Mario Tama

Citigroup (NYSE:C) appears to be like very low-cost, buying and selling at round 0.6x P/TBV. Nevertheless, the U.S. banking large has traded at these distressed multiples for over a decade now, and buyers are probably doubting that low valuation alone is a catalyst for upside. However it just isn’t solely the low valuation that’s talking for Citigroup: The financial institution has recently been making good progress in restructuring its operations, organising for an increasing cost-to-income ratio going into 2024 and past. Furthermore, conviction on charge cuts is constructing confidence on an enhancing credit score atmosphere, with each supportive mortgage progress and manageable write-downs on the financial institution’s existent ebook. For my part, this backdrop might drive multiples greater shortly.

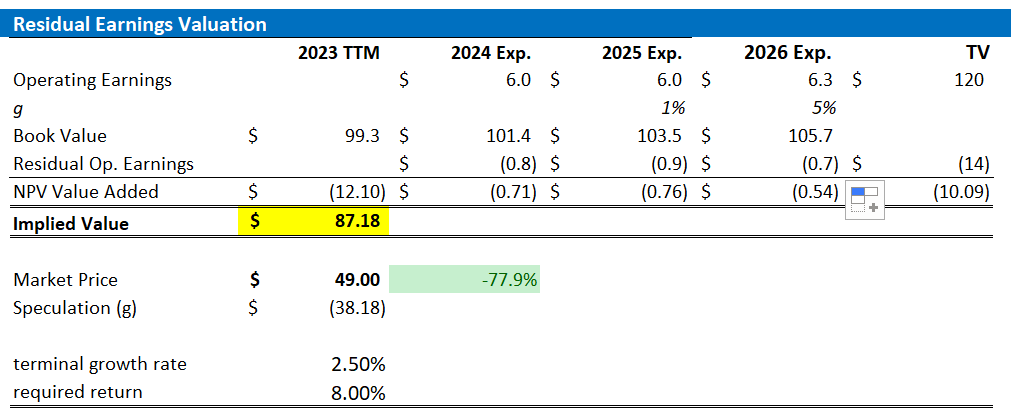

Going into 2024, I replace my residual earnings valuation mannequin for Citigroup inventory; I now calculate a good implied share value equal to $87.18/ share. Reiterate “Strong Buy”.

I’ve covered C inventory about two months in the past, additionally with a “Strong Buy” score. Nevertheless, since then, the Fed shifted dovish fairly aggressively and Citi CFO Mark Mason offered buyers with extra steering. On this article I’ll focus on an up to date view on Citi.

