SmileStudioAP

CyberArk (NASDAQ:CYBR) is a Privileged Entry Administration centered identification safety vendor. The corporate has had a troublesome multi-year interval because of its transition to a subscription enterprise mannequin however is now starting to flourish. Identification continues to be central to trendy cybersecurity and CyberArk’s place as a number one PAM vendor positions it to capitalize on this.

The market has been gradual to acknowledge the standard of CyberArk’s enterprise, resulting in continual undervaluation. I fall into this camp as I’ve needed publicity to the identification administration marketplace for some time and have at all times felt that Okta (OKTA) was one of the best alternative. I by no means invested in Okta although as a result of I’ve by no means felt snug with the problems the corporate has been having (gross sales and safety). I’ve previously written about CyberArk, and whereas I’ve acknowledged that it’s a stable firm, I wasn’t certain concerning the risk from Okta increasing into PAM. It more and more seems like CyberArk is greater than outfitted to thrive as unified identification platforms turn into the norm although.

Even with the current value run up, CyberArk’s income a number of has room to extend additional, supported by bettering margins and accelerating progress. The mix of stable progress and a steady/rising income a number of ought to see CyberArk’s inventory proceed to carry out effectively going ahead.

Market

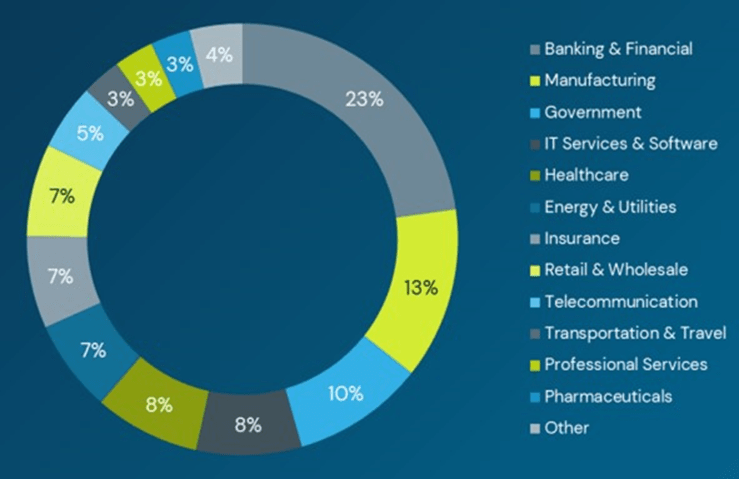

Macro circumstances stay troublesome for CyberArk, however that is one thing that the corporate isn’t actually speaking about, because it does not have to attempt to excuse its efficiency. Cybersecurity is a precedence for purchasers, and inside cybersecurity, identification is being given priority. Because of this, CyberArk witnessed increased demand for its platform in 2023. CyberArk’s enterprise can also be probably being supported by its finish market publicity.

Determine 1: CyberArk ARR by Vertical (supply: CyberArk)

Identification stays a essential assault vector and the proliferation of recent identities, new environments and new assault strategies is supporting demand. For instance, CrowdStrike (CRWD) has prompt that roughly 80% of attacks exploit identity-based vectors.

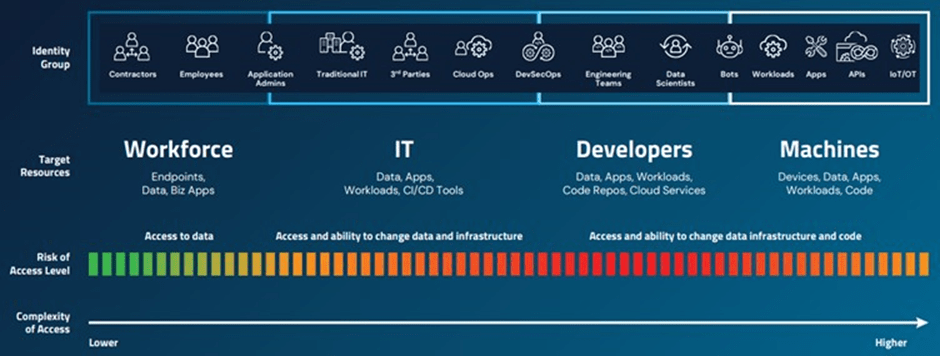

CyberArk believes that completely different ranges of management are wanted to handle the danger of identities with various ranges of danger and complexity. To the extent that that is true, the significance of PAM is prone to rise time beyond regulation, enabling CyberArk to capitalize on its estimated 50 billion USD addressable market.

