MASTER/Second through Getty Photos

By Anthony Sassine, CFA

Introduction

Regardless of world EV gross sales rising 40% final yr, efficiency in associated equities dragged.2 The disconnect between gross sales development and inventory efficiency stems partly from extra conservative development estimates. A consensus of studies estimates EV gross sales to develop by 20% in 2024, which remains to be notable development in comparison with established world industries.1

Though development within the EV {industry} might normalize within the coming years, we imagine the long-term image stays the identical. The world nonetheless wants to switch 1.3 billion inner combustion engine autos (ICE) with EVs by 2040, and we have now solely 40 million EVs on the highway at this time.3 In 2023, we had been as soon as once more reminded that structural development doesn’t all the time type a straight line.

We now have seen this story unfold earlier than with many cornerstone know-how corporations, together with Google (GOOG) (GOOGL), Fb (META), Netflix (NFLX), and now Tesla (TSLA). Whereas gross sales or subscriber development might gradual for 1 / 4 or two, the long-term transformation story stays intact. In spite of everything, we don’t see anyone going again to Blockbuster to hire films. Regardless of challenges, valuations and positioning are at multi-year lows, EV costs are declining in comparison with ICE, and know-how and infrastructure are bettering quickly.

2023 Evaluate

Pure EV corporations reminiscent of Tesla, Li Auto (LI), XPeng (XPEV), and Rivian (RIVN) proved their capacity to compete with legacy automotive corporations in 2023. Conventional ICE automobile corporations like Ford (F) and GM (GM), who’ve launched EVs to their current enterprise mannequin, failed to indicate any appreciable enhancements final yr throughout the board.

