Aajan

It has been some time since I final visited COPT Protection Properties (NYSE:CDP) with a ‘Purchase’ ranking here again in October, highlighting its defensive property profile, discounted valuation, and long-term progress potential.

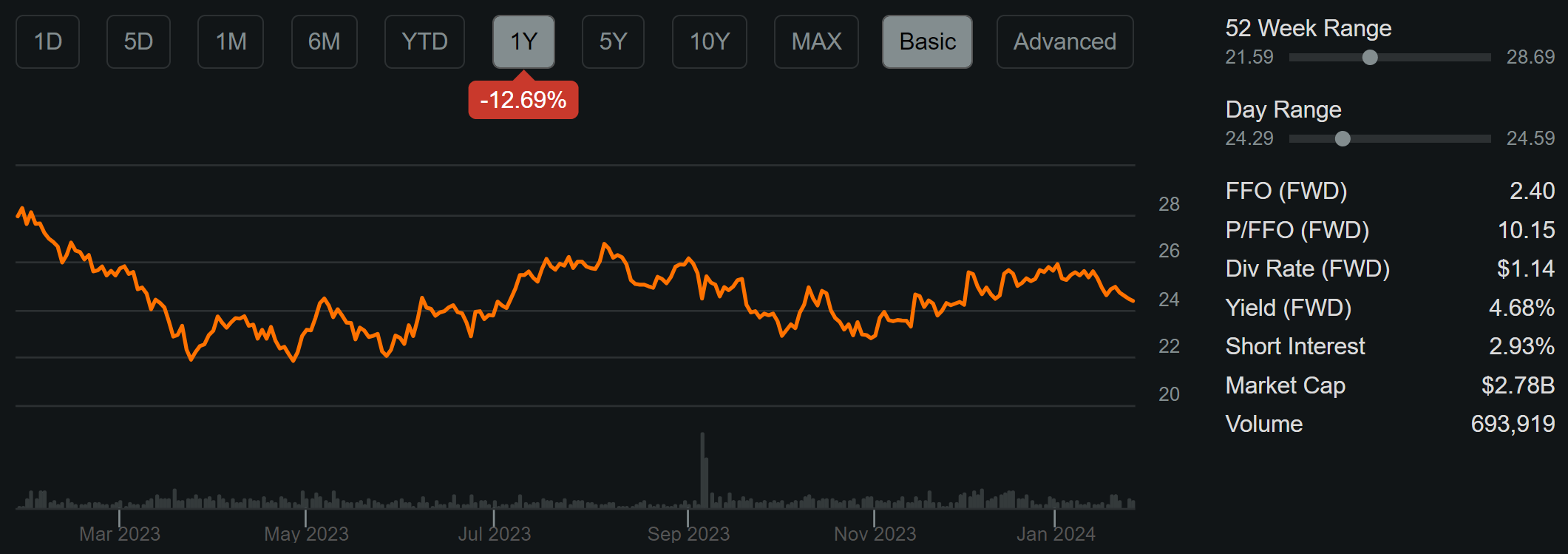

Whereas the inventory has seen its ups and downs since then, largely pushed by market hypothesis across the course of rates of interest, the inventory is down from its current peak in January to land at 1.3% under the place I lined it final. Over the previous yr CDP is down by 13%, as proven under, regardless of wholesome working fundamentals.

CDP 1-Yr Value Return (Looking for Alpha)

On this article, I present an replace and talk about why CDP continues to supply good worth and revenue alternative for affected person buyers targeted on the long-run, so let’s get began!

Why CDP?