Macro Setting A Tailwind For The Banking Business

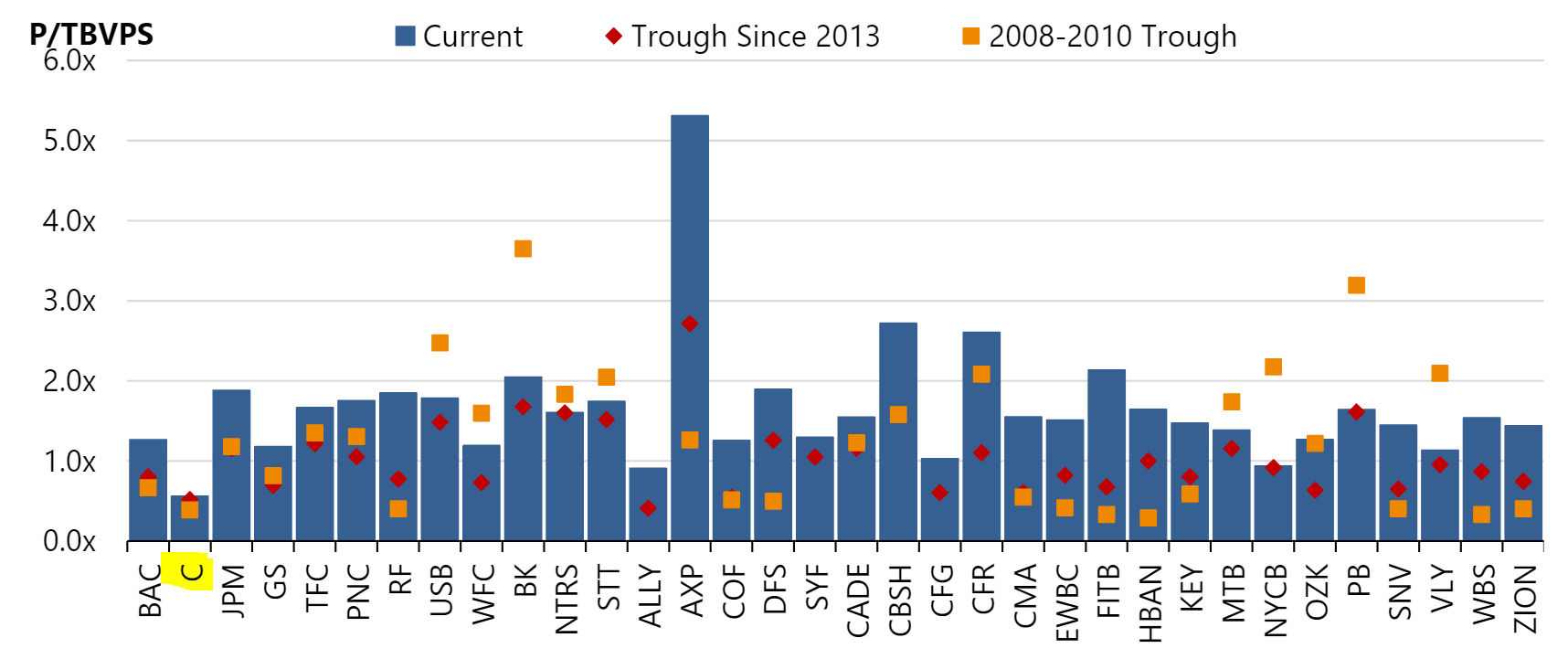

The 12 months 2023 offered fairly a troublesome macro for financial institution shares, much less so for fundamentals than for sentiment: The Q1 failures of Silicon Valley Financial institution and banking icon Credit score Suisse prompted buyers to concentrate on the unfavorable implications of the speed cycle, most notably unrealized losses on the steadiness sheet and funding stress. This precipitated the business to commerce at very low multiples, corresponding to ranges seen round 2008/09 throughout the Nice Monetary Disaster. Extra exactly on Citigroup, the financial institution’s inventory is at the moment buying and selling at a 0.6x P/TBV, in comparison with troughs of 0.5x for each the time interval 2008-2010 and 2013-TTM, respectively (Morgan Stanley analysis observe dated eighth December: Title: US Banks and Shopper Finance: {Dollars} and Cents).

Morgan Stanley Fairness Analysis

These sentiment headwinds ought to notably fade going into 2024, in my view, as financial coverage makers are getting ready for important charge cuts. In that context, on December 13, the FOMC shared their up to date financial projections, stunning markets with a dovish shift. Notably, the committee lowered their inflation estimates for EOY 2023 to 2.8-2.9% from the earlier 3.2-3.4%, whereas boosting GDP progress forecasts from 2.1% to 2.6%. This indicators a picture-book-like macro atmosphere — reducing inflation and growing progress — and considerably challenges the notion of a “Hard Landing.” Accordingly, the FOMC’s revised outlook now predicts round 75 foundation factors in charge hikes for 2024, a big shift from the earlier expectation of solely 25 foundation factors. Though the FOMC is leaning towards a dovish stance, merchants are much more optimistic. Notably, CME’s fed funds tracker suggests an anticipated 150 foundation factors in cuts by 2024 EOY, projecting charges round 3.75%.

That mentioned, about 100-200 foundation level decrease charges ought to materially increase valuation multiples for financial institution shares. Firstly, I level out that fairness multiples usually are inversely associated to charges. Secondly, buyers ought to take into account {that a} dovish charges shift might defend financial institution’s internet curiosity earnings. That is anchored on a softening deposit beta, in addition to an increasing demand for credit score on the backdrop of a pick-up in financial exercise. Thirdly, I anticipate decrease charges to stimulate funding banking exercise, most notably ECM, DCM and M&A quantity.

