hedidwhat/iStock by way of Getty Pictures

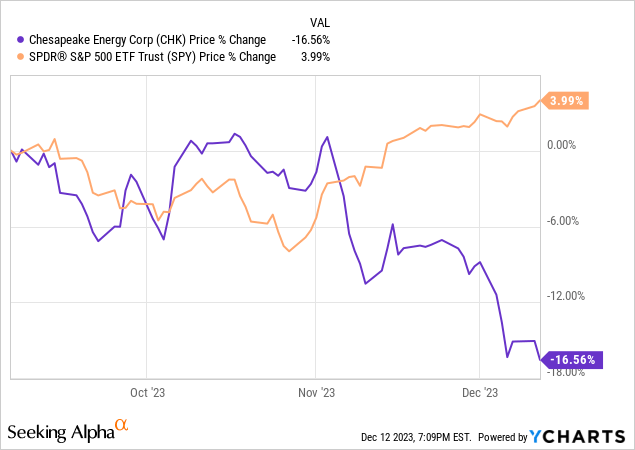

Chesapeake Power (NASDAQ:CHK) traders had a disappointing 2023, together with the previous few weeks. Hotter than regular temperatures just lately and the report final week of a delay within the Gold Bass LNG terminal venture brought about a continued drop in pure fuel costs. CHK inventory worth has dropped about 15% since I downgraded CHK in September to a promote. That is an replace to prior articles.

CHK and S&P 500 ETF Value Change Since Sept 6 Article

Continued Share Repurchases

I wish to begin with a problem that I coated in my prior article. Chesapeake Power is in a capital-intensive commodity-based trade that could be very dangerous, however they continued to make inventory repurchases in 3Q. As I coated earlier than, I believe administration ought to use this money to pay down debt to cut back threat or to extend CAPEX.

Share Repurchases 2023 and 2022

sec.gov

They already “lost” $221 million on their repurchases. The present market worth of their CHK repurchased shares is $1.157 billion in comparison with a complete repurchase quantity in 2022 and 2023 of $1.378 billion with a mean repurchase worth of $89.40 ($74.95 present CHK worth).

Changing into Very Depending on LNG Exports

Many traders purchase/maintain CHK for the LNG potential. That expectation was negatively impacted final week when it was disclosed that the opening of the Gold Go LNG terminal in Texas can be delayed till the primary half of 2025 as an alternative of late 2024. The fact is that main development initiatives typically have delays and I’d not be stunned if there have been additional delays. The significance of the export facility was even mentioned in the course of the newest conference call when administration said they had been planning on rising their variety of rigs of their Haynesville from 5 to six within the second half of 2024 “if that looks like it’s (the new LNG export facility) going to play out and the strip looks like it’s going to hold up”.

On October 31 it was announced that CHK signed a 15-year LNG preliminary, non-binding accord with Vitol for as much as 1 million tonnes of LNG per yr beginning in 2028. Final March they introduced a preliminary, non-binding accord with Gunvor for as much as 2 million tonnes per yr beginning in 2027. (A million tonnes of LNG is roughly 48.7 Bcf of pure fuel.) Whereas these offers is perhaps thought of main constructive developments, I fear in regards to the pricing. The pricing relies on the Japan/Korea Market – JKM Index. That is the benchmark for the Asian LNG market, but when there’s some pure fuel glut, for no matter purpose, in that space and on the similar time there are manufacturing/pipeline points in Haynesville, this might develop into a significant downside. I would like long-term agreements that embrace each prices/bills and market worth variables when figuring out the acquisition costs. One-sided long-term agreements are too dangerous, in my view.

One of many issues with massive publicity to the LNG market is that there are actually many extra geopolitical and worldwide financial points that instantly affect CHK, which provides further dangers for traders. Years in the past, earlier than the U.S. exported LNG these dangers had been simply oblique. I count on a few of their LNG exports may even be related to TTF – Title Switch Facility, which is the pipeline pricing index and is usually used when pricing LNG merchandise in Europe. So, CHK traders must now fear in regards to the climate in Europe and Asia, along with the U.S. As well as, there are transportation points such because the affect on delivery by way of the Panama Canal that’s at the moment having main issues.

At the moment, there’s a important worth distinction between U.S. pure fuel costs and people in Europe and far of Asia, which makes the LNG market so enticing. That doesn’t, nonetheless, imply these differentials will proceed long-term. I believe the political hostility towards utilizing fossil fuels is way stronger in most of Europe in comparison with the U.S. The fact is that the LNG market could possibly be severely impacted if the varied Inexperienced Events in Europe finally win sufficient seats and drive the banning of fossil fuels and even main reductions of their use.

