Arturo Holmes/Getty Photographs Leisure

Following my latest Crocs article

In October, I wrote an article about Crocs (NASDAQ:CROX), grading it as a robust purchase. I addressed the vital query relating to Crocs’ future: its model reliance. Since then, the market has skilled an enormous rally, with the inventory hovering by 27%. Nevertheless, in November, the Q3 earnings had been launched, and, in my opinion, they weren’t constructive. On this article, I’ll clarify why I imagine the mix of the upper value and unsure outlook is adequate to downgrade the inventory to a purchase.

I’ll present an up to date valuation and take a better take a look at administration incentives, an element I didn’t embrace in my final article.

Administration

Total, Andrew Rees, because the chief, has orchestrated an unbelievable run since assuming the function in 2017. He holds roughly 950,000 shares of the corporate, most certainly constituting a good portion of his web price, particularly contemplating his prior absence from a serious CEO place earlier than Crocs. This implies robust private incentives for him to boost the corporate’s efficiency and, consequently, the inventory value.

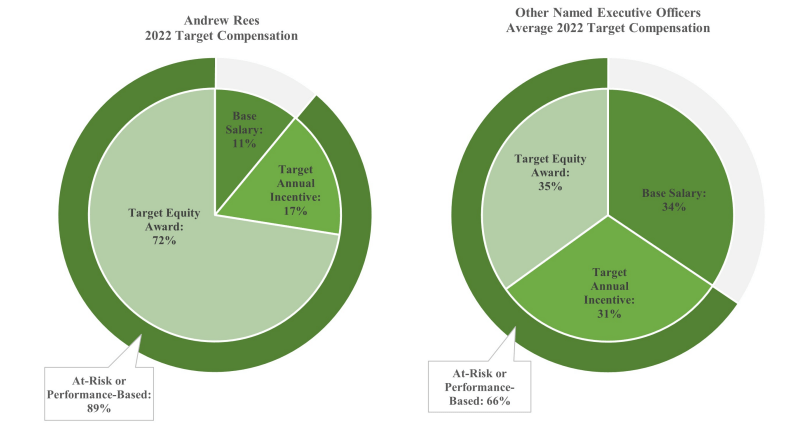

The motivation system in place is powerful, with nearly 90% of the CEO’s compensation in danger, and round 70% of the entire compensation within the type of fairness. Different NEOs, together with the CFO and COO, allocate about two-thirds of their compensation on a efficiency foundation, with half of it in fairness. Administrators even have greater than 50% of their compensation tied to fairness.

compensation construction (crox proxy)

It is price mentioning that in round August, each the CFO and one of many administrators made direct purchases of the inventory at costs of $101 and $94, respectively—not removed from the present valuation.

Q3 and up to date valuation

In abstract, I’m not impressed with HEYDUDE’s efficiency; it has declined by 9% YOY in Q3 and is projected to additional lower in FY23. Whereas the model stays robust, the disconnect between its energy and precise gross sales raises questions for me relating to the administration’s M&A initiatives. This uncertainty casts doubt on future development charges, essentially altering the valuation. Now, a 5% development charge doesn’t appear out of attain.

For FY 23, administration has up to date their steering, forecasting a top-line development of 10-11%, amounting to round $3.9 billion. This represents a lower from the beforehand said 12-14% steering. The revision is primarily attributed to weak gross sales in HEYDUDE, whereas the steering for the Crocs model stays unchanged.

HEYDUDE gross sales are projected to say no by 4-6%, as indicated by professional forma projections. These figures seem inconsistent with the model energy that Crocs claims HEYDUDE possesses. Notably, the model has skilled a major improve in model consciousness, rising from 18% to 32% in simply 5 months. Moreover, HEYDUDE has achieved a notable rating because the seventh favourite footwear model.

Though the corporate reveals high quality, as evidenced by excessive returns on capital, the surge in value and the complexities surrounding the HEYDUDE model have considerably altered the valuation panorama.

In evaluating my latest valuation with the brand new ones, I am putting explicit emphasis on the expansion charges. Initially, I thought of a 4% development charge to be overly pessimistic, however given the weakened HEYDUDE gross sales, I’m now reconsidering this attitude. The present scenario suggests {that a} extra cautious strategy may be warranted.

