Walter Bibikow

Introduction

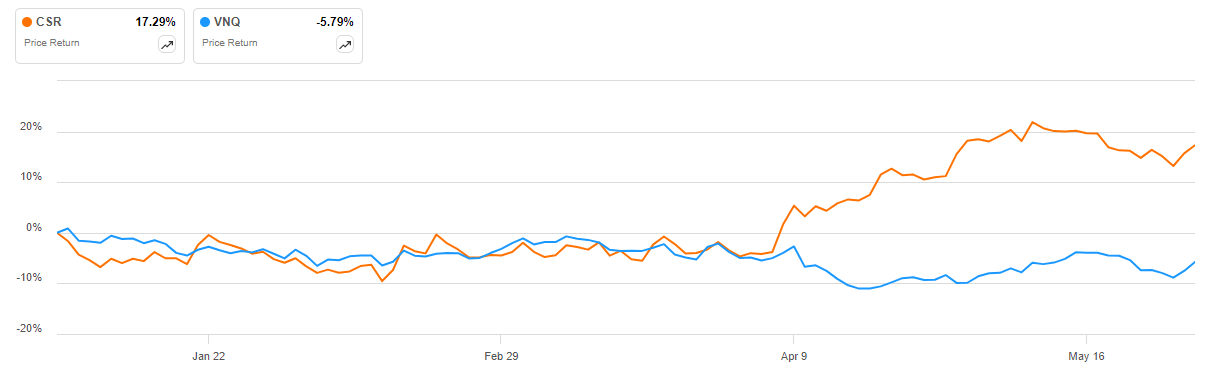

Centerspace (NYSE:CSR) has significantly outperformed the Vanguard Real Estate Index Fund ETF (VNQ) so far in 2024, with the REIT’s shares delivering a double-digit gain, significantly above the mid-single-digit decline of VNQ:

CSR vs VNQ in 2024 (Seeking Alpha)

Looking ahead, I think the company will continue to outperform, with a 7.5% market-implied cap rate, rising net operating income and a well-structured debt maturity profile, notwithstanding the somewhat elevated leverage and declining occupancy. I think management overhead appears quite bloated, and as such Centerspace could be an acquisition target in light of its attractive valuation but high administrative expenses.

Company Overview

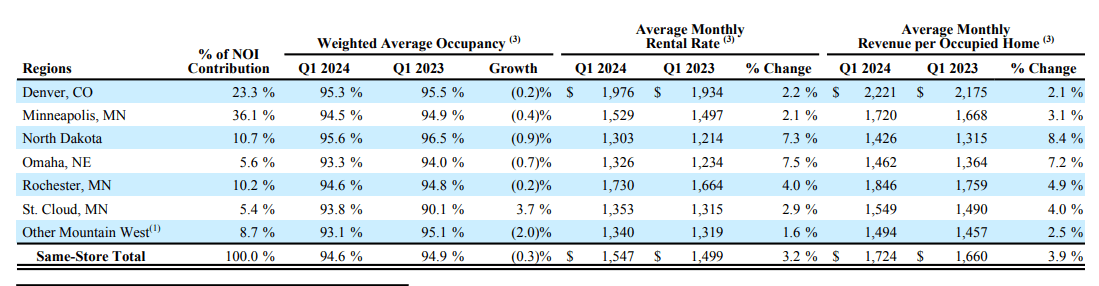

You can access all company results here. Centerspace is a Residential REIT that has interests in 70 apartment communities consisting of 12,883 apartment homes. The REIT is heavily concentrated in a few states, namely Minnesota (52% of total net operating income, or NOI), Colorado (23%), and North Dakota (11% of NOI):

Same-store portfolio overview (Centerspace Q1 2024 Financial Supplement)

Operational Overview

Centerspace reported occupancy of 94.6%, down 0.3% Y/Y, indicating some distress in the REIT’s portfolio, but overall a solid level for a residential REIT.

NOI developments were markedly move positive, with rising rents and lower expenses resulting in a very robust 7.5% NOI increase year-over-year. This drove Core FFO to 1.23/share in Q1 2024, 15% higher Y/Y. The strong Core FFO per share was also helped by a lower share count, with the company spending $4.7 million on share repurchases in the quarter.

Updated 2024 Outlook

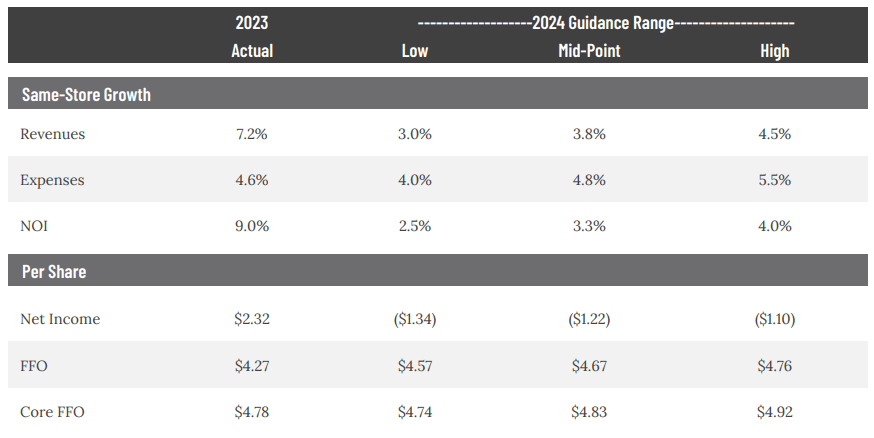

The strong start of the year prompted Centerspace to boost its low-end Core FFO guidance, with Core FFO now expected in a range of $4.74-4.92/share, up 1% Y/Y:

Updated 2024 Outlook (Centerspace June 2024 Investor Presentation)

The NOI outlook was also upgraded, driven primarily by lower expense growth. As a result, NOI is expected to increase by 2.5-4% in 2024.

Debt Position

The company ended Q1 2024 with a net debt of $916 million, implying that net debt accounts for 44% of the company’s enterprise value. It should also be noted that the company has preferred shares which account for 5% of enterprise value.

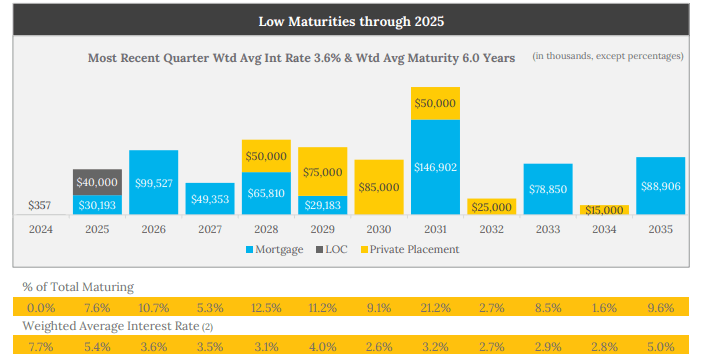

The average cost of debt is 3.6%, with a weighted average maturity of 6 years. What’s more, the company has just 7.6% of all debt maturing through 2025, with 42% of all debt locked at rates around 3% and expiring in 2030-2034:

Debt maturity overview (Centerspace June 2024 Investor Presentation)

As a result, the company will benefit from its tiered debt maturity structure for at least 6 more years before refinancing at higher rates kicks in.

Market-implied cap rate

Centerspace is expected to generate net operating income of about $157 million in 2024, which against an enterprise value of about $2.1 billion represented a very attractive market cap rate of 7.5%. General and administrative expenses are forecast at about $27.75 million, implying a 1.3% burden from management overhead, which is quite high.

Larger REITs could potentially bring the management overhead down to about 0.8% of enterprise value, indicating a takeover of Centerspace by a more efficient competitor could create significant value.

Synergies from a potential takeover

As highlighted in the above paragraph, I believe Centerspace is overspending on general and administrative expenses. AvalonBay Communities (AVB), the largest residential REIT in the United States by market capitalization, currently has an enterprise value of about $35.2 billion, and spent only $76 million on general and administrative expenses in 2023, as per its annual report. This represents just 0.2% of enterprise value spent on general and administrative expenses.

For comparison, Centerspace spent $20 million on general and administrative expenses in 2023, as per its annual report, representing almost 1% of its enterprise value. The difference to the 1.3% management overhead burden outlined above is made up by property management expenses which are not deducted from net operating income.

All in all, I believe it is reasonable to assume a larger peer could materially cut down on general and administrative expenses, resulting in a circa $10 million savings relative to enterprise value, or about $0.67/share boost to earnings on a common shareholder level, taking into account the current share count of 14.9 million.

Considering that the largest shareholders in Centerspace are Blackrock and Vanguard, each holding about 17% and 16% respectively, an opportunistic buyer is unlikely to face opposition from shareholders.

I should note there is no concrete evidence that a third party is planning to take over Centerspace, but the financial rationale is certainly there in my opinion.

Risks

The main risk facing Centerspace is its slightly elevated leverage, at 44% of its capital structure. This is offset by a favourable maturity profile and limited near-term maturities. That said, the company is actively buying back shares which boosts leverage even further.

Another thing to note is that occupancy is decreasing as the company is raising rents, indicating tenants are struggling to keep up with higher payments. If this trend continues, it would put the company’s strong NOI growth in question. This risk is somewhat mitigated by the low unemployment in the states where the company’s portfolio is concentrated, with Minnesota (2.7% unemployment rate) and Colorado (3.7%) both below the U.S. average of 3.9%.

Conclusion

Centerspace had a very strong start to 2024, with NOI rising 7.5% Y/Y, driven by higher rents and lower expenses. For the full year, the NOI increase is set to be more muted, by around 3.25%, as the company catches up with its expense spending.

The market-implied cap rate of 7.5% is very attractive for a residential REIT, although the high amount of administrative expenses does not allow the full amount to reach shareholders. As such I think the full value of Centerspace will only be unlocked by an acquisition by a larger player.

Thank you for reading.