Art Wager/E+ via Getty Images

Introduction

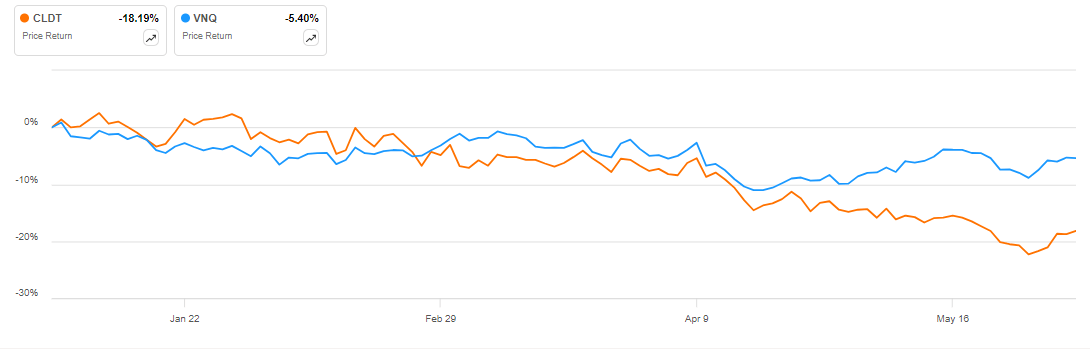

Chatham Lodging Trust (NYSE:CLDT) is one of the weakest-performing REITs so far in 2024, with a negative return of 18% significantly below the 5% drop in the benchmark Vanguard Real Estate Index Fund ETF (VNQ):

CLDT vs VNQ in 2024 (Seeking Alpha)

I think the company is quite cheap, offering a cap rate of 10.3% and a robust operating performance, notwithstanding the risks related to the drivers of its revenue growth and expensive debt.

Company Overview

You can access all company results here. Chatham Lodging Trust is a lodging REIT focused on extended-stay accommodations as well as premium-branded select-service hotels. In fact, extended stay rooms account for circa 63% of all 5,883 rooms across the REIT’s 39 hotels.

From a market perspective, the company operates in 17 states and D.C., with a particularly large exposure to California – the state accounts for some 28% of Chatham Lodging’s last twelve-month EBITDA:

Portfolio breakdown by key markets (Chatham Lodging March 2024 Investor Presentation)

From a brand perspective, Residence Inn accounts for 46% of the last twelve month EBITDA:

Hotels by Brand (Chatham Lodging March 2024 Investor Presentation)

Operational Overview

On June 3 Chatham Lodging provided an ad-hoc business update for its operations in April and May of 2024. The REIT grew revenue per available room, or RevPAR, by 5% Y/Y in both April and May. This is significantly higher than the 1.5% Y/Y growth reported in Q1 2024.

The RevPAR increase in April and May was driven primarily by higher occupancy, which clearly is not a sustainable driver of RevPAR since you can only grow occupancy ever so much (occupancy was 83% and 82% in April and May respectively). On a more optimistic note, CEO Jeffrey Fisher noted:

As occupancies climb, rate growth should accelerate, and this is very encouraging as we enter our busiest time of the year.

With no Adjusted FFO figures provided with the April/May business update, I will highlight the results achieved in Q1 2024, with trend growth certainly higher in the second quarter. In Q1, adjusted FFO was $0.16/share, flat Y/Y, with revenue growth offset by higher interest and operating expenses. For reference, the adjusted FFO was $1.18/share in 2023.

2024 Outlook

Chatham Lodging was initially guiding for a 2.5-4% RevPAR increase in Q2 2024. With the latest update, the REIT will clearly beat the top range of its guidance, which is very encouraging. Furthermore, as growth is accelerating into the REIT’s busiest season, 2024 is set to be a year of solid RevPAR growth for Chatham Lodging. For reference, RevPAR grew 2.5% in 2023.

Capital structure

Chatham Lodging ended Q1 2024 with net debt of $412 million, which increased to about $450 million in Q2 following the acquisition of the Home2 Suites by Hilton Phoenix Downtown for $43 million. Furthermore, the company has $120 million in preferred equity outstanding in series A preferred shares. This implies that net debt currently accounts for 45% of enterprise value while preferred equity funds 12% of the capital structure (I have conservatively taken preferred shares at $25 face value rather than the current $21.15 market price).

The company plans to address July 2024 maturities with an incremental $140 million borrowing on its revolving facility which carries an interest rate of about 7% (secured overnight financing rate, or SOFR, plus a spread of 1.5-2.25%). The remaining maturities are fixed rate, but unfortunately the interest rates are fixed at quite high rates, marginally above 7%, which will clearly create a headwind for the company starting in July 2024. For reference, the interest rates on expiring debt are circa 4.6%.

Market-implied cap rate

I estimate Chatham Lodging should generate about $104 million in net operating income on a run-rate basis, driven by 2% Y/Y NOI growth relative to 2023 levels and a contribution from the recently acquired Phoenix hotel. Relative to the $1 billion enterprise value, this represents a market-implied cap rate of 10.3%, which is highly attractive.

The company’s capital investment budget for 2024 is $37 million, implying a post-capex cap rate of 6.7%, which is also quite attractive. Finally, I estimate general and administrative at about $12 million in 2024, or a 1.2% management burden to enterprise value, which is a bit on the high side, but generally what you would expect from a small REIT such as Chatham Lodging.

The Series A preferred shares

The series A preferred shares currently offer a 7.8% yield, clearly 2.5% below the NOI the company trades at, but still an attractive amount considering they also trade at a discount to par. At market prices, the preferred shares are currently worth about $102 million, implying they are more than four times covered by common equity market capitalization.

The preferred dividends of $2 million a quarter are also covered by adjusted FFO 4 times.

Risks

From an operational perspective, Chatham Lodging Trust is doing very well, with 5% Y/Y RevPAR growth in April and May. The key going forward will be whether the company can sustain an above-inflation RevPAR growth through increases in the average daily rate, or ADR, as opposed to occupancy gains. So far in Q2, ADRs were down 1% Y/Y in April and up 1% Y/Y in May, which is quite disappointing. If this trend continues, the company will see its RevPAR growth evaporate as occupancy cannot increase indefinitely.

The other risk facing Chatham Lodging is its quite high average cost of debt, which I estimate at about 7% once the July 2024 maturity is addressed. It is true that roughly a third of the debt will be floating rate following the July 2024 paydown, and as such will benefit from FED interest rate cuts, but unlike the vast majority of other REITs the company has no cheap financing locked in for the long term. Instead, its 2030s maturities carry an interest rate of circa 7%, which is quite high, and potentially in a few years this debt will trade above par as it nears maturity and interest rates have fallen.

Conclusion

Chatham Lodging Trust’s April and May business update points to the company easily beating its Q2 guidance. The key point of attention going forward is whether occupancy growth translates into ADR growth. With a market cap rate of 10.3% and a growing topline, Chatham Lodging appears quite cheap and can easily deliver a low-double-digit return to enterprise value. Of course, if you are risk averse, the series A preferred shares are well-covered by both earnings and market capitalization. To me, the common shares are clearly undervalued given the excellent operating performance, hence I rank them a buy.

Thank you for reading.