Robert Manner/iStock Editorial by way of Getty Photographs

CrowdStrike (NASDAQ:CRWD) is gearing up for accelerating business momentum in 2024, after a robust efficiency in 2023. Based on varied CIO surveys, IT budgets are set to develop in 2024, and inside IT, the demand for cybersecurity is anticipated to outpace the broader software program spent. On that observe, I agree with analysts {that a} 25% YoY topline development for CrowdStrike could also be cheap over the subsequent 4 quarters. This development is extremely priceless for traders, as CrowdStrike generates roughly 36 cents in free money movement for each greenback of incremental gross sales.

Regardless of these constructive fundamentals, traders shouldn’t neglect that each funding alternative can be a perform of valuation. And on valuation, CrowdStrike inventory seems overpriced, with CRWD shares trading at a 22x EV/ Gross sales and a 103x EV/EBIT (projected 2024 Gross sales and EBIT). Contemplating such aggressive valuation multiples, I doubt that CrowdStrike traders will obtain alpha-rich returns in 2024.

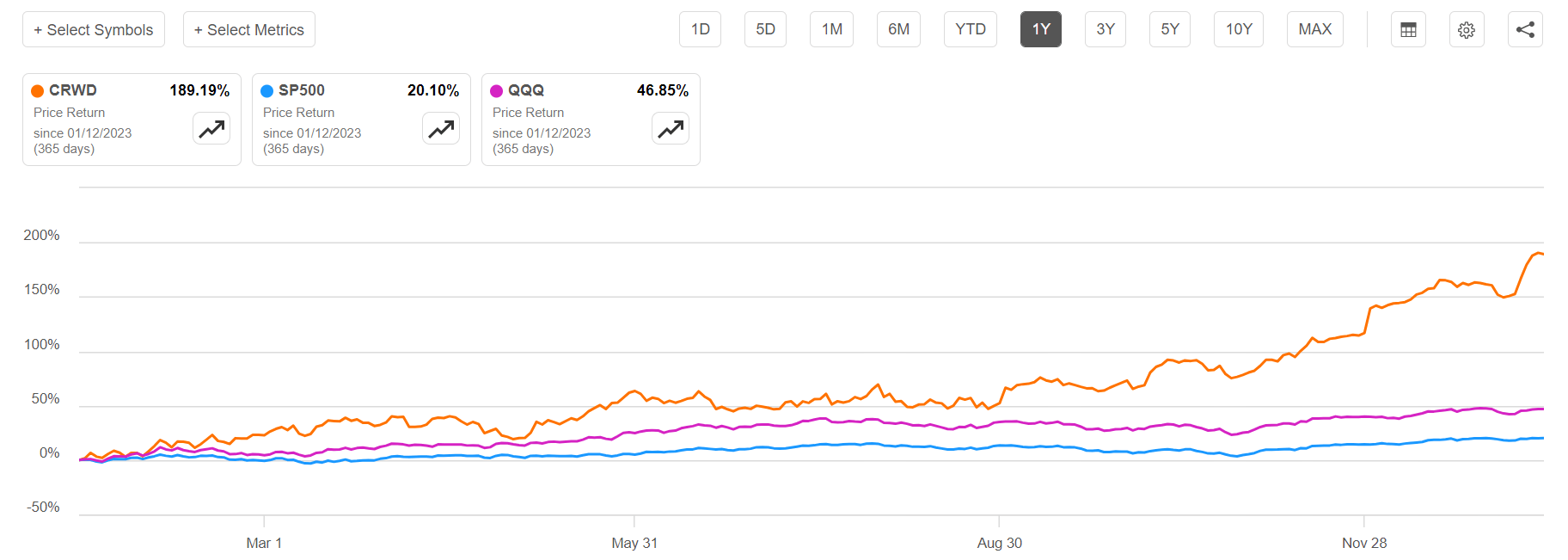

For context, CrowdStrike inventory has strongly outperformed the broad equities market in 2023, additionally when in comparison with the “Tech” benchmark. For the trailing twelve months, CRWD shares are up about 189%, in comparison with a achieve of roughly 20% for the S&P 500 (SP500) and a achieve of near 47% for the Nasdaq tech-heavy Nasdaq 100 (QQQ).

Searching for Alpha

Cybersecurity May Thrive in 2024’s Bull Market…

As we strategy 2024, the general outlook for IT budgets is exhibiting indicators of enchancment. This development is echoed within the insights gathered from varied Q3 convention talks, which highlighted a discount in gross sales cycles for brand spanking new purchasers and sooner billing processes for present ones. Such a shift is especially useful for cybersecurity investments, in my view, because the urgency for sturdy cyber protection mechanisms is escalating as a consequence of growing geopolitical tensions and the complicated safety challenges rising from GenAI developments, together with deep-fakes, knowledge poisoning, and adversarial assaults. In that context, Qualys reported a notable 26,447 disclosed vulnerabilities in 2023, surpassing 2022’s depend by over 1,500 and marking a seventh consecutive 12 months of rising vulnerabilities. Equally, ransomware assaults have been up 72% YoY in 2023 vs 2022, with hackers more and more using new GenAI instruments to develop malware at an accelerating tempo.