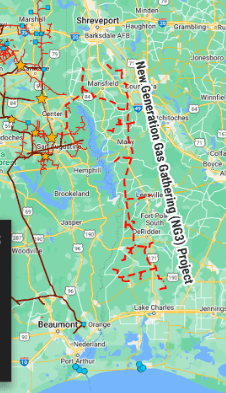

Indicative of how vital the LNG market is to their future, Chesapeake purchased a 35% fairness curiosity in Momentum Sustainable Ventures which is within the strategy of constructing a gathering system/pipeline to the Gulf Coast from Haynesville. In accordance with their current replace the entire funding for 2023 on this deal is estimated at $285 million to $315 million. The venture is anticipated to grow to be operational in late 2024.

NG3 Undertaking

rextag.com

Pure Fuel Costs – Climate Is Every thing (Nearly)

Should you had been constructing a posh econometric mannequin to forecast pure fuel costs, the climate can be some of the vital variables – present temperatures, variations from common, and short-term and long-term temperature forecasts. At the moment, and during the last six weeks all of these temperature metrics have been negatives for pure fuel costs within the U.S. and far of Europe, which has resulted in plunging Henry Hub costs. Decrease-than-normal pure fuel utilization has resulted in higher-than-normal pure fuel storage, which overhangs the market even when temperatures get again nearer to regular later this winter.

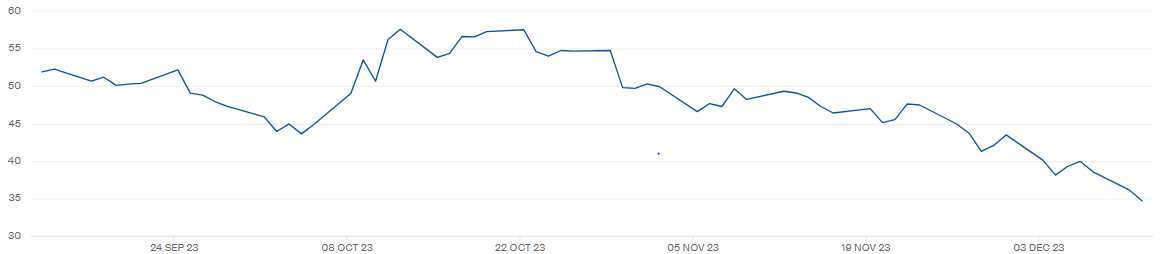

January 2024 Henry Hub Futures Value

www.cmegroup.com

Whereas Henry Hub costs are sometimes utilized by traders, Chesapeake’s Marcellus manufacturing is offered into the northeastern U.S. market and there’s typically a big worth distinction.

www.eia.gov

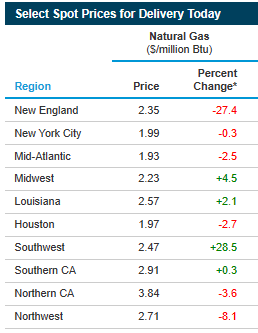

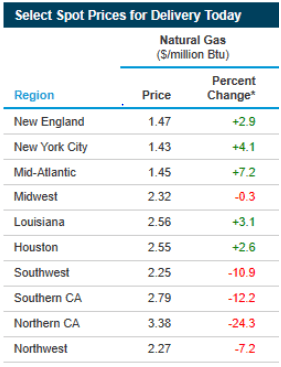

Most of the regional spot pure fuel costs are at the moment pretty near the costs in my September CHK article. Among the regional costs rose considerably throughout October when there have been lower-than-normal temperatures however then fell because the climate was hotter than regular in November and December.

Sept. 1, 2023

www.eia.gov

Costs in Europe as measured by the Dutch TTF futures January 2024 contract have additionally dropped sharply because the finish of October.

