Jira Pliankharom

By Sean Bogda, CFA, Grace Su, & Jean Yu, CFA, PhD

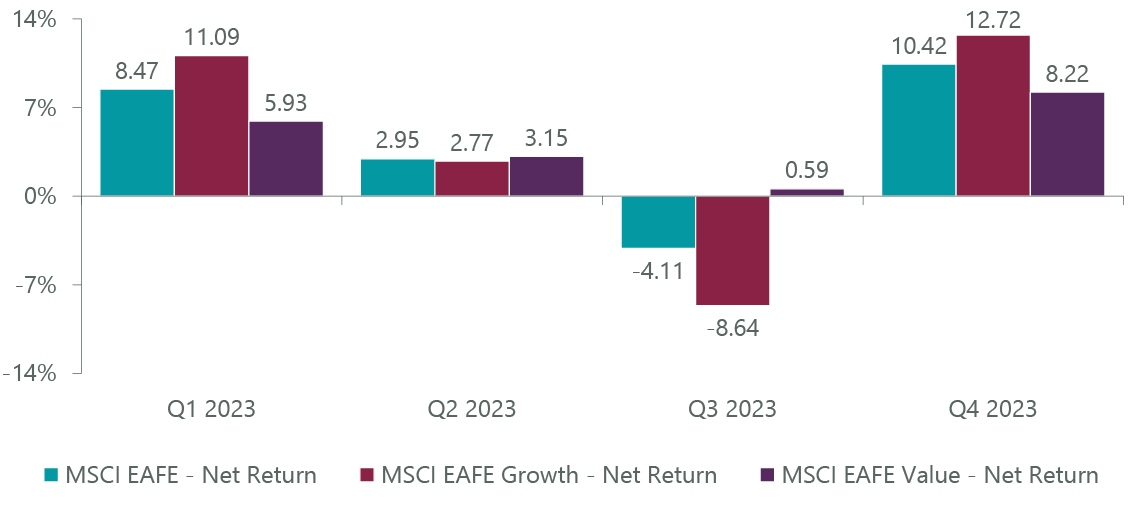

Worth Lags Broader Worldwide Rally

Market Overview

Worldwide markets generated optimistic returns within the fourth quarter, as disinflationary knowledge, renewed hopes of an financial smooth touchdown and declining bond yields within the U.S. and Europe overcame considerations over renewed hostilities within the Center East and continued financial challenges in China. The benchmark MSCI EAFE Index returned 10.42% for the quarter. A dovish coverage pivot by the Federal Reserve helped to spur progress shares forward of worth shares for the quarter, with the MSCI EAFE Progress Index returning 12.72% versus the 8.22% return of the MSCI EAFE Worth Index (Exhibit 1). Whereas the fourth quarter helped to slender the complete 12 months efficiency hole, the MSCI EAFE Worth Index nonetheless ended the 12 months forward of the Progress Index by roughly 140 foundation factors.

Exhibit 1: MSCI Progress vs. Worth Efficiency

Information as of Dec. 31, 2023. Supply: FactSet.

Regardless of investor considerations over the chance and timing of a recession getting into the quarter, worldwide markets rallied as disinflationary knowledge in Europe and the U.S. helped to resume buyers’ hopes that financial tightening had peaked. This helped to spur a rally in November and December, notably benefiting longer period sectors like info know-how (‘IT’) in addition to cyclical sectors on hopes of financial re-acceleration.

Nevertheless, this optimistic sentiment was not common. The fourth quarter additionally noticed the outbreak of struggle in Israel and reprisal assaults on cargo ships within the extremely trafficked Pink Sea, leading to elevated investor fears of a deteriorating geopolitical surroundings within the Center East and a detrimental impression on international provide chains as ships have been re-routed to safer, albeit longer, transport channels. On the opposite facet of the globe, financial knowledge out of China continued to show disappointing and failed to revive market confidence regardless of a myriad of measures and packages rolled out by Beijing geared toward re-igniting the home financial system. The scenario was additional exacerbated by a selloff in December, as investor redemptions and geographic repositioning resulted within the Chinese language market’s worst performing month of the 12 months and third-largest month-to-month outflow on file, in keeping with Morgan Stanley. Traders’ exit from China continued to assist bolster the Japanese financial system, which confirmed continued optimistic efficiency within the fourth quarter due to elevated investor demand stemming from company reform potential and perceived beneficiaries of a strengthening home financial system.

In opposition to this backdrop, the ClearBridge Worldwide Worth Technique underperformed its benchmark within the fourth quarter, as a mix of inventory choice within the industrials, financials and well being care sectors overcame optimistic contributions from our client discretionary shares.