Aligned with the growing menace surroundings, the Piper Sandler 2024 CIO Survey (printed on December eleventh) presents a bullish perspective for cybersecurity spending, inserting safety spending on the high of IT funds decision-makers priorities. In that context, survey members place particular emphasis on areas like Cloud Safety, Endpoint Safety, Risk Intelligence, and Community Detection & Response – areas which can be strongly aligned with CrowdStrike’s experience. Equally, surveys carried out by UBS, Jefferies and Morgan Stanley underscore the anticipated enhance in cybersecurity budgets, pointing to the adoption of GenAI and its associated safety implications as key areas of concern.

…With Structural Progress Supporting Lengthy Time period Enlargement

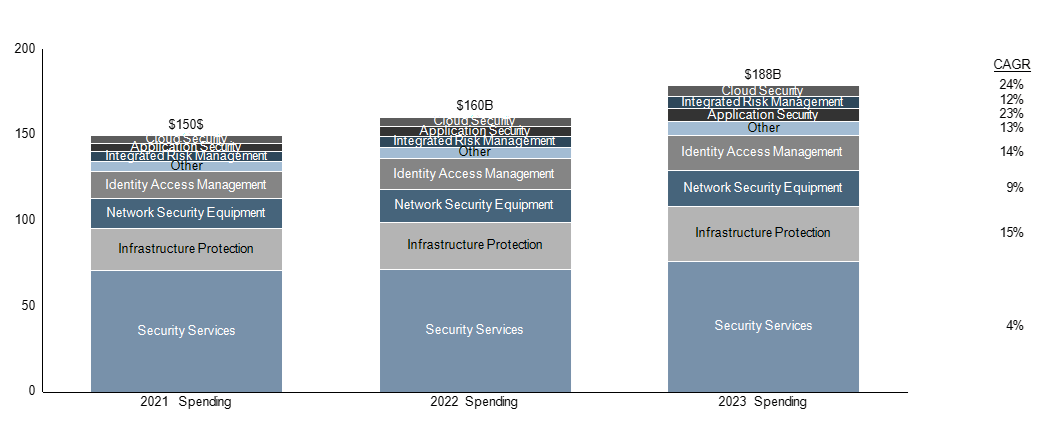

From a extra structural development perspective, traders ought to contemplate that the cybersecurity market continues to develop considerably. In actual fact, Gartner projected that the Complete Addressable Marketplace for the cybersecurity trade topped $188 billion in 2023, rising about 13% YoY. Furthermore, higher than double-digit YoY development charges are anticipated to persist via the subsequent 5 years, as cybersecurity is projected to say an more and more bigger share of general IT spending.

Gartner, Cavenagh analysis modelling

On that observe, I level out that CrowdStrike is strengthening its place of market management as a SaaS safety platform. The corporate has a robust monitor report of gaining market share throughout the core endpoint market, together with the growing adoption of its rising modules (akin to identification safety and cloud workload safety). As well as, CRWD’s ongoing technique to develop past endpoint safety, notably with LogScale’s integration that merges cybersecurity and infrastructure, is enhancing CRWD’s integration and engagement with its prospects.

On a special observe, CrowdStrike seems properly positioned to leverage AI, as I imagine that bigger platforms like CrowdStrike and Palo Alto stand to learn probably the most from AI developments. Traders ought to contemplate that getting access to in depth knowledge permits these firms to coach AI fashions extra effectively and permits for a complete view throughout varied segments of a buyer’s cybersecurity panorama. This functionality facilitates the correlation of information from completely different sources, akin to linking endpoint knowledge with identification knowledge.

