metamorworks

Funding Thesis

Right here I evaluate and distinction The Commerce Desk (NASDAQ:TTD) with AppLovin (NASDAQ:APP). I make the case that The Commerce Desk is overvalued for what it presents buyers, with its inventory priced at greater than 30x ahead free money flows. Sure, The Commerce Desk may be very steady and has a really sturdy steadiness sheet, with in all probability greater than $1.5 billion of money on no debt on the subject of reporting its This autumn ends in a couple of weeks.

Whereas AppLovin carries a good quantity of debt, at roughly $2 billion of internet debt, whereas its underlying progress charges are extra unpredictable. Naturally, because of this APP ought to carry a decrease a number of on its inventory.

And but, I contend that in 2024 APP might be a superior funding to TTD.

Speedy Recap,

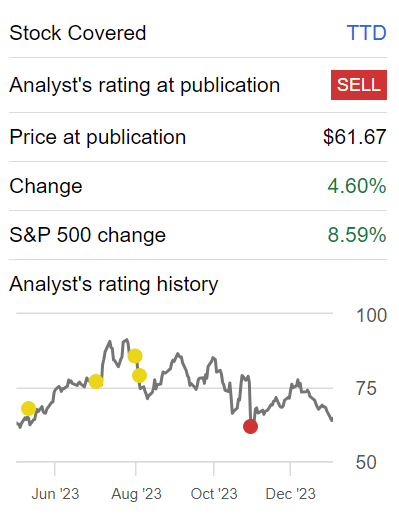

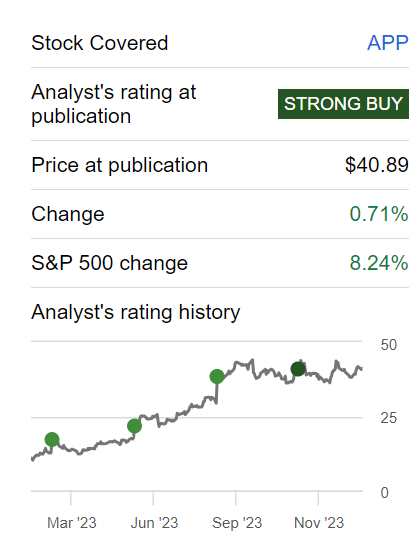

At the beginning of November, I took a bearish outlook on The Commerce Desk.

Writer’s work on TTD

As you possibly can see above, since I took a bearish view, the inventory has underperformed the S&P 500 (SPY).

In the meantime, at roughly the identical time, I took an excellent bullish view of AppLovin, and that inventory has carried out even worse than The Commerce Desk, though not by a lot.

Writer’s work on APP

What we see right here is that the inventory prior to now 3 months has additionally underperformed the S&P 500.

However, as we glance forward over the subsequent 12 months, I consider that APP will meaningfully outdistance itself from TTD. Here is why.

The Commerce Desk vs AppLovin

The Commerce Desk and AppLovin, each outstanding gamers within the digital promoting panorama, diverge of their core enterprise focuses and goal audiences.

The Commerce Desk positions itself as a number one impartial demand-side platform, providing advertisers a complete resolution for programmatic promoting throughout numerous channels resembling show, video, audio, cell, and native. With an emphasis on transparency and data-driven decision-making, The Commerce Desk caters to advertisers and businesses looking for versatile and impartial promoting options.

In distinction, AppLovin specializes within the cell app ecosystem, offering a mobile-centric platform for builders. AppLovin’s major clientele contains cell app builders and publishers, providing them instruments for consumer acquisition, engagement, and in-app promoting options. Whereas The Commerce Desk maintains independence and a broader trade focus, AppLovin’s specialization lies in empowering cell app builders throughout the dynamic cell app panorama.

With this context in thoughts, let’s now flip our dialogue to their respective outlooks.

