domnicky/iStock by way of Getty Pictures

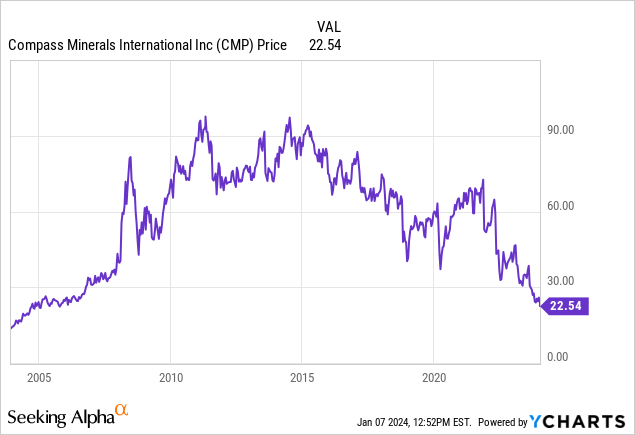

Compass Minerals Worldwide (NYSE:CMP) caught my eye nonetheless buying and selling close to 52-week lows at $22.54 however the firm has some rocky challenges forward. Money flows and curiosity protection point out tight liquidity resulting in fairness issuances within the previous yr. The corporate has halted additional improvement on their brine lithium challenge, which is a optimistic for my part because the challenge has loads of regulatory uncertainties and a protracted lead time. The halt will drive Compass Minerals to give attention to their roots in salt manufacturing till the lithium trade and rules grow to be extra clear. This text will talk about Compass Minerals’ newest outcomes and respectable salt money flows in addition to the expansion initiatives in Lithium manufacturing and forest fireplace prevention merchandise.

So much has modified since I last wrote about Compass Minerals again in September 2017 questioning the sustainability of the dividend, however a few of the core salt enterprise has stayed the identical too. Since this final article, the inventory has achieved whole returns of detrimental 55.9% in comparison with optimistic 87% returns from the S&P 500. Over the interval since my final article, Compass Minerals has bought off the South American plant diet enterprise and invested closely in new development initiatives. The low ROIC makes me apprehensive that the corporate could possibly be a worth lure even at at the moment’s low costs with the excessive debt load.

Newest Quarterly Outcomes

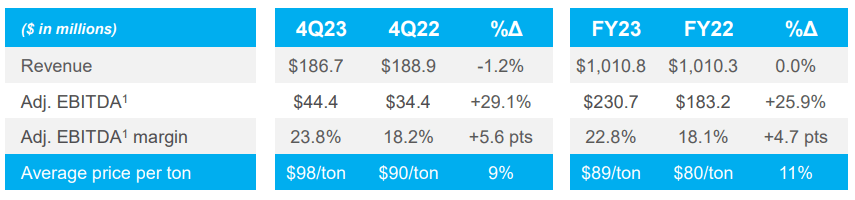

Within the latest fiscal year results, the corporate restored full-year adjusted EBITDA margins in extra of $20 per ton for the Salt enterprise. Fiscal yr income might have been flat for the Salt section, however EBITDA was a strong $230.7 million (+25.9%) pushed partly by pricing being up 11% per ton to $89.

Income and EBITDA Highlights (from firm This fall & FY earnings launch)

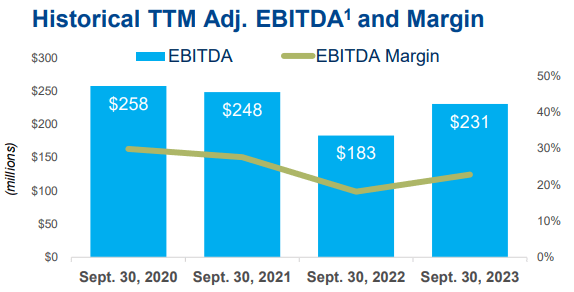

Offsetting the pricing features had been salt quantity declines of 9.8% to 11,320 thousand of tons from 12,556 in 2022 throughout Freeway Deicing and Client & Industrial. These Salt section figures proceed to recuperate again in the direction of current highs of $258 million EBITDA again in FY 2021 and proceed to make up 84% ($231 million) of Compass Minerals EBITDA with Plant Vitamin contributing the opposite vital quantity with 16% ($45.1 million).

