John M Lund Pictures Inc

CrowdStrike’s (NASDAQ:CRWD) dominance in endpoint safety and adjoining markets is changing into extra obvious over time. Whereas many cybersecurity firms face an ongoing slowdown, CrowdStrike’s progress seems to be stabilizing at a fairly excessive charge given the corporate’s dimension, a notion that’s supported by sturdy hiring and fairly aggressive long-term monetary targets. CrowdStrike is leaning into the present scenario, suggesting that lots of its opponents are struggling as a result of they’ve flawed merchandise.

That is all extraordinarily constructive, however it’s troublesome to get excited in regards to the inventory at present costs. CrowdStrike is already a big firm, and it’s maturing, leaving a much smaller progress runway than existed a number of years in the past. The inventory can in all probability nonetheless outperform the market from present ranges over an extended timeframe however there’s a excessive likelihood of larger than a 50% drawdown in the occasion of macro weak spot or a shift in narrative.

I suggested that CrowdStrike’s valuation was starting to look stretched in January. The share worth has moved increased since then, though has been pretty flat for the reason that fourth quarter earnings name.

Market Situations

Whereas deal scrutiny stays elevated, CrowdStrike has stated that the macro surroundings has been steady in current quarters. It is a sentiment broadly shared throughout cybersecurity friends. Whereas finish market publicity varies throughout firms, and will account for variations in outlook, CrowdStrike at the moment seems as bullish as anybody.

That is supported by a risk panorama that continues to evolve and expose clients to a larger selection and quantity of threats. Primarily based on inside analysis, CrowdStrike believes that assaults have gotten sooner. The cloud can also be changing into a bigger goal, with CrowdStrike observing a 75% improve in cloud intrusion makes an attempt over the previous 12 months. Generative AI is one other adverse improvement, growing the amount of assaults and enabling extra individuals to perpetrate assaults.

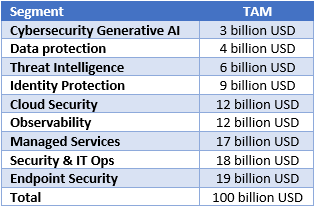

The sophistication and quantity of cyberattacks, together with issues like SEC reporting necessities, are creating demand for added instruments, supporting progress of the market. CrowdStrike expects its addressable market to develop to 225 billion USD by 2028. Of notice is how a lot of CrowdStrike’s addressable market now lies outdoors of its core endpoint and SecOps markets.

Desk 1: CrowdStrike Estimated TAM (supply: Created by writer utilizing knowledge from CrowdStrike)

Not solely does the chance proceed to develop, CrowdStrike’s aggressive place additionally seems to be strengthening. CrowdStrike has characterised most opponents as level merchandise that go away clients attempting to create a viable answer from stitched collectively items or “platforms” which can be actually a bundle of unintegrated options. Each of which might result in excessive prices and poor outcomes, one thing that CrowdStrike has steered is the actual purpose for buyer spending fatigue.

CrowdStrike’s aggressive place is demonstrated by its excessive progress, low churn and steady premium pricing. CrowdStrike believes it might probably maintain premium pricing because it nonetheless supplies clients with a decrease complete value of possession.

CrowdStrike Enterprise Updates

CrowdStrike’s enterprise relies round a single light-weight agent that’s straightforward to deploy and doesn’t require a reboot when put in. That is vital because it permits CrowdStrike to simply rollout extra options and absolutely leverage the info its giant endpoint footprint provides it. The endpoint market nonetheless presents CrowdStrike a big progress alternative as an estimated 50% of the market remains to be utilizing legacy AV.

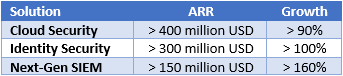

Growth into adjoining verticals is more and more vital to CrowdStrike’s progress although, and that is an space that the corporate is having monumental success. CrowdStrike’s cloud, identification and LogScale companies now have ARR in extra of 850 million USD.