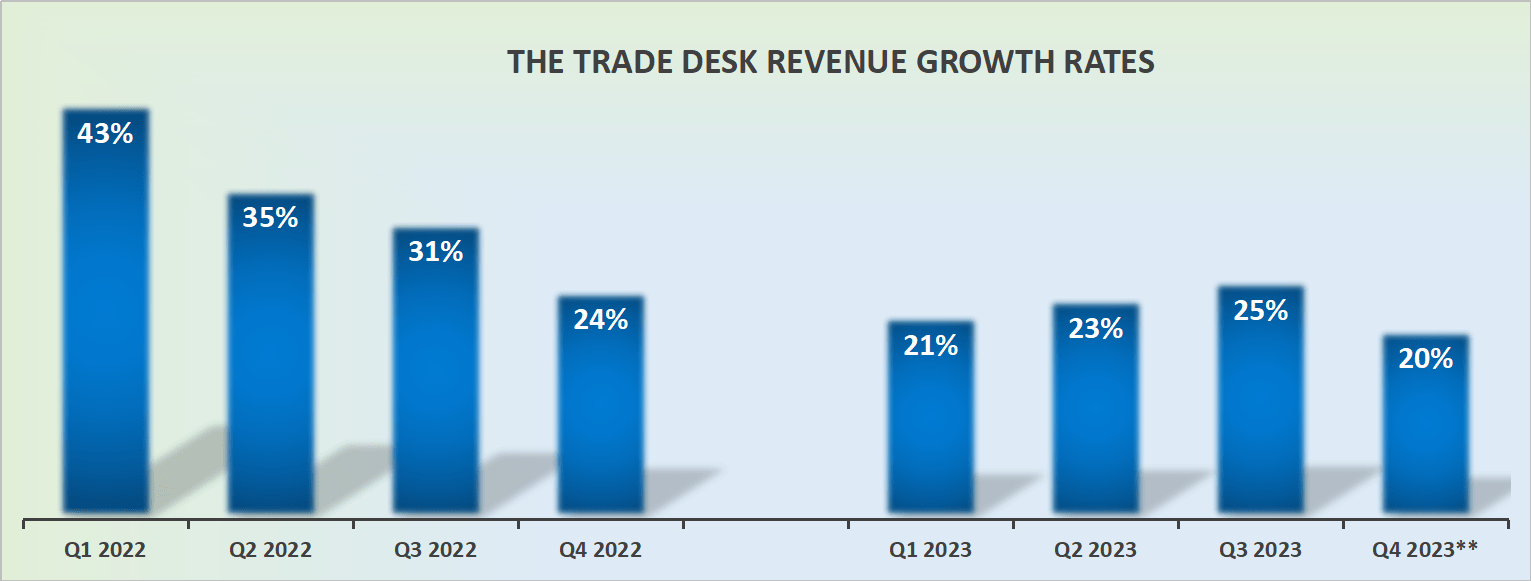

TTD’s Income Progress Charges Are Moderating

TTD income progress charges

Ben Graham re-quotes Horace by saying:

Many shall be restored that now are fallen and lots of shall fall that now are in honor.

The issue with investing is that we prefer to consider that there are companies that may all the time be in favor, these companies with superior administration. And I put The Commerce Desk on that record. And but, the very fact of the matter is that The Commerce Desk’s income progress charges are beginning to reasonable.

Not way back this enterprise could possibly be counted on for greater than 30% CAGR. At this time, its income progress charges are prone to stabilize round 20% CAGR. And this has dramatic implications on the a number of that buyers are keen to pay for the inventory.

Working example, I’ve said on quite a few events that when investing, it isn’t ok to be a contrarian for a contrarian’s sake. In the end, one must be a contrarian that’s confirmed appropriate.

SA Premium

Certainly, on the subject of investing, it is a recreation of chances. Getting as many elements as potential on our facet of the equation, so that there is a greater than 50% probability that our funding works out efficiently.

