Maksim Safaniuk

For many who are bullish about oil, 2024 is seeking to be a really stable 12 months. Already, Brent crude costs are up 12.1% 12 months to this point, whereas WTI crude costs are up a formidable 15.6%. The newest transfer larger was pushed by information that, along with OPEC+ extending its voluntary manufacturing cuts, Russia has committed to cut production by round one other 0.5 million barrels per day for the foreseeable future. Whereas some may argue that these momentary measures will trigger solely a short-term blip in costs, we might be setting ourselves up for a sustained transfer larger. However on the finish of the day, this relies largely on whose knowledge is appropriate. If the info supplied by OPEC is correct, topic to some cheap changes, the end result for the market might be costs that may exceed $100 per barrel later this 12 months. However even if the much more conservative EIA (Power Info Administration) is correct, we may see costs hover the place they’re or transfer a bit larger earlier than leveling off.

A have a look at the bullish case

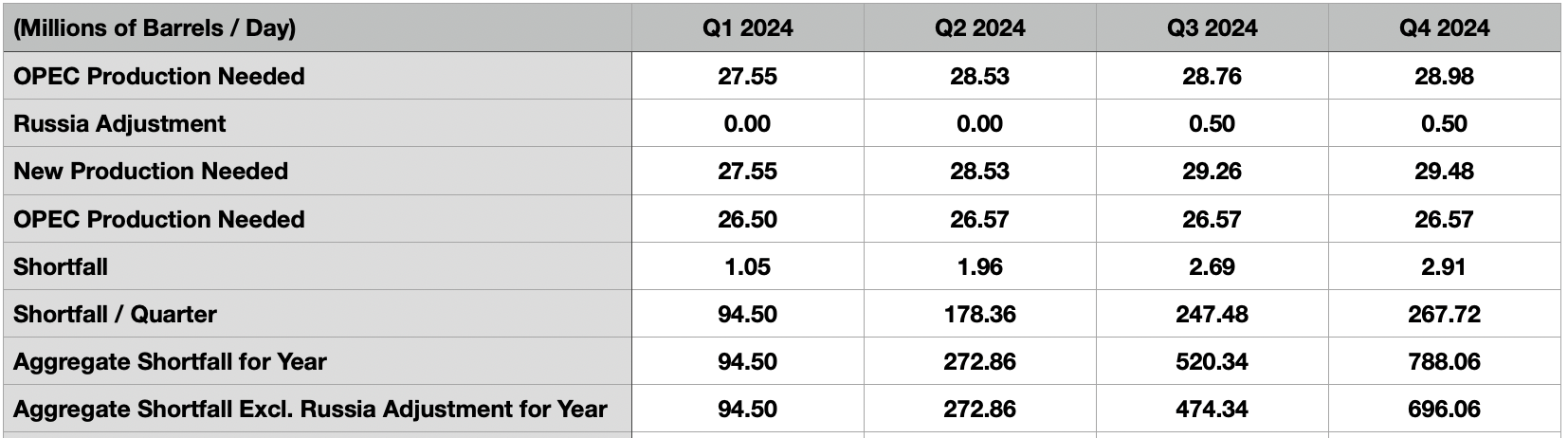

It could be greatest to begin with the case in accordance with OPEC and the data it provides. Each month, the group comes out with its personal oil report. This seems at manufacturing from its member nations, in addition to supplies a worldwide outlook of provide and demand. What’s attention-grabbing concerning the estimates supplied by OPEC is that they already end in a reasonably sizable manufacturing scarcity with out considering this extra reduce from Russia. Within the first quarter of 2024, as an illustration, it was estimated that OPEC would wish to supply 27.55 million barrels of crude and gasoline condensate per day in an effort to meet international demand. Nonetheless, it is trying like their output will probably be round 26.50 million barrels per day. That is a shortfall of 1.05 million barrels per day, or 94.5 million barrels for your entire quarter.