Salt Historic EBITDA & Margins (from firm This fall earnings launch)

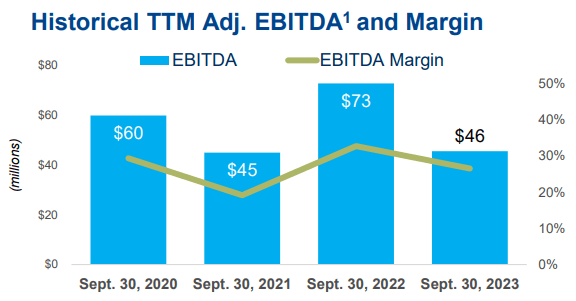

Then again, the Plant Vitamin section had income declines of twenty-two.6% to sit down at $172 million for FY 2023. Volumes within the section declined 23.4% to 219,000 tons from 286,000 tons in 2022. EBITDA of $45 million for the fiscal yr was down 37.4% with EBITDA margins down 6.3%.

Plant Vitamin Historic TTM EBITDA & Margins (from firm This fall earnings launch)

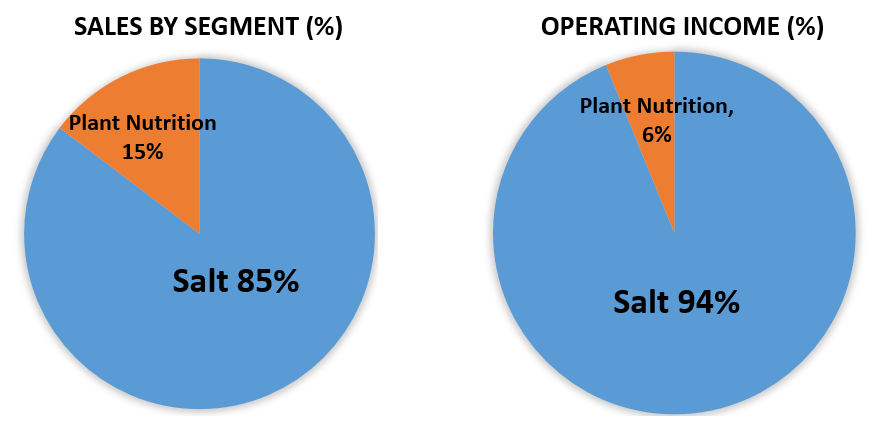

Compass Mineral’s core Salt enterprise stays the money cow of the corporate contributing to 85% ($1.0 billion) of revenues and an much more necessary 94% ($171.1 million) of working revenue in comparison with Plant Vitamin. This working revenue goes a protracted solution to protecting the $55 million of curiosity funds within the TTM interval.

Sadly, throughout the entire firm, internet working revenue for the TTM interval was $79.1 million signifying that different capital sources are being spent on much less productive initiatives. For the most recent FY 2023, SG&A bills had been $154.8 million (+0.6%) however for the This fall interval they elevated 24.1% YoY to $40.2 million.

Section Gross sales & Working Earnings (compiled by creator from firm financials)

The corporate’s development initiative of the brand new fireplace retardant enterprise, Fortress, contributed round $12 million to adjusted EBITDA, however as talked about within the earnings launch, that will not get booked to earnings till the contract is finished in FY 2024. In Might 2023, the corporate signed an settlement for the 2023 fireplace season with the U.S. Forest Service (USFS) to offer services at as much as 5 cell retardant bases. This enterprise achieved its first business gross sales in June 2023 with the primary business drops of product in Arizona. In Might, the corporate closed on buying the remaining 55% of Fortress not already owned. The ultimate settlement with the USFS just isn’t anticipated to be finalized till late December 2023 or early January 2024. I shall be holding an eye fixed out for the outcomes of this contract and the way significant the expansion shall be from this new enterprise.

The lithium development initiative is the place the difficulty begins. Given the unsure regulatory atmosphere in Utah surrounding the extraction of Lithium from the Nice Salt Lake, Compass Minerals suspended indefinitely additional funding into the challenge. The corporate’s administration said they’re dedicated to avoiding using frequent fairness on the enterprise stage and are in search of a associate to de-risk the challenge by means of the regulatory wait occasions. Compass Minerals already extracts a number of minerals by means of brine evaporation strategies and lithium would solely be one other useful resource they might be extracting within the present course of.

The halt of spending will take time as some elements of the challenge have providers set to be delivered already in 2024. The lithium challenge will add one other $25 – $30 million of capital wants along with $90 – 100 million of sustaining capital expenditures for the salt and plant diet enterprise. Administration laid these expectations out clearly within the This fall earnings launch.

