John M. Chase/iStock Unreleased by way of Getty Photos

The electrical car (“EV”) charging station section continues hitting velocity bumps, with the sector now dealing with car demand points. ChargePoint Holdings, Inc. (NYSE:CHPT) was a first-rate instance of an organization missing the enterprise mannequin to deal with issues confronted alongside the supposed path to profitability. My investment thesis stays Impartial on the inventory with ChargePoint now buying and selling under $2, although the chance stays extra to the draw back than any main rally.

Supply: Finviz

Weak This fall

ChargePoint has seen gross sales collapse during the last yr, with the corporate reporting the next FQ4 ’24 numbers:

Supply: Searching for Alpha

Not solely did ChargePoint report a income decline of 24%, but additionally the corporate missed analyst estimates by over $4 million. Whereas the unhealthy information is that revenues slumped, the EV charging station firm did generate gross sales development in the important thing Subscription enterprise.

The difficulty with the enterprise was all the time the mismatch of the working expense base with the restricted gross earnings from Community gear the place nearly all of gross sales had been targeted. On the similar time, the inventory valuation soared primarily based on gross sales development of merchandise, although these gross sales supplied restricted monetary worth to the corporate.

ChargePoint nonetheless managed to report a $52 million web loss for the quarter, together with an adjusted EBITDA lack of $45 million. The EBITDA loss really grew from the $42 million loss final FQ4 in an indication of how chopping out low margin product gross sales have not actually helped the corporate enhance their monetary image.

The EV charging station firm solely produced a gross margin of twenty-two% with a gross revenue of $25 million. In essence, ChargePoint has to scale back the working expense base to this degree with the intention to be breakeven, or the corporate should hike margins and gross sales dramatically to spice up gross earnings.