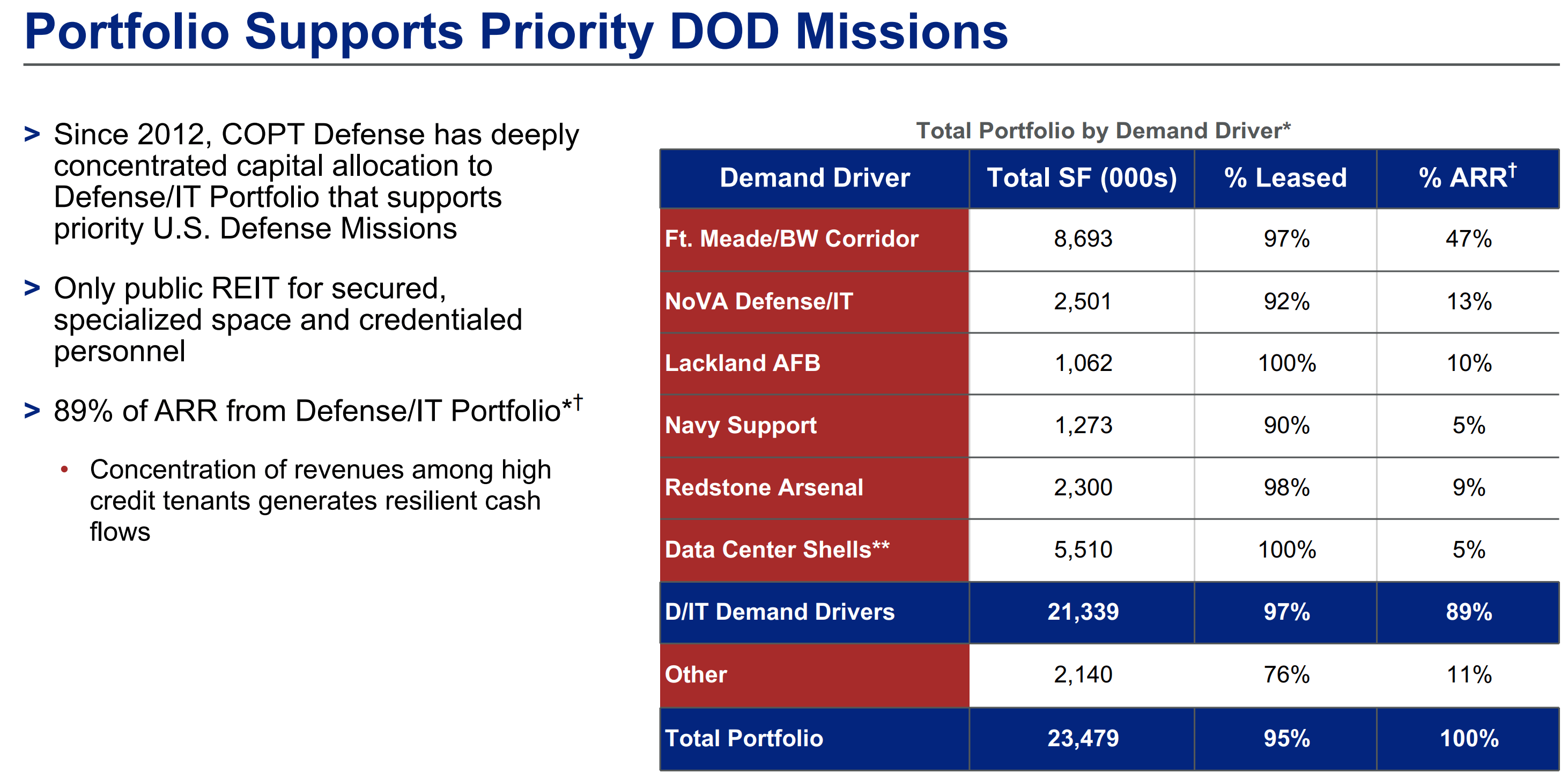

COPT Protection Properties is a member of the S&P MidCap 400 Index, and is a self-managed REIT that is targeted on proudly owning and leasing properties related to the mission-critical Protection/IT phase. This contains properties associated to the U.S. authorities and its protection contractors, from which CDP derives 89% of its annual recurring rents. At current, COPT’s portfolio consists of 188 properties overlaying 21.3 million sq. ft, of which almost half (47%) of annual rents come from Ft. Meade/Baltimore-Washington Hall, as proven under.