Industrials proved to be the largest detractor from relative efficiency. Regardless of our obese allocation to the sector, a number of of our holdings did not hold tempo with the rally within the broader industrials sector. The varied nature of the sector, each geographically and throughout enterprise traces, could make it troublesome to find out short-term actions, however relatively than chase worth developments we proceed to concentrate on corporations with sturdy underlying companies and leveraged to long-term developments equivalent to automation and power transition. For example, one in all our prime performers through the quarter was Schneider Electrical (OTCPK:SBGSF), a French firm specializing in digital automation and power administration. We consider the corporate shall be a long-term beneficiary of the worldwide power transition given its sturdy place in numerous electrical power-related markets. The corporate’s inventory worth rose after one other quarter of sturdy earnings, and we consider the corporate’s rising ahead bookings level to continued progress.

Well being care additionally weighed on efficiency, centered in pharmaceutical holdings Bayer (OTCPK:BAYRY) and Sanofi (SNY). Sanofi, a French drug maker, confronted challenges because of revisions in its strategic and monetary outlooks after saying a $1 billion improve in analysis and growth to speed up its drug growth pipeline. Likewise, Bayer, a German pharmaceutical and agriculture firm, noticed its share worth decline after seeing disappointing outcomes from one in all its most anticipated anticoagulant pipeline medication, in addition to a authorized challenges in its crop enterprise resulting in elevated legal responsibility estimates. Our opinion is that the reactions in each circumstances have been overdone. With Sanofi, we consider that future price cuts and elevated R&D investments are anticipated to offset short-term earnings impacts and be helpful to long-term gross sales progress. Likewise, Bayer’s low valuation signifies that buyers have largely given up on any turnaround, which means that any excellent news – pharma price chopping, client well being sale, a rebound within the crop enterprise or any optimistic outcomes on the litigation entrance – may very well be a optimistic catalyst.

“From a geographic perspective, the clear value opportunity remains China.”

Inventory choice within the client discretionary sector was a optimistic driver. Our prime holding within the sector was Spanish clothes, footwear and equipment retailer Industria de Diseno Textil (OTCPK:IDEXY). The corporate’s flagship vacation spot retail model, Zara, has seen sturdy optimistic efficiency due to a rebound in tourism and the comparatively sturdy efficiency in southern European markets in comparison with northern Europe because of sturdy service elements of their economies. The corporate continues to ship sturdy execution pushed by funding in each its e-commerce and omnichannel operations to drive balanced progress. One other optimistic contributor was Arcos Dorados (ARCO), a Latin American proprietor/operator of McDonald’s fast service restaurant franchises. We consider the market has inherently sturdy progress prospects, and the corporate’s positioning as a frontrunner within the house has allowed them to seize important share. Moreover, we consider the corporate’s focused funding in its digital operations helps to additional drive gross sales.

From a regional standpoint, inventory choice in Europe was a detractor from efficiency. The biggest geographical allocation within the portfolio, Europe displays a difficult financial backdrop, and we proceed to guage our publicity to the area by specializing in investing in best-in-class companies at engaging costs. Slightly than see these downticks as disappointing, we consider these durations of underperformance present alternatives and this quarter isn’t any exception. We proceed to observe our European holdings to make sure they’re performing in-line with our expectations.

Portfolio Positioning

We made a number of changes to the portfolio through the interval, initiating three new positions and exiting one.

We added a brand new place in Cellnex Telecom (OTCPK:CLNXF), within the communication companies sector, a Spanish-headquartered operator of wi-fi telecommunication infrastructure. As Europe’s largest impartial tower firm, Cellnex had capitalized on the low-rate surroundings to develop considerably however has been challenged in latest instances as charges spiked. Spurred by calls for from activist shareholders for a brand new administration staff, Cellnex has refocused its efforts on deleveraging its stability sheet, price optimization and enabling natural progress.

We additionally added Capgemini (OTCPK:CAPMF), one of many world’s main know-how outsourcing corporations. The French firm noticed its shares come underneath stress because of elevated considerations of a slowing macroeconomic backdrop and uncertainty surrounding the impression of generative AI on the demand for IT companies. Nevertheless, as extra readability has emerged surrounding the unbelievable complexity of generative AI, we consider it will really show a tailwind for Capgemini and result in compelling, long-term returns.

We exited Tencent (OTCPK:TCEHY), a Chinese language-based communication companies firm working within the value-added companies, internet marketing, fintech and companies companies industries. The corporate’s shares have been underneath stress for the previous few years because of investor considerations surrounding the Chinese language authorities’s scrutiny of the digital financial system, and the fourth quarter witnessed one other episode of potential regulatory modifications within the gaming enterprise. We consider these laws create important challenges to Tencent’s potential to deploy capital freely and maximize shareholder worth, and we elected to exit the place in favor of investments with a greater danger/reward profile.

Outlook

In distinction to the pessimism getting into 2023, the market seems to be pricing in a hopeful outlook for 2024, anticipating higher actual revenue progress, much less constraints from rising charges, margin upside from enter disinflation, and a return of accommodative financial coverage as sequential inflation knowledge eases again to focus on ranges. With the bar of expectations now raised, we consider it’s helpful to extend portfolio diversification.

