MarioGuti/iStock via Getty Images

A Stock in Drive

China Automotive Systems, Inc. (NASDAQ:CAAS) stock is a victim of China’s New Electric Vehicle and automotive sales industry success. This small company with a $108.97M market cap has been unnoticed for too long. The stock hit a high of $9.61 per share in early 2023. Subsequently, bad news disappointed investors in the EV industry, compounded by political and economic headwinds that undercut the stock’s momentum. 12 months later, CAAS shares closed just above $3.

But Times They Are A-Changin’. YTD, the stock is up 11.7% and has been up as much as 15%. Shares closed on May 22 at $3.67 per share. Momentum is building (+12.8% over the last 3 months) because China’s strategies and investments in domestic vehicle makers are deepening. So, we are holding to our Buy assessment of CAAS shares we made in previous articles.

China’s government is on a quest to dominate the global auto industry. A MarkLines report on Q1 ’24 vehicle sales and production claims, total sales of passenger cars are up 10.6% this year and 8.1% for commercial vehicles Y/Y. Most of these are gas-powered. In the NEV sector, China is the world’s largest producer. Another report claims China exported more cars than Japan, which dominated as the world’s largest car exporter for decades. By 2030, China-based automakers will make 75% of the vehicles sold domestically.

Many countries subsidize domestic industries directly or through tax incentives. Company management told shareholders in the Q1 ’24 earnings meeting that government subsidies in Q1 ’24 topped $1M over Q1 ’23. The success of China’s strategies and investments can be a long-term potential opportunity for China Automotive Systems investors.

The 30-year-old China-based company designs, manufactures, and sells power steering systems and parts to over 60 leading passenger and commercial vehicle makers primarily in China, Russia, Mexico, North America, Europe, and Brazil. Their success bodes well for the growth and profitability of CAS. The company is committed to R&D spending to spur sales; it spends ~4.5% of revenue annually on R&D, putting it above the auto parts R&D industry average of 4.2%. CAS owns 2 trademarks and +200 patents. It is focusing on integrating electronic chips into its power steering systems.

Headwinds Are Easing

As U.S.-China tensions rose over the last decade, America made life nearly impossible for Chinese EV makers to sell into the U. S. The former and current Presidents imposed restrictions and tariffs, claiming to protect American autoworkers and security interests. Foreign investors began avoiding and pulling out of Chinese companies. They feared China’s stock market collapse. Fear spread, compounded by a flailing real estate market, justifying Bloomberg to report that through 2023 foreign investors severely cut their holdings “for higher returns elsewhere.” Other factors contributed to CAS’s uneventful Q1 ’24 reports.

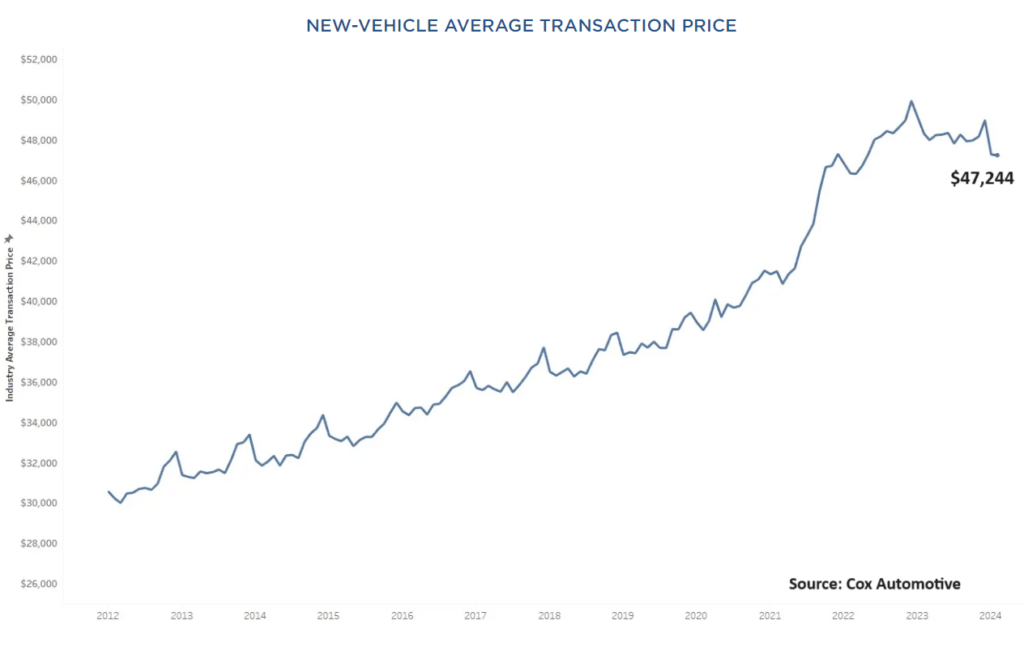

Cost of New Cars (Car Edge)

The company’s FY’23 financial earnings report released in March ’24 was positive. Net sales set a record, gross margin rose, and diluted net income per share popped +81% to $1.25. CAS management told shareholders that Q1 ’24 results were softer. Net sales slipped -2% to $139.4M. North American sales declined due to less consumer demand, high interest rates, and trade tariffs as high as 27.5% faced by one of CAS’s Chinese customers. In a face-off, a Chinese automaker launched a car selling for ~$12K (in China) to rave reviews for craftsmanship. The Chinese are not caving easily to the political protectionism of the U. S. auto industry.