Investor Presentation

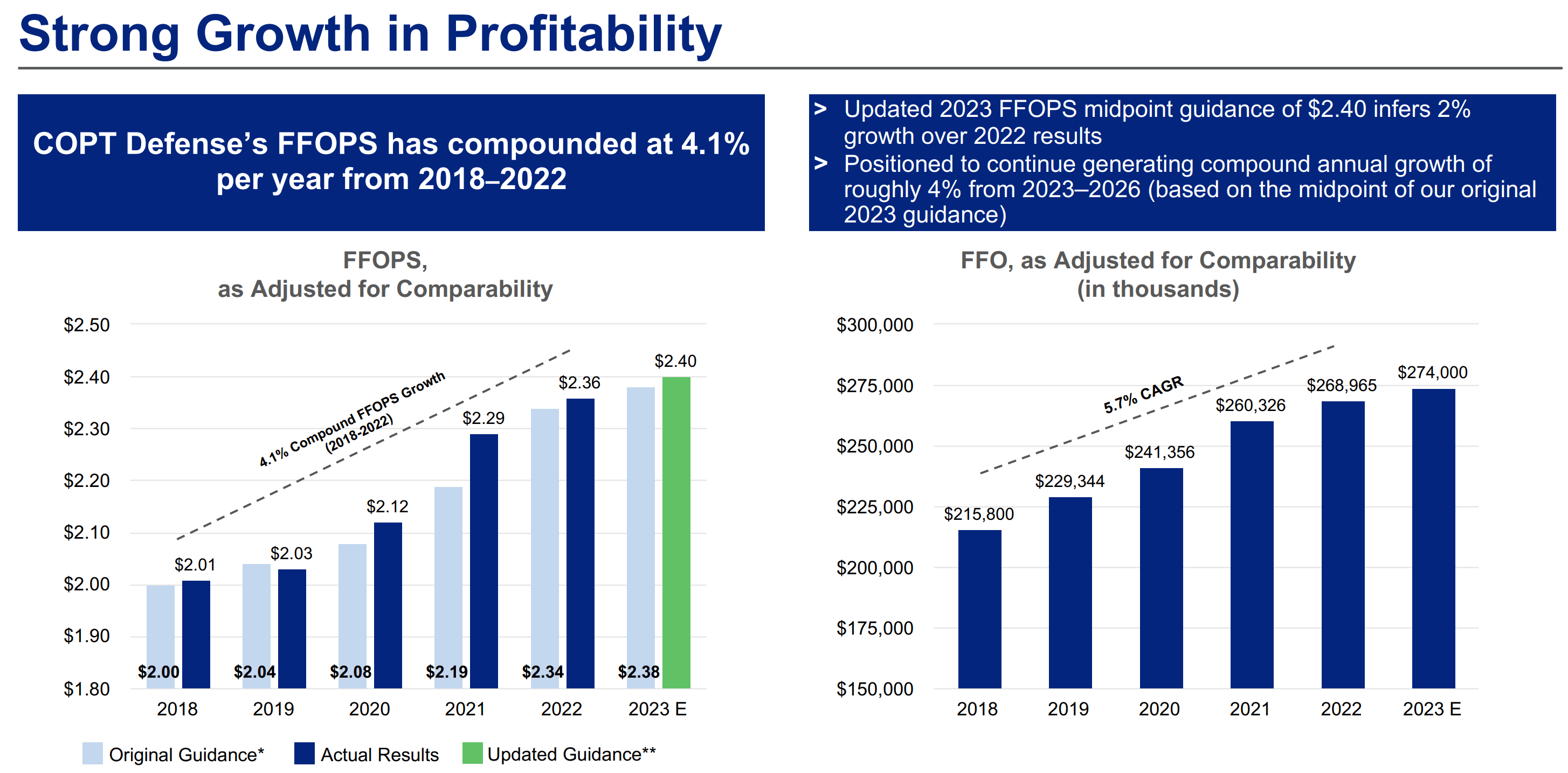

What units CDP other than its Workplace REIT friends is that distant work does probably not issue into the equation. That is as a result of the critical nature of the work carried out at its websites makes it merely unrealistic or unsecure for the work to be carried out remotely. This has resulted in regular FFO per share progress since 2018 for CDP, at a time when industrial workplace actual property has seen loads of upheaval. As proven under, CDP’s FFO/share has risen at a good 4.1% CAGR since 2018.

