xxwp

We beforehand coated Crocs, Inc. (NASDAQ:NASDAQ:CROX) in September 2023, discussing its underwhelming prospects forward, due to the immense pulled ahead development throughout the hyper-pandemic interval and the painful normalization in demand over the following few years.

Mixed with the tightened discretionary spending from the elevated rate of interest surroundings and the reimbursement of federal scholar loans from October 2023 onwards, we had most well-liked to downgrade the inventory as a Maintain then.

On this article, we will talk about why the CROX inventory’s current restoration is prone to be unsustainable, attributed to the decelerating development of its core model and HeyDude’s disappointing efficiency, worsened by the slowing gross sales within the North American area.

With it now not providing a compelling development story and no dividends to stay up for, we consider that the inventory might at finest commerce sideways forward, till the administration is ready to generate convincing development in gross sales.

CROX Is No Longer A Viable Progress Funding Thesis

For now, CROX has generated a double beat FQ3’23 earnings call, with overall revenues of $1.04B (-2.4% QoQ/ +6.2% YoY) and adj EPS of $3.25 (-9.4% QoQ/ +9.4% YoY).

A lot of the top-line tailwinds are attributed to the sturdy efficiency of Crocs Model gross sales of $798.8M (-4.1% QoQ/ +11.6% YoY), albeit pulled down by HeyDude’s declining gross sales of $246.9M (+3.1% QoQ/ -8.3% YoY).

Then once more, CROX continues to document exemplary improve in its adj gross margins to 57.4% (-0.7 factors QoQ/ +2.3 YoY), implying the sturdy demand for its Crocs merchandise.

This has allowed the administration to partially offset the rising operational prices of $307.7M (+1.6% QoQ/ +13.7% YoY), triggering its considerably secure adj working margins of 28.3% (-2 factors QoQ/ +0.4 YoY).

Whereas the CROX administration has raised its FY2023 bottom line guidance to $11.70 (+7.1% YoY) on the midpoint, due to the upper gross margins, it’s obvious that the top-line steering has additionally been lowered to $3,922.5M (+6% YoY).

That is in comparison with the previous midpoint guidance of $11.15 (+2.1% YoY) and $3.95B (+9.7% YoY) provided within the FQ4’22 earnings name, respectively.

If readers look intently, CROX additionally guided impacted adj working margins of roughly 21% in FQ4’23 (-7.3 factors QoQ/ -5 YoY) in comparison with 27.7% in FY2022 (-2.4 factors YoY), implying that HeyDude’s overhead and distribution community prices might stay elevated.

That is worsened by the minimal development guided for the HeyDude model, with a This autumn’23 steering of -5% YoY decline in gross sales, additional underscoring why shareholders have remained bearish on the administration’s newest acquisition.

The one few shiny spots in CROX’s FQ3’23 report is its wholesome steadiness sheet, with the declining long-term money owed of $1.91B (-4.5% QoQ/ -26.2% YoY) triggering the discount in its gross leverage to 1.7x (-0.1x QoQ/ -0.7x YoY).

That is on prime of the sustained share retirement to this point, with 61.62M of shares excellent within the newest quarter (-0.98M QoQ/ -0.75M YoY/ -10.15M from FY2019 ranges).

