Editor’s word: Searching for Alpha is proud to welcome GP Sigma Analytics as a brand new contributor. It is simple to grow to be a Searching for Alpha contributor and earn cash on your finest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click here to find out more »

YvanDube

Thesis

After conducting an intensive evaluation, I firmly imagine Costco Wholesale Company (NASDAQ:COST), a widely known membership-only warehouse retailer, presents a sexy funding alternative. What catches my consideration is the corporate’s superior monetary metrics, profitability ratios, and strong top-line development prospect, pushed by its distinctive membership solely mannequin, outperforming its rivals like Walmart (WMT) and Goal (TGT). Though the inventory has risen sharply over the previous 12 months, in my evaluation it stands out as a purchase advice.

Firm Overview

Costco Wholesale Company is an Issaquah, Washington, USA headquartered large retailer based by James Sinegal and Jeffrey Brotman in 1976. Over time it has grown to function 874 warehouse and on-line platforms worldwide. Their mantra for fulfillment? A low-margin, high-volume enterprise strategy, which can appear counterintuitive to some, I imagine is a key differentiator that delivers worth constantly to members and fosters buyer loyalty and drives sustainable development.

Membership Mannequin and Buyer Loyalty

In my view, Costco’s membership-only mannequin is the important thing to their unbelievable efficiency. With 73.4 million paid members and 132 million cardholders worldwide, Costco’s loyal group drives its profitability, with membership charges totaling $4.6 billion in fiscal 2023 alone. Whereas some traders could solely see this as a quantity, I contemplate Costco’s membership mannequin to be a big aggressive benefit.

The corporate’s give attention to offering worth proposition for its members by high quality merchandise at low cost, and retention methods corresponding to discounted sizzling canine, and added companies on its tyre have helped it to take care of a loyal buyer base and generate long-term income streams. As such, its renewable charges have reached 92.9% within the US and Canada, and 90.5% worldwide. My perspective on these excessive renewable charges is that they point out sturdy buyer loyalty in the direction of the Costco model. Moreover, as tendencies point out continued market saturation and development, Costco’s membership mannequin is for my part not only a barrier to entry but additionally a logo of loyalty, making certain their dominance over the retail business.

Nevertheless, a possible membership charge hike has been overdue, primarily based on its historic common hole between hikes. That is making many traders uneasy as I count on it to hike its membership charge by round 10%, in step with its competitor Walmart’s current 11% enhance. This potential hike may considerably enhance the corporate’s web earnings, however, with inflation nonetheless above fed’s tolerance price, and up to date management adjustments, notably the appointment of Ron Vachris as CEO, and Gary Millerchip as CFO, I extremely doubt the brand new CFO would take such an enormous determination so early which may negatively affect the efficiency of the corporate.

Crafting Worth And Simplifying Selection

When it comes to the corporate’s retail technique, Costco shows a reasonably restricted however reasonably priced merchandise combine starting from groceries to fancy delicacies to state-of-the-art electronics. Every merchandise is rigorously chosen, with solely round 4,000 energetic inventory preserving items (SKUs) per warehouse in comparison with Walmart’s 100,000+. My perspective is {that a} deliberate choice course of ensures accuracy, in addition to optimizes its stock administration and offers negotiating energy with suppliers to offer aggressive pricing to its members. On the core of Costco’s retail idea lies its personal label model, Kirkland Signature, which contributes round one third of Costco’s whole income, goals to supply prime quality merchandise at reasonably priced value in comparison with name-brand merchandise. Whether or not it’s family staples or fancy delights, each Kirkland Signature product comes with Costco’s return coverage and affordability. In my view, by its unique manufacturers like Kirkland, Costco enhances its members’ purchasing expertise and differentiates itself from different retail friends.

Monetary efficiency and Outlook

Costco has demonstrated wonderful energy by constantly driving larger income development over time, primarily resulting from enlargement efforts, strong membership charges, and powerful gross sales quantity. Though Costco missed income estimates in Q2 2024, I’m not overly involved as I imagine the underlying demand and membership development remained sturdy, and value controls additional strengthening its place. The corporate reported whole income and web gross sales of $58.44 billion and $57.33 billion respectively, a rise of 5.7% Y/Y, reflecting sturdy buyer demand and better gross sales in e-commerce, however decrease than the analysts estimate due to the detrimental impacts from low gasoline value, and slower income development in its conventional warehouse enterprise.

Membership charges, which is a big contributor to the general profitability of the corporate, have been $1.11 billion in Q2 ’24, a rise of 8.2% from the identical quarter prior 12 months. This energy in membership charges is because of Costco’s sturdy enterprise mannequin and varied strategic initiatives. Moreover, Costco demonstrates proactive strategy to expense administration and budgeting, as its SG&A expense as a % of web gross sales has improved to achieve 9.14% within the newest quarter in comparison with 10.10% in fiscal 2019.