Investor Presentation

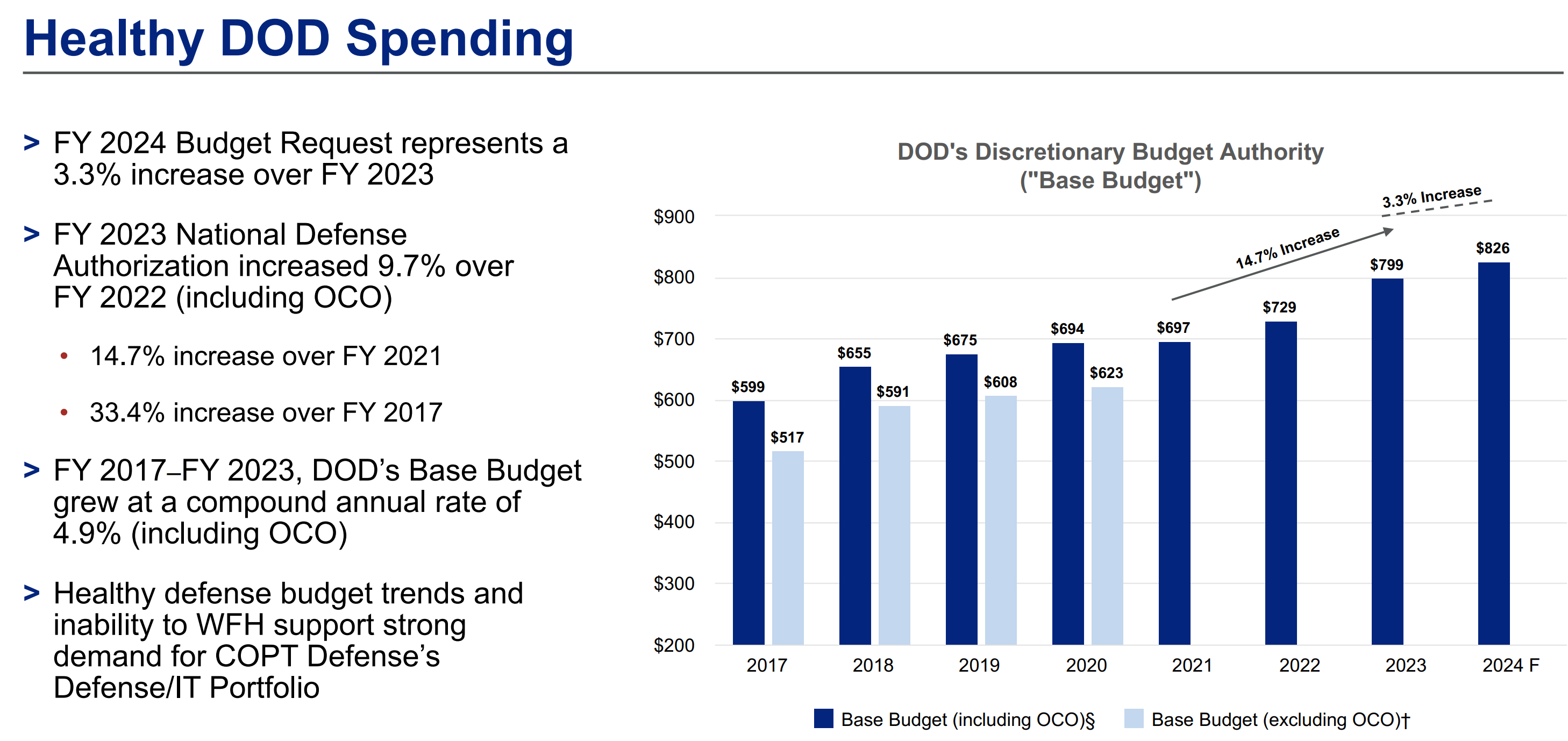

As well as, the regular nature of presidency contracts and funding for the Division of Protection makes CDP’s tenants much less vulnerable to financial downturns and company downsizing. That is supported by the next chart, which reveals that the Nationwide Protection price range has risen yearly since 2017, and that the FY23 price range rose by 9.7% over FY22. Notably, this timeframe contains government management from each U.S. political branches.

Investor Presentation

Whereas CDP’s share worth has largely stagnated for the reason that final time I visited it in October, its working fundamentals have solely strengthened over this timeframe. That is mirrored by CDP’s Occupancy bettering by 230 foundation factors from 93.6% in Q2 to 95.9% in Q3, and by the leased price bettering by 200 bps from 95.0% to 97.0% between the 2 quarters. This features a 97% leased price for the Protection/IT portfolio, which is a file excessive for the corporate because it started disclosing this phase in 2015, and represents a 70 bps YoY enhance.

Additionally encouraging, CDP continues to see similar property money NOI progress of 4.5% throughout the third quarter (down from 5.8% progress in Q2) pushed by sturdy leasing quantity and excessive tenant retention. That is mirrored by tenant retention of 83% within the first 9 months of 2023 (82% in Q3), placing CDP on observe to realize its annual aim of 80% to 85%.

Waiting for This fall outcomes sand past, CDP has avenues for exterior progress, because it has 1 million of energetic developments underway. This could possibly be a fabric progress driver for CDP, because it represents 4.7% of CDP’s present portfolio base. This contains six initiatives situated in Maryland, Northern Virginia, and Alabama, which can