Count on ~30% YoY Topline Progress In 2024 On Excessive FCF Margins

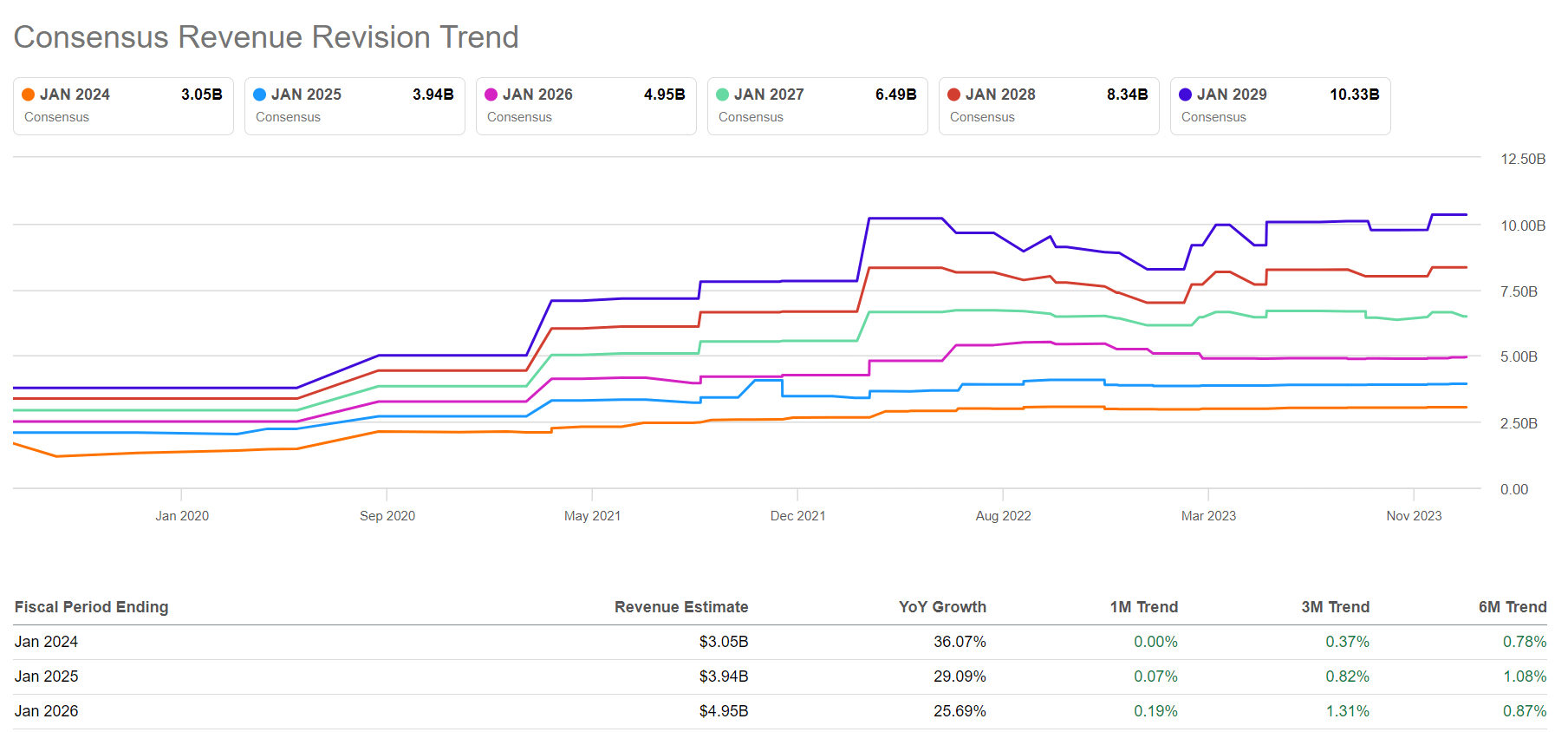

As mentioned in earlier sections of the article, CrowdStrike is properly positioned to seize a big share of the growing demand for cybersecurity in 2024 and past. In additional element, analyst consensus at the moment projects ~30% topline development in 2024, adopted by 25% development in 2025. I believe the estimated development, though excessive, needs to be an inexpensive benchmark for CrowdStrike’s income outlook.

Searching for Alpha

Reflecting on CrowdStrike’s development, traders ought to bear in mind the numerous worth that extra income brings to shareholders. For each greenback of incremental gross sales, CrowdStrike at the moment generates roughly 0.36 cents in free money movement. And because the firm beneficial properties scale, constructive working jaws might push the free money movement margin nearer to 40%.

If we assume that CrowdStrike grows its income to $5 billion by finish of 2025, as estimated by consensus, and apply a 40% free money movement margin, then we might moderately mission CrowdStrike’s 2025 FCF at about $2 billion. Benchmarked towards the corporate’s market capitalization of about $70 billion, the implied ahead P/FCF is a proud 35x.

Investor Takeaway

CrowdStrike is predicted to seize a considerable share of the booming demand for cybersecurity, with analyst consensus projecting a sturdy ~30% YoY topline development in 2024 and 25% in 2025. Regardless of these constructive development indicators and CrowdStrike’s spectacular free money movement margin – producing roughly 36 cents for each greenback of incremental gross sales – the corporate’s valuation at 22x EV/ Gross sales and a 103x EV/EBIT raises issues. As a perform of each business momentum and valuation, I assign a Maintain suggestion.