Peggy Cheung

Datadog (NASDAQ:DDOG) reported their 4Q23 earnings outcomes, the place each prime and backside line beat expectations.

I additionally discovered administration commentary and tone constructive, whereas the corporate continued to execute properly on the R&D entrance with many new options and capabilities launched within the yr, together with sturdy execution on the gross sales and advertising entrance with momentum within the go-to-market persevering with within the quarter.

That stated, administration did launch steerage for 2024 that was weaker than anticipated, particularly after the sturdy outcomes that got here out for 4Q23.

I do assume that there’s a probability that the staff is being conservative in its 2024 steerage given what we have now seen.

I’ve written extensively about Datadog on In search of Alpha, and in my last article, I had a Purchase score on the corporate given the extra interesting valuation after the earnings plunge. I proceed to offer Datadog a Purchase score, as I’ve defined briefly above, and extra particulars within the sections to return.

A robust 4Q23

There is no denying this.

Datadog’s 4Q23 have been forward of expectations on a number of fronts.

Income got here in at $589.6 million, up 26% from the prior yr. This was forward of consensus expectations by about 4 proportion factors.

Working revenue got here in at $166.6 million or 28.3% working margins. This was forward of consensus by 26%.

Curiously, Datadog has exceeded the steerage by a bigger margin in 4Q23 than within the first half of 2023, just like what we noticed in 3Q23.

For reference, Datadog exceeded the steerage by 2.9% in 1Q23, 2.0% in 2Q23, 4.8% in 3Q23 and 4.3% in 4Q23.

Whole RPO grew 26.9% sequentially to $1,840 million, which was the strongest sequential development we noticed prior to now two years.

Clearly, we’re seeing an inflection level within the making.

Datadog shared that they’re seeing continued utilization development from current clients contribute to the sturdy efficiency in 4Q23, which was what they noticed in 3Q23 as properly.

Additionally, administration additionally famous a constructive pattern on optimization as they observed that the depth of optimization seen within the final six quarters appear to have declined and in reality, they’re beginning to see giant optimizers start to develop once more.

The cohort of shoppers that Datadog has mentioned about in the previous couple of quarters which have been optimizing really noticed their utilization develop at a quicker tempo than the broader buyer base.

It does look like the optimization headwind is beginning to dissipate, which is a transparent constructive for the Datadog enterprise.

Steering lighter than anticipated

Whereas the 4Q23 outcomes have been sturdy, the steerage for FY2024 was lighter than what was anticipated.

Income steerage for FY2024 was $2,565 million, up 20.5% from the prior yr, however was 1% beneath consensus.

Working revenue steerage for FY2024 was $545 million, or 21.2% working margins, 4% beneath consensus.

You’ll count on that steerage ought to are available stronger after the constructive commentary highlighted earlier and rising momentum within the enterprise.

It does seem to me that the steerage appears conservative contemplating 4Q23 and the administration commentary.

In accordance with administration, nevertheless, their steerage philosophy remains unchanged and relies on the tendencies that they’ve seen in the previous couple of months together with some conservatism utilized to these numbers.

As well as, it is very important notice that Datadog intends to take a position for future development in 2024, and expects to speed up hiring in R&D and S&M within the yr forward to seize long-term alternatives and international clients.

The expectation right here is thus for working expense to develop within the mid-20-percent vary, ramping all through 2024.

The query right here is absolutely whether or not administration was being conservative within the FY2024 information. It does appear that the arrange appears constructive on condition that we’re seeing enhancing fundamentals as optimizations appear to have slowed, administration commentary turning extra constructive and the income and bookings for 4Q23 got here in higher than anticipated.

Continued R&D in 2023

Datadog spent 43% of revenues on R&D. Clearly, the corporate has a powerful concentrate on innovation and launching new merchandise, which in my opinion will keep its market management within the long-term.

In 2023, Datadog launched greater than 400 new options and capabilities.

Within the observability section, administration highlighted that Datadog now has greater than 700 integrations to permit clients to learn from the latest AWS, Azure and Google Cloud capabilities, together with the newly rising AI stack. Administration shared that they’re seeing rising engagement in its generative AI integrations, which have grown 75% sequentially in 4Q23.

Within the generative AI house, Datadog continues to carry new capabilities to Bits AI, which is its pure language incident administration copilot. As well as, Datadog is progressing in the direction of giant language fashions observability in order that clients can deploy and handle their fashions safely.