be already 90% leased, signaling optimistic demand drivers which can be solidly in place. Three of those initiatives have been positioned into service within the fourth quarter, with all 3 being 100% leased. Past that, CDP has the potential for an additional 1.2 million sq. ft of improvement potential, giving it an excellent line of sight into the close to to medium time period.

Dangers to CDP embrace potential for increased than anticipated inflation, which might outpace its common annual hire escalations of two.7% on just lately renewed leases. Different dangers come from the truth that CDP’s tenant well being is very dependent upon authorities funding for protection spending. Nonetheless, that threat could also be muted within the close to time period, because the FY 2024 price range request represents a 3.3% enhance from 2023 ranges, which appear cheap contemplating international conflicts within the Center East and Ukraine.

In the meantime, CDP carries a powerful stability sheet with no variable debt publicity and $200 million of money available together with 85% out there capability on its revolving credit score strains. It additionally has an affordable internet debt to EBITDA ratio of 6.0x, which is on the stage at which scores companies take into account to be protected for REITs, thereby supporting its BBB- funding grade credit standing. As proven under, CDP has no important debt maturities till 2026, thereby making it much less vulnerable to the present increased rate of interest setting.

Importantly for revenue buyers, CDP presently yields 4.7% and the dividend is well-covered by a 47% payout ratio. It is value noting that CDP has demonstrated its means to lift dividend final yr with a 3.6% enhance after maintaining the dividend flat since 2012 because it deleveraged the stability sheet.