OPEC

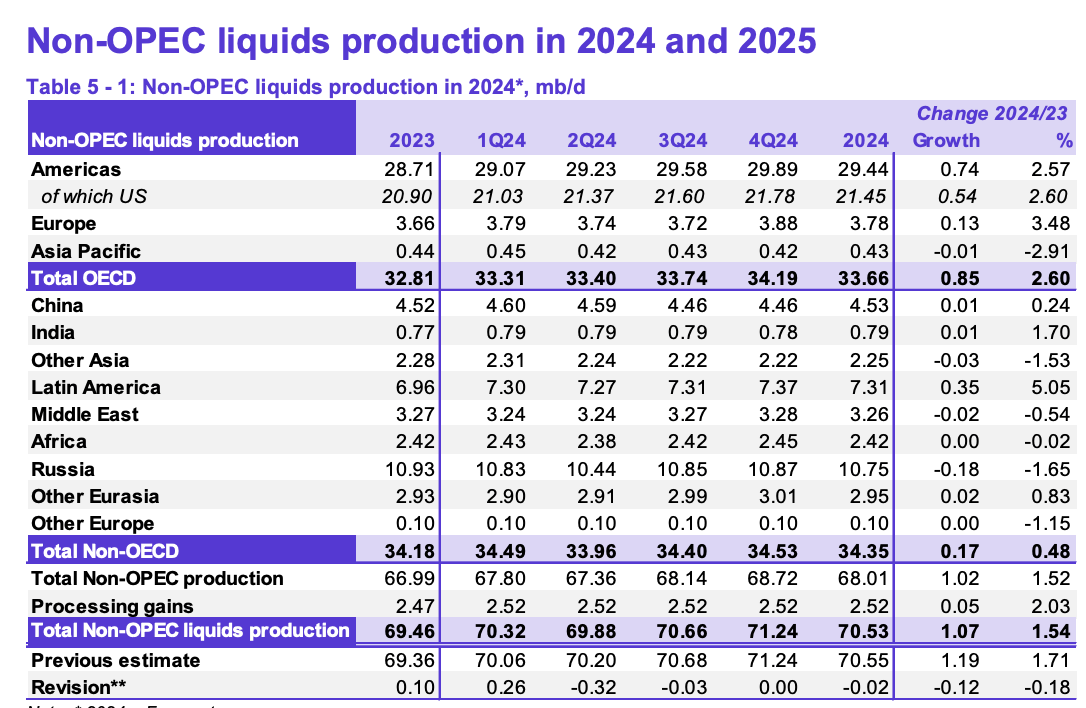

When their estimates for Russia, you see a decline from 10.83 million barrels per day within the first quarter to 10.44 million barrels per day within the second quarter. This looks as if a big unfold in comparison with the 9 million barrels per day that Russia is planning to chop output again to. However remember the fact that about 1.4 million barrels per day of output is gasoline condensate. You strip that out, and we get a quantity approximating the 9 million that the nation has introduced. So it seems as if OPEC is factoring within the aforementioned manufacturing reduce from that nation. Nonetheless, because the picture above illustrates, we see a reversal within the third quarter of this 12 months. However by that point, Russia could have solely simply reached their 0.5 million barrels per day goal. I discover it extremely doubtless that they might simply spring output again to these ranges.

Creator – OPEC Knowledge

As an alternative, it could be smart to imagine that they preserve their manufacturing reduce all through the remainder of this 12 months in an effort to preserve oil costs elevated. Because the desk above reveals, this could have large ramifications on the subject of further manufacturing coming offline. By the ultimate quarter of 2024, we might be a scarcity of two.91 million barrels per day globally. Unfold throughout your entire 12 months, this might quantity to 788.06 million barrels of crude much less in storage than what now we have at this time. Even when we assume that Russia goes again to producing a extra regular degree within the third quarter and fourth quarter of this 12 months, the shortfall may nonetheless quantity to as a lot as 696.06 million barrels.

On the finish of the 2023 fiscal 12 months, in accordance with OPEC, OECD nations had industrial inventories of round 2.76 billion barrels. This was along with 1.44 billion barrels on the water, most of which is simply oil in transit. Typically talking, an oil surplus or scarcity has been outlined based mostly on the variety of days of provide that exist in industrial inventories amongst OECD nations. Utilizing the info for the tip of 2023, we had 60.26 days value. A typical quantity ought to be someplace between 55 days and 60 days. So if something, we began this 12 months with a really modest surplus of crude. However even when half of the shortfall in oil finally ends up impacting industrial OECD inventories, excluding the additional Russian output, we might have a decline of seven.63 days. That will push us all the way down to 52.63 days value of inventories. To place this in perspective, again in 2016 when Brent crude costs averaged $43.64 per barrel, we had extra inventories of solely about 3.91 days. It would not be shocking, seeing the pendulum swing the opposite approach, to see a reasonably vital surge in costs ought to any of those situations play out.