Datadog shared that 3% of its ARR comes from generative AI clients at this time, in comparison with 2.5% within the 3Q23 quarter, however I believe the hot button is administration commentary right here, as they “believe the opportunity is far larger in the future as customers of every industry and every size start deploying AI functionality in production”.

Within the Utility Efficiency Monitoring (“APM”) house, Knowledge Streams Monitoring was launched to assist clients monitor queuing, streaming and event-driven pipelines. Datadog additionally launched single-step APM onboarding, which permits only one engineer to allow APM throughout advanced purposes in a matter of minutes.

Datadog’s Cloud Safety enterprise is rising properly in my view. There are actually greater than 6,000 clients utilizing no less than considered one of Datadog’s Safety merchandise. Amongst among the new options and capabilities this quarter embrace the launching of software program composition evaluation, which helps its clients to have the ability to detect, after which tackle vulnerabilities within the code earlier than it will get to manufacturing. As well as, Datadog additionally introduced Cloud Infrastructure Entitlement Administration, which serves to assist clients forestall identification and entry administration safety points. Datadog additionally shipped its cloud SIEM Investigator, which permits its clients to conduct deep safety investigation utilizing logs over lengthy intervals of time. Datadog additionally expanded its information safety capabilities with Sensitive Data Scanner now , which helps clients uncover, classify and redact delicate information each at scale and in real-time.

Lastly, Datadog prolonged Cloud Cost Management, to be now GA for AWS and Azure, and Google Cloud would be the subsequent on the checklist, to assist clients have a complete view of prices throughout their cloud footprint. Datadog additionally shared that it intends to attain FedRAMP Excessive and Impression Degree 5 authorizations.

Working metrics enhance

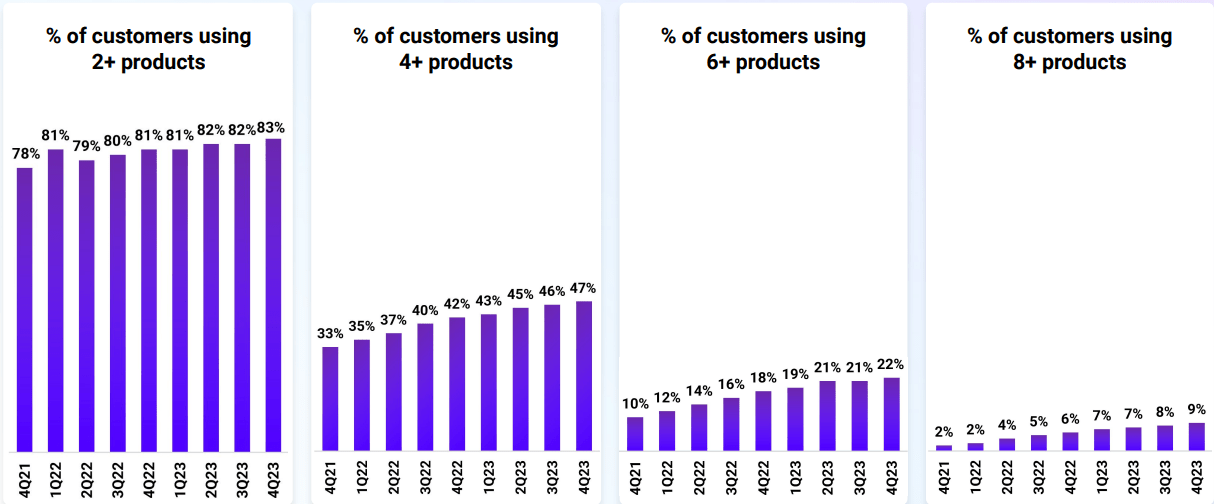

Datadog has been profitable in getting clients to make use of extra of its merchandise over time.

Right now, 83% of its clients use no less than 2 merchandise, up from 81% one yr in the past.

Right now, 47% of its clients use no less than 4 merchandise, up from 42% one yr in the past.

Right now, 22% of its clients use no less than 6 merchandise, up from 18% one yr in the past.

Right now, 9% of its clients use no less than 8 merchandise, up from 6% one yr in the past.

It’s price noting that this sturdy adoption is throughout platforms and merchandise. Datadog’s newer merchandise, which excludes its infrastructure monitoring, APM suite, and log administration merchandise, grew 75% from the prior yr.