Citi CFO Provides Bullish Steering

Citigroup’s CFO Mark Mason not too long ago updated buyers relating to the financial institution’s basic outlook: Presenting at Goldman Sachs’ Monetary Providers Convention, Mr. Mason projected Citi’s 2023 revenues to settle within the vary of $78-79 billion, as he emphasised a supportive Internet Curiosity Earnings backdrop of round $47.5 billion. Extra notable than the quick time period steering, nonetheless, was the CFO’s expectation for future topline progress, bills and ROTE targets. In that context, Citi now initiatives a 4-5% CAGR income progress purpose by way of 2026, rising topline to $87-92 billion. In the meantime, the financial institution’s working expense base is focused to compress to round $51-53 billion per 12 months, notably beneath the 2023 bills of round $54.3 billion. If the targets are achieved, the financial institution would understand a 11-12% ROTE.

In keeping with the CFO’s commentary, Citi’s progress outlook is properly supported by the financial institution’s segments: In Treasury and Commerce Options, administration highlighted that roughly half of the 18% surge in revenues weren’t influenced by charges. If that is true, and progress is extrapolated at an identical charge to 2026, then Citi’s TTS might materialize as a lot as $4 billion of incremental topline upside. The expansion story in Funding Banking is sort of apparent, because the phase is ranging from a really depressed 2023 base. As exercise picks up in keeping with an increasing financial system, charges might develop wherever between $1-3 billion as advised by the latest up/ down cycle 2019-2023. In Wealth Administration, Citi administration has advised a bullish alternative for fairly a while now, because the financial institution goals to spice up market share from 2% to doubtlessly usher in $2-3 billion incremental income within the coming years. The excellent $2-3 billion income delta to realize the group’s 4-5% CAGR income progress goal might from Markets/Buying and selling and/or the financial institution’s Card division, which ought to be fairly possible, in my view.

Set Goal Worth at $87.18

According to my bullish outlook for Citi’s consensus EPS by way of the subsequent 3 years, I replace the enter for my residual earnings valuation mannequin for the financial institution’s inventory: I now estimate that Citi’s EPS in 2024 will probably fall inside the vary of between $5.8 and $6.2. Equally, I set ,y EPS expectations for 2025 and 2026 to $6.0 and $6.3, respectively. I proceed to anchor on a 2.5% terminal progress charge, which I see about in keeping with nominal GDP progress, in addition to on an 8% value of fairness requirement. On the backdrop of the highlighted EPS expectations, I calculate a good implied inventory value for C inventory equal to $87.18, suggesting nearly 80% upside!

Analyst Consensus; Firm Financials; Writer’s Calculations

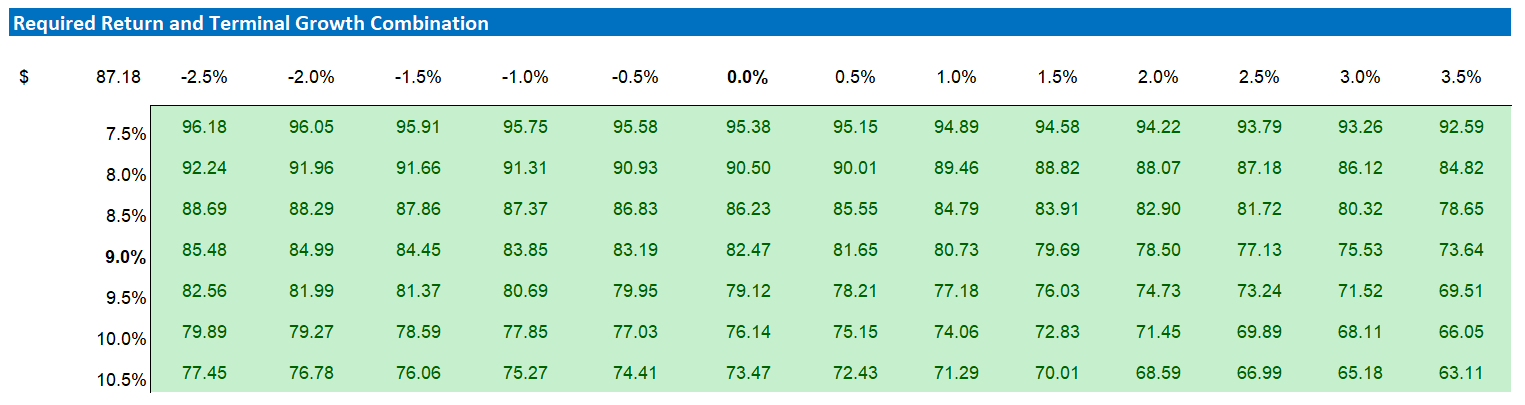

Beneath additionally the sensitivity desk, which assessments completely different assumptions for value of fairness (row) in addition to terminal progress charge (column).