Desk 3: CrowdStrike ARR by Answer (supply: Created by writer utilizing knowledge from CrowdStrike)

CrowdStrike just lately added Information Safety Posture Administration to its cloud safety enterprise by means of the acquisition of Flow Security. Circulate presents a cloud knowledge runtime answer which supplies steady and real-time knowledge visibility for each knowledge at relaxation and knowledge in movement. One thing that’s changing into more and more vital with the rise of LLMs.

Prospects desire a holistic cloud safety answer that may defend in opposition to real-time threats and CrowdStrike can present this by means of its single agent and agentless answer. CrowdStrike’s cloud safety providing now contains identification, software safety posture administration, workload safety and cloud knowledge safety.

CrowdStrike’s SIEM enterprise can also be starting to takeoff, with LogScale ARR growing 170% YoY within the fourth quarter. Over 1,000 clients are utilizing the product, which is a small determine relative to CrowdStrike’s 20,000+ complete clients. CrowdStrike believes it has entry to round 85% of the core data that goes right into a SIEM, which coupled with index free ingestion, creates a compelling answer. CrowdStrike, SentinelOne (S) and Elastic (ESTC) have all steered that clients are abandoning legacy SIEMs.

CrowdStrike’s identification safety enterprise surpassed 300 million USD ARR within the fourth quarter, greater than doubling YoY. Nearly all of assaults contain identification vectors, making identification safety a important a part of any cybersecurity platform. CrowdStrike has steered that friends both lack an identification safety answer or supply it as a non-integrated characteristic.

Falcon for IT has simply been made usually accessible. This product goals to unify IT and SecOps, changing legacy merchandise with CrowdStrike’s single-agent structure.

Charlotte AI can also be now usually accessible, though I do not imagine the product shall be significantly impactful. Charlotte AI will not present significant income as CrowdStrike seems to be pricing it for ubiquity. Over 80% of beta customers imagine that Charlotte will save them time, which might assist make CrowdStrike’s platform stickier. Most cybersecurity firms plan on providing comparable merchandise although and it isn’t clear any of them could have a bonus.

Monetary Evaluation

CrowdStrike’s income elevated 33% YoY within the fourth quarter to 845 million USD. Subscription income grew 33% and Skilled providers income was up 26%. ARR was 3.44 billion USD in This fall, up 34% YoY, and CrowdStrike delivered web new ARR of 282 million USD, a 27% YoY improve.

Buyer progress stays stable, with CrowdStrike now having 29,000 subscription clients. Buyer progress continues to reasonable although, pointing the best way to a decrease progress future. It’s value noting that CrowdStrike is now making larger use of MSSPs and SMBs served by means of these companions don’t present up within the buyer rely. CrowdStrike’s MSSP enterprise grew triple digits YoY within the fourth quarter.

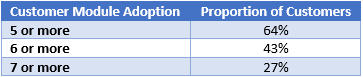

Prospects proceed to land bigger, initially adopting 4.9 modules on common. CrowdStrike’s dollar-based web retention charge was 119% within the fourth quarter, partly as a result of firm touchdown larger offers. This determine remains to be comparatively excessive although and demonstrates the success that CrowdStrike is having driving consolidation on its platform.

Desk 2: Buyer Module Adoption (supply: Created by writer utilizing knowledge from CrowdStrike)

