Tippapatt

Thesis

Credit score Suisse Asset Administration Earnings Fund (NYSE:CIK) is a reputation we have now lined earlier than extensively, with the final piece on the CEF coping with the UBS / Credit score Suisse merger and implications for his or her funds. On this article we’re going to revisit the title on the again of a vicious rally in danger belongings previously six months, rally which has seen excessive yield spreads tighten extensively, and names reminiscent of CIK rally to what we imagine are unsustainable ranges.

A great deal of CCC names on this CEF

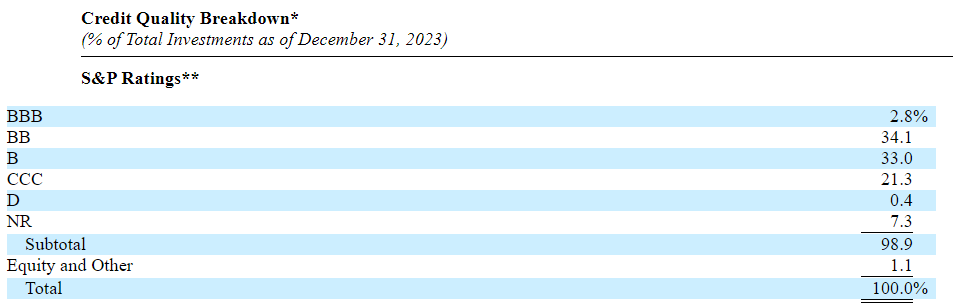

If we have a look at the scores parsing for the CEF, we are able to see this can be a very risk-on automobile:

Scores (Annual Report)

The CEF has a really giant ‘CCC’ bucket that stands at 21.3% as of December 2023. This interprets right into a excessive volatility and sensitivity to the default cycle. When the CEF’s leverage is taken into account, presently at 27%, we get a greater image on how the basics can transfer from a pricing perspective.

The fund has a tough ‘a 3rd’ allocation to BB, B and CCC names, however to notice that the majority funds have a cap at 10% of belongings for riskier CCC debt. Any such debentures are the riskiest types of HY debt, and S&P describes them as:

An obligation rated ‘CCC’ is presently weak to nonpayment, and depends upon favorable enterprise, monetary, and financial circumstances for the obligor to fulfill its monetary dedication on the duty.

A lot of the names on this fund are mounted charge bonds, thus the CEF can also be working a little bit of rate of interest danger:

Composition (Annual Report)

From that angle the fund is properly set-up, with our ‘home view’ that peak charges are behind us, regardless of the sticky inflation image that has materialized previously weeks.

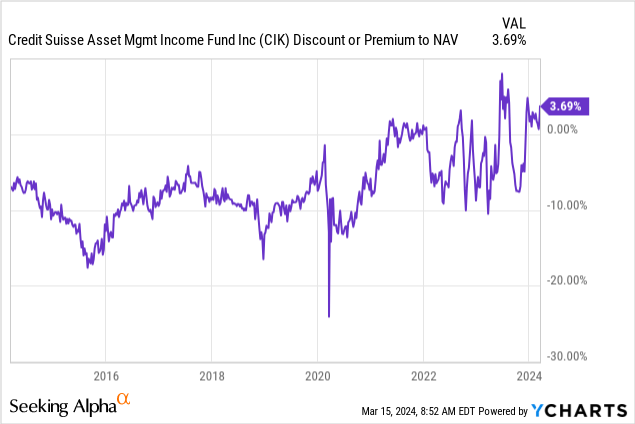

Eye popping rally has seen the CEF transfer to a premium

CIK has traditionally traded at a reduction to internet asset worth:

On a 10-year look-back we are able to see how the title has often traded at a tough -10% low cost. There are temporary intervals of time nevertheless when it was buying and selling flat to NAV, particularly in the course of the 2020/2021 zero charges surroundings. Shockingly, the CEF is now buying and selling at a 3.69% premium to internet asset worth. We really feel these ranges are overextended, and HY CEFs shouldn’t commerce on the prime of their vary when danger free charges are nonetheless above 5%.

The fund has a premium to NAV Z-statistic of 1.07, representing the usual deviations above the imply for the fund’s premium/low cost to NAV. The principle offender right here is the ‘comfortable touchdown’ narrative that has seen a clamoring for danger in any format (excessive yield, progress shares, bitcoin). We imagine in imply reversion, and the introduction of a story that introduce a component of doubt round an ‘immaculate’ comfortable touchdown. We expect a -5% underperformance right here from the premium shifting to barely under internet asset worth in such an occasion.

