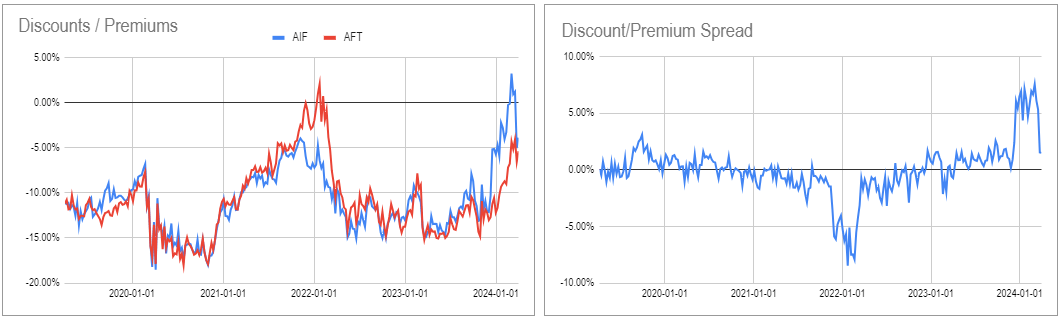

The 2 Apollo mortgage CEFs and AIF, particularly, have struggled over the previous week. Till a reversal within the final two days of the week, the AIF low cost widened 10% and the AFT low cost widened 5%.

It’s not clear what the catalyst for the AIF collapse is – it kicked off earlier than the latest SEC submitting which, as soon as once more, described the mechanics of the merger with MFIC, if permitted. If AIF returns to its current premium peak of three.3% (e.g. $15.37 value vs $14.87 NAV), the AIF investor would obtain 0.965 shares of MFIC for every share of AIF which equates to a price of $14.18. After that, every AIF share will get a further $0.25 fee as an inducement to vote sure which provides as much as $14.43. In different phrases, the AIF shareholder whose 1 share of AIF was priced at $15.37 finally ends up with $14.43 which does not seem to be a tremendous deal.

Now that the low cost has opened up in AIF, the mathematics makes rather more sense. In truth, if the AIF low cost widens additional in the direction of 10% it may even make sense to carry on to the fund and vote sure on the merger to select up round 5-6% of worth.

One other consequence of the current volatility in AIF and AFT is that the earlier uncommon valuation divergence we highlighted has principally closed.

Systematic Earnings CEF Device