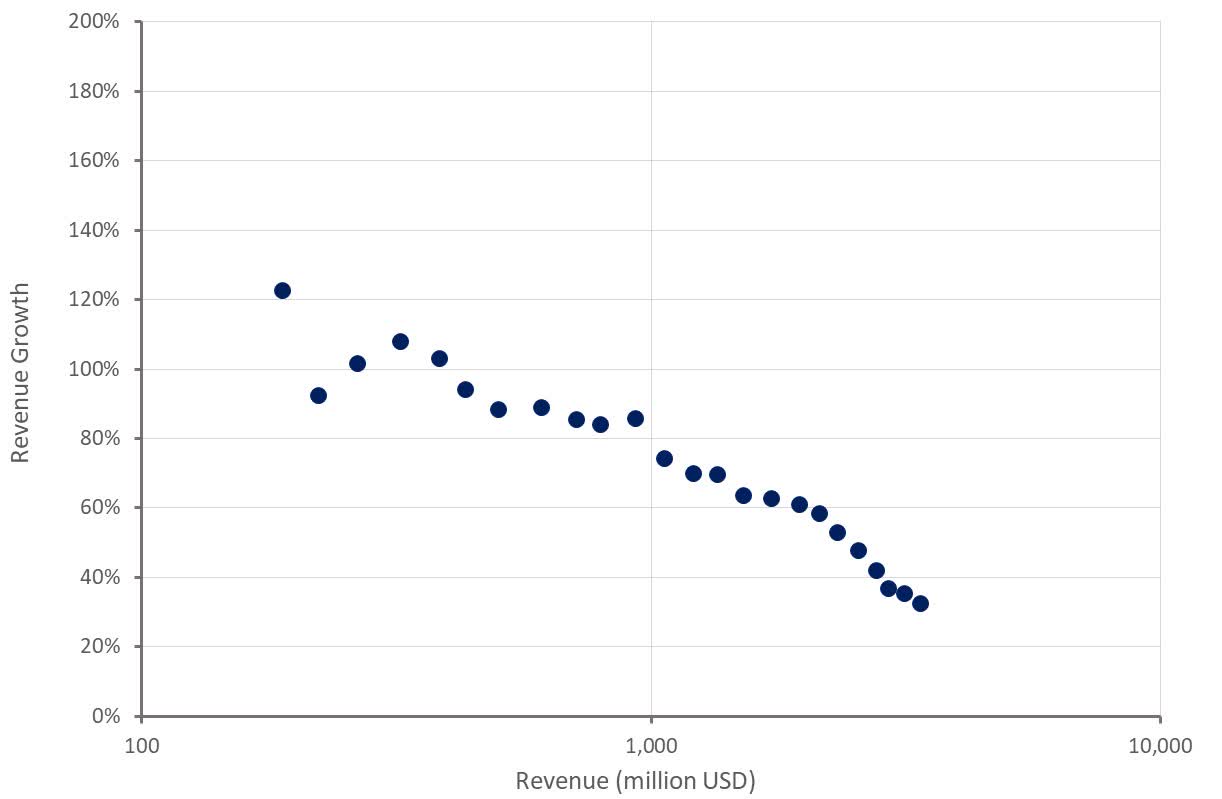

CrowdStrike anticipates roughly 30% YoY income progress within the first quarter of FY2025 and 28-31% progress for the complete 12 months. The corporate can also be concentrating on 10 billion USD ARR inside the subsequent 5 to seven years (16-23% progress). Whereas that is in all probability a extremely conservative public goal, it does show the course CrowdStrike’s progress goes as the corporate matures.

Determine 1: CrowdStrike Income Development (supply: Created by writer utilizing knowledge from CrowdStrike)

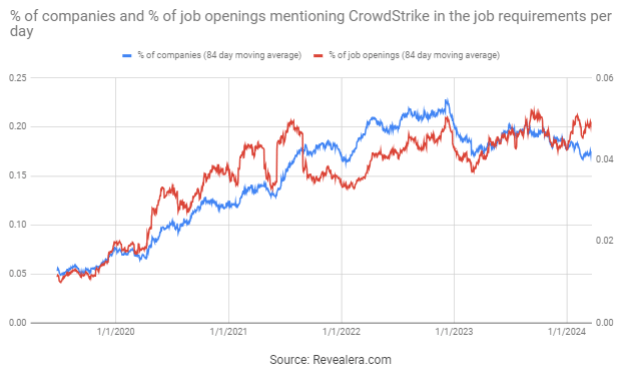

The variety of job openings mentioning CrowdStrike within the job necessities has been pretty steady over the previous 12 months. There’s little to point a progress reacceleration at this stage however steady demand within the present surroundings is a constructive.