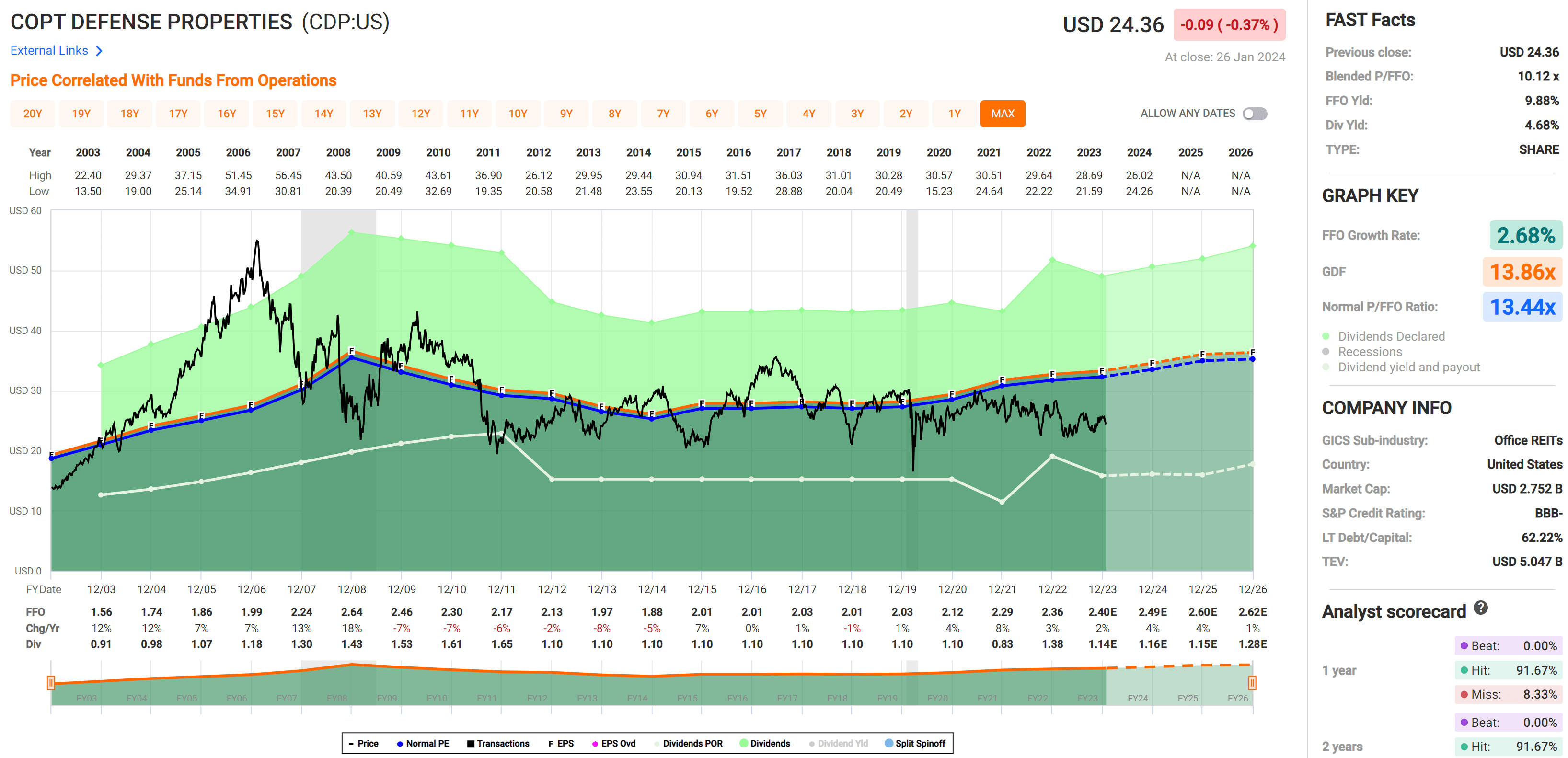

Lastly, I see worth in CDP on the present worth of $24.36 with a ahead P/FFO of simply 10.2, sitting under its regular P/FFO of 13.4. On the present valuation, the market is pricing in loads of uncertainty, which I do not imagine is affordable for CDP’s certainty round its sturdy government-related tenants. Analysts venture 4% annual FFO/share progress over the subsequent 2 years, which I imagine is affordable estimate contemplating the two.7% annual hire escalators and improvement pipeline that ought to add worth. As such, CDP might produce market-beating returns with a 4.7% yield, a 4% annual FFO/share progress price, and a conservative 2% per yr reversion to imply valuation.