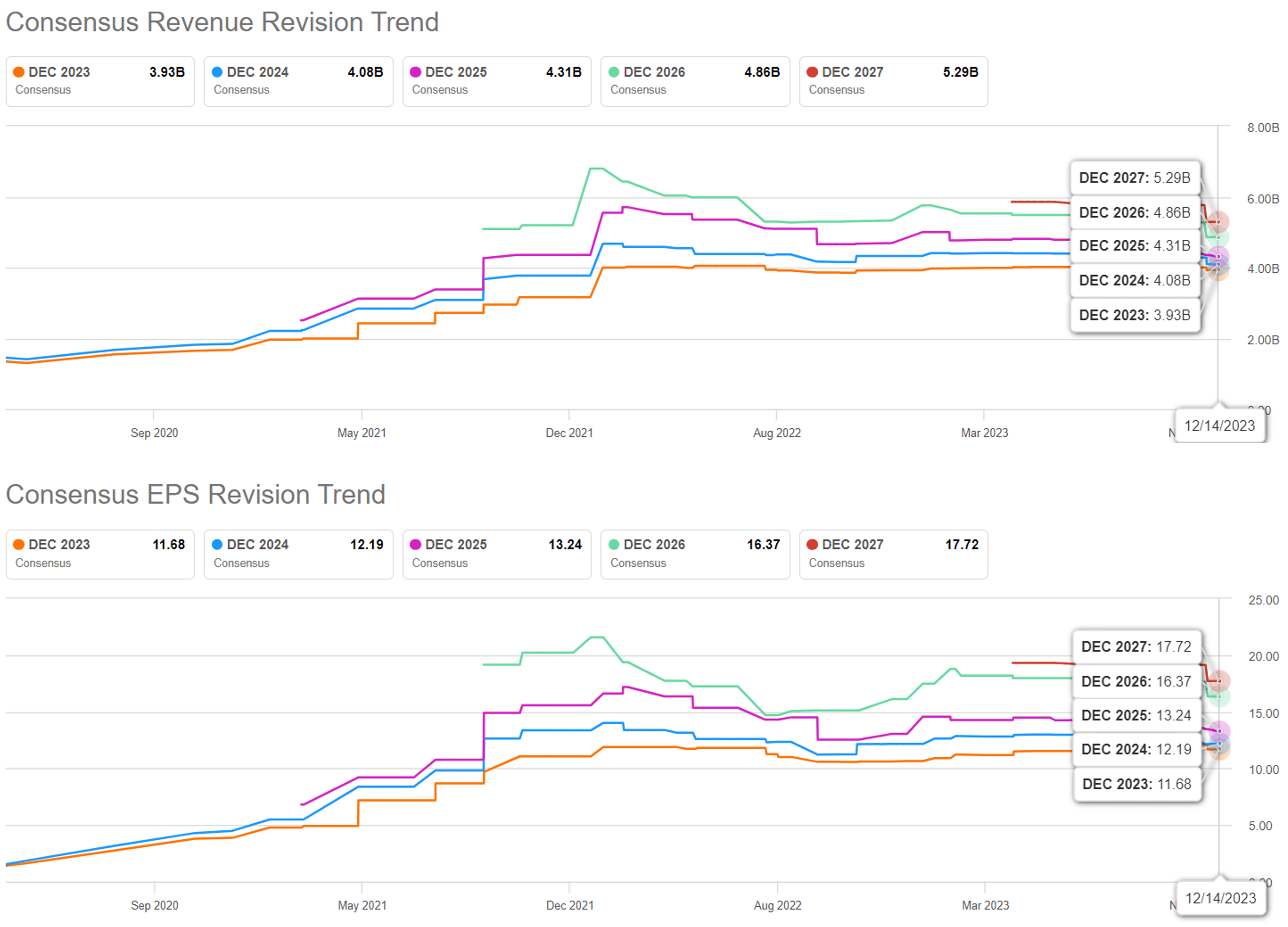

The Consensus Ahead Estimates

In search of Alpha

Nonetheless, the consensus has lowered the ahead estimates, with CROX anticipated to generate a prime and backside line CAGR of +6.6% and +6.6% by way of FY2025.

That is in comparison with the earlier estimates of +12.09%/ +10.09% and the historic CAGR of +22.8%/ +65.1% between FY2016 and FY2022, respectively.