Determine 2: Job Openings Mentioning CrowdStrike within the Job Necessities (supply: Revealera.com)

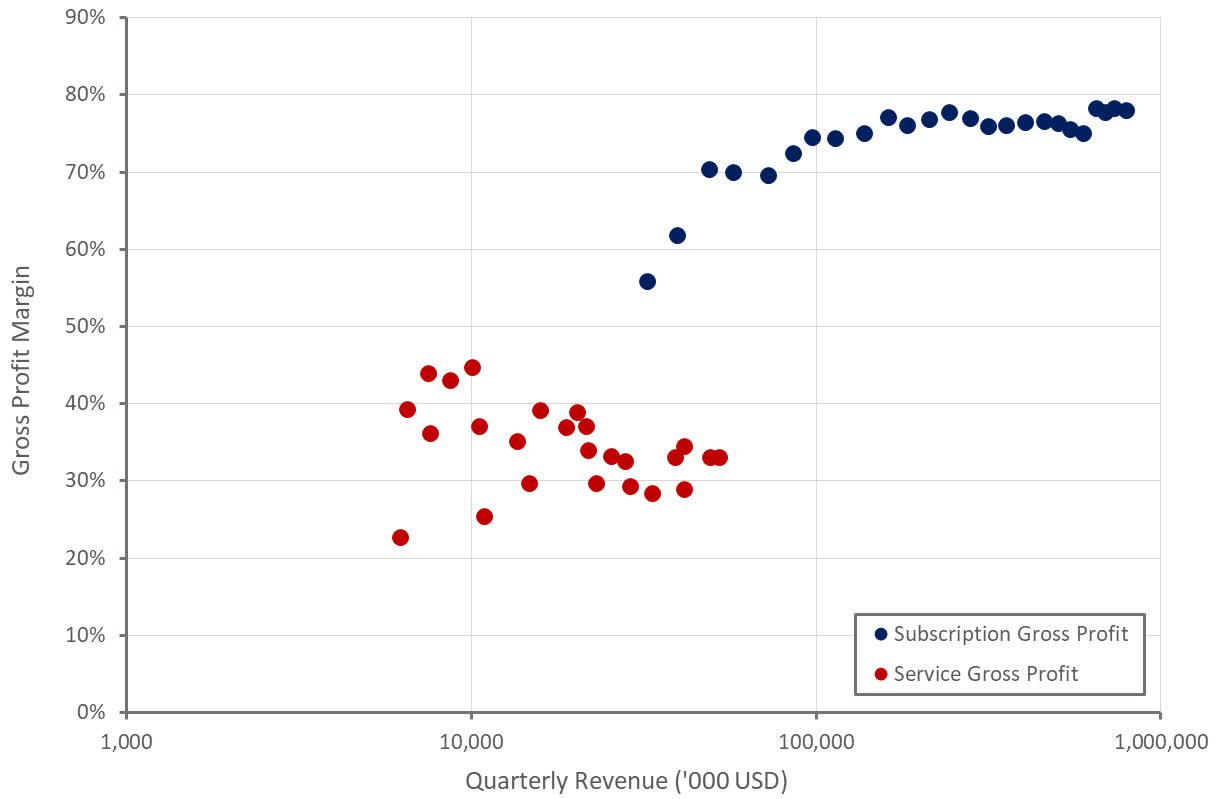

Subscription and repair gross revenue margins have been each stable within the fourth quarter, with CrowdStrike persevering with to profit from scale and economies of scope.

Whereas it usually goes neglected, CrowdStrike’s providers are a reputable enterprise in their very own proper. Many firms use providers as a stealth buyer acquisition software and therefore have low and even adverse gross margins on their providers.