Whole capital expenditures for the corporate in fiscal 2024 are anticipated to be inside a variety of $125 million to $140 million. This contains between $90 million and $100 million in sustaining capital expenditures associated to the core Salt and Plant Vitamin companies. As well as, $25 million to $30 million of lithium-associated capital, principally associated to “in flight” objects ordered previous to the just lately introduced challenge suspension and scheduled to be delivered and put in in 2024, is anticipated to be deployed in 2024

– Fiscal This fall and FY 2023 Outcomes

The corporate’s core belongings stay sturdy as this text will talk about, however whether or not they can generate the long-term returns wanted for buyers at at the moment’s valuation is one other query. With Salt doing the heavy lifting in Compass Minerals’ EBITDA let us take a look at the remaining lifespan of the corporate’s most necessary belongings; the principle three salt mines in Goderich, Winsford, and Cote Blanche which make up 85% of Compass Minerals’ salt manufacturing capability as of September 30, 2022.

The weighted common amortization interval for the possible mineral reserves is 86 years for the leased portion as of September 30, 2022, and 35 years for the owned portion. Trying individually on the 2020 yr mine life knowledge when the corporate final gave the beneath desk, with the manufacturing run price assumption of 6.5 million metric tons, the Goderich mine (largest underground rock salt mine on the planet) has a present mine life of roughly 81 years. On the smaller aspect of reserves, the Winsford mine (the most important devoted rock salt mine within the U.Ok. with a 177 yr historical past) solely has a present mine life of roughly 26 years, and Cote Blanche has a lifespan of round 99 years.

Remaining Mine Life as of Sep 2020 (2020 Annual Report)

A Worthwhile Core Enterprise

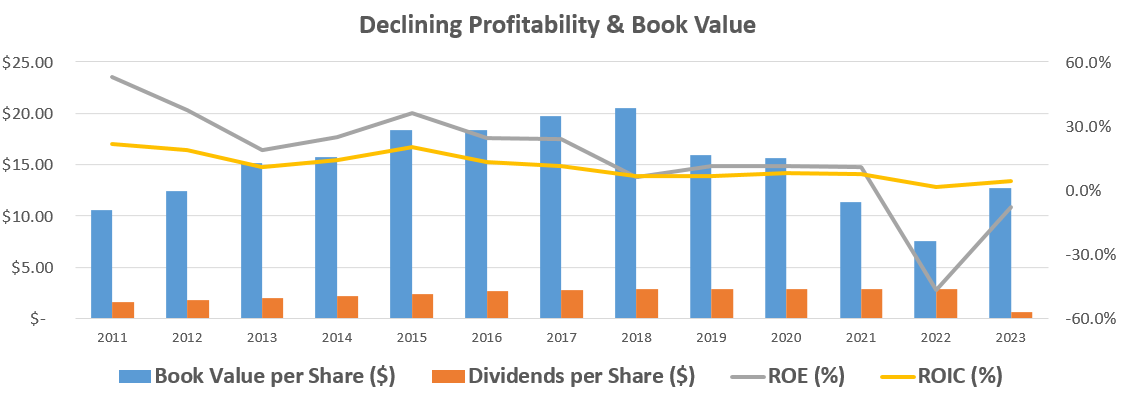

Compass Mineral’s core salt belongings have allowed the corporate to realize a mean return on fairness and return on invested capital of 14.8% and 10.5%, respectively, since 2008. This common stage of profitability is nicely round my rule of thumb in search of 15% ROE and 9% ROIC, however has considerably declined lately because the divestiture of the South American Plant Vitamin enterprise in 2021. ROIC within the newest TTM interval was round solely 2.5% with the 2022 and 2021 years exhibiting declines from way more acceptable highs of seven.4% within the 2020. The massive ROE decline in 2021 is as a result of $300 million impairment cost in 2021 which isn’t picked up within the nonetheless optimistic ROIC determine of 1.26% for that yr.

Profitability and E book Worth Declines (compiled by creator from firm financials)

The corporate misplaced vital top-line revenues after the 2021 divestiture of the South American plant diet enterprise. SG&A bills haven’t been reduce to the identical extent and have chipped away 1.7% in working margins since. That is vital for a low-margin commodity enterprise with working margins of 6.6% within the newest yr.

The corporate’s low profitability lately makes me surprise if Compass Minerals will be capable of preserve its intrinsic worth over a enterprise cycle. The current impairments spotlight that query. The lengthy lifetime of the salt mine belongings ought to enable some base within the Compass Minerals’ operations. We could also be seeing the energy of this base now with the corporate spending money flows from salt operations at a hefty price on development initiatives in lithium and the Fortress fireplace retardant enterprise acquisition.