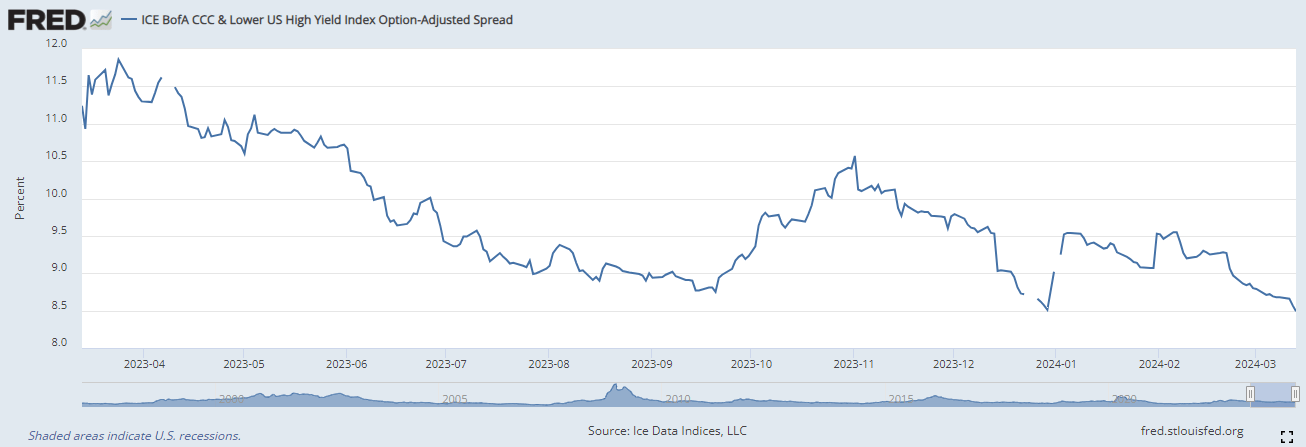

Spreads have rallied considerably

The principle danger issue for this fund is represented by CCC spreads:

CCC Spreads (The Fed)

As per the above graph, courtesy of the St. Louis Fed, CCC spreads have rallied from 11.5% to eight.5% presently. Contemplating Fed Funds are at 5.3%, the credit score danger part is now a mere 3.2%, not ample in our view to compensate the fund for the chance taken.

In impact, CIK is now yielding solely 8.7% which is a really low determine when leverage is taken into account. Suppose that many quick dated bond funds can go to buyers over 6% as of late. Do you have to take leveraged CCC danger for 8.7%? We predict not.

In our view the CEF ought to pay in extra of 10% as a distribution so as to make the chance/reward bundle engaging. At present ranges buyers are higher served by decrease volatility choices or floating charge ETFs or CEFs which yield in extra of 10% with decrease danger metrics.

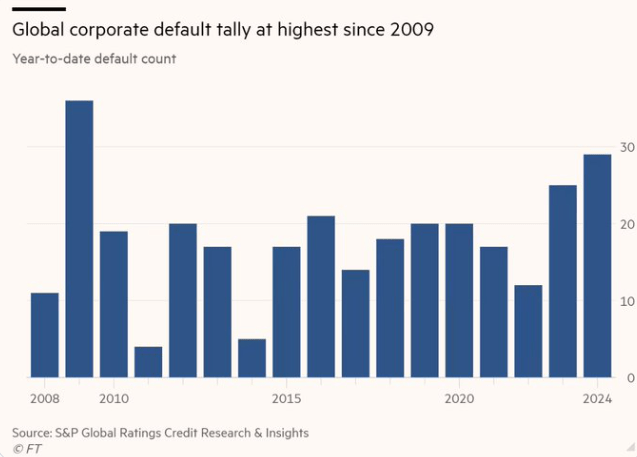

Defaults are climbing

The rally in CCC spreads has been primarily pushed by the ‘immaculate touchdown’ narrative, all whereas fundamentals aren’t shifting in the identical route:

Defaults (FT)

As an investor you usually need credit score spreads to tighten on the again of an bettering default image. The other has occurred right here. Company defaults are nonetheless climbing, all whereas credit score spreads have tightened. One thing must give, and we imagine the weak point will likely be in credit score spreads.

Our home view is for credit score spreads to widen from right here, because the ‘greater for longer’ rate of interest surroundings begins taking its toll on firms with floating charge financing or charge caps which mature. We’ve not but felt the complete impression of the upper charges surroundings as a result of throughout 2020/2021 many corporates had been capable of lock-in low-cost long run financing. After the Covid maturity wall trauma, many CFOs realized the significance of terming out their debt profiles, and ended up doing simply that. It’ll simply translate right into a protracted default surroundings.

For many individuals the present vacillations in unfold may be puzzling. Too many retail buyers assume a linear transfer in credit score spreads. The actual world is completely different, and it often depends on narratives. If the market is of the idea the economic system and the buyer will likely be high-quality, it should value excessive yield credit score for a benign default state of affairs, even when we nonetheless have materially greater defaults. Similar to equities, credit score spreads are ahead trying and spotlight the implied ahead market view. We presently imagine the market is simply too optimistic, and it’s due for a correction.

Conclusion

CIK is a hard and fast earnings CEF from Credit score Suisse. The fund focuses on mounted charge HY debt and holds a big allocation to CCC names. The CEF has traditionally traded at a reduction to NAV however is now priced at a 3.6% premium, highlighting the violence of the risk-on transfer previously six months. The automobile has seen this pricing on the again of a considerable rally in CCC credit score spreads, which now provide solely 3.2% greater than Fed Funds. We imagine we’re due for a correction in each credit score spreads and the CEF’s premium to NAV, thus anticipating a tough -10% sell-off within the title. We had been holders of the title earlier within the 12 months however have now offered our place.