A Texaco-branded Chevron gasoline station. hapabapa/iStock Editorial by way of Getty Photos

My main goal as an investor is to construct a viable and rising stream of passive earnings. Why dividend development investing?

The concept is that this strategy will hopefully assist me meet/exceed my month-to-month bills via passive earnings. At that time, I will likely be free to maintain doing what I presently am doing with out worrying about cash as a lot.

I additionally determine that if my portfolio produces ever larger quantities of passive earnings, capital appreciation may even ultimately observe. That will be the cherry on high of the fudge sundae in my view.

How do I plan on reaching the promised land of investing? There’s the all-important residing under my means facet. By American requirements, my tastes are in all probability among the many easiest on the market. Past the necessities that all of us take as a right and an web connection, I do not want or need a lot.

That permits me to steadily construct up capital for investing, which raises the subsequent query: What do I do with it? I intention to load up my portfolio with essentially the most qualitative, confirmed companies on the planet.

Chevron (NYSE:CVX) is a Buffett-owned business that I’ve had on my watch listing for years now, however I’ve by no means pulled the set off. After I cease aggressively build up my emergency fund and resume investing (probably in February 2024), I hope so as to add Chevron in some unspecified time in the future subsequent yr. Please enable me to unpack the corporate’s fundamentals and valuation to clarify why.

DK Zen Analysis Terminal

Chevron’s 4% dividend yield is presently about 10 foundation factors larger than the 3.9% yield of the 10-year U.S. treasury. To not point out that it’s practically triple the 1.5% yield of the S&P 500 (SP500). Suffice it to say, that Chevron’s dividend is aggressive in even a excessive charge surroundings resembling this one.

Higher but, the corporate’s payout seems to be reasonably secure. For one, the 30% EPS payout ratio is nicely under the 40% EPS payout ratio that ranking companies take into account secure for Chevron’s trade.

Moreover, the corporate’s 13% debt-to-capital ratio clocks in at lower than half of the 30% trade secure guideline put forth by ranking companies. Due to this low payout ratio and modest debt load, Chevron is rated AA- on a steady outlook by S&P. For context, that is simply three notches under an ideal company credit standing. That means the likelihood of Chevron going to zero over the subsequent 30 years is simply 0.55%.

On account of these practically impeccable fundamentals, Dividend Kings pegs the chance of the corporate chopping its dividend within the subsequent common recession at solely 0.5%. That is the bottom allowed likelihood for Dividend Kings’ dividend reduce danger metric. The possibility of a dividend reduce within the subsequent extreme recession stays low at simply 1.5%. That is solely a contact greater than absolutely the minimal dividend reduce danger of 1% for a extreme recession for even essentially the most dependable dividend payers.

DK Zen Analysis Terminal

Chevron is a wonderful enterprise, which additionally appears to be like to be undervalued. Utilizing historic valuation metrics resembling dividend yield, Dividend Kings estimates that shares of the supermajor are value $161 every. Relative to the present $152 share worth (as of December 20, 2023), this is able to symbolize a 6% low cost to truthful worth.

If Chevron matches the expansion consensus and its valuation reverts to truthful worth, listed below are the overall returns that it might ship to shareholders within the coming 10 years:

- 4% yield + 8.3% FactSet Analysis annual earnings development consensus + a 0.6% annual valuation a number of growth = 12.9% annual whole return potential or a 236% cumulative 10-year whole return versus the 8.6% annual whole return of the S&P or a 128% cumulative 10-year whole return

Chevron Is Positioning Itself For The Future

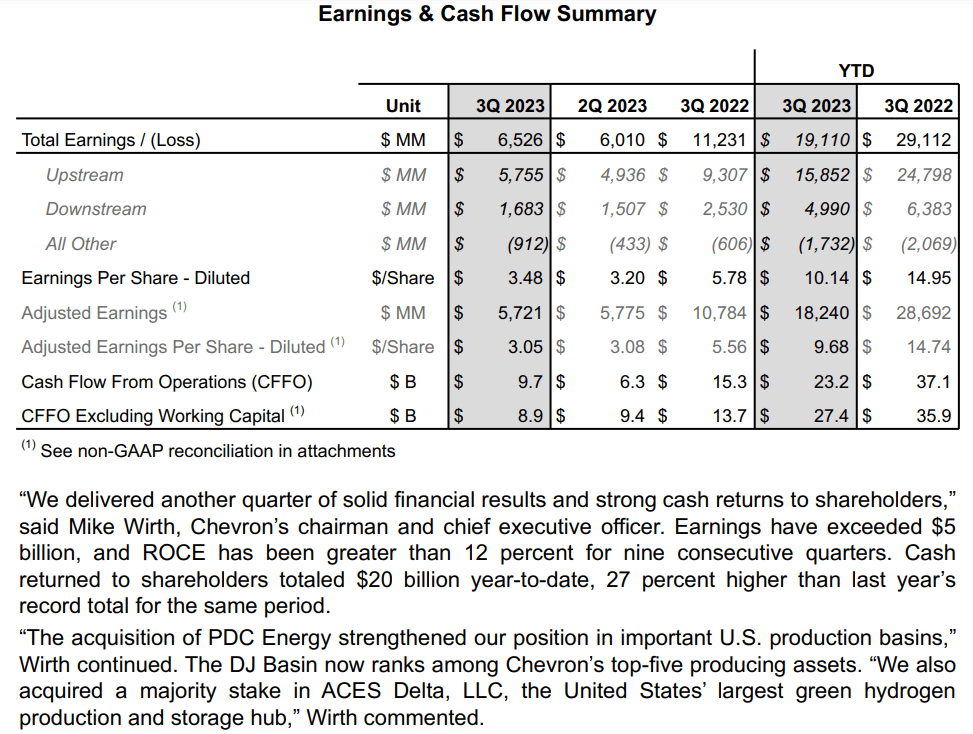

Chevron Q3 2023 Earnings Press Launch

Contemplating the circumstances, Chevron’s third quarter ended September 30 was respectable. The corporate’s whole income of $54.1 billion was down by 18.8% year-over-year, however this did beat the analyst consensus by $1.1 billion.

