IgorSPb/iStock by way of Getty Pictures

Shares of Costamare (NYSE:CMRE) have rebounded notably in current weeks. This may be attributable to the corporate’s dry bulk and containership fleets, that are seemingly set to profit notably from the continuing questions of safety within the Purple Sea, averting vessel passage within the Suez Canal. Nevertheless, I consider that the market has not priced the advantages of this ongoing disruption totally into the inventory.

However first, let me present some context to this story.

Except you could have been dwelling below a rock these days, over the previous few weeks, Yemen’s Houthi rebels haven’t simply been disturbing vessels making an attempt to enter the Suez Canal but additionally straight-up firing rockets. Final month, they even boarded Bahamas-flagged Galaxy Chief, a car service. Trying on the footage was like these Somali Pirate movies on steroids.

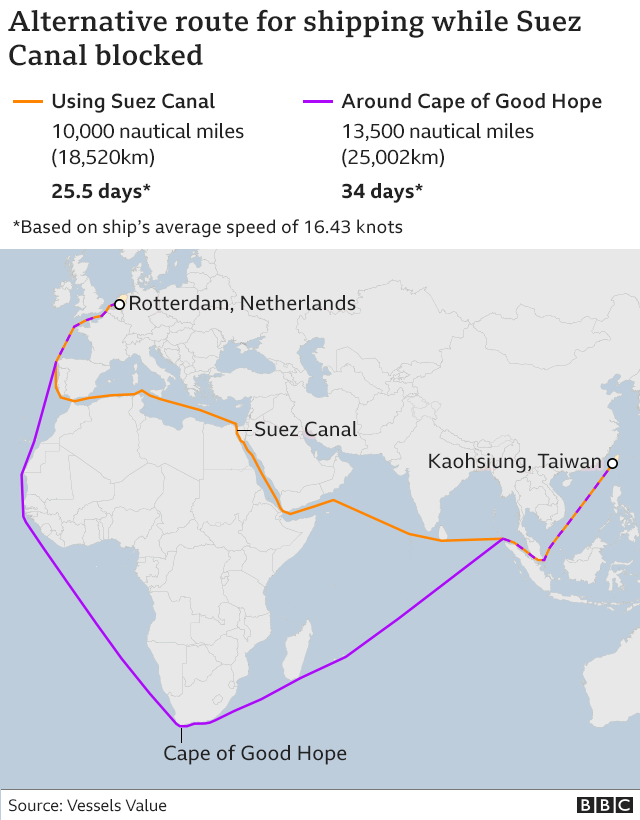

With assaults intensifying week after week, outstanding delivery corporations, similar to Mediterranean Delivery Firm, Maersk (AMKBY), Hapag-Lloyd (OTCPK:HPGLY), and the oil firm BP (BP) have all acknowledged they’re rerouting vessels away from the Purple Sea. Buying and selling from Asia to Europe now has to happen by way of vessels going all the best way round by way of the Cape of Good Hope.

Different Route To Suez Canal (BBC)

On account of an ever-riskier maritime surroundings, this implies greater gas prices, longer journeys, and better insurance coverage prices. The end result? Increased charges. If somebody is benefiting from this example, it is the vessel house owners, like Costamare.

What’s value noting right here is that we’re not used to this sort of scenario, and subsequently, we could intuitively really feel that it’s going to get resolved quickly. For many years, motion by way of the Suez Canal has been secure. Thus, the typical particular person seemingly thinks this example will probably be resolved eventually. Initiatives to revive order, similar to Operation Prosperity Guardian led by the U.S., definitely alludes to that narrative.

Nevertheless, the fact is way completely different.

Operation Prosperity Guardian failed earlier than it even started. It shortly collapsed, with Italy, Spain, and France refusing to operate under U.S. command. Who can blame them? It is just too dangerous. Positive, navy vessels can shoot down a number of drones attacking business vessels.

However what number of of them can they shoot down, and the way costly is that? Warships carry a restricted variety of missiles, and so they price loads. Houthis can ship an “unlimited” quantity of assault drones for chip change. A missile costs a couple of million dollars. A drone prices a number of thousand {dollars}. It is merely “not a good business” to be within the suicide drone interception trade nowadays.