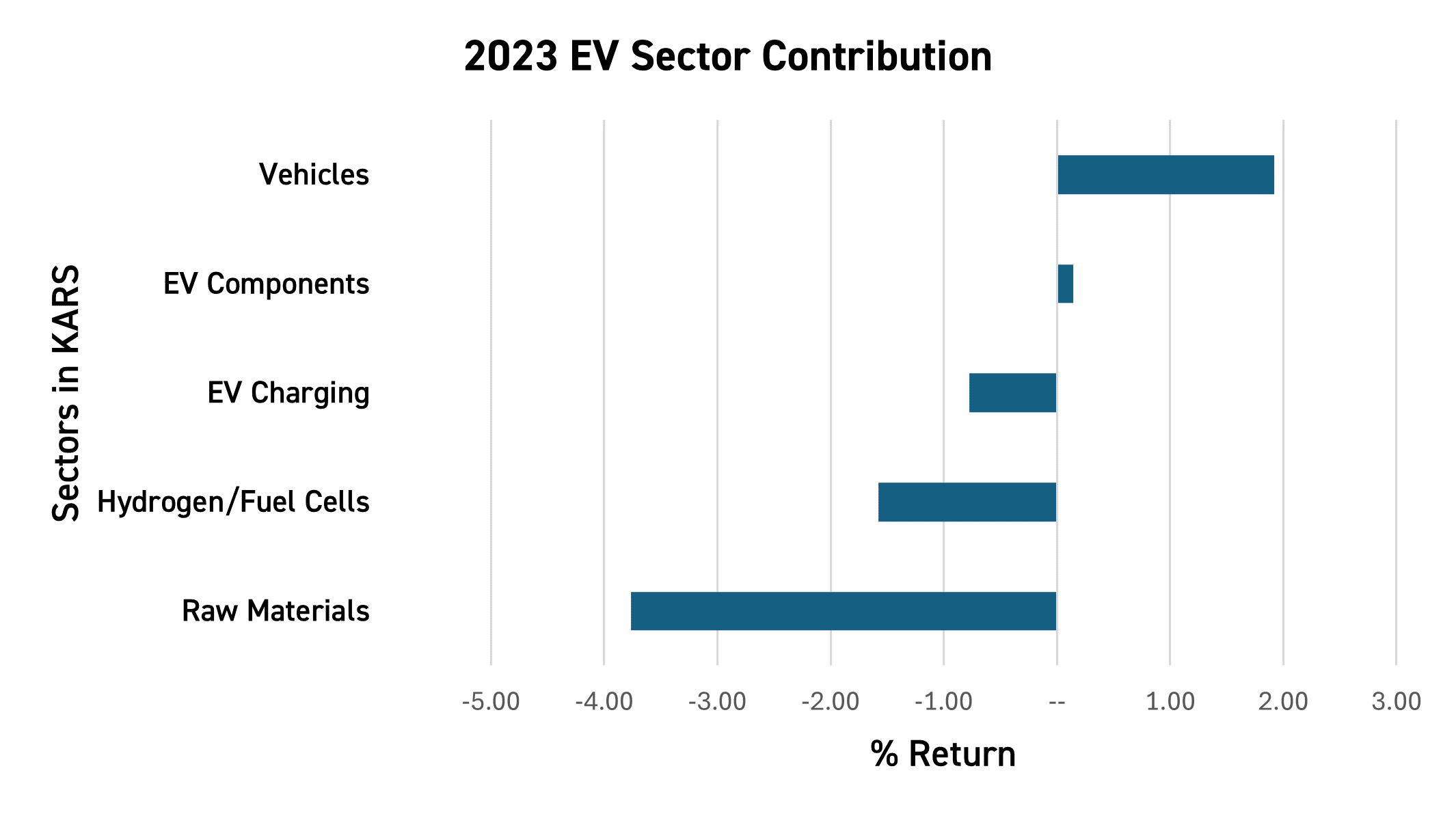

Whereas basic development inside pure EV corporations was robust final yr, uncooked materials and battery suppliers detracted on account of decrease demand and extra capability in electrification metals. After document funding flowed into mining tasks in 2022, the sub-industry noticed an inflow of provide that outpaced total EV demand.4 We imagine this imbalance will right itself as EV corporations speed up automobile manufacturing to fulfill world demand.

FactSet: December thirty first, 2023 FactSet: December thirty first, 2023

2024 Overview

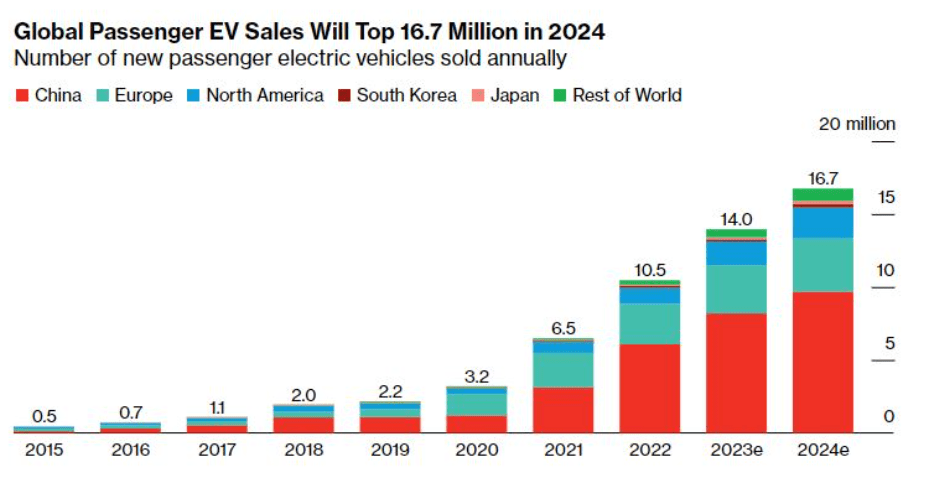

In 2024, we count on world EV gross sales to develop by 20% to 16.5 million items.7 Many of the gross sales are anticipated to be in China, which is estimated to account for about 10 million of the EVs offered globally.8 The US is predicted to promote almost 2 million EVs, representing extra modest development over 2023.9 Alternatively, European gross sales development is predicted to be within the single digits for the yr, with round 3.8 million items.10

BNEF: January 2024.

Pleasure within the US over EVs started to weaken following the revision of the Inflation Discount Act (IRA) to restrict the variety of manufacturers that qualify for the total $7,500 credit score for EV purchases. Nevertheless, the IRA efficiently ignited a serious funding cycle not seen in a few years, particularly in battery factories. Moreover, the upcoming US presidential elections might current extra uncertainty for clear power help within the coming years.