Chevron Q3 2023 10-Q Submitting

It will solely make sense that Chevron’s whole income was decrease by as a lot because it was within the third quarter. Because the illustration above demonstrates, power costs have largely trended down and to the fitting over the past yr and alter. For instance, West Texas Intermediate crude oil averaged $95 a barrel all through 2022, peaking across the summer time (the year-ago interval for Q3 2023). Now, WTI crude oil is round $75 a barrel. The identical was true for pure gasoline spot costs, peaking in Summer season 2022 at roughly $9. That made for a troublesome comparability interval for Chevron.

Unsurprisingly, the corporate’s non-GAAP EPS of $3.05 in the course of the third quarter was 45.1% decrease than the year-ago interval. This missed the analyst consensus by $0.64.

Nonetheless, it wasn’t all unhealthy information for Chevron. Most prominently, the corporate upped its internet oil-equivalent manufacturing by 4% over Q3 2022 to over 3.1 million barrels each day. This was fueled by the $7.6 billion acquisition of PDC Vitality earlier this yr.

World pure gasoline manufacturing was comparatively flat. That is encouraging, given the drop in pure gasoline costs was way more precipitous than in WTI crude oil.

Chevron’s 3% compound annual development charge goal in manufacturing via 2027 additionally is not only for the sake of upping manufacturing (slide 8 of 55 of Chevron’s October 2023 Investor Presentation). The corporate’s return on capital employed was above 12% for the ninth consecutive quarter. Such an ROCE determine in a risky trade by which Chevron operates exhibits that the corporate has traditionally been a prudent steward of capital. This alone is a part of why I give the corporate the advantage of the doubt on the acquisition of Hess Corp. (HES). For a extra in-depth rationalization of why it could possibly be a sensible transfer, I’d refer readers to Michael Fitzsimmons’ recent article on the acquisition.

Chevron additionally stays a monetary fortress. The corporate’s curiosity protection ratio via the primary 9 months of 2023 was a whopping 75.8. Working in an unpredictable trade, it is a sturdy curiosity protection ratio that may service Chevron’s debt in nearly any working surroundings.

Free Money Move Can Help Strong Dividend Progress

Chevron has upped its dividend for 36 consecutive years, which comfortably earns it the excellence of being a Dividend Aristocrat. In simply the final 5 years, the corporate’s quarterly dividend per share has surged 34.8% larger to the present charge of $1.51. That is adequate for a 6.2% compound annual development charge.

Chevron additionally appears to be like prefer it has many extra years of dividend development left within the tank. It is because the corporate generated $11.7 billion in free money circulate via the primary 9 months of 2023. That is even with a $3 billion-plus uptick in capital expenditures to $11.5 billion over the year-ago interval. In opposition to the $8.5 billion in dividends paid over that point, this means Chevron’s dividend is safe (particulars sourced from web page 7 of 163 of Chevron’s most recent 10-Q filing).

Dangers To Contemplate

Chevron is a world-class enterprise. Nonetheless, the corporate has dangers that needs to be thought-about by traders.

The corporate ought to have the subsequent few a long time to pivot to being another power enterprise. Chevron’s $8 billion in forecasted decrease carbon investments and $2 billion in carbon discount tasks via 2027 will likely be a great begin to the aim of main power into the long run. Nevertheless it’s vital to notice there aren’t any ensures that these investments will repay. If Chevron cannot efficiently transition towards the way forward for power, its fundamentals might deteriorate and the funding thesis might break.

One other danger to Chevron is the magnitude of its $60 billion deal for Hess. Research have proven that the majority of M&A activity destroys shareholder worth. Chevron has confirmed itself to be distinctive at creating worth for shareholders, however that does not exempt it from the potential for executing a failed acquisition.

Lastly, traders should be snug with the cyclical nature of Chevron’s enterprise. If someone goes to personal the enterprise, they have to be capable of dwell with the peaks and troughs that come up in its working and monetary outcomes.

Abstract: A Warren Buffett Favourite At A Low cost

FAST Graphs, FactSet FAST Graphs, FactSet

Chevron is a rising enterprise with a conservative stability sheet that is dedicated to shareholders. Though Berkshire Hathaway (BRK.B) has been trimming its place of late, the supermajor stays the corporate’s fifth-largest holding, valued at $16.8 billion.

Chevron’s blended P/OCF ratio of seven.9 is only a bit greater than the historic P/OCF ratio of seven.7 per FAST Graphs. If the corporate grows as anticipated and falls to its common valuation a number of, cumulative whole returns could possibly be 25% via 2025. That is practically twice as a lot because the 13% cumulative whole returns that the SPDR S&P 500 ETF Belief (SPY) is anticipated to generate via 2025. For this reason I consider shares of Chevron are a purchase proper now.