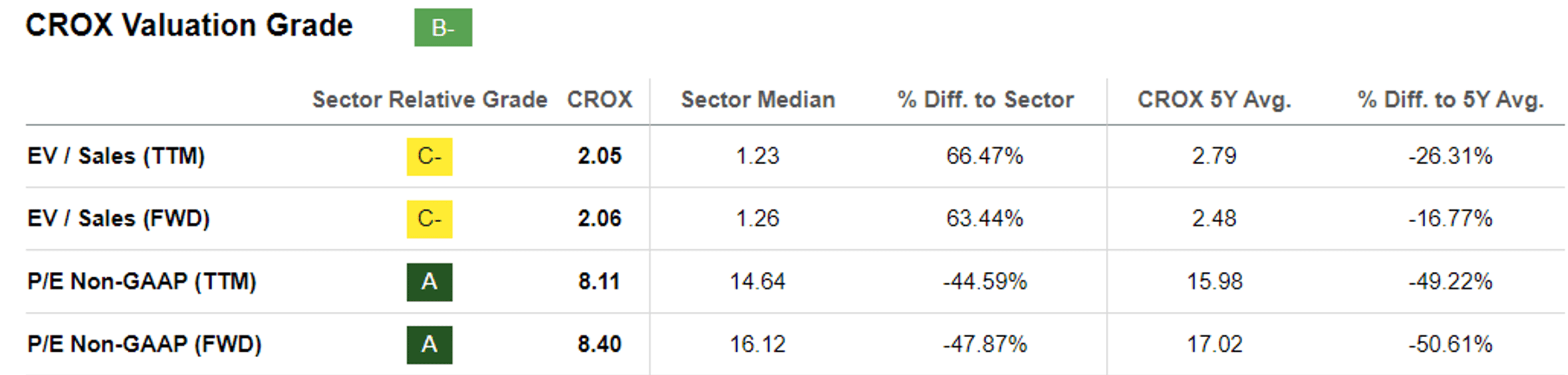

CROX Valuations

In search of Alpha

With HeyDude being prime and backside line dilutive, it’s unsurprising that CROX’s FWD EV/ Gross sales valuation of two.06x and FWD P/E of 8.40x have been additional discounted from its 1Y imply of two.24x/ 9.31x, pre-pandemic imply of 1.45x/ 31.47x, and the sector median of 1.26x/ 16.12x, respectively.

Based mostly on the administration’s FY2023 adj EPS steering of $11.70 on the midpoint and its impacted FWD P/E of 8.40x, the inventory seems to be buying and selling close to its truthful worth of $98.20.

Based mostly on the consensus FY2025 adj EPS estimates of $13.24, there appears to be a minimal upside potential of +13.2% to our long-term value goal of $111.20 as effectively.

With CROX now not providing a compelling development story and no dividends to stay up for, we consider that the inventory might at finest commerce sideways forward, till HeyDude is ready to generate convincing development in gross sales.