Determine 2: Spectrum of Secured Identities (supply: CyberArk)

CyberArk

Inside identification safety, there’s a pattern in direction of the creation of unified platforms that present IAM, PAM and IGA. CyberArk is primarily a PAM vendor, that means that it tries to make sure that each identification (human and machine) is secured with the precise degree of privilege controls.

CyberArk believes {that a} siloed method to IAM, PAM and IGA is suboptimal from a safety perspective and in consequence is including to its identification administration options. CyberArk needs all of its options to have elements of governance, entry and privileged management. Whereas CyberArk plans on persevering with to spend money on IGA, it doesn’t look like absolutely pursuing the IGA alternative within the near-term. The corporate has said that if clients have to do a large-scale IGA deployment throughout environments, its partnership with SailPoint is a viable resolution.

Whereas MFA and SSO are necessary, CyberArk believes that they’re now not adequate. Because of this, CyberArk is making an attempt to reinvent workforce identification by leveraging privileged controls and including options like Safe Internet Classes, Workforce Password Supervisor, and CyberArk Safe Browser on high of MFA and SSO.

- Safe Internet Classes present safety by enabling steady authentication and delivering visibility into the actions taken by customers inside net functions.

- Workforce Password Supervisor helps clients to securely retailer, handle and share enterprise software credentials.

- CyberArk’s Safe Browser helps clients shield towards cookie harvesting and browser-based assaults. It’s constructed with native integrations to CyberArk’s workforce capabilities and offers a gateway to all of CyberArk’s options.

CyberArk’s Endpoint Privilege Supervisor resolution removes native admin rights and enforces least privilege on endpoints. This helps to defend towards ransomware and cease credential theft. Whereas EPM has seen stable progress over the previous few years, CyberArk believes that there’s nonetheless a big alternative to cross-sell EPM throughout its put in base.

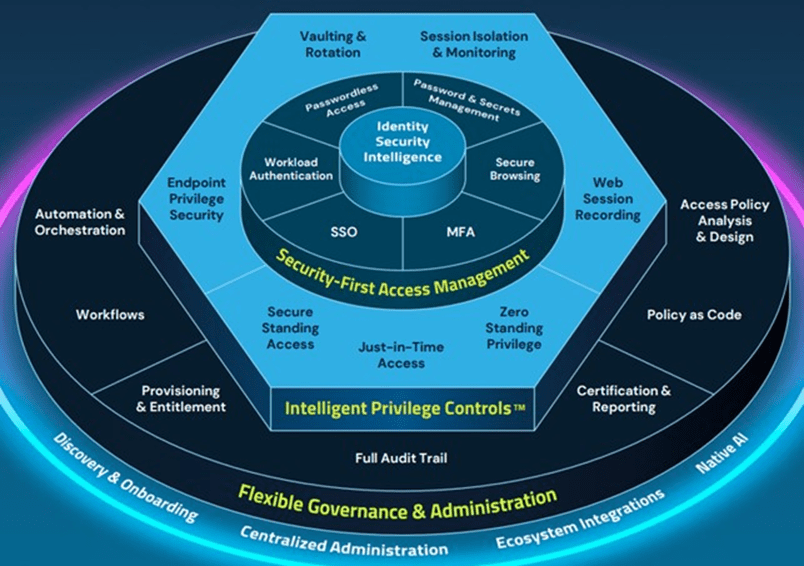

Determine 3: CyberArk Identification Safety Platform (supply: CyberArk)

CyberArk believes that the speedy shift to the cloud has led to inadequate entry management. CyberArk’s Safe Cloud Entry resolution brings privileged controls to the cloud, serving to CyberArk to handle builders, knowledge scientists and engineering groups. SCA is considered one of CyberArk’s latest choices, however it’s reportedly performing well.

When it comes to identities, builders are a excessive progress space and are additionally driving the rise in machine identities. CyberArk’s Conjur Cloud Secrets and techniques Supervisor helps to guard these machines whereas avoiding vault sprawl. Secrets and techniques Supervisor was part of six of CyberArk’s top ten deals in the course of the fourth quarter.