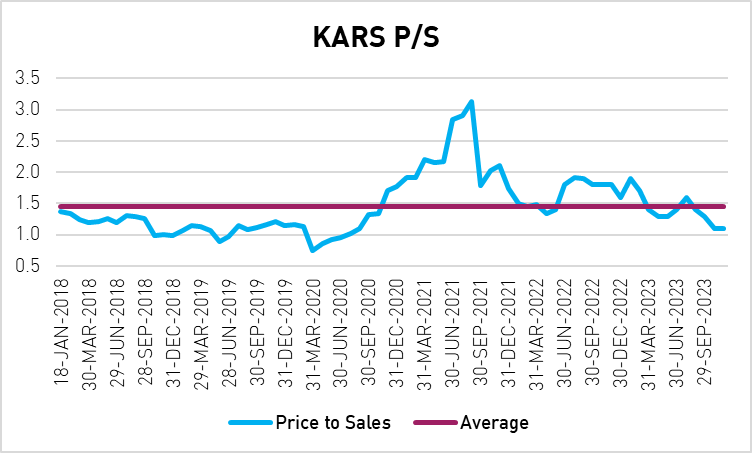

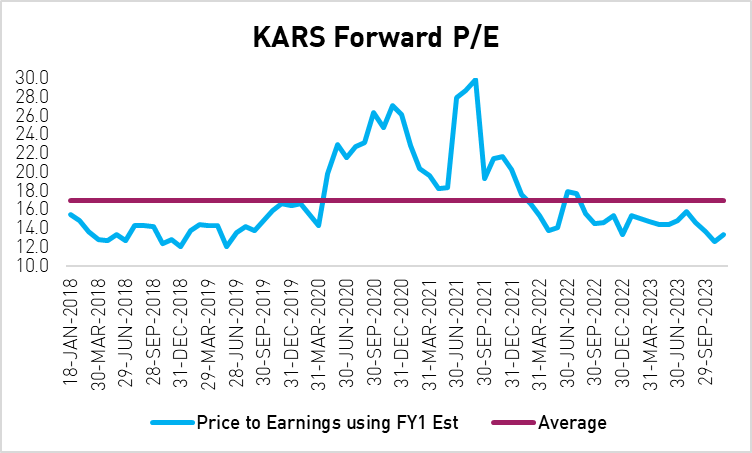

We imagine EV inventory valuations look very engaging, particularly on a price-to-sales foundation after an unremarkable begin to 2024. Many of those corporations are buying and selling at a price-to-sales (P/S) stage between 1 and a pair of.11 BYD’s (BYD) P/S is 0.9.12 In the meantime, Tesla’s P/S has declined from 10 to six after a latest earnings miss.13

FactSet: December thirty first, 2023 FactSet: December thirty first, 2023

Additionally, positioning within the sector is the bottom it has been in a few years, and sentiment is bearish. Any indicators of enchancment in EV gross sales, China’s macroeconomics, or charge cuts within the US might change sentiment shortly. Given the present surroundings, we favor corporations with lower cost tags over luxurious EVs, which, in the long run, will contribute essentially the most to closing the hole between EVs and ICE autos.

Battery and Metals Overview

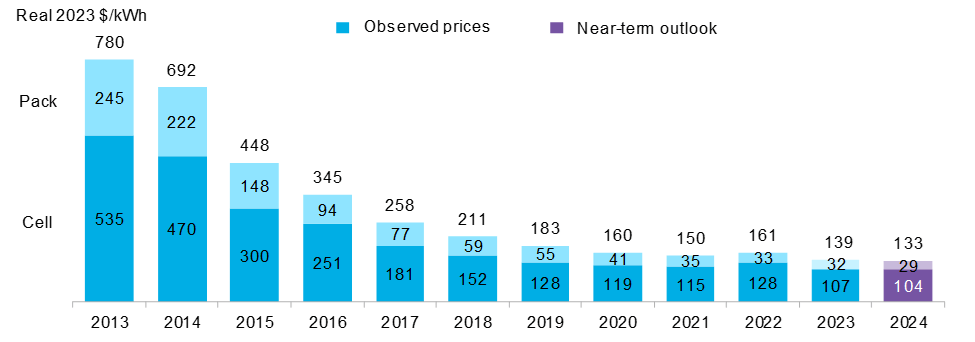

On the battery facet, pack and cell costs resumed their downward course in 2023 after rising in 2022 for the primary time in no less than ten years on account of excessive metallic costs. The Cell worth reached an all-time low with a weighted quantity common of $107/kWh.14 Pack costs hit $32/kWh.15 This worth contains inputs from all electrification segments, together with Plug-In Hybrids (PHEV), Battery EVs (BEV), Stationary, E-Busses, and so forth. BEV battery costs in 2023 had been noticed at $128/KWH, whereas PHEV battery costs had been $343/kWh.16

Costs are anticipated to ease additional in 2024, bringing us nearer to ICE parity. Absent a serious know-how enchancment in batteries, ICE parity is predicted to be reached for particular fashions, reminiscent of light-weight autos, in sure international locations, reminiscent of China, in 2025. The remaining are anticipated to comply with within the following years. Price parity with ICE autos is predicted to unleash mass adoption for EVs.