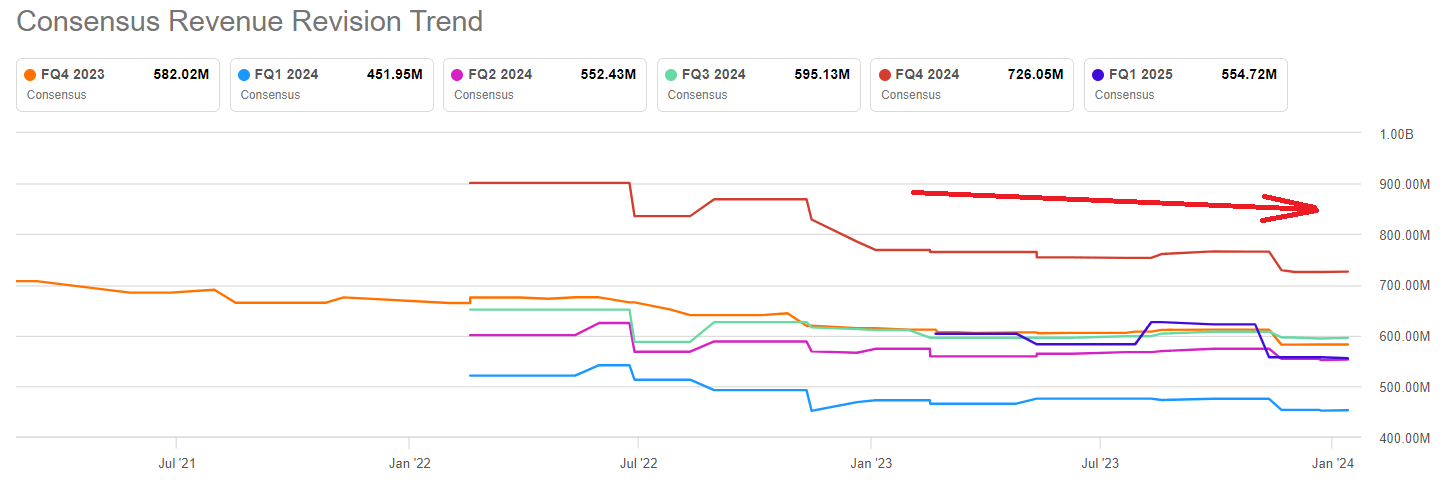

And for that, I’ve typically informed my readers that when investing, search to place capital to work in shares the place the Avenue has a good outlook in your inventory and the Avenue is on the market upwards revising their consensus income figures.

At the same time as I admit that no funding technique is ideal. In spite of everything, this can be a recreation of chances. And but, what you see within the graphic above is opposite to this line of reasoning. What we see is that with time, analysts are slowly downwards revising their income estimates for The Commerce Desk.

Does this imply that the analyst group is true? No, it completely doesn’t. Nevertheless it does imply that The Commerce Desk is now a ”present me” inventory. And present me shares wrestle to commerce at a premium valuation.

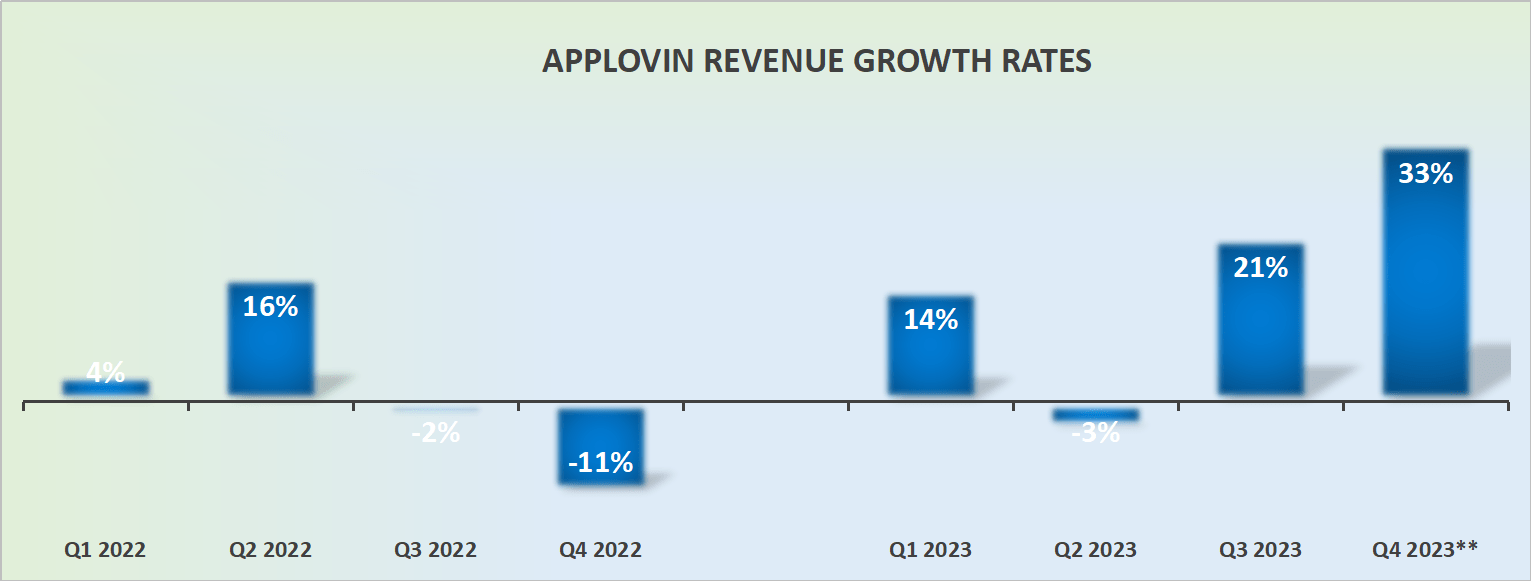

Subsequent, see beneath AppLovin’s progress charges.

APP income progress charges

What we see above is that AppLovin’s progress charges are dramatically extra erratic. This can naturally affect the a number of that buyers might be keen to pay for its inventory.