% of shoppers utilizing Datadog merchandise (Datadog)

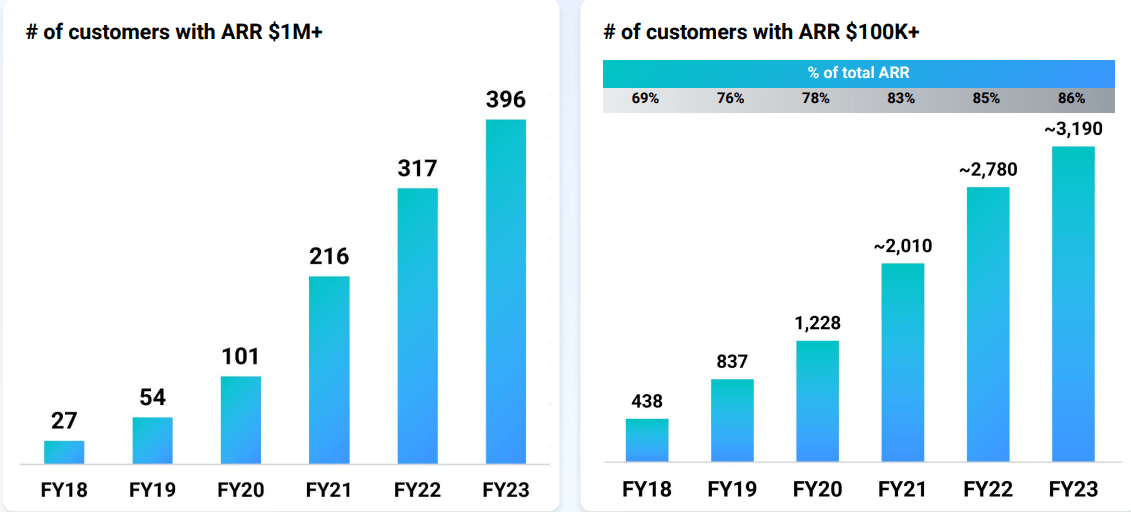

With the rising adoption of the variety of Datadog merchandise by clients, we’re naturally seeing an increasing number of clients spending extra on the Datadog platform.

The variety of clients with greater than $1 million in ARR grew 25% from 317 in 2022 to 396 in 2023.

In flip, the variety of clients with greater than $100k in ARR grew 15% from 2,780 in 2022 to three,190 in 2023.

Additionally the shoppers with greater than $100k in ARR are additionally those which are contributing disproportionately to ARR, making up 86% of whole ARR.

Clients ARR development (Datadog)

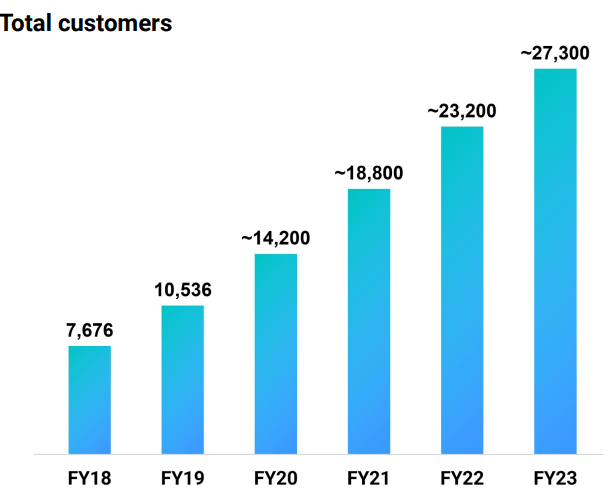

The whole buyer rely grew 18% from 23,200 in 2022 to 27,300 in 2023.

I believe this highlights the potential development in ARR from the continued sturdy development in buyer rely as these new clients which are added at this time might be anticipated to spend extra within the coming years given the sturdy land-and-expand technique of the staff.

Clients (Datadog)

Administration highlighted that its land-and-expand technique continues to have a really sturdy potential. On the finish of 2023, 42% of Fortune 500 corporations are clients of Datadog, however the median Datadog ARR for these Fortune 500 clients is definitely lower than $0.5 million.

This does indicate these giant enterprises are nonetheless early of their migration to the cloud journey and there’s a large alternative for Datadog to develop with these clients.

Lastly, churn has stayed low as Datadog’s dollar-based gross retention fee is secure within the mid-to-high 90s, and the dollar-based internet retention fee is within the mid 100s.

Buyer wins

I believe that we’re seeing that Datadog is not only gaining traction amongst clients, however we’re additionally seeing its clients consolidating with Datadog or that Datadog is efficiently displacing rivals.

Datadog achieved its first ever nine-figure take care of a serious international fintech firm, which is a three-year enlargement settlement. This buyer is predicted to make use of 15 Datadog merchandise and consolidate 10 legacy instruments.