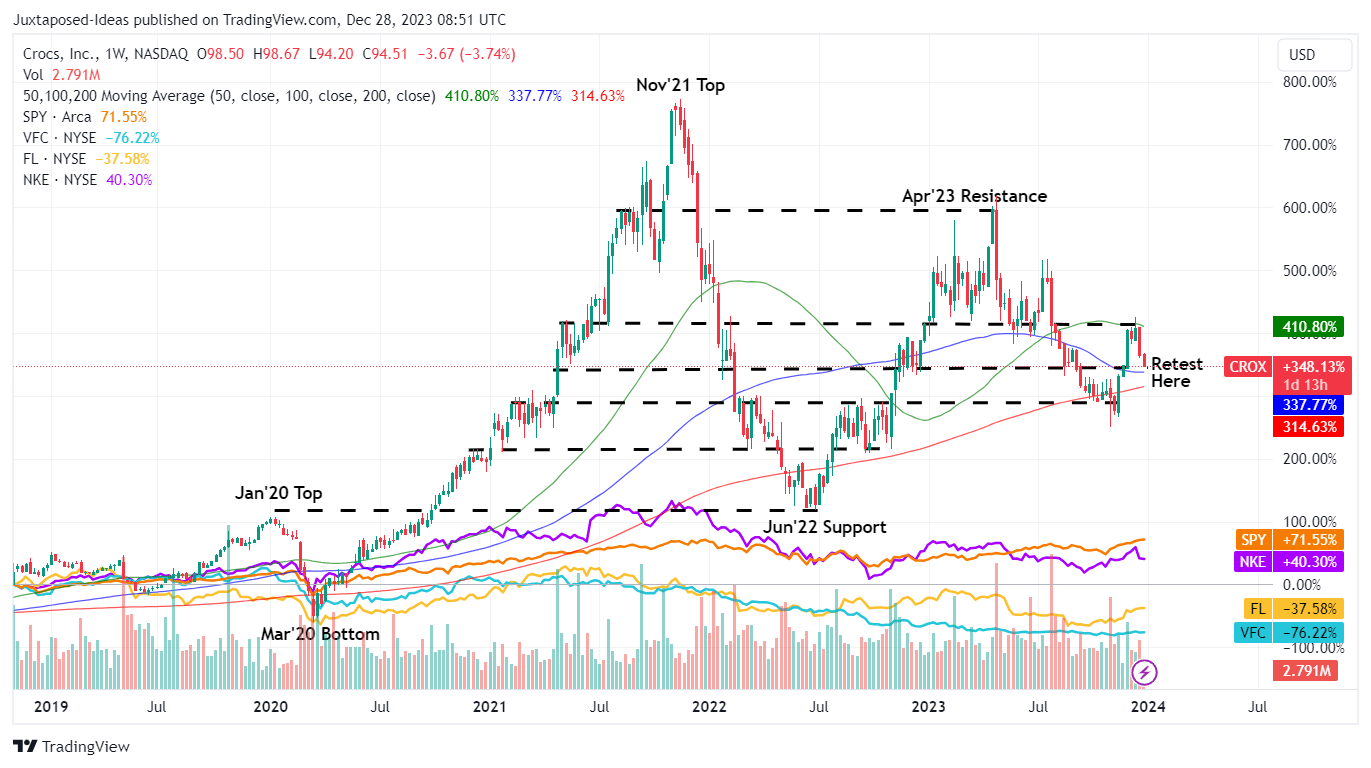

So, Is CROX Inventory A Purchase, Promote, or Maintain?

CROX 5Y Inventory Worth

Buying and selling View

For now, CROX has been lifted optimistically from the November 2023 backside, due to the cooling inflation, sturdy labor market, and the elevated probability of a Fed pivot in Q1’24, with an analogous restoration noticed market vast.

Nonetheless, it’s also obvious that shopper discretionary spending stays tight, with Nike (NKE) already warning “higher promotional activities to counter the slowing gross sales in North America,” implying impacted margins forward.

Most significantly, NKE already studies decelerating development for FQ2’24 footwear sales at $8.6B (+2.2% QoQ/ +1.2% YoY), in comparison with $8.5B a yr in the past (+4.8% QoQ/ +25.3% YoY).

Whereas CROX has been capable of report rising Crocs gross sales within the North American area at $480.7M (+1.2% QoQ/ +7.9% YoY), it seems that Mr. Market prefers to be cautious for now, with a number of footwear shares already plunging in sympathy since NKE’s newest earnings name on December 21, 2023.

On account of its obvious development (and probably backside line) headwinds as mentioned above, we favor to proceed score CROX as a Maintain right here, with the pessimistic sentiments prone to set off the inventory’s subsequent retracement to the earlier assist ranges of $85s, implying a painful -13% draw back from present ranges.

![The Power of Nostalgia in Social Media Marketing [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/06/bG9jYWw6Ly8vZGl2ZWltYWdlL3NvY2lhbF9ub3N0YWxnaWExLnBuZw.webp.webp)