FAST Graphs

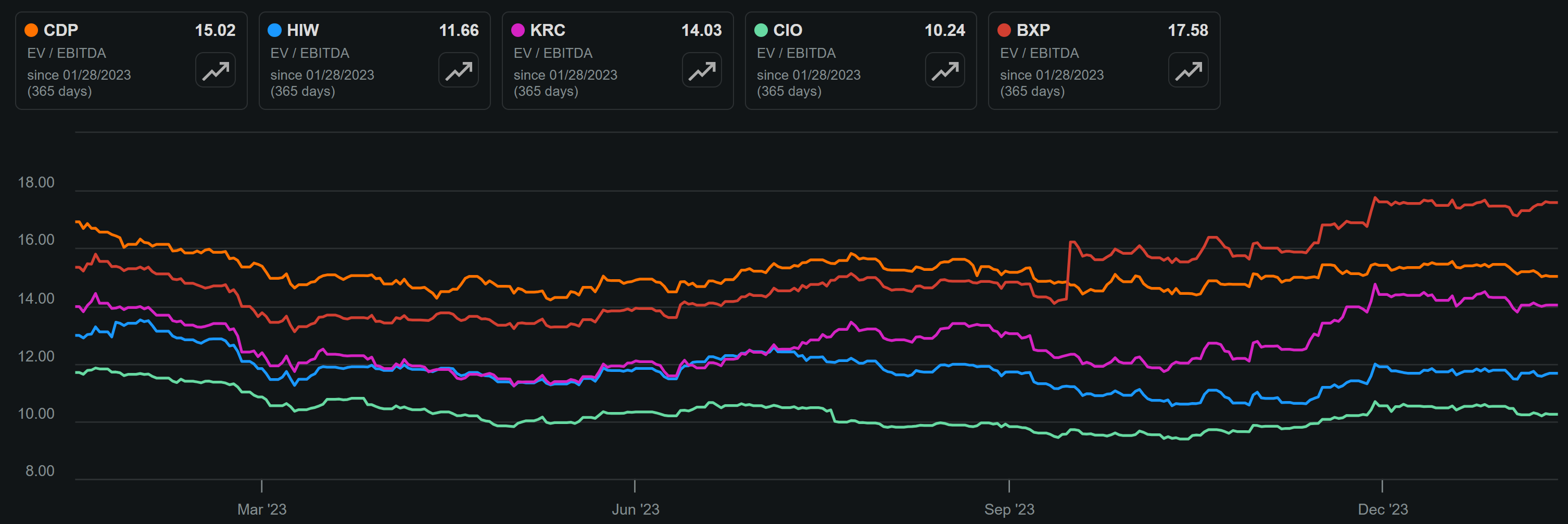

In comparison with Workplace REIT friends, CDP has a ‘center of the highway’ valuation. For this train, I exploit EV/EBITDA, since Enterprise Worth contains each the worth of fairness and debt, leading to a normalized and honest comparability in comparison with utilizing P/FFO, which measures solely fairness worth.

As proven under, CDP carries an EV/EBITDA, which is cheaper than that of Boston Properties (BXP), however dearer in comparison with Kilroy Realty (KRC), Highwoods Properties (HIW) and Metropolis Workplace REIT (CIO). Whereas I do see worth in CDP’s cheaper Workplace REIT friends, I imagine CDP stays a strong selection for these searching for a relatively safer property profile together with higher dividend progress potential within the close to time period.

CDP vs. Friends EV/EBITDA (Looking for Alpha)

Investor Takeaway

CDP has a powerful portfolio of government-leased workplace properties with secure money circulate, a fairly leveraged stability sheet, and strong dividend progress potential. Its concentrate on the protection sector supplies stability in its tenant base, whereas its improvement pipeline might drive future progress. Plus, CDP provides a lovely present yield and potential for above-market returns due partly to its undervaluation. As such, CDP could also be a worthy addition to a diversified revenue portfolio for its high quality attributes. For the above causes, my thesis round CDP stays unchanged for the reason that final time and I preserve a ‘Purchase’ ranking.