BlackJack3D

The Cooper Firms (NASDAQ:COO) has been fairly profitable of their core contact lens trade, experiencing high-single-digit progress. The corporate has been increasing into the ladies’s well being enterprise, with the CooperSurgical enterprise combine growing from 17% a decade in the past to 32% of complete income immediately. I consider their strategic enterprise growth is sensible, and they’re on the appropriate path for margin growth. I’m initiating a ‘Purchase’ suggestion with a good worth of $415.

Contact Lens: Secure Progress in a Concentrated Market

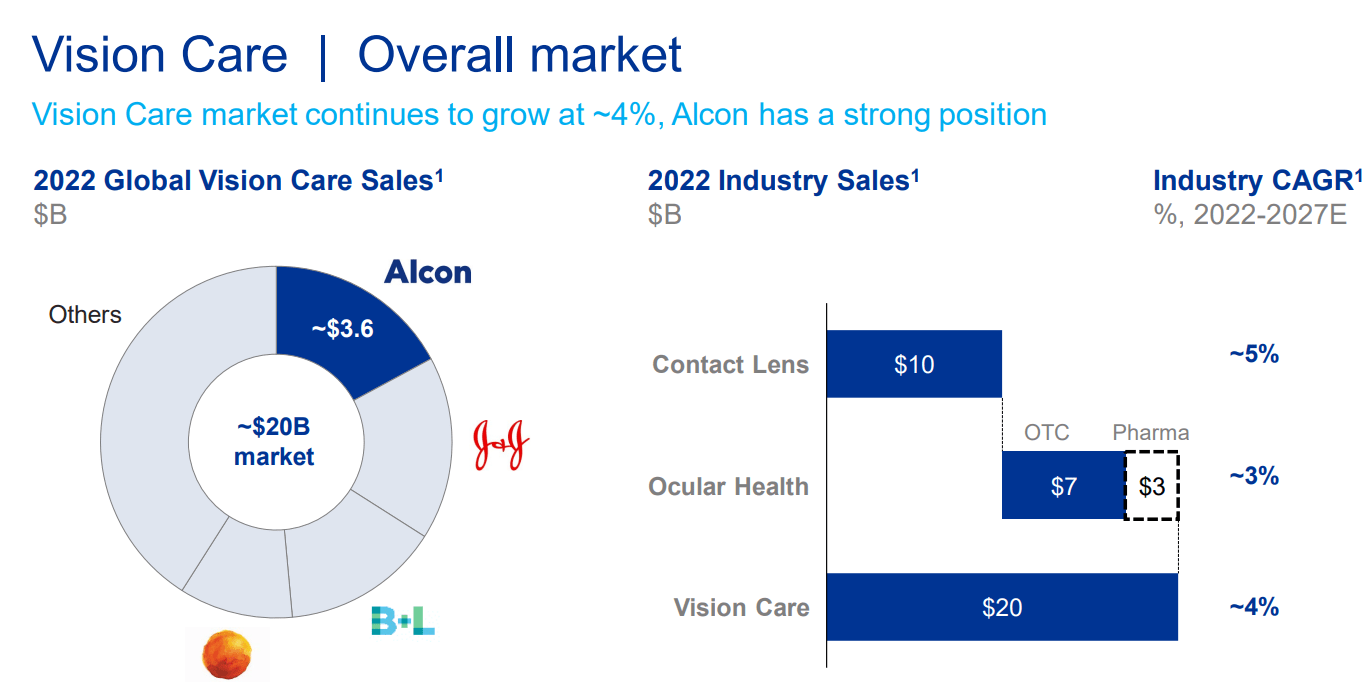

Within the imaginative and prescient care markets, the trade is extremely concentrated, with solely 4 main gamers worldwide, as illustrated within the chart beneath. Within the particular context of the contact lens market, which constitutes a complete addressable market of roughly $10 billion, Cooper holds a big place, accounting for round 23% of the entire market share.