Due to this fact, whereas you might even see some liners resuming operations within the Purple Sea, such as Maersk, that is solely as a result of a few of their vessels having the posh of being accompanied by U.S. warships. This does not apply to most vessels nonetheless compelled to go round South Africa.

I count on that even present U.S. help will fade within the space as it’s ineffective. You can not patrol and accompany each single vessel perpetually. It is simply not possible. Thus, the present scenario is destined to final for a very long time. There’s simply no solution to cease these assaults, and there’s no incentive for the Houthis to cease so long as their calls for will not be met.

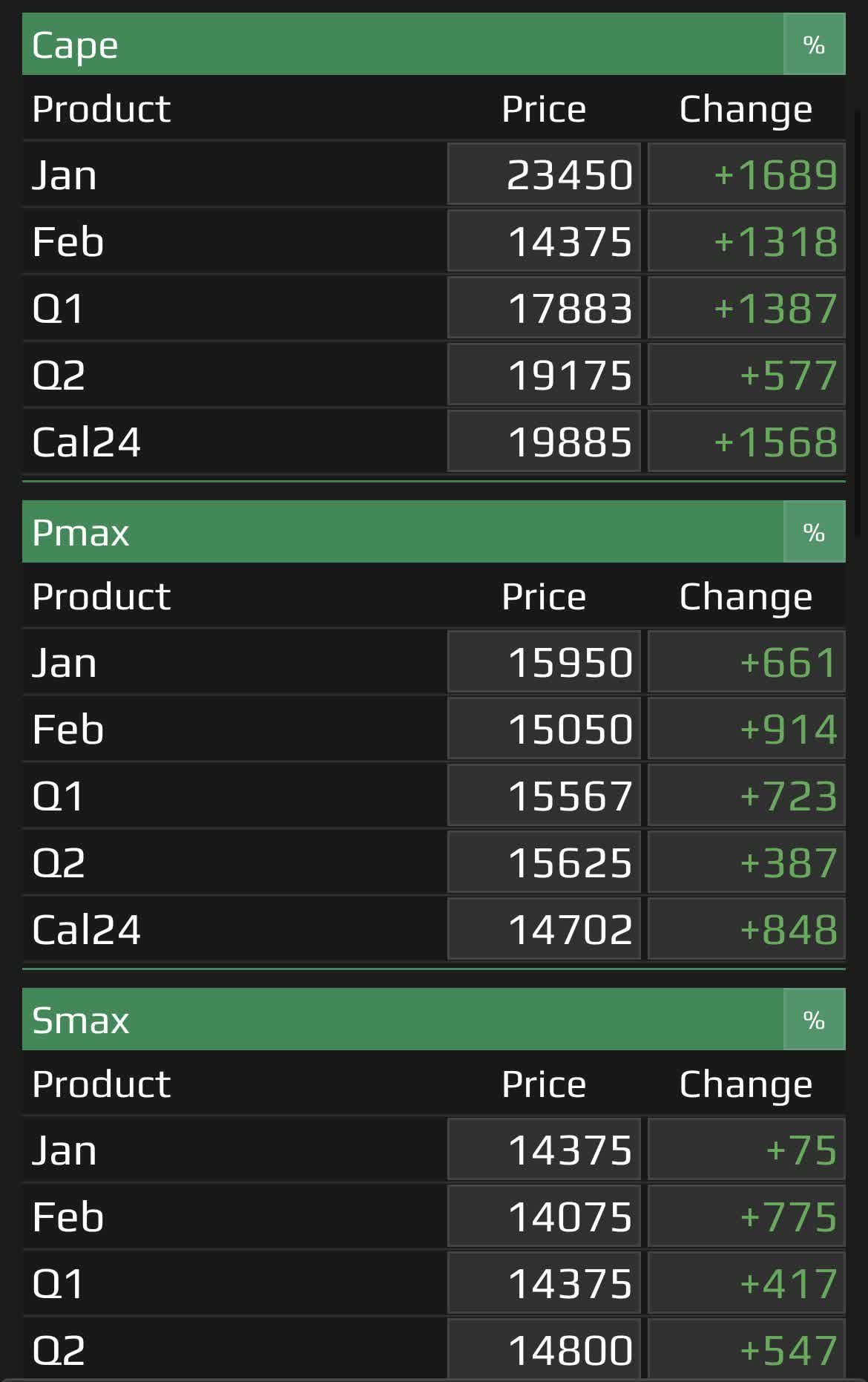

Delivery buyers perceive this. Evidently, spot charges throughout most delivery asset lessons have skyrocketed. Let’s check out the dry bulk first. Listed here are the FFAs as of December twenty eighth.