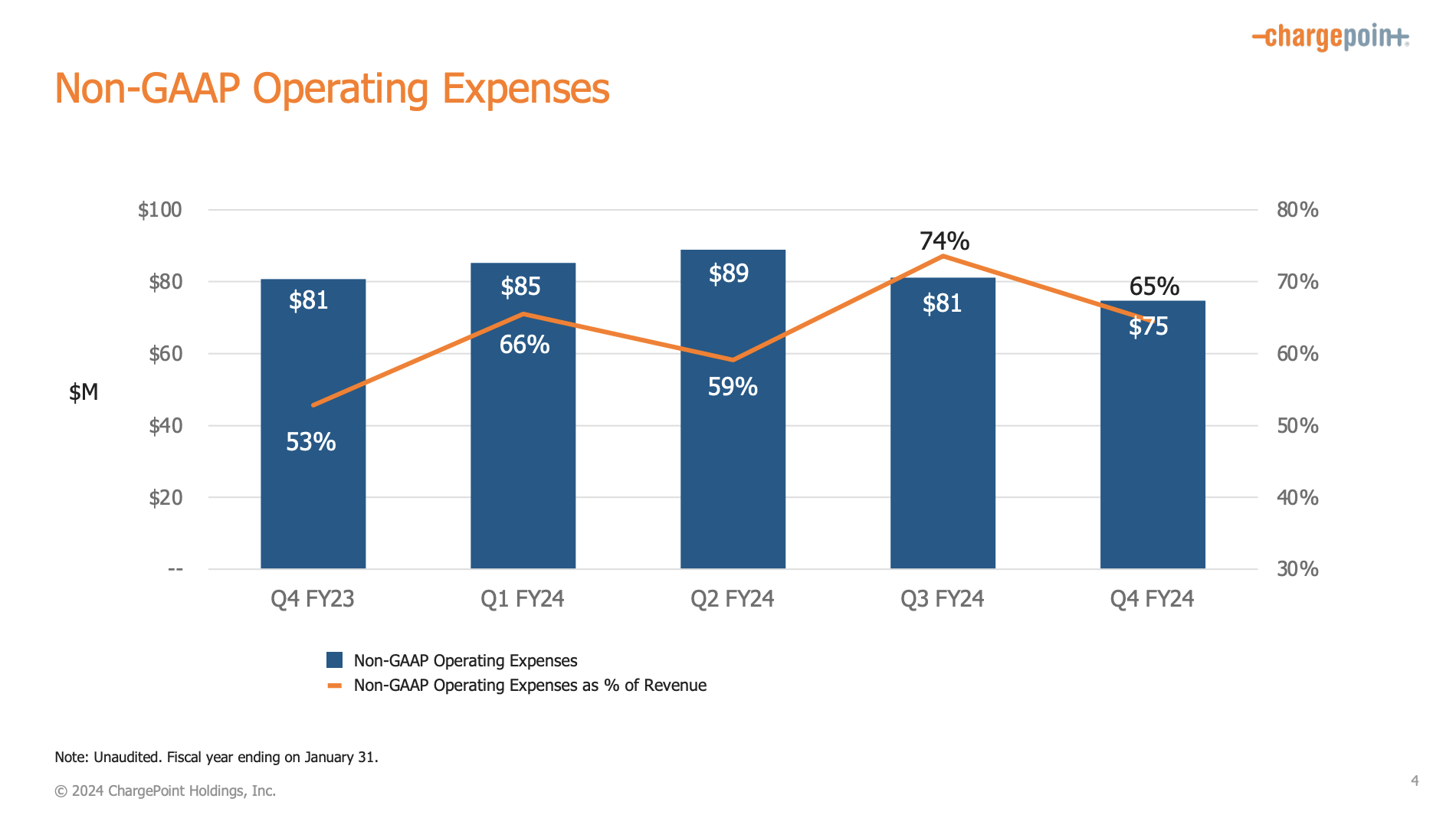

The corporate has lower working bills from the $89 million peak again in FQ2, however ChargePoint remains to be spending a whopping $75 million on opex. Administration tasks being adjusted EBITDA worthwhile by year-end FY25, however the hole is at present large with gross earnings needing to triple from present ranges even with quarterly opex forecast to dip under $70 million primarily based on the most recent job cuts.

Supply: ChargePoint FQ4’24 presentation

As talked about above, the one excellent news tidbit from the January quarterly report was the Subscription enterprise nonetheless rising 30% to achieve $34 million. The section even produced nearly all of the FQ4’24 gross earnings at $14 million.

The massive query is how a lot ChargePoint can drive Subscription development going ahead with out promoting extra Networked gear used to drive recurring revenues. The Subscription enterprise nonetheless solely has annual revenues base of $134 million.

Flawed Course

ChargePoint guided to FQ1’25 revenues of solely $100 to $110 million, down sequentially from the FQ4 degree of $116 million. The dip is because of regular seasonality, however the EV charging station enterprise does not have the margin of security to deal with the dip.

The corporate ended the quarter with a cash balance of $358 million and with debt of $284 million. ChargePoint hardly has a web money place now after burning almost $42 million of money from operations over the last quarter and $329 million from operations for all of FY24.

Administration made numerous guarantees concerning improved margins from the manufacturing deal with AcBel and Kinpo, however ChargePoint did not present any strong metrics to help how the enterprise improves sufficient to get rid of these large losses. The deal was simply introduced a couple of weeks in the past, and these kind of offers can take a yr or so to be absolutely applied and useful to operations.

The consensus estimates solely forecast FY25 revenues of $562 million, but the steerage for FQ1 is already under analyst estimates. Even with ChargePoint producing $50 million in further quarterly revenues, 20% gross margins solely add $10 million in gross revenue whereas the corporate would want $150 million in quarterly revenues and 30% gross margins (8 proportion factors above FQ4) with the intention to produce simply $45 million in gross earnings.

ChargePoint already has an enormous hurdle to beat and most corporations wrestle to reinvigorate development after chopping so many bills from operations. The corporate estimates almost $70 million has now been lower from the non-GAAP working expense base and the discount in R&D and gross sales/advertising sometimes result in unintended impacts on future gross sales.

The market cap is right down to ~$800 million and can possible pattern decrease till the continuing losses are eradicated. ChargePoint simply does not warrant a lot upside as a result of attending to adjusted EBITDA worthwhile in the course of the peak quarter is not the identical as the corporate being worthwhile, contemplating curiosity bills and depreciation prices are authentic price hurdles.

Takeaway

The important thing investor takeaway is that ChargePoint Holdings, Inc. inventory has no margin of security and the EV charging station enterprise is now struggling. The corporate should develop gross sales and increase margins dramatically to simply get rid of ongoing losses and money burn. The inventory nonetheless does not supply any upside for shareholders till the corporate shifts the enterprise past simply attending to adjusted EBITDA worthwhile, but that’s already a giant velocity bump.