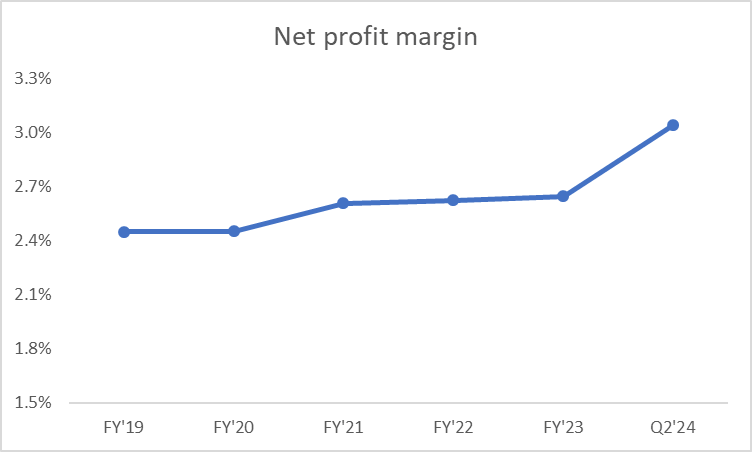

Costco’s diluted earnings per share (EPS) of $3.92 for the second quarter beat consensus estimates by $0.31. The rise in EPS was due to $94 million in tax advantages resulting from deductibility of particular dividends, and better development in membership charges. Its NPM within the second quarter reached 3% from 2.4% in fiscal 2019, showcasing operational effectivity and favorable membership tendencies over time. Whereas fluctuations in fuel costs have negatively impacted Costco’s profitability these days, the corporate has a number of doable mitigation methods. These embody underscoring development alternatives within the huge ticket discretionary class and sustaining a diligent expense administration programme. These measures sign the corporate’s underlying monetary energy to me.

Firm Knowledge, Creator’s Compilation

Strategic Initiatives and Progress Prospects

Trying forward, Costco continues to strategically pursue enlargement alternatives each domestically and globally to drive its future development. With a community of 874 membership warehouses throughout varied nations, Costco continues to discover new methods to extend retailer depend. In Q2, Costco opened 4 web new warehouses, together with one in China, and for the fiscal 2024 it plans to open 30 items in whole, largely within the US. Relating to enlargement within the US, CFO Richard Galanti through the Q2’24 earnings call mentioned:

our view is over the subsequent 10 years that we may simply add one other 150 and that is on high of nonetheless many enterprise facilities, name it, however simply within the U.S. So – and that quantity retains altering … .So, we’re discovering extra alternatives right here and it is evidenced by simply the sheer volumes of the items – that our items are doing right this moment versus three or 4 years in the past. It is a lot larger than we’d have anticipated three or 4 years in the past. So we expect that there’s nonetheless a whole lot of runway in that regard.

I’m notably impressed with Costco’s strategic initiatives like Costco Subsequent, Costco Logistic, and its E-commerce push. The profitable implementation of Costco Subsequent which comprised of reworking and relocation of shops, has considerably strengthened gross sales development, with the corporate reporting a 5.6% enhance in same-store gross sales throughout Q2 2024. In the meantime with Costco Logistics, the corporate is working to enhance its provide chain and logistics by constructing new distribution facilities and enlargement of its transportation community.

The E-commerce and digital initiatives have been of nice assist in income development for the corporate. Its on-line enterprise grew by 18.4% Y/Y final quarter, which primarily drove their general income development. I discover that these efforts not solely improve income of the corporate, but additionally set it for the long run by bettering operational excellence and provide chain. Nevertheless, there are some dangers and challenges related to it, like elevated infrastructure prices, elevated competitors from different retailers like Amazon (AMZN), Walmart and Goal, and difficulties within the means of attracting & retaining clients within the quickly evolving digital panorama.

In my view, Its energy was demonstrated final 12 months with the fast sell-out of gold bars upon their introduction. Likewise, the enlargement of Kirkland Signature model and enchancment of its omnichannel capabilities place Costco to additional drive income development and market share beneficial properties.

Valuation

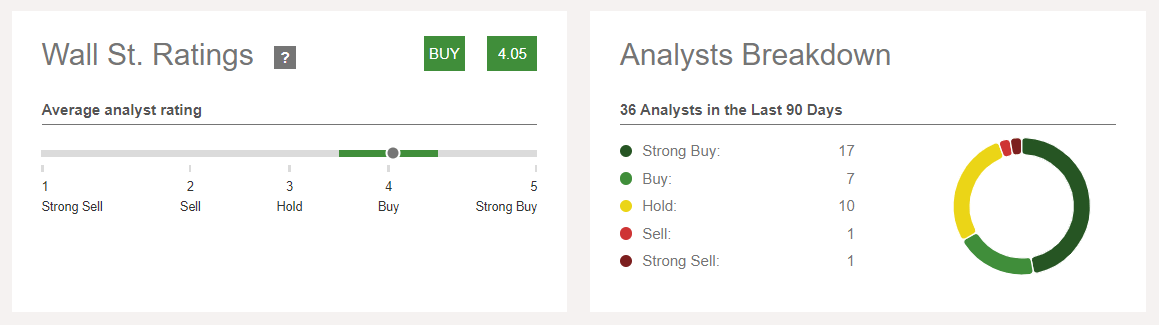

Whereas it’s true that the corporate’s share value has risen by ~45% over the previous 12 months, which some traders may even see as a warning signal about valuation, I imagine the current correction of over 10.33% presents a sexy entry level for long-term traders like myself. As well as, Money dividends of Costco make it a sexy funding selection for earnings oriented traders. Costco’s present inventory value of $705.69 displays an upside of 8.63% from Wall Road analysts average price target of $758.77. So, I’m not alone right here, 24 out of 36 analysts have both a powerful purchase or purchase score on the inventory with common rating of 4.05 out of 5.