January Capes above $23K and Cal24 simply $20K are tremendous worthwhile charges.

Dry bulk FFAs (braemarscreen.com)

I consider that Costamare will profit considerably from the surge in dry bulk charges. On the finish of Q3, their 34 Newcastlemax/Capesize vessels had a mean tenor of 1.1 years, while their 14 Kamsarmax/Panamax vessels had an average tenor of 0.4 years.

These are very quick tenures, as is widespread within the dry bulk house, that means that Costamare will need to have already began renewing lots of its charters at a lot greater charges than the beforehand depressed ranges.

Within the meantime, the corporate’s containerships, which boasts a contract backlog of about $2.7 billion with a TEU-weighted period of three.7 years, is about to maintain producing resilient money flows within the coming years, as has been the case quarter after quarter these days.

As quickly as among the firm’s containerships begin popping out of their current charters, like Dyros, Arkadia, and Virgo, as proven under, it is fairly seemingly that Costamare can have the chance to resume their employment at greater charges.

Containerships With Charters Ending Quickly (Costamare Investor Presentation)

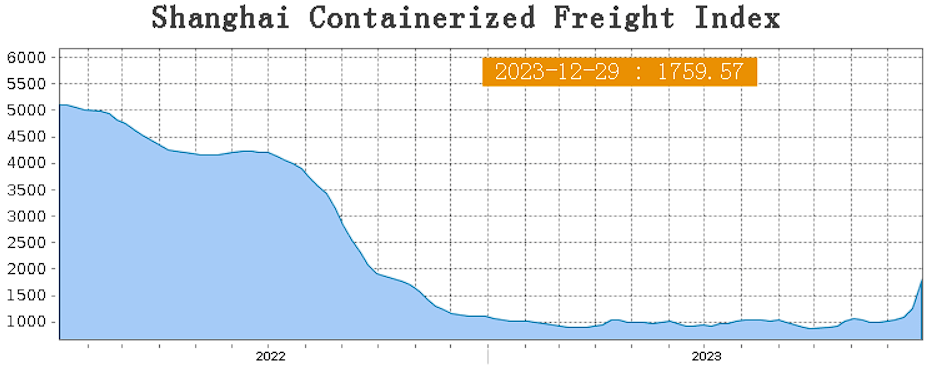

As you may see, the Shanghai Export Containerized Freight Index jumped by 40.2% week-over-week to 1,759.57 on December 29.

Shanghai Containerized Freight Index (en.sse.web.cn)

This pattern is prone to be sustained as an rising variety of containerships proceed to keep away from the Purple Sea.