Not as dangerous

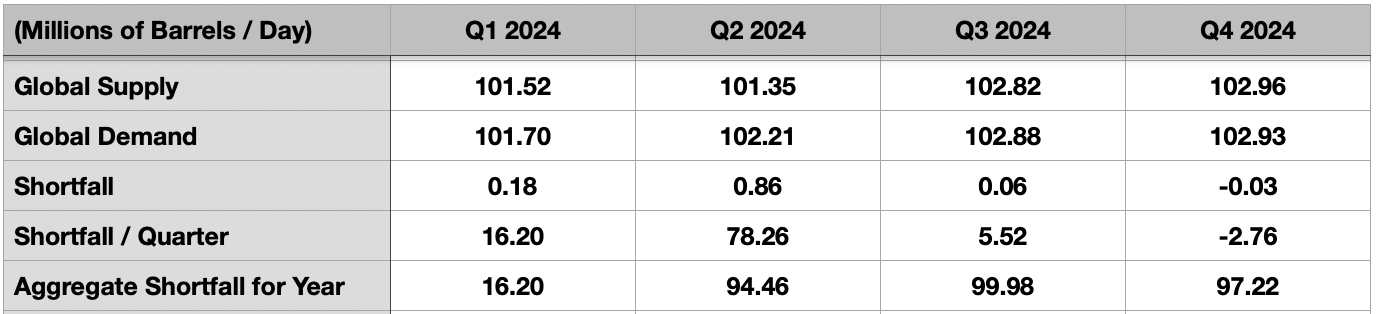

It is value noting that OPEC isn’t the one supply of estimates on this area. We must also be data provided by the EIA. Apparently, based mostly by myself observations, they’ve already accounted for sustained manufacturing cuts from Russia for the remainder of this 12 months, with solely small will increase to that output forecasted by the tip of the 12 months. This implies we need not make any changes to their numbers. Nonetheless, even in that case, we may see demand outpace provide by an honest quantity. Sure, by the ultimate quarter of this 12 months, the info suggests a surplus of crude amounting to 0.03 million barrels per day. However even with that, we’re an mixture shortfall of about 97.22 million barrels this 12 months in comparison with final 12 months.

Creator – EIA

This does create some confusion for those who dig deep sufficient into the info supplied by the group. I say this as a result of, regardless that output is anticipated to fall wanting demand, OECD industrial inventories are forecasted by the group to drop from about 2.78 billion barrels on the finish of final 12 months to 2.72 billion barrels on the finish of this 12 months. This means that each one extra inventories, after which some, will transfer be remoted to non-OECD nations. What’s extra, at 59.64 days on the finish of final 12 months and 58.59 days of provide this 12 months, the EIA knowledge appears to counsel that we are going to not have a manufacturing shortfall that is massive sufficient to push us terribly excessive. In reality, the group even went as far as to forecast that Brent crude costs will common round $83 per barrel this 12 months. That is $3 per barrel larger than what their earlier forecast known as for earlier than Russia determined to extend its manufacturing reduce. And it is also a bit decrease than present costs.

Some essential notes

For these questioning concerning the disparity between the EIA and OPEC, it truly has little or no to do with anticipated output from the OPEC+ nations. As an alternative, it has to do with anticipated oil demand for this 12 months and subsequent. Globally, OPEC sees oil demand averaging 2.03 million barrels per day extra this 12 months than the EIA is forecasting. And subsequent 12 months, the expectation is for demand to be 2.49 million barrels per day above what the EIA thinks. Though the EIA is much less more likely to be biased than OPEC is, I’d enterprise to say that OPEC in all probability has a greater concept of what is going on on within the international oil markets than the EIA does. Both approach, this appears to level to both a situation the place now we have in all probability kind of discovered a flooring in pricing or a separate situation the place costs may be anticipated to rise reasonably materially from right here. What this implies is that decrease pricing, which might be bearish for lots of the firms working within the oil and gasoline area, doubtless is not going to come to go.

