A businesswoman works in her office. AndreyPopov/iStock via Getty Images

Although I am self-employed, I have never run my own business. I can understand how difficult it is to lead a business to even remain a going concern over years, decades, or centuries, though.

Formerly working as an accountant, this is why I so deeply appreciate Dividend Aristocrats and Dividend Kings. These are businesses that have not only survived for decades. They haven’t just paid dividends for decades.

They have paid growing dividends to shareholders for decades. Doing so takes exceptional business models, operating fundamentals, and an awful lot of conviction.

As far as I’m concerned, Cincinnati Financial (NASDAQ:CINF) is one of the all-time great dividend growth stocks. In January, the company upped its quarterly dividend per share by 8% to $0.81. If it pays that dividend throughout 2024, it would be the 64th consecutive year CINF’s payout to shareholders has grown.

When I last covered CINF with a buy rating in December, I liked its growth prospects. I also found the balance sheet to be sound. Shares also looked to be a solid value.

Today, I’m reiterating my buy rating. CINF’s first-quarter results shared on April 25 were vigorous. The company’s financial positioning remains admirable. Finally, shares have grown in fair value enough to remain a value proposition.

The Perfect Storm Led To A Double Beat

CINF Q1 2024 Earnings Press Release

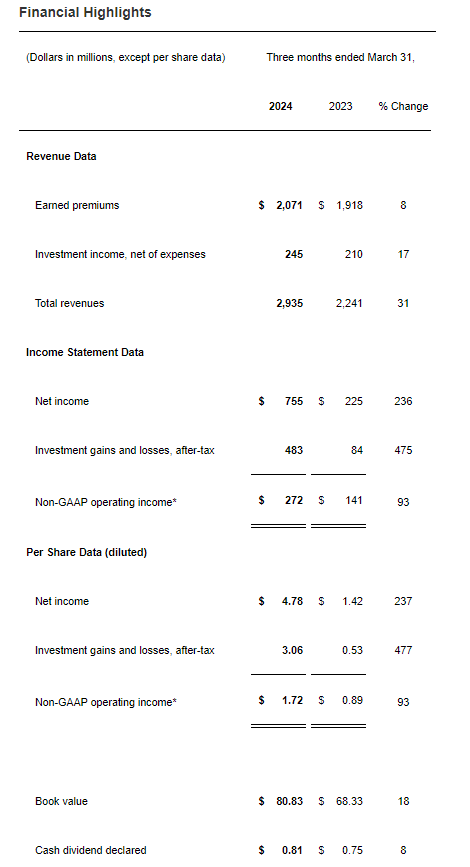

CINF came through with what I thought were exceptional results in the first quarter that ended March 31. The company’s total revenue rocketed 31% higher year-over-year to top $2.9 billion during the quarter. That came in ahead of the Seeking Alpha analyst consensus by a whopping $430 million.

A favorable operating environment for CINF and strength throughout the business contributed to these results.

As a P&C insurer, the company benefited from the higher interest rate environment via its $26.2 billion in debt and equity investments as of March 31. Along with higher dividend income, this pushed revenue from investment income higher by 16.7% over the year-ago period to $245 million for the first quarter.

Additionally, favorable valuation changes within the equity portfolio more than offset net losses within the bond portfolio per CFO Mike Sewell’s opening remarks during the Q1 2024 Earnings Call. That is what propelled revenue from net investment gains nearly six-fold higher to $612 million in the first quarter.

Lastly, CINF also shined on the earned premiums front. The continued additions of new agencies helped earned premiums to climb 8% higher to almost $2.1 billion during the first quarter.

CINF’s healthy showing for the first quarter didn’t end at the top line, either. The company’s non-GAAP operating income per share nearly doubled to $1.72 in the quarter. For context, this was $0.01 better than Seeking Alpha’s analyst consensus.

According to Chairman and CEO Steve Johnston, this was largely due to a $93 million decrease in after-tax catastrophe losses. CINF’s property casualty combined ratio of 93.6% was 7.1 points better than the year-ago period. Of note, 6.9% of that was because of a downtick in catastrophe losses, with the remainder being attributable to better underwriting.