Analyst Consensus; Firm Financials; Writer’s Calculations

Conclusion

Citigroup inventory appears to be like very low-cost at round 0.6x P/TBV. The low valuation a number of is particularly engaging together with a shortly enhancing macro backdrop, in addition to the financial institution’s sturdy basic inflection. In keeping with a current CFO presentation, Citi administration now sees a path in the direction of 10-11% ROTE by 2026, by suggesting a 4-5% CAGR topline CAGR over the subsequent 3 years on a falling working expense base. On that data, I replace my residual earnings valuation mannequin for Citigroup inventory and I now calculate a good implied share value equal to $87.18/ share.

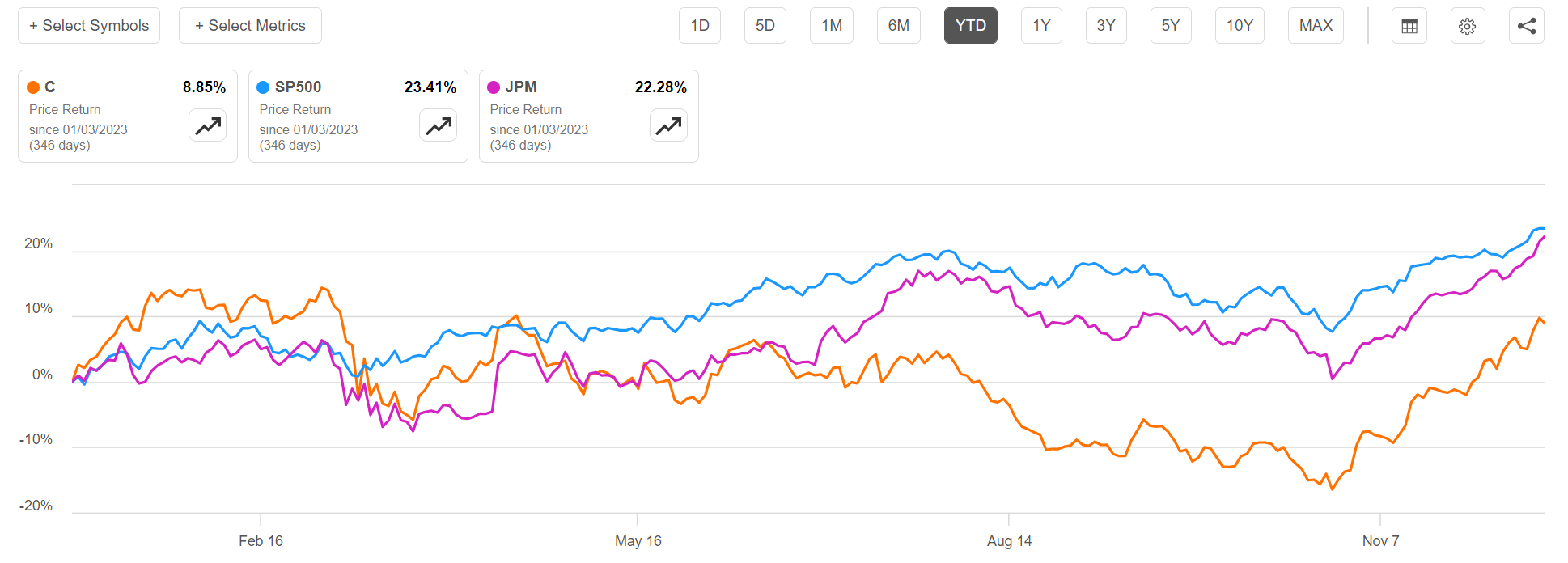

For context, Citigroup inventory has underperformed the market YTD. For the reason that begin of the 12 months, C inventory is up lower than 9%, in comparison with a achieve of 23% and 22% for the S&P 500 (SP500) and banking business chief JPMorgan (JPM), respectively.

In search of Alpha