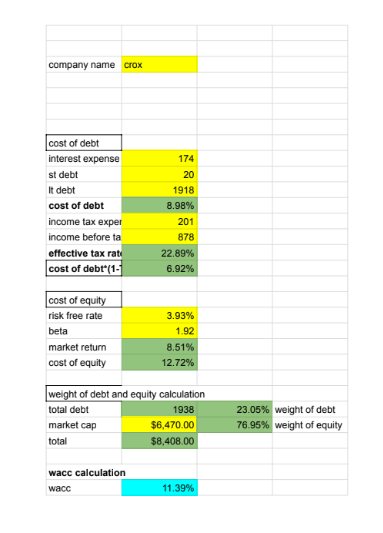

Moreover, I imagine that my wacc calculation is now extra correct. It is important to acknowledge that whereas perfection is unattainable in such calculations and they’re topic to steady change, the changes made contribute to a extra exact analysis within the current context.

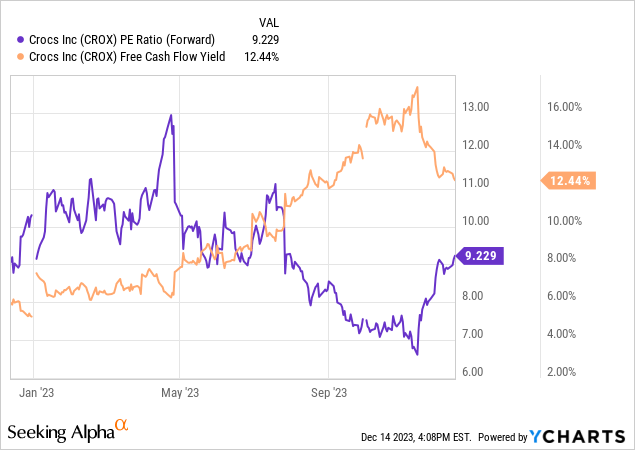

Presently, with a 12% FCF yield for a enterprise with a excessive ROCE, it nonetheless seems low-cost, however the questionable development trajectory poses a problem. Assuming analyst estimates of seven% EPS development subsequent yr, we find yourself with a 1.3 PEG ratio, which does not place it as a cut price.

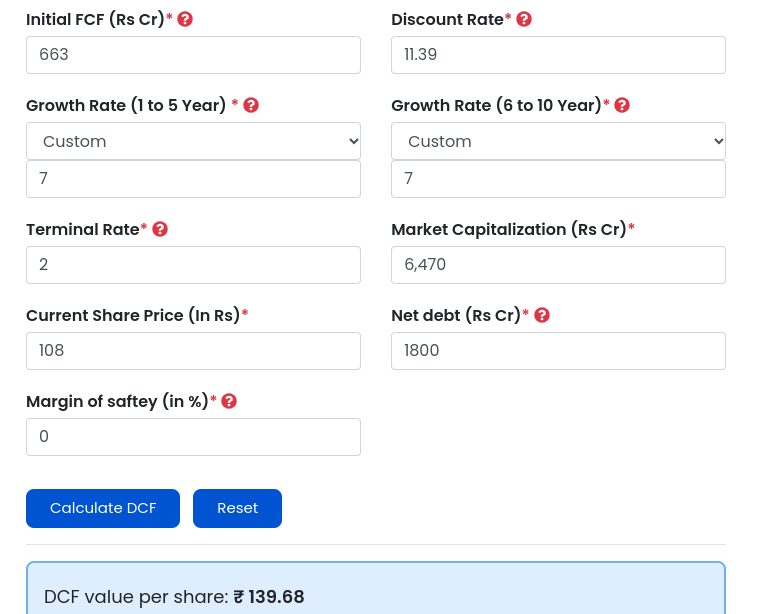

Contemplating the discounted money stream, I imagine it’s extra correct. I used the 17% free money stream margin from the final yr, factoring in a 2% terminal development charge and an up to date 11.3% wacc. Assuming a 7% development charge, which aligns with analyst EPS development estimates for the subsequent three years, the inventory seems undervalued by 22%. Nevertheless, these assumptions are contingent on the expansion of HEYDUDE or, conversely, a a lot larger development from the Crocs model.

wacc (writer)

DCF (finology)

