FiledIMAGE/iStock Editorial by way of Getty Photos

Union Pacific Q1 Earnings

Jim Vena, Union Pacific’s CEO, is nailing it. We’re lastly seeing Union Pacific (NYSE:UNP) report stronger earnings and overperforming the trade, instead of being the laggard. Union Pacific’s earnings confirmed the corporate’s power amidst a mushy freight surroundings and Union Pacific’s shares jumped up over 4% because the press launch was out there. On this article, I’ll stroll you thru the report, displaying why I now see it acceptable to charge UNP as a purchase.

SA readers could know I have been extremely meticulous with Union Pacific, as I used to be somewhat disenchanted with rising inefficiency whereas the corporate was taking up increasingly debt to fund its beneficiant buybacks. Nevertheless, whereas shareholders did get pleasure from a pleasant experience up, the corporate’s fleet and community weren’t being maintained and renewed adequately. Because of this, Union Pacific’s buybacks repurchased shares of a enterprise with slowly deteriorating belongings, making me wonder whether the company was going off track or not. Then rates of interest spiked up and this blissful playbook got here to an finish: buybacks were paused to guard the stability sheet.

Eight months in the past, Jim Vena was appointed as the brand new CEO of the corporate to repair these actual points and make Union Pacific a real trade chief.

Union Pacific’s Turnaround Appears Starting

To begin with, a brand new approach of operating the enterprise will be seen in how the quarterly result presentation is now constructed. We lastly see one thing distinctive within the trade, one thing I’ve lengthy needed to see railroads report.

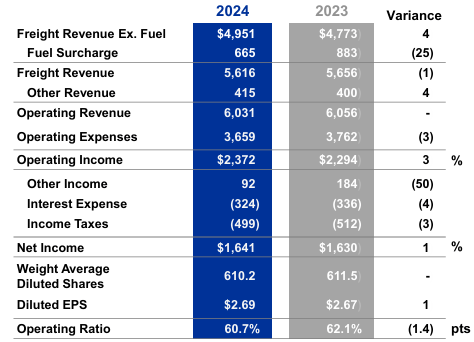

Union Pacific studies its freight income excluding the gas surcharge, which is then added as a separate merchandise. That is of utmost significance to evaluate the operations of a railroad. Certainly, gas surcharges vastly affect complete revenues by both rising or lowering them. Since railroads do not launch the precise quantity earned by these applications of their quarterly studies (we normally discover extra data within the annual studies), it’s tougher to know if a railroad is gaining quantity and whether it is flexing its pricing energy.

Union Pacific makes this a lot simpler now and this proves to me that Mr. Vena needs to be crystal clear in regards to the enhancements he’s executing in Union Pacific’s operations.

UNP Q1 Earnings Presentation

So, proper off the bat, we see that Union Pacific did report complete revenues down 1% YoY to $5.62 billion as a substitute of $5.66 billion. But, freight income really elevated by 4% YoY if we excluded the gas surcharge. This implies the worth/combine was favorable for Union Pacific.

Working bills moderated and had been down 3% YoY. Particularly, Union Pacific’s administration pressured that the corporate has decreased its energetic fleet by parking round 500 locomotives round its community. This has the double benefit of smoother operations and decreased prices. Furthermore, it helps the corporate’s gas effectivity as a result of older locomotives are stopped, whereas newer ones hold operating.

The consequence on the working ratio had been significant: an enchancment of 140 bps, from 62.1% all the way down to 60.7%. If Union Pacific retains strolling down this highway, we should always quickly see it report an OR beneath 60%, which might most likely foster renewed pleasure for the inventory.

Union Pacific’s web earnings elevated 1% YoY due to a 3% enchancment in working earnings. Because of this, UNP’s earnings per share elevated by $0.02 to $2.69 with out the assistance of any share discount. Contemplating that in Q1 2023, there was a $0.14 per share actual property achieve, as Union Pacific disclosed throughout its final earnings call, we see that Union Pacific is making nice strides towards enhanced profitability.

Union Pacific’s Volumes

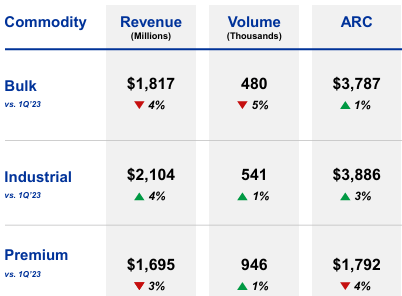

Union Pacific studies its freight revenues underneath three fundamental segments: bulk (grain, fertilizers, meals, and coal); industrial (petrochemicals, metals, minerals, forest merchandise, power); and premium (automotive and intermodal).