CyberArk thinks managing all customers in the identical means as extremely privileged customers offers it with differentiation. Because of this, the corporate believes that its competitive positioning has never been better. Competitors varies throughout merchandise although. For instance, there’s usually present competitors in entry administration, whereas EPM is extra of a greenfield alternative. Within the secrets and techniques area, CyberArk is competing with a variety of instruments, together with open-source and hyperscaler native secret shops.

Monetary Evaluation

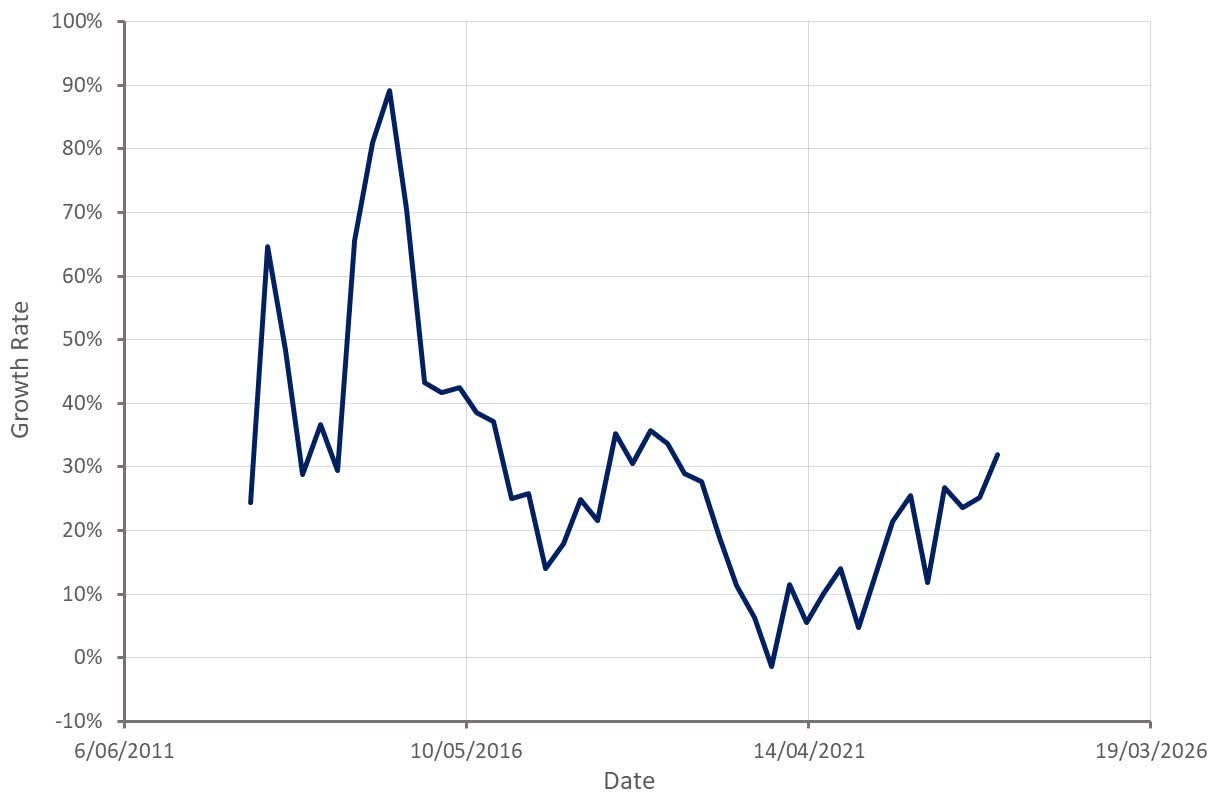

CyberArk’s income increased 32% YoY to 223 million USD within the fourth quarter. Development was stable throughout areas, with the Americas rising 31% YoY, EMEA rising 33% and APJ rising 35%.

Because of CyberArk’s enterprise mannequin transition, ARR and subscription ARR progress are each outpacing income progress. Perpetual license income has largely been eradicated over the previous few years, resulting in speedy subscription progress (self-hosted and SaaS). This course of is basically full now as over 95% of CyberArk’s bookings are coming from subscriptions.

CyberArk is guiding 209-215 million USD income within the first quarter, a rise of 29-33% YoY. For the complete yr 2024, CyberArk is guiding 920-930 million USD income, representing 22-24% progress.