Alcon Investor Presentation

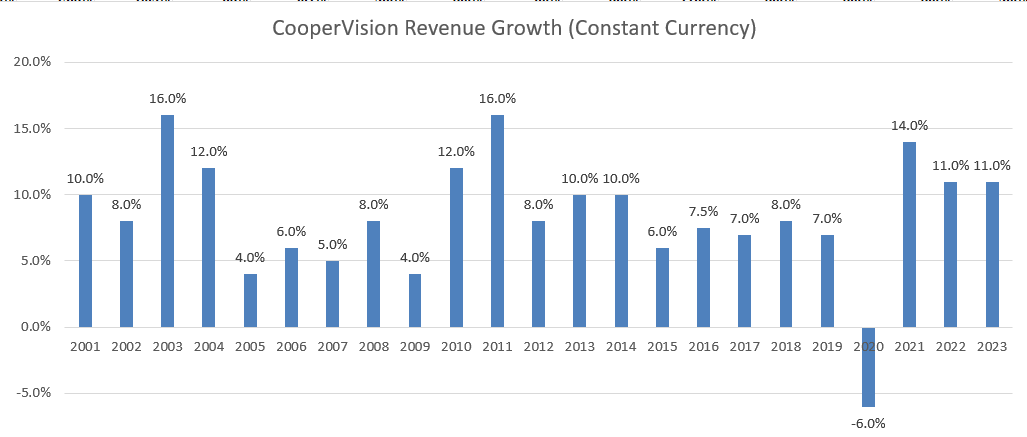

CooperVision has loved sturdy income progress over the previous twenty years, averaging an annual progress charge of greater than 8%, considerably outpacing the trade’s 5% progress charge. A number of elements contribute to their success within the imaginative and prescient market.

The complete contact lens market is present process a shift from non-dailies to day by day disposable merchandise. Each day merchandise supply varied advantages for patrons, together with comfort, fewer considerations about lens care, enhanced consolation, and elevated security. Research and Market tasks that the disposable contact lens markets to develop a CAGR of 9.27% throughout 2022-2027 interval. Cooper’s MyDay day by day disposable product has been extremely profitable in capturing a big share of this quickly rising market.

Moreover, toric and multifocal lenses operate like annuities. As soon as an optometrist prescribes toric or multifocal merchandise to a affected person, they’re inclined to stay with the identical model sooner or later. For producers like Cooper, this represents a constant and recurring income stream.

CooperVision has delivered sturdy progress over the previous twenty years, as illustrated within the chart beneath, and the expansion within the imaginative and prescient division has contributed to their success within the imaginative and prescient care trade.

Cooper 10Ks

Increasing right into a Girls Well being Enterprise

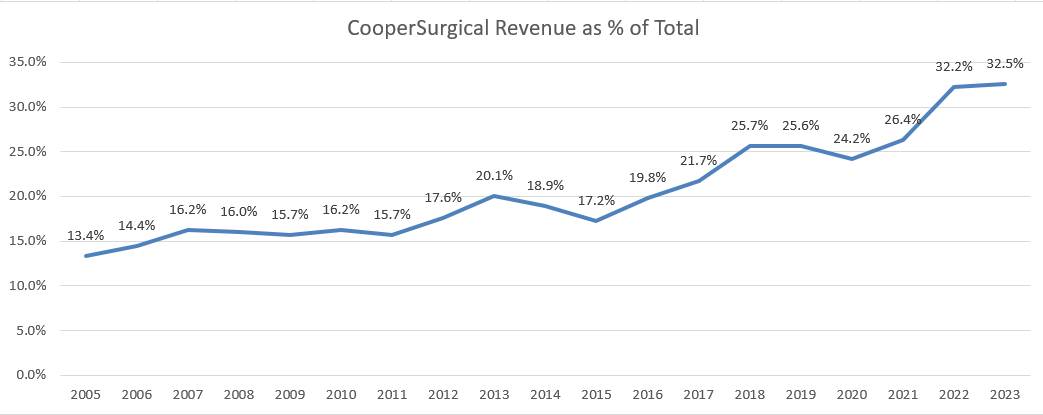

Cooper has deployed vital capital in the direction of acquisitions to bolster its surgical enterprise, providing a variety of medical units, together with these in fertility, genomics, diagnostics, cryostorage, and contraception. CooperSurgical’s contribution to complete income has grown from 13.4% in FY05 to 32.5% in FY23.