BNEF: January 2024

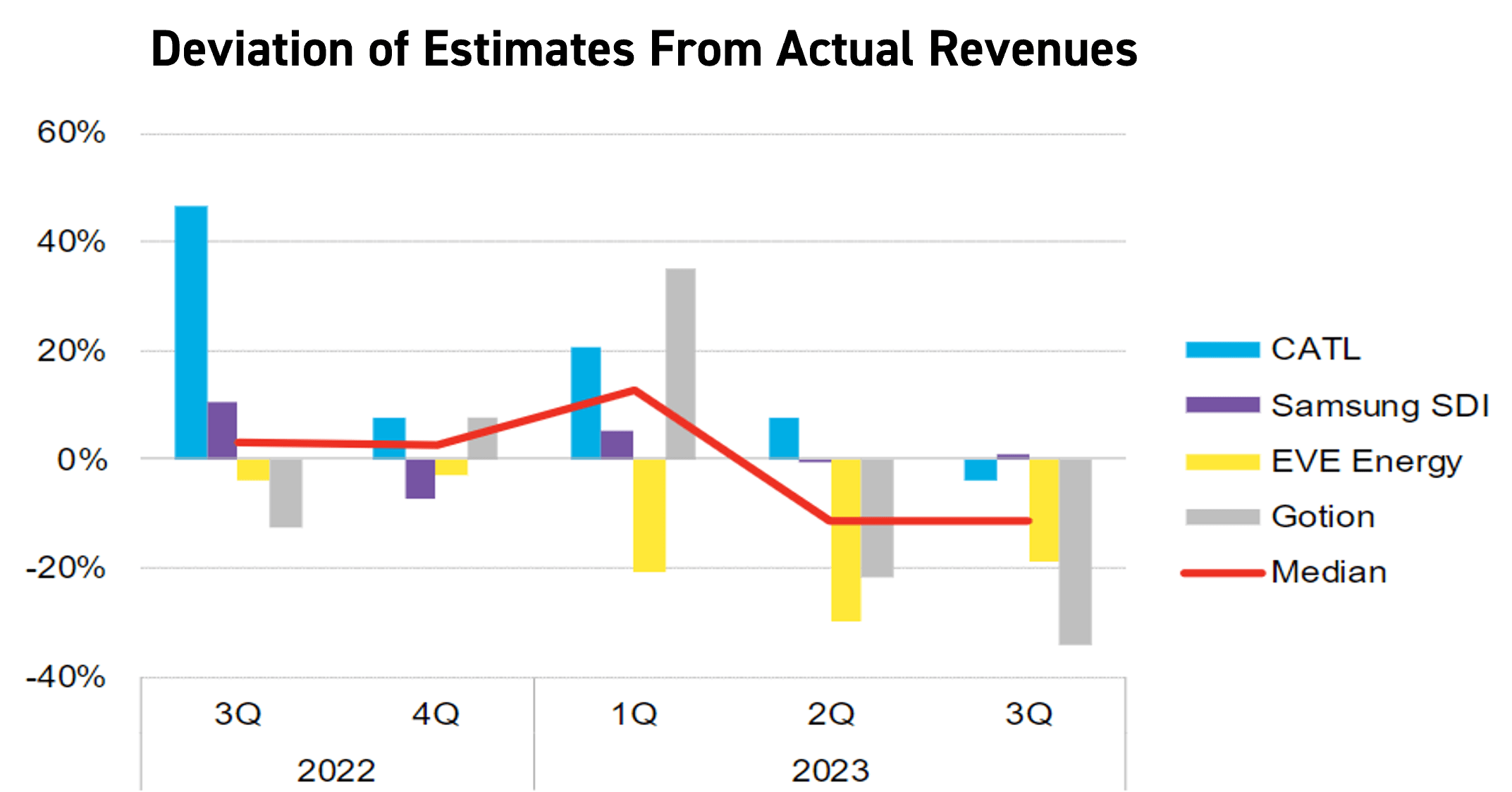

Battery firm shares suffered in 2023 regardless of considerably decrease metallic costs on account of lower-than-expected demand for EVs. Many corporations, together with CATL and Samsung (OTCPK:SSNLF) SDI, had been working under capability and delivered revenues and earnings that had been under Wall Avenue’s expectations. Decrease metallic costs normally bode effectively for battery makers because it cheapens their uncooked supplies. Nevertheless, on account of decrease demand for EVs, many battery corporations needed to supply more and more aggressive contracts to automakers to lock in demand within the quick time period.