Determine 4: CyberArk Income Development (supply: Created by writer utilizing knowledge from CyberArk)

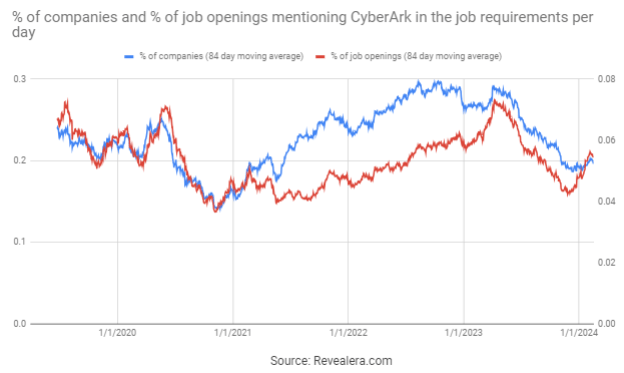

The variety of job openings mentioning CyberArk within the job necessities eased within the second half of 2023. This might be indicative of decreased demand, however there was no impression on CyberArk’s enterprise to date.

CyberArk signed round 340 new logos within the fourth quarter, with new logos more and more touchdown with two or extra options. CyberArk additionally now has over 1,700 clients with ARR in extra of 100,000 USD, a rise of 30% YoY. The cohort of consumers with greater than 500,000 USD ARR elevated by greater than 45%, to round 300.

This sturdy progress in bigger clients is being pushed by cross-selling and up-selling. The platform method helps to safe CyberArk’s aggressive place and may result in decreased churn and higher income per buyer over time, which is able to finally result in improved margins.

Determine 5: Job Openings Mentioning CyberArk within the Job Necessities (supply: Revealera.com)

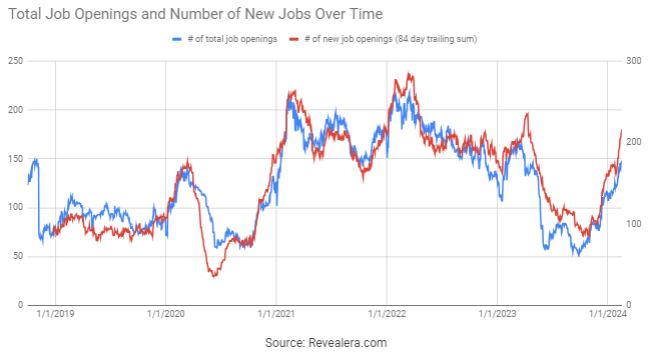

The variety of CyberArk job openings has elevated quickly in current months, which means that the corporate expects demand to stay sturdy in 2024.

Determine 6: CyberArk Job Openings (supply: Revealera.com)