Money Flows Going to Funding Spending

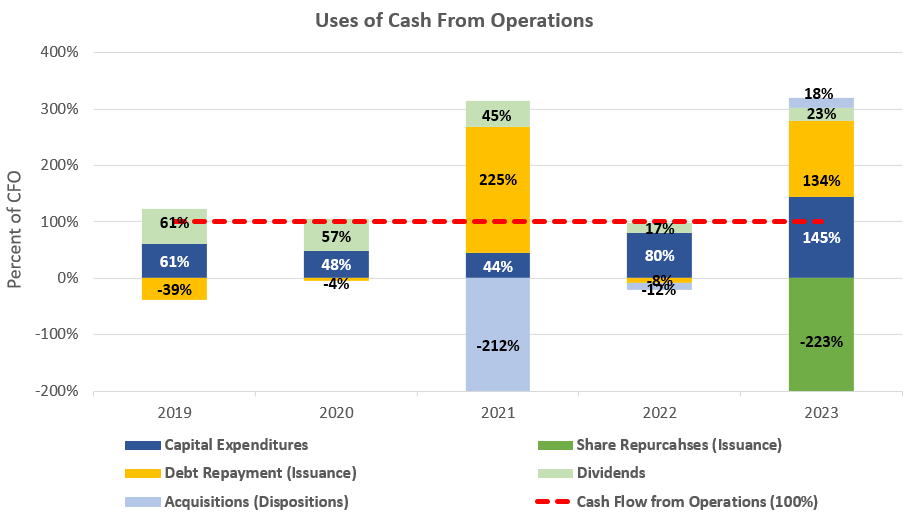

Compass Minerals has respectable money flows however the heavy spending has led to dividend cuts lately and fairness issuances. For fiscal 2023, internet money utilized in investing actions was $173.0 million in comparison with $80.0 million in fiscal 2022. This contains the 2022 receipt of an extra $61.2 million in proceeds from the sale of the corporate’s South American chemical substances enterprise. Compass Minerals stays lively on the portfolio administration aspect since promoting the South American Plant Vitamin enterprise.

With common money flows from operations of $114.2 million prior to now 2 years, Compass Minerals’ spending on capex has been vital with $156.2 million (145% of CFO) spent within the newest 2023 fiscal yr and $96.7 million (80% of CFO) in 2022. The common spending over the previous 5 years has approximated 76% which might suggest a low 3.0% free money move yield on the present $929 million market capitalization of Compass Minerals.

Historic Money Circulation Evaluation (compiled by creator from firm financials)

Earlier knowledge from the 2019 – 2021 years earlier than the spending spree started present decrease capex averaging 51% of CFO. On this state of affairs, the FCF yield could be round a extra cheap 6.0%. Nonetheless, I don’t see this slowdown in spending coming anytime quickly given administration’s steering, so free money flows from Compass Minerals usually are not that spectacular at at the moment’s valuation.

