Daniel Grizelj/DigitalVision via Getty Images

Investment Thesis

Criteo (NASDAQ:CRTO) is showing strong momentum in its transition into a fast-growing adtech software provider. Upgraded management guidance for 2024 revenue and EBITDA has resulted in a 16% return since our last article three months ago, on February 15th 2024. However, Criteo’s EBITDA multiple has remained largely flat. We believe this indicates that the market is still pricing Criteo on this year’s metrics, and not giving due credit to its long-term growth potential. Subject to continued successful execution, Criteo’s share price is likely to continue appreciating in the coming months.

Recalling the Ongoing Transition at Criteo

Criteo’s business model used to be, and still is to some extent, reliant on cookies, which are small files that advertisers use to track consumers’ online behaviour. Criteo’s Retargeting solutions leverage cookies to collect detailed data, particularly on browsing and shopping behaviour, which enables accurate ad targeting and retargeting. As a result, online advertisements shown to consumers are tailored based on their individual preferences, which is a key pillar of ensuring a viable return on investment for online advertising campaigns. Facing the deprecation of cookies due to both regulatory and commercial pressure, Criteo’s revenue in that segment has been steadily declining in recent years. The future of Criteo now hinges on alternative addressability solutions, leveraging first-party data, emerging tools such as Google’s (GOOG) Privacy Sandbox, and also contextual targeting enabled by machine-learning.

Positive Signals from Management

For Q1 2024, Criteo reported a whopping 34% year-over-year growth in Retail Media contribution ex-TAC, and 13% for Performance Media. Even the challenged Retargeting segment, which has been declining since 2021, proved resilient with a 4% growth rate. We do not read too much into the slight uptick in Retargeting given the structural challenges it is facing in the context of third-party cookie deprecation. Over time, we still expect Criteo’s other segments to be the key revenue drivers.