Determine 3: CrowdStrike Gross Revenue Margins (supply: Created by writer utilizing knowledge from CrowdStrike)

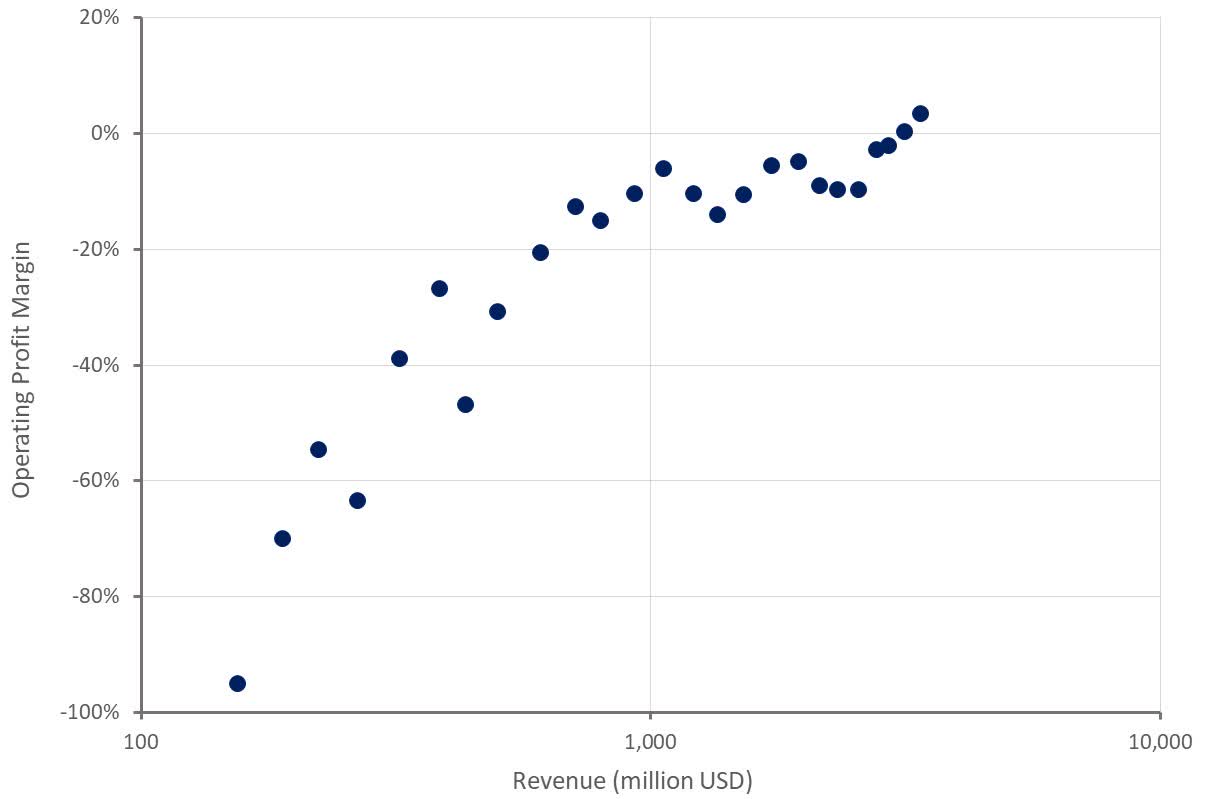

CrowdStrike’s working revenue margin additionally proceed to enhance, which is spectacular on condition that CrowdStrike remains to be investing in progress. Two years in the past CrowdStrike’s goal working revenue margin was solely 20-22%, a determine that has now elevated to 28-32%. I’ve lengthy steered that CrowdStrike could be extremely worthwhile because the enterprise matures and nonetheless assume the corporate is on observe for one thing like a 30-35% working revenue margin.

Determine 4: CrowdStrike Working Revenue Margins (supply: Created by writer utilizing knowledge from CrowdStrike)