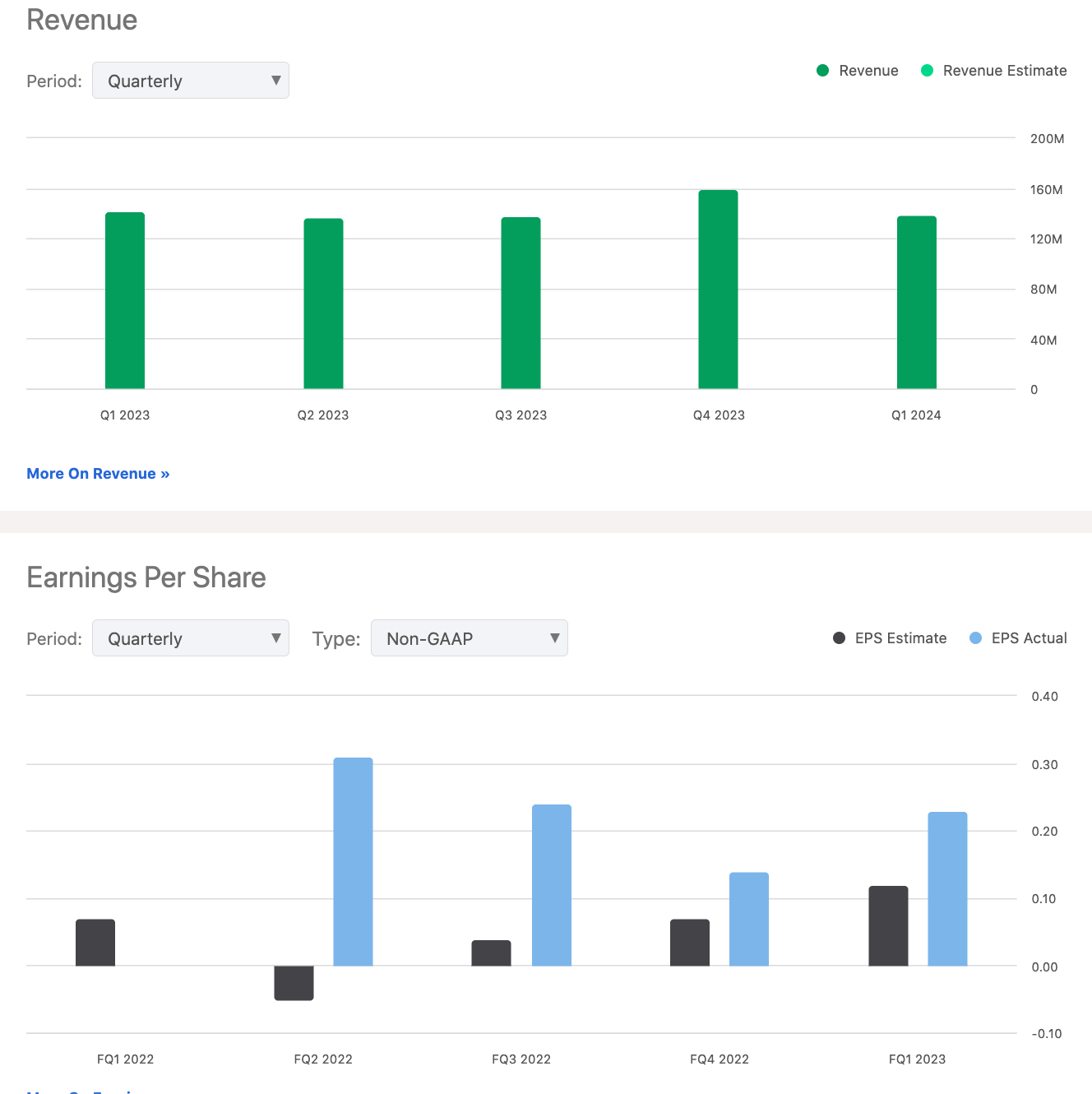

Revenue & Earnings CAS (Seeking Alpha)

Two other changes in the direction and intensity of headwinds are noticeable. First, there are reports that European automakers are investing heavily in China’s automobile industry and targeting the NEV sector. Fiat in Brazil and leading brand-name carmakers in Europe foresee China’s capacity to meet their growing consumer demand as an opportunity to expand sales. In 2002, China began permitting foreign ownership of passenger car manufacturing as another strategy for attracting foreign investment, reveals Seneca ESG.

Second, it appears now that hedge funds and other investors are again buying Chinese stocks. Foreign company investments last February touched $20B. Additional notable investments in Chinese companies’ stocks were made in 7 of the last 8 weeks; perhaps this accounts for the upturn in the price of CAAS shares.

Valuation

By our estimation, China Automotive has a fair value price of $3.60 per share; we multiply the 2.81 PE by the FY ’23 EPS of $1.25 to make this determination. We confirmed this by considering the company’s growth potential and momentum and the fundamentals including price-to-book (0.30), enterprise value of 71M, EV-to-EBITDA (1.9), and price-to-sales (0.197). The shares can potentially reach an average target price of $7 each over the next 12 months.

Another analysis using various PE multiples forecasts a 411% Real Valuation upside for CAAS shares. Value Investing concludes that “the range of the Relative Valuation is 14.28-25.48 USD” with a fair price of $18.45.

Takeaway

At the current share price, it is our opinion that China Automotive Systems shares are selling at a fair value and deserve our Buy-rating. There is the potential for greater revenue and profit in FY ’24 than the Q1 ’24 earnings report suggests. And there are political and economic risks to consider.

China’s strategies and investments in its automaker industry, particularly in the NEV sector, indicate the country’s leadership wants to dominate car making, which mirrors the dominance of their manufacturing of consumer goods, textiles and clothing, and electronics. China Automotive sells to low-price vehicle makers, luxury brand-name companies, and commercial producers. The company has the potential for a higher share price once it attracts investors who appear confident of better returns in Chinese company stocks.