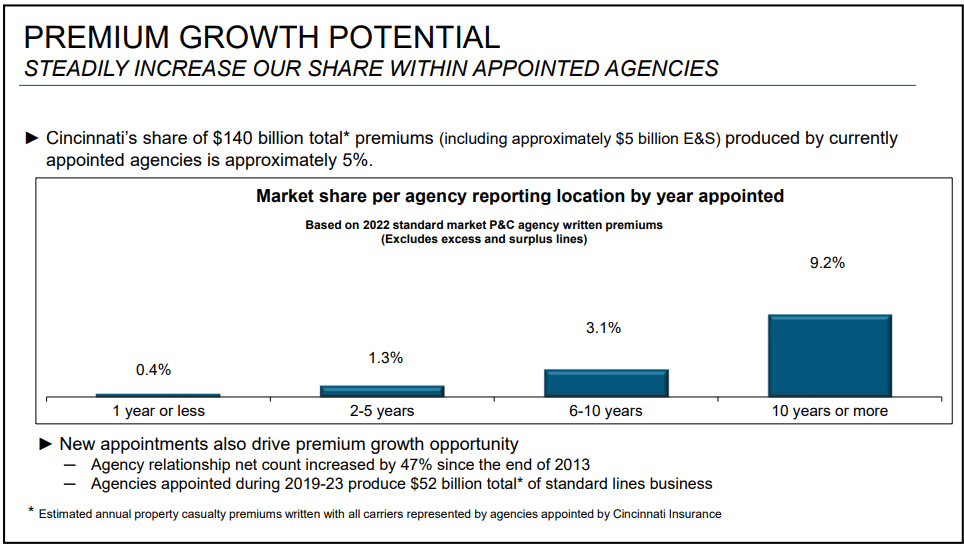

CINF May 2024 Investor Handout

The FAST Graphs analyst consensus also points to an optimistic outlook for the next few years.

On 10 analyst estimates, the consensus is that non-GAAP operating income per share will rise by 6.4% to $6.41 in 2024. For 2025, the consensus from 10 analysts has non-GAAP operating income per share growing an additional 8.1% to $6.93. On just one estimate, in 2026, it is predicted that non-GAAP operating income per share will increase by 5.7% to $7.32.

In my opinion, a closer look at CINF’s fundamentals supports these high-single-digit annual growth forecasts.

This is because, in the past four quarters, the company expanded the number of agencies marketing its products by 6.4% to 2,125 as of March 31, 2024. Simply put, the company’s exceptional reputation within its industry is leading more agencies to carry its insurance products.

The longer that these products are offered at these agencies, the more market share they tend to gain. This is reflected by a 0.4% market share at agencies appointed in 1 year. That climbs to a 9.2% market share at agencies appointed 10 years or more ago.

As more agencies are added and the market share at recently appointed agencies keeps growing, earned premiums will keep climbing. This will also fuel investment float growth. Combined with CINF’s unique approach of 43.7% of its investments in equities, book value should continue to grow at a respectable clip.

CINF’s balance sheet is also robust. The company’s debt-to-capital ratio was just 6.1% as of March 31, 2024. This was well below the 20% that rating agencies prefer from the industry per The Dividend Kings’ Zen Research Terminal. That is what underpins investment-grade credit ratings from the three major rating agencies: An A- credit rating from Fitch, an A3 credit rating from Moody’s, and a BBB+ credit rating from S&P (unless otherwise sourced or hyperlinked, all details in this subhead were according to CINF’s Q1 2024 Earnings Press Release, CINF’s Q1 2024 10-Q Filing, CINF’s May 2024 Investor Handout, and CINF’s Q1 2023 10-Q Filing).