Cooper 10Ks

It makes strategic sense for Cooper to broaden its surgical enterprise.

Firstly, based on Alcon’s (ALC) capital market day presentation, all the contact lens market is barely $10 billion in complete, presenting a restricted progress alternative for Cooper. To attain substantial progress, they have to diversify into markets the place they possess experience.

Secondly, the ladies’s well being trade is a distinct segment market with fewer international gamers, making it comparatively simpler for Cooper to scale.

Lastly, the worldwide pattern of delayed childbirth creates a structural progress driver for the ladies’s well being market. In line with the BMC report, the proportion of ladies who delay childbearing till or past 30 years has dramatically elevated within the final three a long time. The pattern has generated an enormous potential marketplace for fertility, genomics, diagnostics, cryostorage, contraception, and many others.

In brief, Cooper’s growth into girls’s well being may add one other progress leg for the corporate and broaden their complete addressable market dimension.

Historic M&A Created Margin Stress

Cooper is actively pursuing bolt-on acquisitions to broaden their girls’s well being enterprise. For instance, in 2022, they acquired Prepare dinner Medical’s Reproductive Health business, a producer of minimally invasive medical units targeted on the fertility, obstetrics, and gynecology markets, for $875.0 million. In 2021, they acquired Generate Life Sciences, a privately held main supplier of donor egg and sperm for fertility therapies, for $1.663 billion.

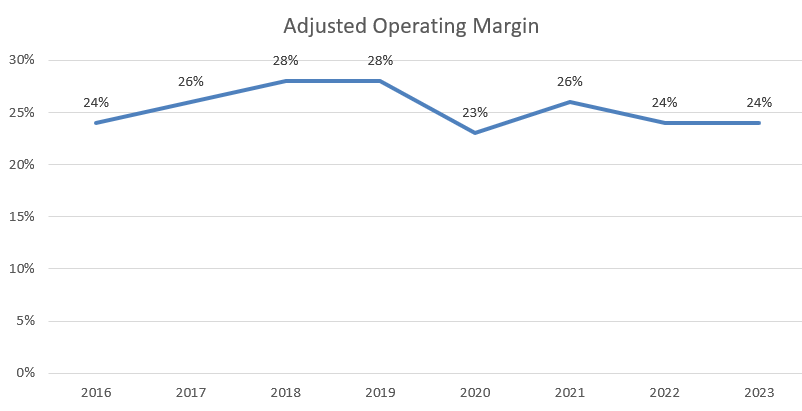

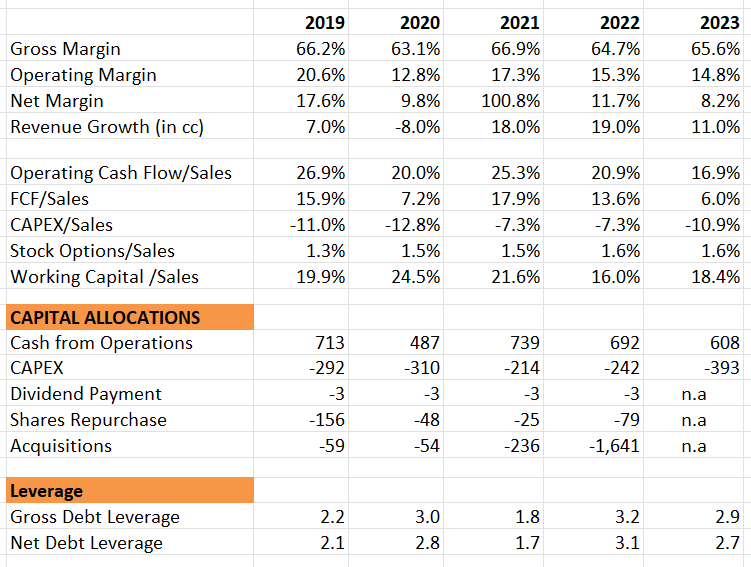

These acquisitions helped them scale up their girls’s well being enterprise phase; nevertheless, these strategic acquisitions have impacted their near-term margins. The adjusted working margin declined from 28% in FY19 to 24% in FY23, contributing to a lower of their inventory value lately.