Searching for Alpha

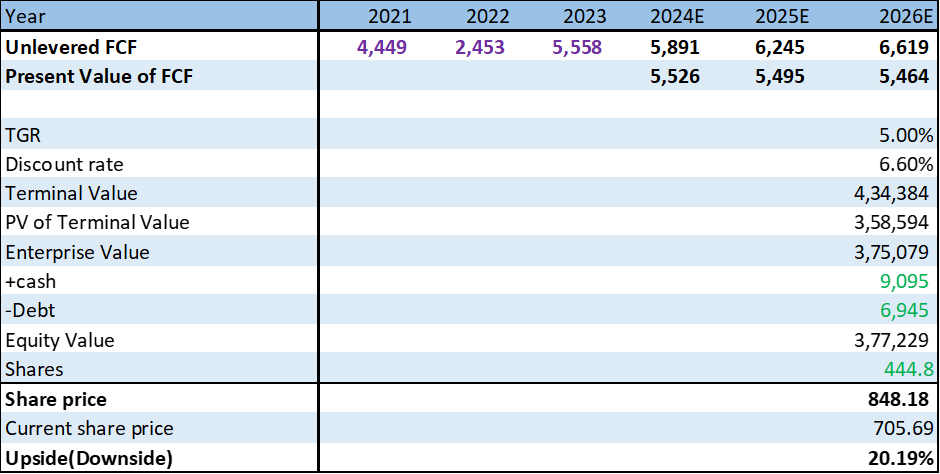

For my DCF evaluation, I’m discounting unlevered annual free money circulation (FCF) to reach on the honest worth. FCF represents the money accessible to the corporate after accounting for CapEx and adjustments in working capital, making it a extra correct illustration of the corporate’s potential to generate money flows for its stakeholders. As I count on the corporate ought to proceed to develop its FCF for fiscal FY’24 to FY’26 close to its historic 5-yr common FCF development price of ~6.18%, I’m preserving it at 6% and additional I count on it ought to have the ability to develop perpetually on the price of 5% as the corporate is already in its mature stage. This development price additionally accounts for its sturdy membership mannequin and potential charge hikes. I’m assuming a reduction price of 6.6%, which is obtained by adjusting 10-year US authorities bonds’ yield of 4.30%. I’ve added a danger premium to the risk-free price to seize the inherent dangers related to Costco’s enterprise. As you’ll be able to see in DCF output, we arrived at a good worth of $848.18 for the inventory, representing a possible upside of over 20.19%.

Costco’s DCF (Firm Knowledge, Creator’s Compilation)

For the more severe case, if we assume that its FCF grows indefinitely at solely 4.50%, which is nicely beneath its historic 5-year development price of 6.18%, and discounted at 7.00%, goal value comes out to be $549.72, which is 22.10% decrease than the present value. Now for one of the best case, as an instance its FCF grows indefinitely at 5.5% and discounted at 6.50%, the goal value comes out to be $1341.74, which is 90.13% larger than the present value. Beneath each these excessive case situations the chance of upside potential is larger. Due to this fact, I feel the inventory seems to be undervalued with sturdy potential return underneath the bottom case honest worth of $848.18.

Dangers

Costco operates in a really aggressive retail panorama, going through stress from conventional retailers like Walmart and Goal which have additionally launched membership applications in response to Costco’s success, and on-line retailers like Amazon, which has a big on-line presence, profitable membership base and has been increasing its bodily shops. Nevertheless, neither Walmart nor Goal has been as profitable as Costco with its membership mannequin or Amazon with its bodily shops enlargement.

Additionally, the corporate has gone by management adjustments lately, they now face the chance of a strategic shift from its lengthy standing rules, which may disappoint its loyal members who imagine within the worth it offers, leading to upset traders who worth the corporate at a premium in comparison with its friends. Nevertheless, for my part, Costco’s member loyalty ought to assist mitigate this danger, however nonetheless I imagine traders needs to be conscious of those dangers to make knowledgeable selections.

Conclusion

In conclusion, the monetary efficiency of Costco continues to be on an increase, pushed by operational excellence, strategic initiatives, and aided by its membership mannequin. With the aim of boosting income, increasing profitability, and seizing the enlargement alternatives, Costco is nicely positioned within the retail business to generate long-term worth for its shareholders. Primarily based on my evaluation of Costco, I’ve assigned a purchase score on the COST inventory with a value goal of $848.18.