January 2024 Dutch TTF Pure Fuel Futures

www.ice.com

(Costs: Euro cents per MWh)

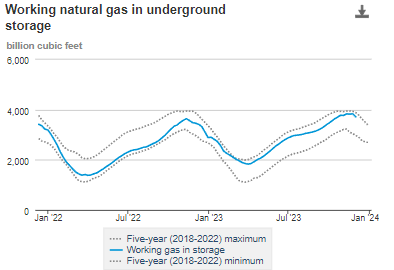

I maintain studying forecasts that due to El Niño the climate this winter shall be hotter and wetter than regular. Buying and selling vitality shares based mostly solely on climate forecasts, in my view, just isn’t investing – it’s playing. As a substitute of future climate forecasts, I choose to have a look at a recognized metric and that’s present pure fuel underground storage. The present storage is close to the five-year most, which might imply that even when climate turns into extra regular later this winter there’s a important quantity of fuel already obtainable to assist provide that demand.

www.eia.gov

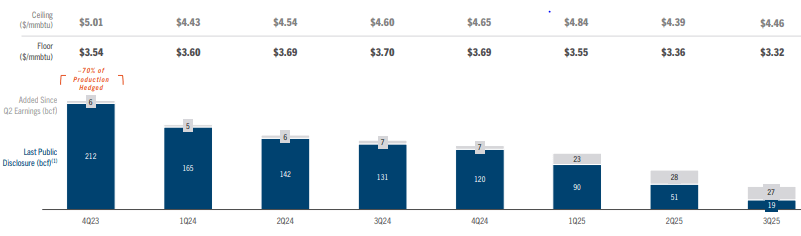

Hedging In opposition to Value Declines

Chesapeake typically hedges a good portion of its anticipated future manufacturing. For 4Q 2023 they’re 70% hedged with a $3.54 mmbtu flooring and $5.01 ceiling so the affect of current decrease costs won’t be as nice if there have been no or little or no hedge positions. What I discover stunning, nonetheless, is the very modest quantity of latest hedges that had been added between 8/1/23 and 10/26/23 as might be seen by the chart under as a result of costs had been comparatively sturdy in October.

Hedge Positions

traders.chk.com

As a result of CHK makes use of in depth hedging it’s actually not the most effective inventory to commerce forecasted pure fuel worth modifications. Usually vitality trusts, which might’t hedge, are extra delicate to cost modifications. These trusts often have implied pure fuel and/or oil name choices constructed into their present market values.

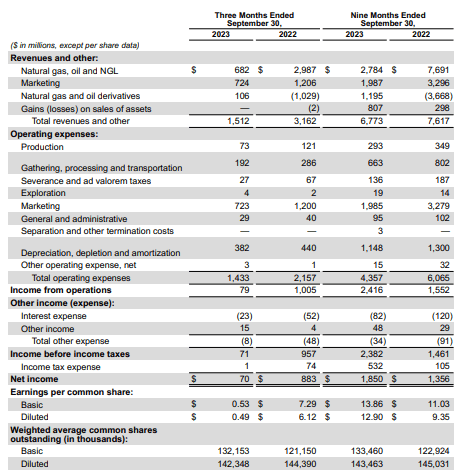

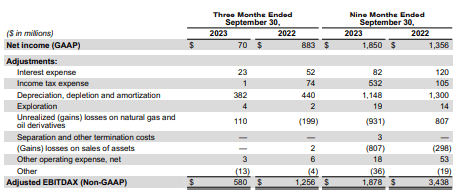

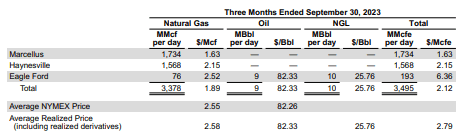

Latest Outcomes – 3Q 2023

Chesapeake’s 3Q outcomes illustrate a important concern that too typically traders ignore. An vitality producer can have top-tier belongings, which Chesapeake has, and nonetheless report mediocre outcomes if costs are weak. As a result of there was such a dramatic change of their core belongings over the previous few years with the acquisition of Marcellus belongings and the current sale of Eagle Ford belongings, which had some oil manufacturing, evaluating prior long-term outcomes to present figures just isn’t actually related when valuing their present operations.

3Q and 9 Months Revenue Assertion

traders.chk.com

3Q and 9 Months Adjusted EBITDAX

traders.chk.com

3Q Common Day by day Manufacturing and Costs Acquired

traders.chk.com

Conclusion

I’m persevering with my promote suggestion on CHK as a result of I believe the inventory might drop just a few extra factors earlier than it turns into a maintain. These are the most important the reason why CHK might proceed to drop: 1) I count on pure fuel costs to stay weak due to El Niño and since I count on a decision within the first half of 2024 to the Russian/Ukraine battle. 2) LNG exports almost certainly shall be a short-term constructive, however due to geopolitical pressures, the long-term outlook for fossil fuels could be very detrimental, particularly in Europe. 3) I really feel that administration just isn’t correctly managing their stability sheet by repurchasing inventory as an alternative of lowering threat by paying down debt.