Jordan Feeg

By Garey J. Aitken, CFA, & Michael Richmond, CFA

Upgrading Portfolio High quality into Power – Market Overview

After almost two years of managing by means of steadily larger coverage charges and common prognostications of financial troubles, traders clearly anticipated 2024 to be a transition yr. Somewhat than a change, the primary quarter of 2024 appeared very like 2023. The broadly held expectations of additional disinflation, a softer actual economic system and decrease coverage charges have confirmed largely misplaced: inflation has remained sticky and above central financial institution targets, the economic system has been strong and forecasts for decrease coverage charges have been frequently pushed later into the yr and 2025.

North American equities have shrugged off these altering views on the economic system and better rates of interest with U.S. equities, the S&P/TSX Composite and the S&P/TSX Small Cap Index all up meaningfully within the first quarter. The mega-trend trades of synthetic intelligence (AI) and GLP-1s broadened out to incorporate a wider fairness participation as traders turned comfy with earnings progress and valuations throughout plenty of sectors, whatever the path of rates of interest.

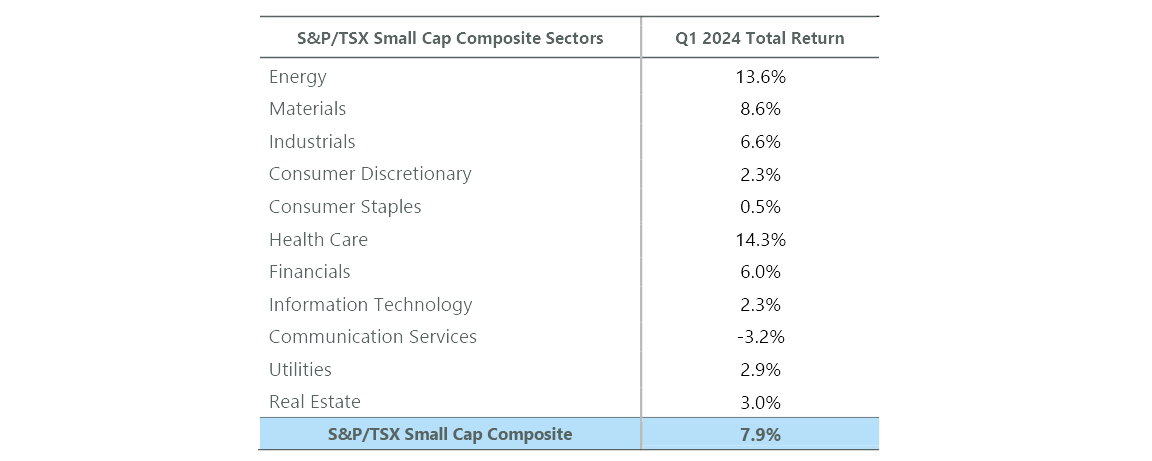

The S&P/TSX Small Cap Whole Return Index elevated 7.9% within the first quarter. The index’s heavy-weight commodity sectors led the best way larger, with vitality (+13.6%) and supplies (+8.6%) two of the three sectors to outperform the broader index. The U.S. crude benchmark worth (WTI) moved from US$71/bbl on the finish of 2023 to US$83/bbl on the finish of the quarter. The mix of a stronger than anticipated international economic system, muted U.S. exercise/manufacturing, and OPEC+ manufacturing curtailments has tightened the supply-demand outlook for crude, pushing costs larger. Canadian oil and gasoline producers entered this cycle from a place of power. Steadiness sheets are, on common, extremely robust and firms have held the road on capital commitments. In consequence, liquids producers are testing highs set in the summertime of 2022 when crude pricing was above US$120/bbl.

Exhibit 1: Small Cap Sector Efficiency

Supply: FactSet.

Oilfield service corporations additionally had a really robust begin to the yr as fears round declining North American drilling and completions exercise abated with stronger commodity costs. The small cap oilfield group was up 16.4% through the quarter.

Gold costs added gasoline to the commodity commerce in March. Gold reached an all-time excessive of US$2,250/oz through the quarter and has subsequently moved larger. Curiosity in gold producers and builders moved down the market cap vary with the metals and mining subsector rising by over 10% within the quarter, with the transfer occurring totally throughout March.

Rate of interest delicate sectors continued to fall behind the small cap index. Actual property (+2.9%) and utilities (+2.9%) lagged in a robust market whereas shopper discretionary (+2.3%) and shopper staples (+0.5%) sectors additionally underperformed on a mixture of idiosyncratic strikes throughout the sectors and basic weak spot from the Canadian shopper.

The Canadian small cap info expertise (IT) sector was surprisingly weak given the broader efficiency of North American expertise, up simply 2.3%. The restricted variety of AI-related expertise equities within the Canadian small cap index made inventory choice a key driver of efficiency.

Well being care was a standout performer in Canada (+14.3%), however it’s value stressing that efficiency was the results of hashish corporations which have meaningfully underperformed in recent times as a result of challenged long-term prospects.

Portfolio Positioning

Our portfolio actions within the first quarter had been in step with the steps taken in 2023 to enhance the typical high quality of the holdings whereas remaining dedicated to our views on valuation. This resulted in us eliminating three positions through the quarter.