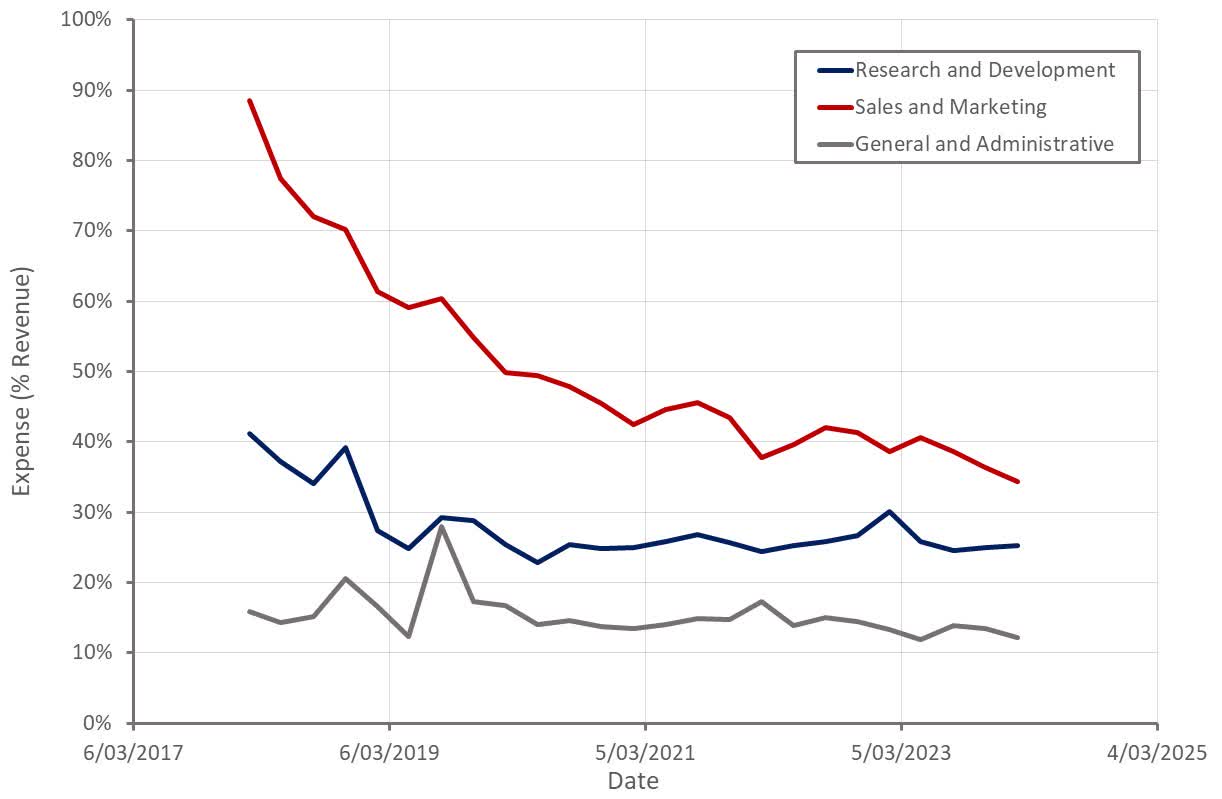

Working profitability features are being pushed by gross sales and advertising and marketing bills. CrowdStrike’s gross retention charge has been constant at round 98%, which ought to see the burden of gross sales and advertising and marketing bills proceed to say no as the corporate matures.

CrowdStrike remains to be investing aggressively in R&D, which is cheap given the dimensions of the chance and CrowdStrike’s effectivity.

Determine 5: CrowdStrike Working Bills (supply: Created by writer utilizing knowledge from CrowdStrike)

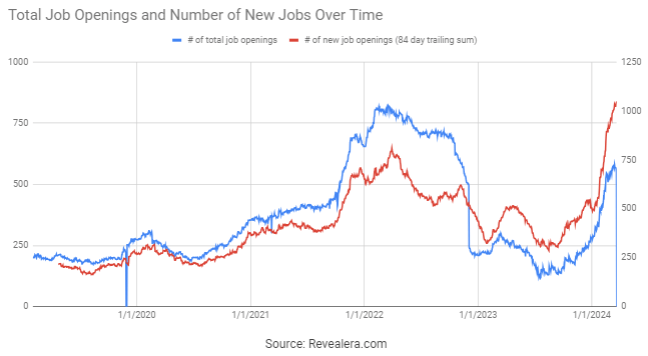

The variety of CrowdStrike job openings has elevated dramatically in current months. This stands in stark distinction to most different software program firms, who proceed to rent at a reasonably modest tempo. This would appear to point expectations of an imminent progress reacceleration, though hiring might start to weigh on enhancements in profitability.