Bulk delivered a income decline of 4% to $1.82 billion, although quantity was down 5%. This implies the typical income per automobile (ARC) was up 1% YoY to $3,787. Nevertheless, bulk was vastly affected by coal, whose carloads had been down 18% and triggered a 23% decline in revenues to $388 million from $505 million a yr in the past. Nonetheless, the general phase held up pretty nicely, due to the great 8% improve in fertilizers and meals merchandise. These two segments have a a lot increased ARC than coal: $4,271 for the previous and a staggering $6,231 for the latter. Coal hovers round $2,200.

So, if we alter for coal, though the freight surroundings is at the moment mushy, Union Pacific would have delivered a rise in volumes of virtually 2%. That is a part of the outperformance we had been anticipating.

Coal is projected to be weak for the entire yr as a result of inventories are rising and pure gasoline is again to low and inexpensive costs.

UNP Q1 Earnings Presentation

Let’s take a look at the opposite two segments.

Industrial’s efficiency happy buyers and should verify that a manufacturing rebound is on its approach. In reality, petroleum grew 11%, each in freight and in quantity. Petrochemicals’ quantity was up 4% YoY and income did even higher with a 7% improve. This implies Union Pacific had pricing energy right here. Rock (metals and minerals) volumes, however, had been mushy and had been down 10%, although freight revenues declined solely 4%. Union Pacific’s administration mentioned that it expects “the rock market to be challenged to exceed last year’s record volume”.

Premium, opposite to the title’s that means, is the phase with the bottom ARC of the three: solely $1,792. Right here, automotive retains on performing nicely, with volumes and revenues up 4%, due to some wins Union Pacific had with Volkswagen and Common Motors. However I anticipate automotive to average all year long as sellers’ inventories replenish and demand softens as a consequence of excessive rates of interest. Intermodal volumes had been constructive within the quarter. This alone is nice information. Particularly, intermodal was pushed by robust worldwide West Coast demand, partially due to site visitors shift away from the Panama Canal. Nevertheless, home intermodal proved mushy and this goes together with the lower-than-expected GDP print that simply got here out.

Union Pacific’s Steadiness Sheet

Union Pacific had to enhance its stability sheet, reducing its debt/EBITDA ratio. We see that previously three months, the money stability decreased by $130 million. On the similar time, Union Pacific paid again $1.36 billion of LT debt, over twice as a lot YoY. As well as, it issued solely $400 million of latest debt in comparison with $1.2 billion issued in the identical quarter of final yr.

Due to LT debt reimbursement of $1.3 billion throughout the quarter, Union Pacific’s adj. debt/EBITDA ratio is now beneath the 3x threshold, at 2.9x, confirming the A-rating on its stability sheet.

Nevertheless, properties did not improve a lot, that means we’re nonetheless not in an enhancement cycle.

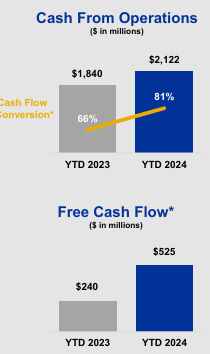

Union Pacific’s Free Money Movement

Union Pacific reported working money of $2.12 billion, which equals to a money move conversion of 81%. These outcomes laid the inspiration for the robust FCF technology Union Pacific reported: $525 million vs. $240 million.

UNP Q1 Earnings Presentation

This made the corporate assured sufficient to reveal that, beginning Q2 2024, the corporate will resume repurchasing its shares. We do not know the way a lot Union Pacific will spend. However, given the reported FCF, we may anticipate UNP to report just a few hundred million value of repurchases. This goes together with a dividend yield of two.24%, which is an effective begin.

Union Pacific’s Outlook

Union Pacific’s outlook expects the corporate’s profitability to achieve momentum whereas volumes are seen kind of flat YoY. What’s going to transfer the needle between development and decline might be worldwide intermodal. In reality, bulk is seen as kind of flat, whereas industrial is predicted to enhance regularly all year long. Premium, excluding worldwide intermodal, ought to be flat as automotive and home worldwide offset each other.

Union Pacific’s Valuation

We have now to provide credit score the place credit score is due. If Union Pacific begins rising as soon as once more, we’ll quickly see it receiving a much higher grade compared to the D+ it’s at the moment being given by SA’s Quant Scores.

The corporate trades at a 20.8 fwd PE, beneath the present earnings a number of of the S&P 500, which is round 23.5 on the time of writing. Furthermore, Union Pacific trades at a fwd FCF yield of 4.2%, which positions the inventory as an attention-grabbing choose.

Since I see a number of indicators hinting that Union Pacific’s turnaround could also be on its approach, we’re earlier than a inventory that might generate substantial returns within the subsequent few years throughout Mr. Vena’s tenure.

Because of this, I upgraded my UNP’s score from maintain to purchase, contemplating the inventory a lot safer now than it has been within the latest previous.