I consider their weak inventory value previously few years was brought on by the dearth of margin growth; nevertheless, I consider their margin will begin to enhance within the coming years. When CooperSurgical grows to a sure dimension, there will likely be a tipping level when the working leverage exceeds the margin influence from acquisitions. At that time, the group-level margin ought to begin to profit from the working leverage pushed by high-single-digit topline progress and mid-single-digit working expense progress. Of their FY24 steerage, the adjusted EPS progress is forecasted to develop by 7.7%, even contemplating the damaging influence from the contact lens scarcity. As such, I feel they’re heading in the right direction for margin growth.

Cooper 10Ks

Monetary Evaluation and FY24 Outlook

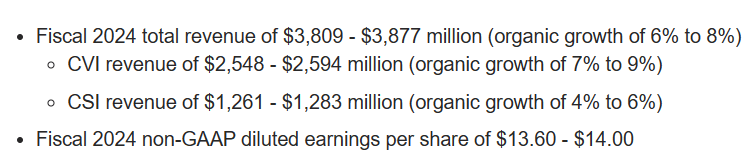

Throughout Q4 FY23, Cooper achieved spectacular outcomes, with a ten% progress in natural income and a outstanding 26% enhance in adjusted EPS. Notably, their imaginative and prescient enterprise skilled an 11% natural progress, whereas the surgical enterprise noticed a 7% year-over-year enhance. For FY24, they anticipate natural income progress within the vary of 6-8%, and I consider they’re positioned to ship on the excessive finish of this steerage, aligning with their historic progress pattern.

Cooper This fall FY23 Incomes Launch

Throughout the This fall FY23 earnings name, the administration highlighted that the robust quarter’s progress was fueled by sturdy demand for day by day silicone hydrogel contact lenses within the Imaginative and prescient division and the fertility enterprise in CooperSurgical. Gross sales of Cooper’s MyDay day by day disposable product are experiencing vital demand, resulting in an growth of producing capabilities to fulfill this growing market want. Consequently, their capital expenditure rose from $242 million in FY22 to $393 million in FY23.

Throughout the earnings name, it was highlighted that CooperVision’s enterprise progress is at the moment constrained by manufacturing capacities, significantly in Q1 FY24. Consequently, they anticipate a 7% progress for his or her imaginative and prescient enterprise within the first quarter. Nevertheless, with the ramp-up of recent manufacturing traces, they anticipate natural income progress for the imaginative and prescient enterprise to speed up all through FY24. Moreover, they undertaking a 2%-3% value enhance for his or her imaginative and prescient enterprise, in step with the conventional value enhance sample noticed previously.

On the margin facet, their adjusted EPS solely grew 3.1% yr over yr in FY23, and they’re guiding for a 7.7% of EPS progress in FY24 on the mid-point. Many questions relating to margin growth have been raised through the earnings name. The administration indicated that contact lens capability constraints have had a damaging influence on their margin steerage.

Cooper is ready to announce its Q1 FY24 earnings on February twenty ninth after the market closes, and I consider they’re extra prone to uphold their full-year steerage for a number of causes. Their present full-year steerage has already taken under consideration the influence of contact lens manufacturing constraints, with a lot of the impact anticipated to be mirrored within the Q1 FY24 outcomes. Moreover, the corporate is within the strategy of scaling up its new manufacturing traces, and the expansion charge is anticipated to speed up from Q2 FY24 onwards. Moreover, they need to be positioned to attain some margin growth by the combination of their historic acquisitions, pricing will increase, and working leverage. In abstract, I discover their full-year steerage to be fairly achievable.

The desk beneath outlines their monetary efficiency over the previous 5 years, revealing the damaging influence of previous acquisitions on their working margins. The free money circulation margin exhibits fluctuations, primarily because of the growth of disposable contact lens manufacturing services. Moreover, previous acquisitions have launched variability of their free money circulation margins. Nearly all money from operations has been directed in the direction of capital expenditure and acquisitions, strategically build up their girls’s well being enterprise.

Cooper 10Ks

Their stability sheet is fairly sound, with gross debt leverage beneath 3x. In abstract, over the previous 5 years, their profitability and free money circulation progress have been comparatively weak, regardless of strong topline progress.