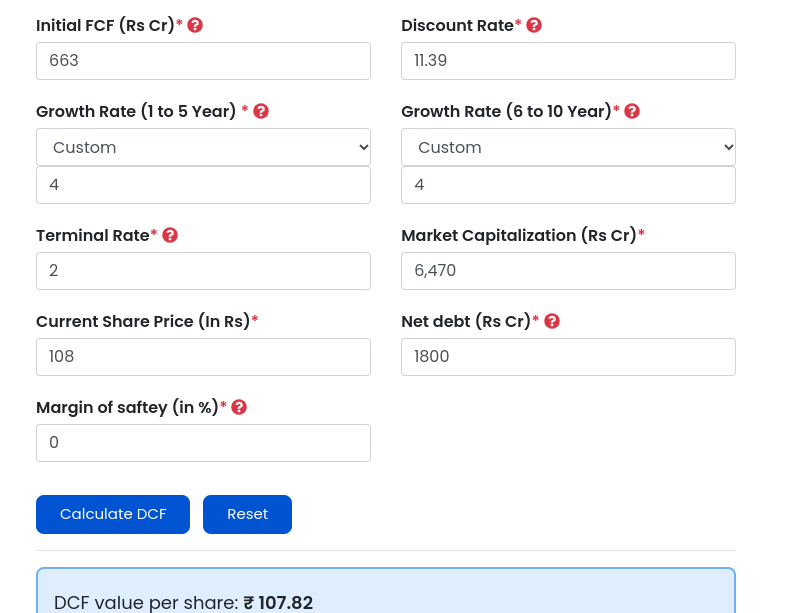

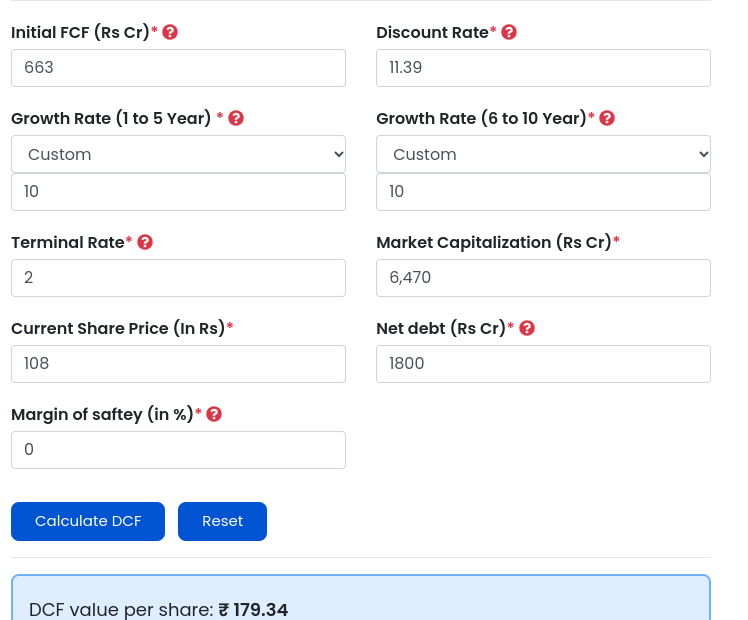

In a extra optimistic state of affairs the place HEYDUDE’s recognition interprets into substantial gross sales (assuming a ten% development), we see a 39% undervaluation. Conversely, if issues worsen from HEYDUDE’s perspective and development slows to the 4-5% vary, the inventory can be pretty valued. That is acceptable should you imagine within the top quality of the enterprise, however I do not take into account it to be the very best high quality, given the related dangers.

DCF (finology)

DCF (finology)

Conclusions

Contemplating the value surge since my final article and the underwhelming outcomes from HEYDUDE, I imagine the extra acceptable ranking for Crocs, in my opinion, is a purchase, downgrading from a robust purchase.

I keep the expectation that the corporate will proceed to outperform, particularly contemplating the comparatively low present value. The viability of this outlook hinges on the corporate’s skill to maintain development within the larger single digits. Nevertheless, the important thing threat, in my evaluation, lies within the efficiency of HEYDUDE. This issue can be intently monitored shifting ahead.

The potential upside is important if the expansion aligns with the model energy asserted by the administration. Nevertheless, as a result of inherent dangers that this may not materialize, I’m reevaluating the funding’s energy, and it not qualifies as a robust purchase in my evaluation.

I want to hear your opinion on this threat/reward play.