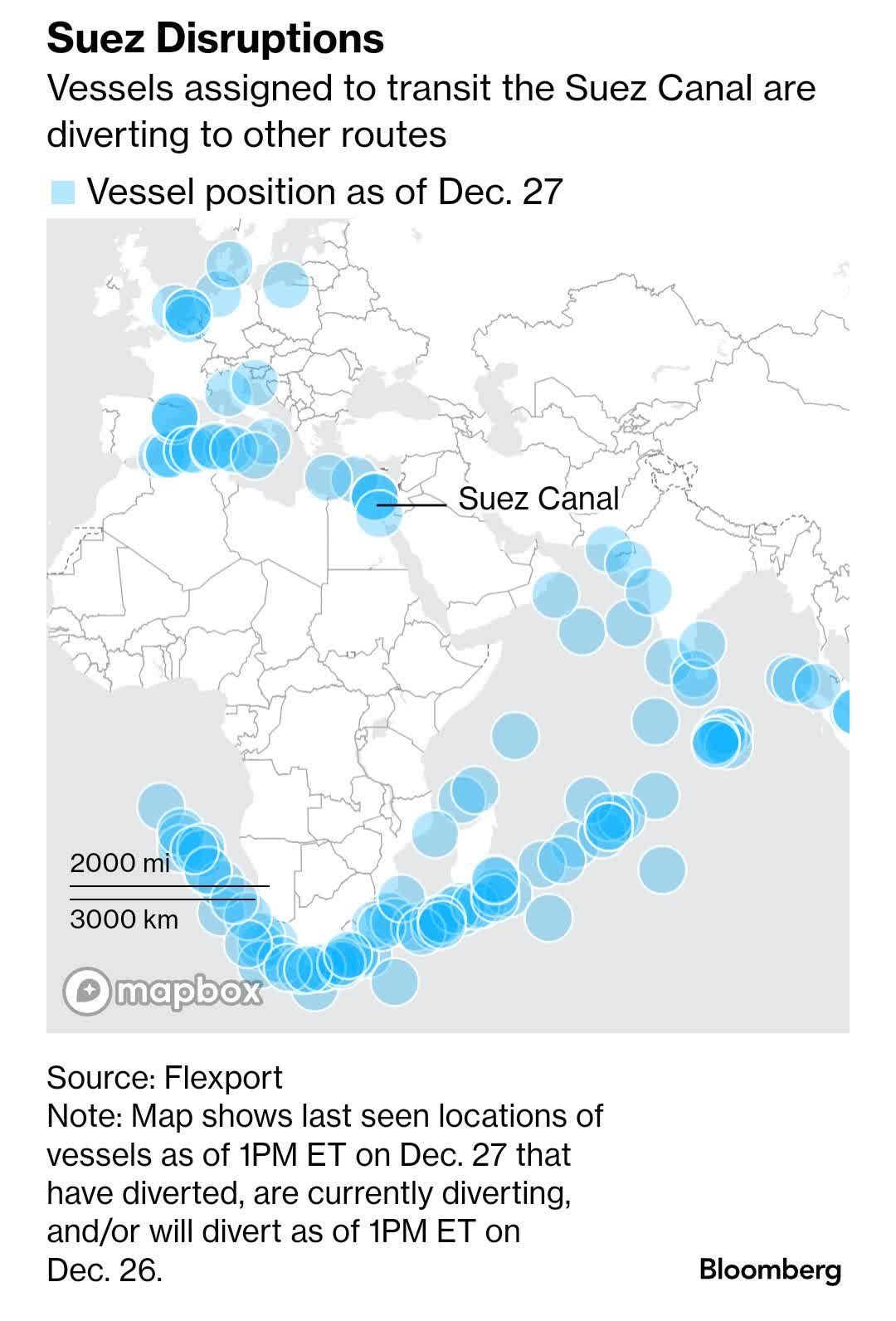

Evidently, Flexport Inc.’s newest information signifies a major change in sea routes. About 299 ships, with a complete capability of 4.3 million containers, have both modified course or are planning on doing so-double the quantity from only a week in the past, making up roughly 18% of worldwide delivery capability.

Suez Disruptions (Flexport/Bloomberg)

These new routes round Africa can take up to 25% extra time than the standard shortcut by way of the Suez Canal. In line with Flexport, this implies greater delivery prices, which may result in elevated costs for shoppers throughout numerous items, from sneakers to meals and oil, if these longer journeys proceed.

I need to spotlight once more that I do not consider this will probably be a short-term challenge. As lately as this previous Friday (Dec. twenty ninth), Mitsui O.S.Okay. Traces (OTCPK:MSLOY) and Nippon Yusen (OTCPK:NPNYY), Japan’s largest delivery corporations, additionally stated their vessels with hyperlinks to Israel had been avoiding the Purple Sea space.

Hapag-Lloyd additionally affirmed that they’ll proceed to reroute vessels across the Suez Canal for safety causes.