Valuations

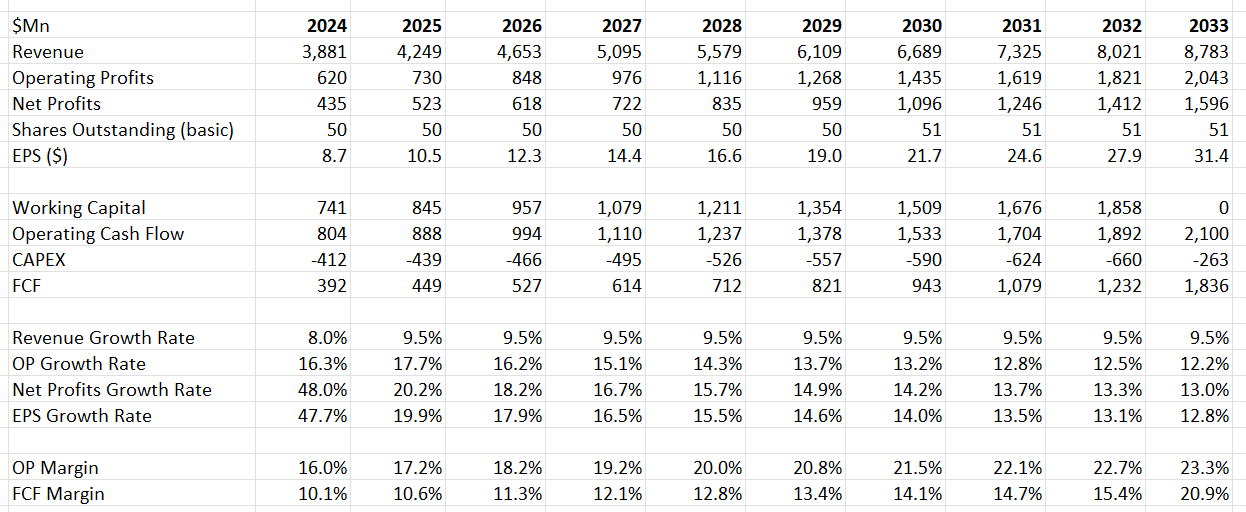

I anticipate they will obtain 8% natural income progress in FY24, in step with their steerage, implying some gross sales progress influence from a contact lens provide subject. The mannequin is assuming 9.5% normalized gross sales progress within the coming years, aligning with their historic pattern. Concerning margins, I anticipate growth over time as they capitalize on working leverage and synergies from previous acquisitions.

Cooper DCF – Creator’s Calculation

The mannequin makes use of a ten% low cost charge, 5% terminal progress, and a 15% tax charge. I apply the identical WACC to all of my DCF valuations, and I consider Cooper ought to be capable to develop sooner than the general GDP progress when the corporate reaches the maturity of its enterprise cycle. Due to this fact, a 5% terminal progress is assumed right here. In line with my calculations, the truthful worth is estimated to be $415 per share.

Key Dangers

Capital Intensive Enterprise: The contact lens enterprise is inherently capital-intensive, requiring substantial investments in huge manufacturing traces, significantly for high-volume merchandise like day by day disposables. Cooper has constantly allotted over 10% of their complete gross sales to capital expenditure. I consider that as they broaden additional into the surgical enterprise, the capital expenditure ratio is prone to decline over time.

Personal Label Contact Lens: There are quite a few non-public label contact lens merchandise out there, with notable examples akin to Costco (COST) providing their very own non-public label contact lens. Moreover, on-line gamers like 1800contacts promote reasonably priced contact lens merchandise over the web. Whereas these non-public label choices could cater to clients looking for budget-friendly options, I consider that within the mid-end and high-end markets, these rivals could battle to compete in opposition to international producers like Cooper. The latter possesses robust model recognition, sturdy analysis and growth capabilities, and large-scale manufacturing capabilities that present a aggressive edge.

Conclusion

I like Cooper’s high-single-digit progress of their core contact lens market, and their growth into the ladies’s well being enterprise is sensible. I’m initiating a ‘Purchase’ suggestion with a good worth of $415.