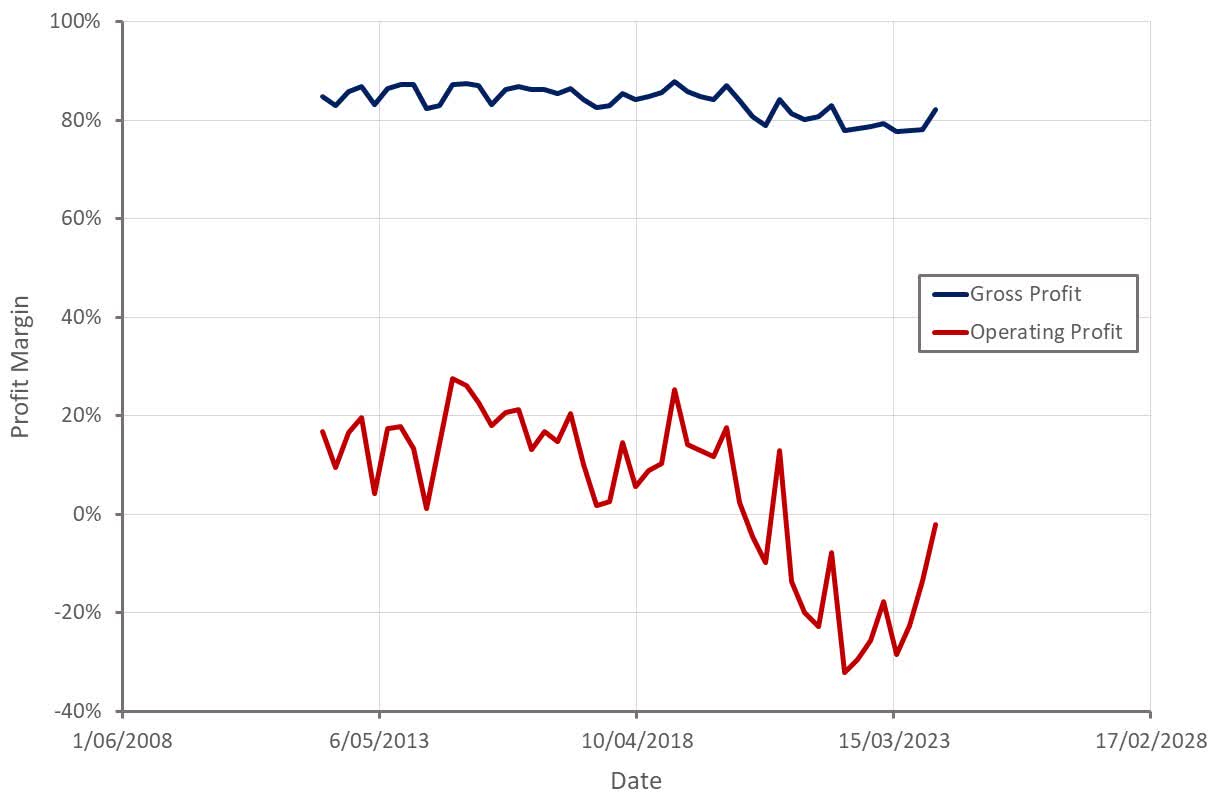

CyberArk’s margins are bettering quickly as its enterprise mannequin transition matures, and this course of is prone to proceed going ahead. Clients adopting extra merchandise is supportive of margins and CyberArk is but to succeed in the purpose the place it has a big base of renewing subscription clients. This could scale back the burden of gross sales and advertising and marketing bills, resulting in additional enchancment in profitability.

Determine 7: CyberArk Revenue Margins (supply: Created by writer utilizing knowledge from CyberArk)

Conclusion

Whereas CyberArk’s income a number of has moved greater in current months, I consider that is justified by quite a few elements:

- CyberArk’s increasing portfolio of options

- Accelerating progress because the enterprise mannequin transition matures

- An imminent return to GAAP profitability

- Better proportion of recurring income

- Strengthening aggressive place

I’d not essentially depend on CyberArk’s income a number of increasing additional, however the inventory ought to proceed to carry out effectively with a steady a number of and continued sturdy income progress.

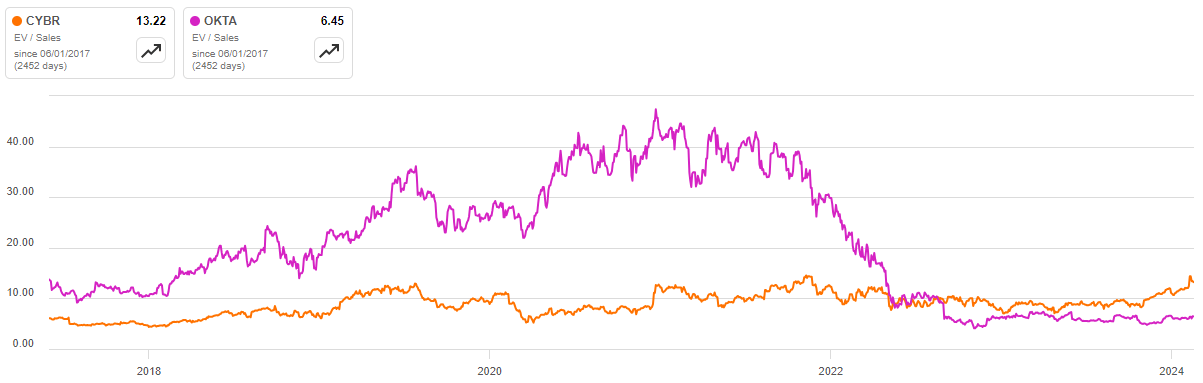

Determine 8: CyberArk EV/S A number of (supply: Searching for Alpha)