Secondly, Datadog signed a seven-figure enlargement with one of many largest restaurant chains globally. This buyer selected Datadog as a result of it believed that Datadog was the one platform that may carry a couple of constant expertise throughout the 4 cloud suppliers it’s utilizing, specifically AWS, Azure, Google Cloud, and Oracle Cloud. This enlargement settlement will imply that the shopper will use 10 Datadog merchandise and deploy Datadog for Cloud Service Administration use circumstances.

There was an eight-figure multi-year enlargement with a number one European monetary providers firm that’s going by way of a big scale migration to Azure. This buyer is beginning with 14 Datadog merchandise and has consolidated greater than 10 legacy cloud monitoring instruments. After the migration to Azure, this buyer expects the variety of groups that use Datadog every month to develop from 400 to greater than 1,000.

Datadog signed a seven-figure win with one of many largest meals and client good firm on this planet, which incorporates 17 Datadog merchandise and the shopper expects to consolidate no less than six industrial observability instruments. Datadog would be the observability basis of its AIOps technique utilizing Datadog’s Watchdog and incident administration capabilities.

Datadog additionally landed a six-figure take care of one of many largest US utilities. Datadog was discovered to be the one platform that would simply combine end-to-end with their current gross sales, buyer expertise and information workflows. This buyer is trying to begin utilizing six Datadog merchandise and displace two industrial observability instruments.

Datadog additionally not too long ago hired a brand new Chief Advertising and marketing Officer Sara Varni. Sara has greater than 15 years of promoting expertise and was most not too long ago Chief Advertising and marketing Officer at Attentive. Earlier than her time at Attentive, she was Chief Advertising and marketing Officer at Twilio (TWLO) the place she helped the corporate scale income and develop the advertising operate. Lastly, earlier than she joined Twilio, she was at Salesforce (CRM) in senior advertising roles.

Valuation

When you recall within the earlier article, Datadog was buying and selling at 50x 2024 P/E.

Right now, it trades at 85x 2024 P/E.

The very first thing to understand is that whereas Datadog could appear costly at this time, that could be a operate of the market pricing within the very sturdy cocktail of above common development and above common profitability or margin profile.

One other factor to notice is the constructive commentary about continued utilization development and constructive pattern for optimization can be supporting the narrative for an inflection in 2024, which justifies the next valuation.

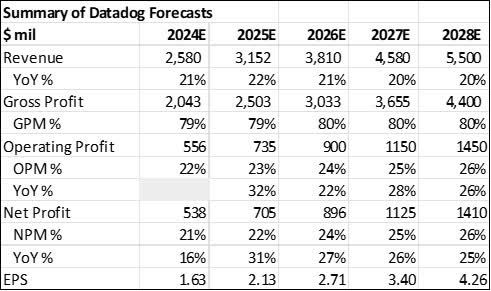

Consequently, I revised my 5-year monetary forecasts for Datadog upwards, as mirrored beneath, the place there’s a 21% income CAGR and 25% EPS CAGR.

Datadog shared that they’re seeing continued utilization development from current clients contribute to the sturdy efficiency in 4Q23, which was what they noticed in 3Q23 as properly.

Additionally, administration additionally famous a constructive pattern on optimization as they observed that the depth of optimization seen within the final six quarters appear to have declined and in reality, they’re beginning to see giant optimizers start to develop once more. 2024 margins additionally mirror the choice of Datadog to put money into its enterprise in 2024.

Abstract of 5-year monetary forecasts (Creator generated)

The intrinsic worth for Datadog relies on a reduced money movement mannequin, assuming 50x 2028 terminal a number of and 12% low cost fee.

Consequently, I derive an intrinsic worth of $121 for Datadog.

My 1-year and 3-year worth targets for Datadog are primarily based on 80x 2024 P/E and 60x 2026 P/E. Whereas each are actually achievable P/E multiples for Datadog to achieve, I’d emphasize that these worth targets don’t provide a lot conservatism.

Conclusion

I believe Datadog continues to execute properly on its innovation plans, with many options and capabilities launched in 2023. The corporate stays in funding mode and can possible proceed to rent key R&D individuals to proceed this innovation.

The corporate has been proactive in generative AI and I believe may very well be one of many beneficiaries to the pattern of accelerating spend in generative AI.

As well as, the gross sales and advertising staff has additionally accomplished job in touchdown giant offers.

The constructive pattern of declining optimizations and rising buyer utilization is driving an inflection within the firm’s outcomes and factors in the direction of a constructive begin to 2024, and highlights that the worst is probably going over for the corporate.