What buyers crave, above all else, is certainty. And AppLovin hasn’t traditionally been in a position to present buyers with this. Whereas The Commerce Desk has supplied buyers with peace of thoughts, and that is why it is inventory has all the time been priced at a premium valuation.

However I now consider that the pendulum has swung too far in each cases. And that is what we’ll focus on subsequent.

TTD vs APP Inventory Valuation — One is Priced at 9x Free Money Circulate

Let’s evaluate The Commerce Desk with AppLovin. For transparency, I am lengthy APP. However I consider that I am going to however be honest in my comparability.

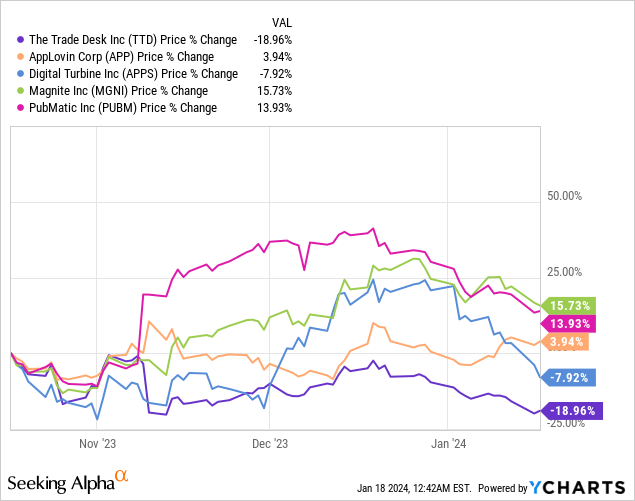

As you possibly can see above, prior to now 3 months, APP has not been the very best performer. Sure, there is a optimistic return for APP, however it’s removed from the group chief. I hope this perception solely goes to show my argument that I am not reverse engineering my trades to drive ahead my argument.

Nonetheless, what we will see is that The Commerce Desk has been the group’s worst performer. And I do know that it is simple to say that because it’s underperformed, it should be undervalued. However once more, I consider this can be a fallacious argument.

I consider that The Commerce Desk will make $1 billion of EBITDA in 2024. For this determine, I’ve assumed that The Commerce Desk’s EBITDA will develop by roughly 25% y/y in contrast with 2023.

Realistically, I do not consider that The Commerce Desk will the truth is ship $1 billion of EBITDA, because it’s troublesome for The Commerce Desk’s underlying profitability to far outpace the expansion in its topline. However for the sake of our dialogue, I’ve be keen to make use of this determine.

This leaves The Commerce Desk at 31x ahead EBITDA. By the way, I consider that The Commerce Desk’s capex might be larger than $100 million in 2024, however let’s assume that The Commerce Desk has no capex wanted in 2024, to depart room for error in my calculations.

Let’s now draw a comparability with AppLovin. I anticipate that AppLovin will generate roughly $1.4 billion in EBITDA for the 12 months 2023. To account for uncertainties, I’ve launched a margin of security into my projections, envisioning that AppLovin’s EBITDA for 2024 could be roughly $1.6 billion.

Whereas the expectation that AppLovin’s free money movement would improve by solely 14% from $1.4 billion in 2023 to $1.6 billion in 2024 may appear conservative, let’s proceed with this estimate. Taking capital expenditures into consideration, this projection interprets to an estimated $1.5 billion in free money movement for the 12 months 2024, positioning APP at a valuation of 9 occasions its free money movement.

It is vital to notice that AppLovin carries a internet debt of $2.8 billion, which is able to impede vital acquisitions in 2024. Nonetheless, assuming AppLovin sustains its strong efficiency and successfully integrates the acquisitions made in 2023, it’s believable that by this time subsequent 12 months, its internet debt might lower to beneath $2 billion. This discount in debt would probably pave the best way for AppLovin to renew extra substantial acquisitions.

The Backside Line

In conclusion, as I assess The Commerce Desk towards AppLovin by way of funding potential, it turns into evident that TTD is presently overvalued, buying and selling at over 30 occasions ahead free money flows, regardless of its stability and strong steadiness sheet.

Notably, TTD’s income progress charges are decelerating, main analysts to revise their estimates downward, positioning it as a “show me” inventory struggling for a premium valuation.

Conversely, AppLovin, regardless of shouldering a good quantity of debt, reveals extra unpredictable progress charges. The evaluation factors to APP, priced at simply 9 occasions its free money movement, as a superior funding to TTD in 2024, underscoring the significance of valuations and progress charges in evaluating these digital promoting entities.