Determine 6: CrowdStrike Job Openings (supply: Revealera.com)

Conclusion

Whereas CrowdStrike’s inventory is now buying and selling on an elevated income a number of once more, I imagine most buyers nonetheless do not absolutely admire the extent to which CrowdStrike goes to be one of many dominant software program platforms sooner or later. The cybersecurity alternative is giant and continues to develop, offering CrowdStrike with a protracted progress runway. On an extended time-frame, I count on CrowdStrike to maneuver past safety, additional increasing its market. The inventory worth seems overextended within the near-term although and macro weak spot or a stumble by CrowdStrike might simply see the inventory full by greater than 50%.

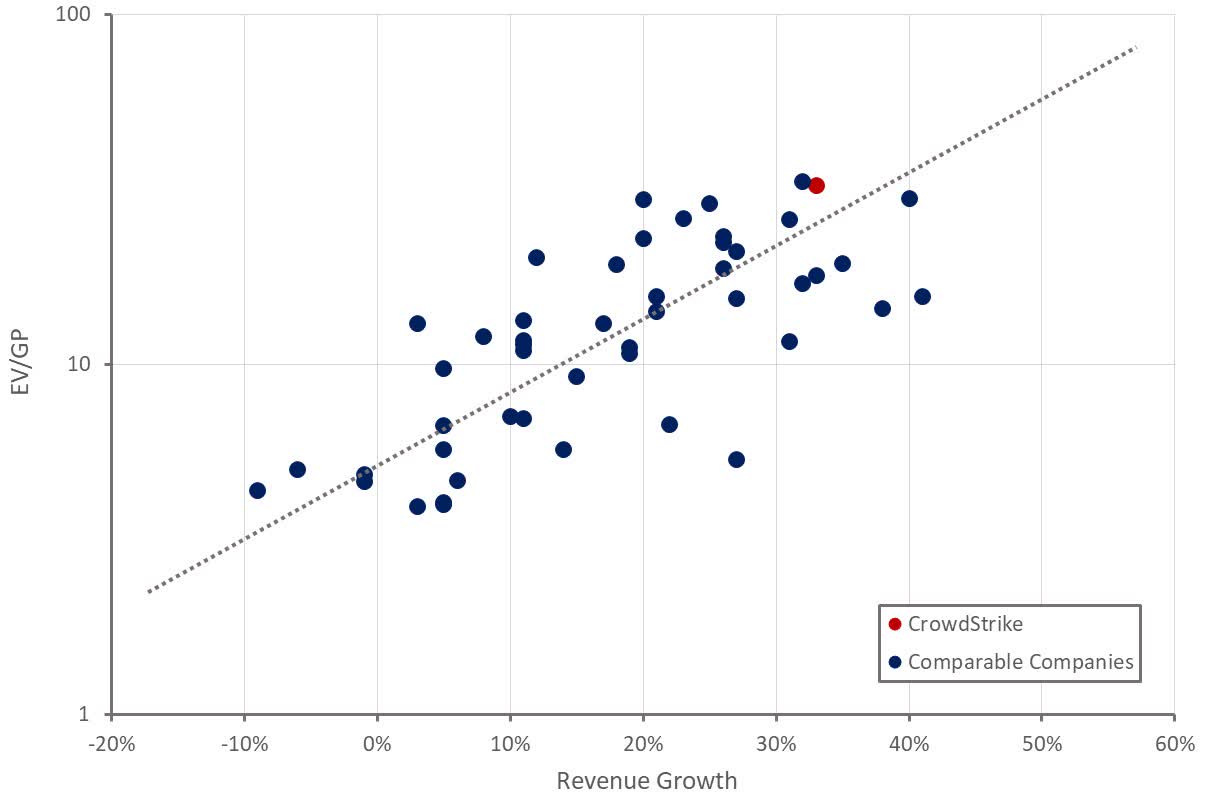

Determine 7: CrowdStrike Relative Valuation (supply: Created by writer utilizing knowledge from Searching for Alpha)