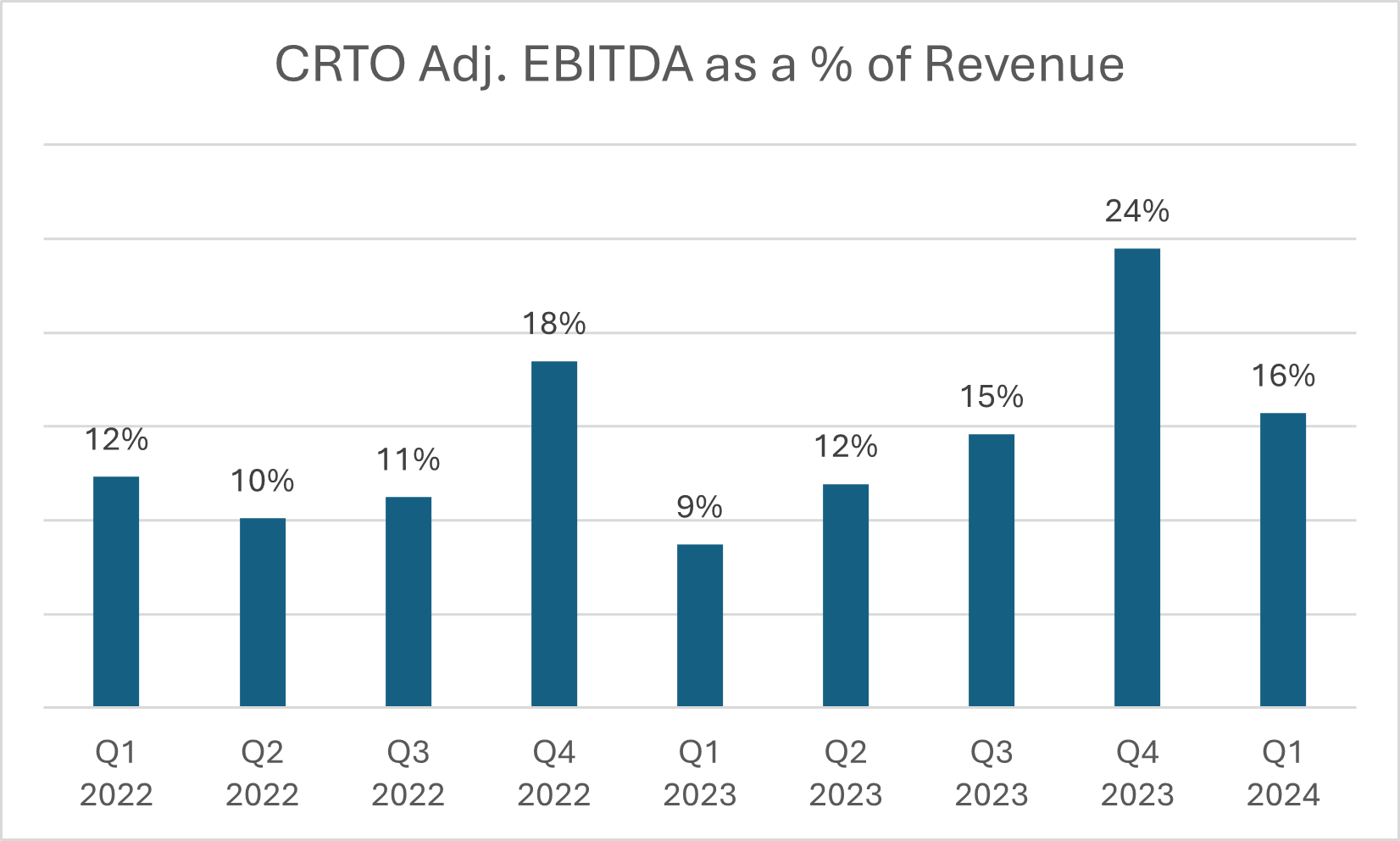

Contribution ex-TAC as a percentage of revenue remained stable vs. Q4 2023, at 56%, which is impressive given that the previous quarter had set a high bar – the average for the previous eight quarters was 49%. EBITDA margin (as a percentage of revenue), on the other hand, saw a material contraction – from 24% in Q4 2023 to 16% in the last quarter. However, 16% is still seven percentage points above Q1 2023, and as we show in the chart below, in the last couple of years this metric has shown a visible degree of seasonality, starting off weak in Q1 and peaking in Q4.

Criteo EBITDA margin as a percentage of revenue (Capital IQ)

We would like to note that we prefer to look at EBITDA as a percentage of revenue, as opposed to management’s preference for calculating it as a percentage of Contribution ex-TAC. This is because adtech companies can exercise some flexibility in terms of how they allocate certain costs between TAC and operating expenses, creating some discrepancies when comparing the profitability of peers within this space. Therefore, looking at EBITDA as a percentage of total revenue results in a more dependable, like-for-like figure. Nevertheless, looking at management’s EBITDA margin, we note that they were right on the bullseye of their guidance of 30%, which represents a twelve percentage-point uplift year-on-year, and a two percentage-point uplift vs. the previous quarter.

Operating indicators remain strong, with close to 90% overall retention, and 136% same-retailer retention measured by contribution ex-TAC. Cash balance stands at $289 million as of March 2024, of which we calculate that a further $88 million will be distributed to shareholders via buybacks in Q2-Q4 2024, on top of $62 million already deployed in Q1. These results were overall in-line with market expectations and did not trigger a significant share price reaction.

Financial Outlook

In our previous article, we expressed our confidence that the company would deliver on its 30% EBITDA margin guidance for 2024, which proved spot-on in Q1 and was amended to 31% for the full year. We also wrote that the Contribution ex-TAC growth guidance of mid-single digit for 2024 seemed conservative, and in fact management also revised it upward to “high-single-digit”. We wrote that if the company delivered on these estimates, we would expect a share price increase of approximately 13%, based on an enterprise value of $1.8 billion. We are pleased to see that the enterprise value stands at $1.9 billion at the time of writing this article, implying a 16% return since we last covered Criteo.

Our projections for 2024 remain unchanged – we underwrite management’s projections of high-single-digit growth and 30%+ EBITDA margins. Additionally, we remain confident that Criteo will unlock double-digit growth starting in 2025. So far, the company’s share price appreciation has been very close to the increase in expected EBITDA, resulting in a practically unchanged multiple of a little over 5x EV / NTM EBITDA. Upon showing positive indicators of double-digit growth towards the end of this year or start of 2025, we expect this multiple to re-rate upwards over time, to no less than 10.0x EV / NTM EBITDA in the mid-term, converging with that of other adtech peers growing at similar rates. This would imply an equity value of c.$3.7 billion, and a c.75% return vs. the current share price of $37.40.

Key Risk Factors

The primary risks to Criteo’s investment thesis are unchanged from those identified in our previous analysis. The key concern for Criteo, like other companies in the AdTech sector, is the potential negative impact of a challenging economic climate. The advertising industry is notoriously vulnerable to economic fluctuations, which can cause a decrease in clients’ advertising budgets, thereby affecting Criteo’s revenues. The company’s results are therefore prone to changes in the economic landscape that may influence advertising expenditure.

Additionally, there is the concern of a quicker-than-expected decline in Retargeting revenue, which remains a significant component of Criteo’s revenue mix. With the industry moving away from the use of third-party cookies – a critical tool for targeting and measuring ad effectiveness – this area is likely to face ongoing challenges.

Furthermore, the regulatory and commercial environment surrounding user privacy poses continuing risks. Shifts in data privacy laws and standards, especially those related to online advertising and consumer data protection, could lead to new compliance demands or limit certain advertising methods. Major industry players such as Apple and Google may keep enhancing the privacy of their ecosystems, which could adversely affect the business models of third-party companies that depend on these platforms. We do note that Google’s recent postponing of cookie deprecation into 2025 provides some breathing room in this respect. Similar industry-wide developments could have a significant impact on Criteo’s business plan.

Conclusion

Criteo’s strategic pivot towards becoming a once-again fast-growing adtech player is showing promising signs, underscored by the positive revisions in management guidance for 2024. Despite this strong recent performance, the market’s perception of this stock remains anchored to short-term metrics, overlooking the broader growth potential in the coming years. We see Criteo as a resilient name in the face of ongoing industry challenges, notably the shift away from third-party cookies. Barring an unforeseen macroeconomic downturn, we expect Criteo’s share price to align more closely with its intrinsic growth potential over time. As the market gradually acknowledges the company’s long-term value proposition, we foresee a re-rating of its valuation multiples towards those of its high-growth peers, and a substantial share price uplift as a result.