Bloomberg and BNEF: January 2024

In keeping with Bloomberg New Power Finance’s (BNEF) yearly Lithium Value Survey launched final November, Lithium-Ion Phosphate (LFP) share versus Nickel-based chemistries continues to rise, reaching an estimated 46% of the full market share. LFP is gaining popularity for battery EVs, with many North American producers like Rivian and Ford switching to LFP this yr. LFP at the moment has the most affordable battery worth within the {industry}, at $130/kWh.17 The lower cost of LFP has been supported by the big decline in Lithium costs seen in 2023 after document new capability got here on-line.

Dangers & Catalysts in 2024

Some potential dangers might emerge in 2024. Probably the most anticipated occasion this yr is the US election. A Republican victory might imply repealing a few of the subsidies within the Inflation Discount Act (IRA). Nevertheless, given the breadth of states, together with purple states, that benefited from the IRA when it comes to jobs and investments over the previous yr, we imagine the affect might not be as massive as anticipated. Examples of this embody Rivian and Hyundai (OTCPK:HYMTF) constructing new EV factories in Georgia, Fisker (FSR) taking on the deserted auto plant in Ohio, and Ford and GM planning to construct battery factories in Michigan and different states. Different dangers embody a probably much less sturdy client restoration in China and better charges for longer durations. Nevertheless, we imagine many of those elements are already priced in.

We imagine bearishness on EV gross sales within the quick time period could also be extreme as a result of many elements might shortly reverse investor sentiment. A few of these elements embody better-than-expected gross sales in Q2 and Q3, potential charge cuts within the US and Europe, a possible technological development, particularly in batteries or autonomous driving, an enchancment in client sentiment in China, extra subsidies, and insurance policies to encourage EV shopping for, particularly within the EU, and the emergence of lower-priced EVs.