On the one hand, we proceed to love corporations with secular progress tailwinds from megatrends equivalent to infrastructure spending and power transition, a lot of that are concentrated within the industrials sector. Complementing this, we additionally keep excessive publicity to deep worth areas, believing that fairness returns ought to broaden out to laggards at engaging valuations. The power sector is an efficient instance of this, with the sturdy profitability and capital self-discipline permitting corporations to return important quantities of capital whilst underlying commodity costs stay vary certain. Equally, in financials, we’re invested in effectively capitalized banks which have dedicated to important capital returns over the subsequent few years. Vitality and financials may additionally show to be good hedges if the market’s disinflation narrative fails to play out and we stay in a higher-for-longer regime. Lastly, selective defensive teams equivalent to utilities and client staples considerably underperformed final 12 months, permitting us to purchase insurance coverage towards a progress slowdown at compelling entry factors.

From a geographic perspective, the clear worth alternative stays China, the place the market is buying and selling at half the valuation of the worldwide index and the earnings yield to bond yield differential (5.7%) is the very best in twenty years. We hesitate to take a position on the subsequent strikes of the Xi administration however keep a number of high-quality names within the portfolio the place upside optionality is excessive. The opposite giant contrarian alternative we see is the U.Okay., the place Brexit and the price of residing disaster lately have deterred investor curiosity. Nevertheless, as actual wage progress and client confidence proceed to enhance, it’s a market that would play catchup, notably within the client and monetary sectors which stay very out of favor and attractively priced. Lastly, we proceed to search for alternatives so as to add to our Japan publicity because the financial system exits the deflationary period and additional implements governance reforms to bolster returns. As at all times, the aim is to construct a diversified portfolio of shares the place we consider danger/reward is mispriced and important alpha era is feasible.

Portfolio Highlights

The ClearBridge Worldwide Worth Technique underperformed its MSCI EAFE benchmark through the fourth quarter. On an absolute foundation, the Technique had positive factors throughout seven of the ten sectors during which it was invested (out of 11 sectors complete). The IT, client discretionary and industrials sectors have been the principle contributors, whereas the well being care and power sectors detracted.

On a relative foundation, general inventory choice and sector allocation weighed on efficiency. Particularly, inventory choice within the industrials, well being care, financials, supplies and communication companies sectors and an obese allocation to the power sector detracted. Conversely, inventory choice within the client discretionary and client staples sectors and an underweight allocation to the well being care sector proved helpful.

On a regional foundation, inventory choice in Europe Ex U.Okay., Asia Ex Japan, the U.Okay. and Japan and an obese to North America weighed on efficiency. Inventory choice in North America and an obese to rising markets positively contributed.

On a person inventory foundation, Samsung Electronics (OTCPK:SSNLF), Industria de Diseno Textil, Holcim (OTCPK:HCMLF), Schneider Electrical and Arcos Dorados have been the main contributors to absolute returns through the quarter. The biggest detractors have been Bayer, Julius Baer (JBPCF), Sanofi, Inpex (OTCPK:IPXHF) and Commonplace Chartered (OTCPK:SCBFF).

In the course of the quarter, along with the transactions talked about above, the Technique initiated a brand new place in Gerresheimer (OTCPK:GRRMF) within the well being care sector.

Sean Bogda, CFA, Managing Director, Portfolio Manager

Grace Su, Managing Director, Portfolio Manager

Jean Yu, CFA, PhD, Managing Director, Portfolio Manager

|

Previous efficiency isn’t any assure of future outcomes. Copyright © 2023 ClearBridge Investments. All opinions and knowledge included on this commentary are as of the publication date and are topic to alter. The opinions and views expressed herein are of the creator and should differ from different portfolio managers or the agency as a complete, and usually are not meant to be a forecast of future occasions, a assure of future outcomes or funding recommendation. This info shouldn’t be used as the only real foundation to make any funding choice. The statistics have been obtained from sources believed to be dependable, however the accuracy and completeness of this info can’t be assured. Neither ClearBridge Investments, LLC nor its info suppliers are answerable for any damages or losses arising from any use of this info. Efficiency supply: Inner. Benchmark supply: Morgan Stanley Capital Worldwide. Neither ClearBridge Investments, LLC nor its info suppliers are answerable for any damages or losses arising from any use of this info. Efficiency is preliminary and topic to alter. Neither MSCI nor some other social gathering concerned in or associated to compiling, computing or creating the MSCI knowledge makes any specific or implied warranties or representations with respect to such knowledge (or the outcomes to be obtained by the use thereof), and all such events hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or health for a selected function with respect to any of such knowledge. With out limiting any of the foregoing, in no occasion shall MSCI, any of its associates or any third social gathering concerned in or associated to compiling, computing or creating the info have any legal responsibility for any direct, oblique, particular, punitive, consequential or some other damages (together with misplaced income) even when notified of the potential for such damages. No additional distribution or dissemination of the MSCI knowledge is permitted with out MSCI’s specific written consent. Additional distribution is prohibited. |

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.