- We continued to trim equities which have carried out effectively and are approaching, or in sure circumstances have surpassed, our estimate of truthful worth, together with Celestica (CLS), DRI Healthcare (OTC:DHTRF), Fowl Development (OTCPK:BIRDF), Converge Expertise (OTCQX:CTSDF), and Propel Holdings (OTCPK:PRLPF). These are a set of high-quality enterprise which have carried out effectively and executed alongside our preliminary funding theses. Nonetheless, we stay disciplined in our valuation method and have trimmed positions into power.

- We exited our place in Neighbourly Pharmacy (OTCPK:NBLYF) following the finalizing of its take-private supply. We had been disillusioned by the implied valuation of the supply, however finally couldn’t see an avenue to floor additional worth and so we moved on.

- We eradicated our place in Whitecap Sources and reallocated towards elevated weights in different E&Ps: Parex Sources (OTCPK:PARXF), Headwater Exploration (OTCPK:CDDRF) and Kelt Exploration (OTCPK:KELTF). The transfer was made partly to extend the typical high quality of our E&P positions and to cut back our internet publicity to Western Canadian pure gasoline pricing. Whitecap has progressively shifted away from its historic roots as a traditional gentle oil producer towards a extra diversified pure gasoline, condensate and lightweight oil manufacturing profile. Given the macro headwinds going through Western Canadian pure gasoline, we determined to shift our E&P publicity towards high-quality pure-play crude producers (Headwater and Parex) and long-resource, Montney-focused pure gasoline/condensate (Kelt).

- We additionally exited our place in Blackline Security (OTCPK:BLKLF), a security expertise/service supplier to industrial purposes that had carried out effectively to develop and enhance profitability, however whose pathway to sustained profitability and acceptable return on invested capital stays unsure. In our view, the fairness worth through the quarter correctly mirrored the risked upside potential on Blackline, and we eradicated our place.

Outlook

Our funding method is a bottom-up technique that prioritizes figuring out and capitalizing on market inefficiencies, utilizing our proprietary analysis, and the time arbitrage that comes with our long-term funding horizon. This method is supported by our affected person tradition, enabling us to make well-informed selections when there are discrepancies between expectations and underlying fundamentals. We stay steadfast in our dedication to our funding model, diligently in search of out companies that exhibit smart capital allocation practices and structural aggressive benefits, can generate high-quality progress, and might accomplish that below acceptable capital buildings.

Our long-term, bottom-up funding method is agnostic to financial cycles, however as valuations in additional cyclical sectors turn out to be stretched, we proceed to search out alternatives in defensive areas of the market and people sectors which have been most negatively impacted by the rise in rates of interest. The Technique in consequence is obese the defensive utilities and shopper staples sectors and has lowered its relative weighting towards the extra closely cyclical sectors.

As we acknowledge the presence of dangers and uncertainties, we’re assured that the longer term will current each challenges and alternatives. We are going to seize on alternatives as they come up, leveraging our in depth observe document of delivering superior risk-adjusted returns over the long run.

Portfolio Highlights

The ClearBridge Canadian Small Cap Technique outperformed its benchmark within the quarter. It was 1 / 4 marked by two halves, with very robust relative efficiency in January and February partially reversing in March because the supplies sector posted an exceptionally robust month. On an absolute foundation, the Technique posted constructive returns in eight out of the ten sectors by which it was invested through the quarter (out of 11 complete).

On a relative foundation, inventory choice had a constructive impression on efficiency, and was partially offset by destructive sector allocation. Particularly, inventory choice in IT, well being care and shopper discretionary drove outcomes. Conversely, destructive choice in supplies, vitality and shopper staples, overweights to utilities and shopper staples and an underweight to supplies, specifically valuable metals, detracted from efficiency.

On a person inventory foundation, the most important contributors to absolute efficiency had been DRI Healthcare, Headwater Exploration, Celestica, Converge Expertise Options and Enerflex (EFXT). The biggest absolute detractors included Jamieson Wellness (OTCPK:JWLLF), Parex Sources, Boralex (OTCPK:BRLXF), Canadian Western Financial institution (OTCPK:CBWBF) and Richelieu {Hardware} (OTCPK:RHUHF).

Garey J. Aitken, CFA, Head of Canadian Equities

Michael Richmond, CFA, Director, Portfolio Manager

|

Previous efficiency is not any assure of future outcomes. Copyright © 2024 ClearBridge Investments. All opinions and knowledge included on this commentary are as of the publication date and are topic to vary. The opinions and views expressed herein are of the writer and will differ from different portfolio managers or the agency as a complete, and aren’t meant to be a forecast of future occasions, a assure of future outcomes or funding recommendation. This info shouldn’t be used as the only foundation to make any funding choice. The statistics have been obtained from sources believed to be dependable, however the accuracy and completeness of this info can’t be assured. Neither ClearBridge Investments, LLC nor its info suppliers are accountable for any damages or losses arising from any use of this info. Efficiency supply: Inner. Benchmark supply: Normal & Poor’s. |