Fair Value Has Surpassed $130 A Share

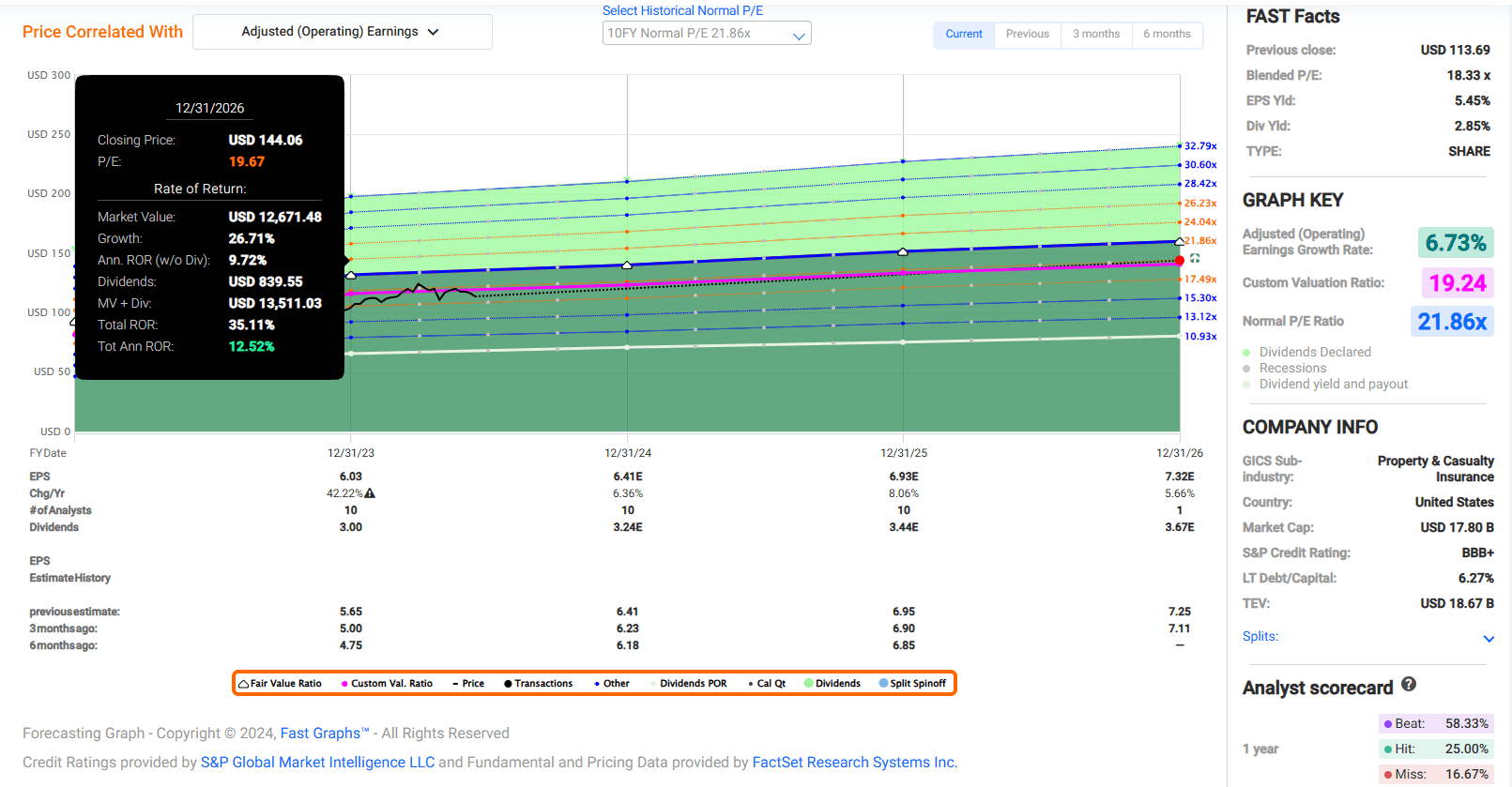

FAST Graphs, FactSet

Since my previous article, shares of CINF have gained 12%. That has largely kept up with the 14% rise in the S&P 500 index (SP500) in that time.

Yet, I think shares are about as attractive of a value now as they were in December. CINF’s current-year P/E ratio of 17.7 registers under the 10-year normal P/E ratio of 21.9 according to FAST Graphs.

I believe that a reversion to a 19.7 multiple or one standard deviation below this valuation multiple is fair. This is because CINF’s three-year forward annual growth consensus of 6.7% is a bit below the 10-year average of 8.2%.

When this week ends in a few days, 2024 will be 46% complete. That leaves another 54% in 2024 and 46% of 2025 ahead in the next 12 months. This is how I’m calculating a 12-month forward non-GAAP operating income per share input of $6.65.

Assigning a fair value multiple of 19.7 to this earnings input produces a fair value of $131 a share. That works out to a 13% discount to fair value, which is comparable to when I last covered the stock. If CINF reverts to my fair value multiple and matches the growth consensus, it could have a 35% upside ahead through 2026.

There’s More Upper-Single-Digit Dividend Growth Ahead

On paper, CINF’s 2.9% forward dividend yield doesn’t stand out. After all, it’s below the financials sector median forward dividend yield of 3.7%. This earns CINF a C- grade for forward dividend yield from Seeking Alpha’s Quant System.

Elsewhere, the company boasts impressive grades. CINF’s exceptional dividend growth streak is almost six times the financials sector median of 11 years. This is enough to receive an A+ grade from the Quant System for dividend consistency.

CINF is slated to pay $3.24 in dividends per share in 2024. Against the $6.41 non-GAAP operating income per share consensus, that would be a 50.5% payout ratio. This is in line with the 50% payout ratio that rating agencies desire from the industry, per the Zen Research Terminal. That earns CINF an A- grade for overall dividend safety from the Quant System.

Couple this payout ratio with the high-single-digit annual growth forecast and the Quant System’s projection for future dividend growth makes sense: CINF’s 7.3% annual forward dividend growth prospects are well above the financials sector median of 4.2%. Thus, it is awarded a B+ grade on this metric from the Quant System.

Overall, a nearly 3% starting yield and high-single-digit annual dividend growth is a nice pairing in my opinion.

Risks To Consider

For my money, CINF is a world-class business. It still has risks, though.

One risk is the potential for a cyber breach. The company has a significant amount of sensitive data, which makes it a frequent target of attempted cyber breaches.

If any were materially successful, sensitive data could be compromised. This could lead to sizable lawsuits against CINF and a deterioration of its reputation. In a worst-case scenario, that could break the growth story.

CINF also operates in a competitive industry. If policy pricing is too aggressive, the company risks losing market share. If policy pricing is too lax, underwriting profits could take a hit. So, it needs to balance appealing to the budgets of potential policyholders with smart underwriting. It’s a very fine needle that CINF has threaded for decades and must continue to do so to maintain its success.

Any major natural disasters, man-made disasters, or terrorist attacks could result in a surge of claims. On the off chance that CINF’s insurance float proves to be inadequate, this could create a liquidity crisis.

Summary: The Returns From This Business Could Be Anything But Boring

In the investment universe, CINF is about as much of a blue chip as is humanly possible. The company’s business model is thrusting earned premiums and the insurance floats higher over time. CINF’s balance sheet is respectable. Best of all, shares in this business can be purchased at an interesting valuation. For these reasons, I think the returns from this otherwise boring business could be reasonably exciting for the next few years.