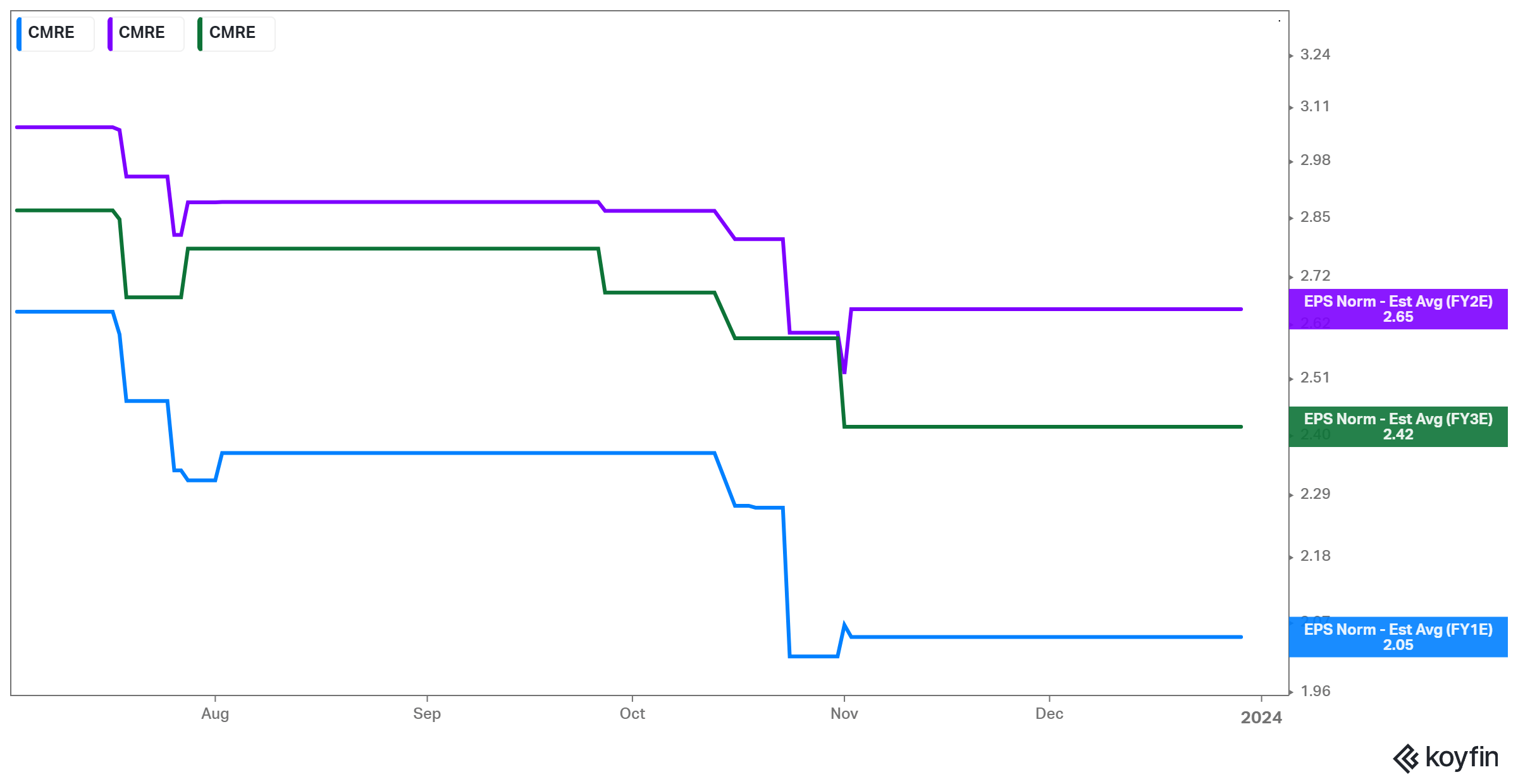

Regardless of these tailwinds for charges, ahead EPS estimates for Costamare haven’t been revised upward. Wall Road appears to be largely sleeping on the continuing Purple Sea scenario and the underlying profit on firm earnings which have been the results of the continuing disruption.

Costamare Ahead EPS Estimates (Koyfin)

Due to this fact, the inventory is at the moment buying and selling at about 5 occasions this yr’s anticipated EPS and at about 4 occasions subsequent yr’s anticipated on what are slightly pessimistic estimates, in my opinion.

Concurrently, Costamare has $996.9 million in liquidity, which equals about 79% of its present market cap, and no vital mortgage/lease maturities till 2026. Company leverage on a Market Values foundation stays under 37% as effectively.

The mixture of:

- A wholesome steadiness sheet with ample firepower for additional growth,

- an aligned administration workforce with 64% insider/household possession that has re-invested $149 million by way of Costamare’s DRIP program,

- non-dilutive financing with ongoing buybacks ($60M over the previous 12 months or 5% of present market cap,

- low cost present and ahead valuation multiples,

- and ongoing Purple Sea-related tailwinds which are seemingly not priced into the inventory,

varieties a compelling funding case, in my opinion. Accordingly, I stay bullish on CMRE inventory.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.