EIA

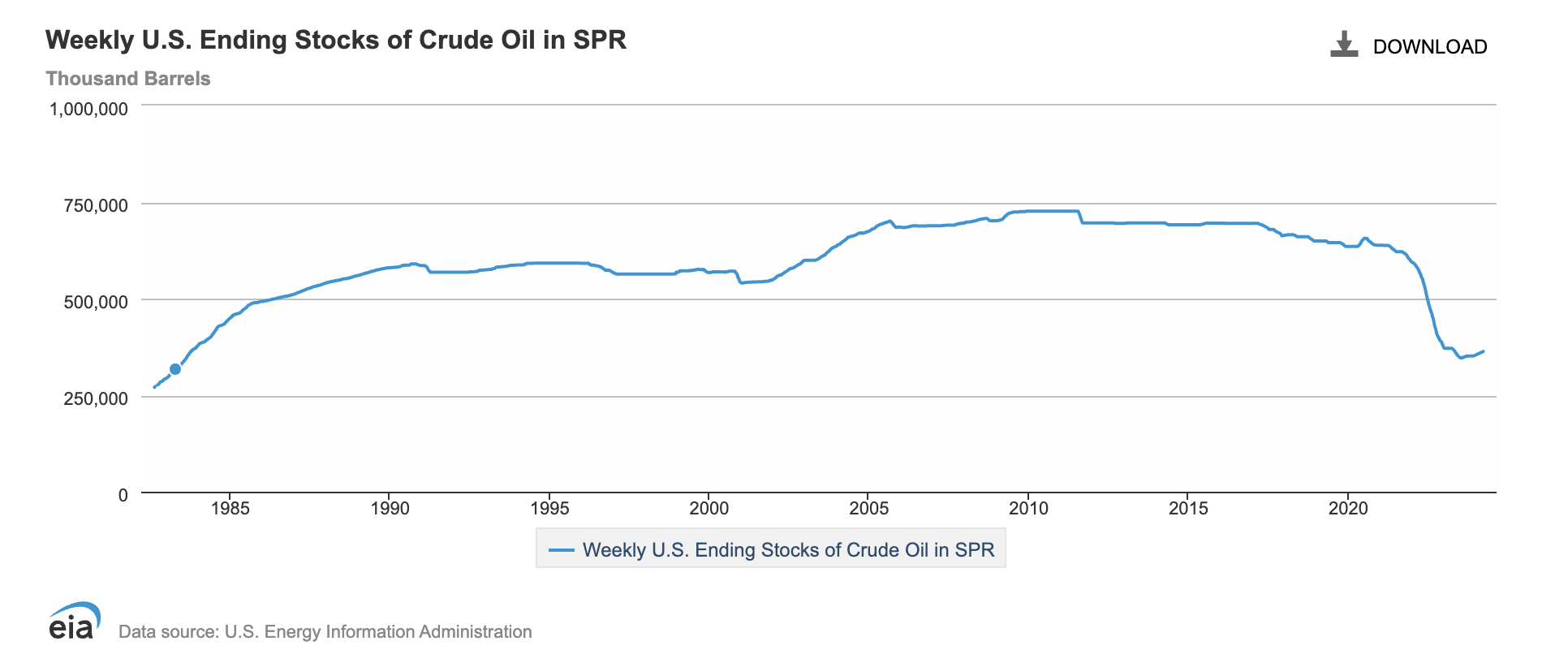

There are two further matters I wish to contact on briefly. The primary could be the concept some might need that the shale producers may simply ramp up output in response to those larger costs. I will not go into element right here as a result of I wrote an article about this subject earlier this 12 months that I imagine it is best to learn. However in brief, the large decline seen in DUC wells doubtless signifies that further vital output from the US is not going to be straightforward to attain. The second pertains to one chance the place oil costs may be capable to come down, a minimum of briefly. On condition that it is an election 12 months, it would not be shocking to see the Biden Administration faucet the SPR (Strategic Petroleum Reserve). The Trump Administration did this and different administrations have executed it prior to now as nicely. As a short-term factor, this might be attainable. However I am unable to think about it lasting various months. I say this as a result of the SPR has already seen significant drawdowns over the previous decade or so. Again in 2011, inventories within the SPR exceeded 725 million barrels at one level. However whilst lately as late 2021, inventories within the SPR we’re within the 600 million barrel to 650 million barrel vary. As of the tip of 2023, inventories stood at 426.4 million barrels. Tapping this additional, particularly to a major extent, may show worrisome from a nationwide safety perspective.

Takeaway

The way in which I see it, we’re in a heads I win, tails I do not lose state of affairs on the subject of oil costs. Those that are bullish on oil will doubtless take pleasure in elevated costs this 12 months and presumably subsequent. It is extremely unlikely that we are going to see any significant pullback beneath $80 per barrel based mostly on the info that is at present obtainable. However that is below the extra conservative situation. Beneath the extra liberal one, it is not unthinkable that costs may hit $100 per barrel or extra. There might be a short-term reprieve if the federal government decides to faucet into the SPR. However exterior of that, I feel it will take a major international financial downturn to see costs journey beneath $80 per barrel for Brent and to journey beneath $75 per barrel for WTI for any significant window of time.

Editor’s Word: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.