Conclusion

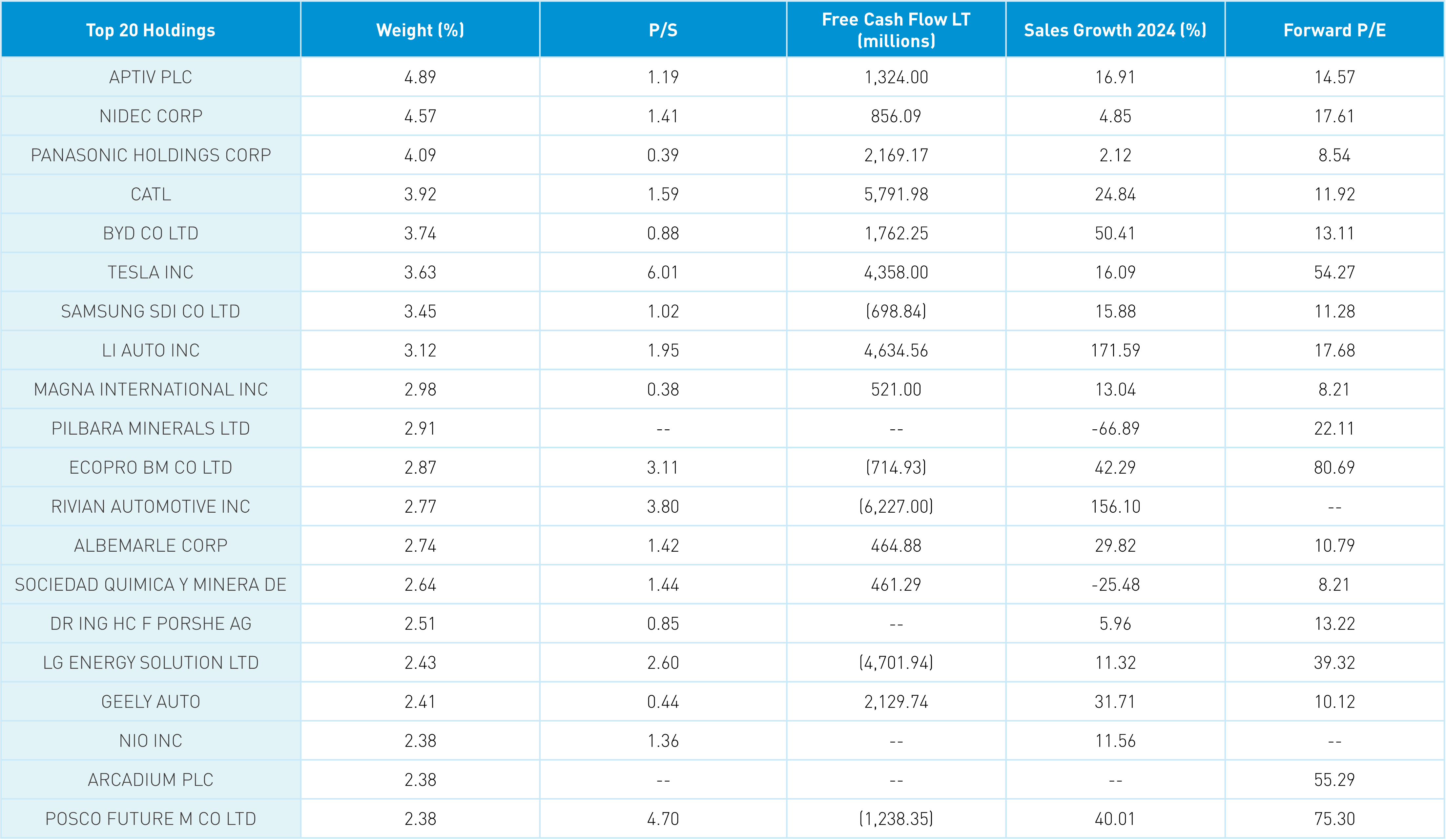

Traders can achieve publicity to corporations engaged within the manufacturing of electrical autos and/or their parts via the KraneShares Electric Vehicles & Future Mobility Index ETF (KARS).

KARS is benchmarked to the Bloomberg Electrical Automobiles Index, which gives publicity to corporations engaged in electrical automobile manufacturing, autonomous driving, shared mobility, lithium and/or copper manufacturing, lithium-ion/lead acid batteries, hydrogen gasoline cell manufacturing, and electrical infrastructure companies.

FactSet: January 2024. Holdings are topic to alter.

This shouldn’t be considered funding recommendation or a suggestion of particular securities. Holdings are topic to alter. Securities talked about don’t make up the whole portfolio and, within the combination, might signify a small proportion of the fund.

Definitions:

Value-to-sales ratio: A valuation ratio that compares an organization’s inventory worth to its revenues. It’s an indicator of the worth that monetary markets have positioned on every greenback of an organization’s gross sales or revenues.

Free Money Circulation LT: The Lengthy-Time period Common Free Money Circulation to Belongings, or FCF LT / Belongings, is a measure of how successfully an organization generates surplus Money Circulation from Revenues. It’s the Common Free Money Circulation over the past 5 years, divided by Complete Belongings.

Gross sales Development: Gross sales development is the rise in gross sales of a services or products over time. It measures how effectively a enterprise performs when it comes to its income from gross sales. Gross sales development might be measured by evaluating the year-over-year, quarter-over-quarter, or month-over-month gross sales.

Ahead P/E: The ahead P/E ratio (or ahead price-to-earnings ratio) divides the present share worth of an organization by the estimated future (“forward”) earnings per share (EPS) of that firm. For valuation functions, a ahead P/E ratio is usually thought of extra related than a historic P/E ratio.

Citations:

- Knowledge from BNEF as of January 2024.

- Knowledge from Bloomberg and FactSet as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from PwC as of June 2023.

- Knowledge from Bloomberg and FactSet as of January 2024.

- Knowledge from Bloomberg as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from FactSet as of January 2024.

- Knowledge from FactSet as of January 2024.

- Knowledge from FactSet as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

- Knowledge from BNEF as of January 2024.

Editor’s Be aware: The abstract bullets for this text had been chosen by In search of Alpha editors.

![A Easy Information to B2B Social Media Advertising and marketing [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/01/bG9jYWw6Ly8vZGl2ZWltYWdlL2IyYl9zb2NpYWwyLnBuZw-600x402.jpg)