Valuation Appears Costly

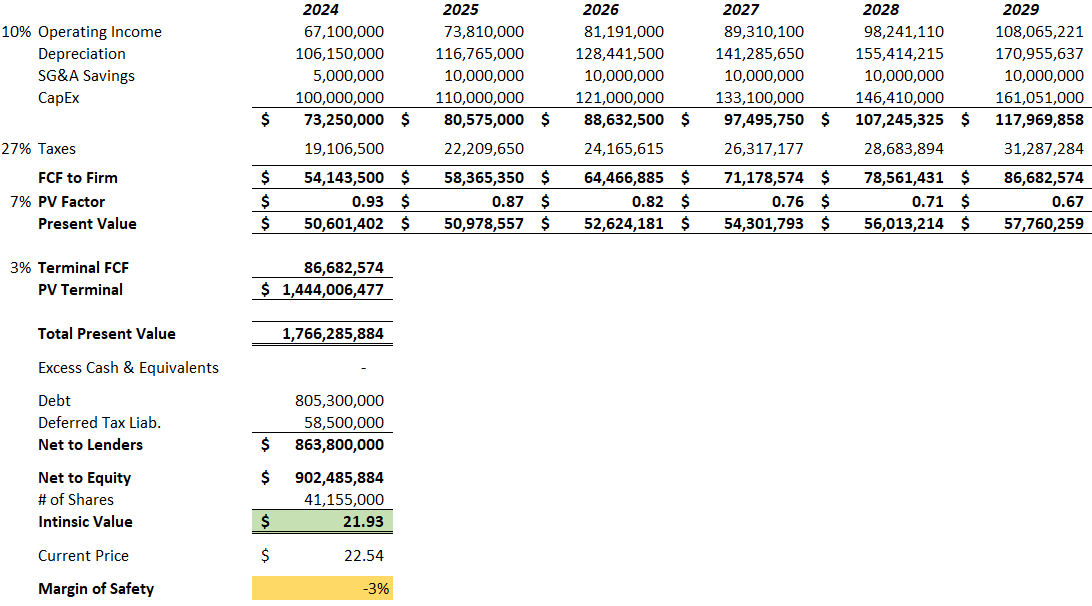

Operating the newly modified Compass Minerals by means of a reduced money move reveals a low-returning enterprise that struggles to justify even a weighted common price of capital of seven%. So as to get the valuation considerably cheap, I needed to aggressively construct in SG&A expense cuts of $10 million inside a few years, give a ten% development over the 5-year forecast interval (terminal development of three%), and likewise decrease capex spending in the direction of the sustainable $90 – $100 million forecast by administration within the newest launch. The beginning 2024 working revenue is conservatively primarily based on the common of the previous two years’ working revenue ($42.9 and $79.1 million) multiplied by the ten% development price. There are loads of favorable changes to solely give an intrinsic worth of round $21.93 per share on the 7% WACC as will be seen beneath.

DCF Valuation Evaluation (estimated by creator from firm financials)

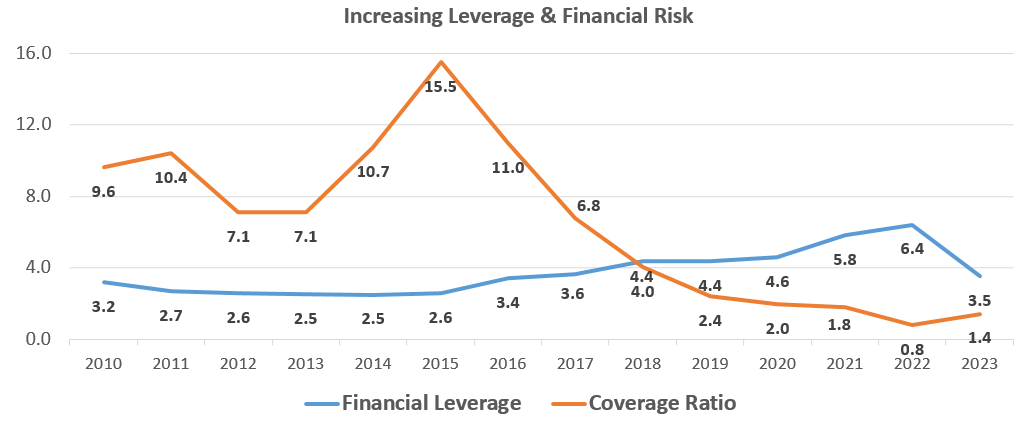

Curiosity Protection Trying Slim

The low-returning current ventures have added to debt capital necessities prior to now couple of years. Curiosity protection stays at a low 1.4x within the TTM interval with working revenue of $79.1 million and curiosity bills of $55.5 million. Monetary leverage is now again down to three.5x after hitting new highs of 6.4x in 2022. The discount in leverage is because of fairness rising to $517 million as of the most recent This fall September thirtieth year-end pushed by the $240.7 million fairness elevate.

Monetary Leverage and Curiosity Protection (compiled by creator from firm financials)

The corporate strengthened its monetary place by issuing $240 million of capital final yr together with a $75 million enlargement of the revolver to $375 million and a $200 million Time period Mortgage A issuance. Compass Minerals ended the fiscal yr with $317.0 million of liquidity, comprised of $38.7 million in money and equivalents and $278.3 million out there on the $375 million credit score facility. That is ample liquidity with the brand new share issuance but it surely must be correctly spent to get the ROIC again as much as acceptable 9% ranges.

Within the close to time period, I wish to see Compass Minerals pivot and tighten up their spendthrift methods on the SG&A aspect and give attention to milking the money flows of the salt enterprise. The halt in spending on Lithium initiatives ought to assist drive administration’s hand in slowing issues down and returning more money to capital suppliers.

Takeaway for Traders

Compass Minerals has nice money flows from their core salt enterprise however that section alone can’t help the valuation with all of the current challenge expansions. A free money move evaluation reveals low anticipated yields round 3.0% with spending nonetheless trailing off with $20-30 million of scheduled lithium expenditures anticipated. Extra sustainable capex spending from pre-2021 years might point out a 6.0% FCF yield.

On the lookout for a JV associate within the lithium enterprise looks like a clever thought and may assist sluggish the current spending. The fireplace retardant enterprise seems synergistic and promising, so I stay up for seeing what contract development comes out of subsequent season. Compass Minerals core salt enterprise stays in tact with good liquidity however it might probably’t help the valuation, even at the moment. I wish to see development initiatives hit the revenue assertion and if not quickly, SG&A prices ought to mirror a smaller enterprise within the close to time period.