pingingz

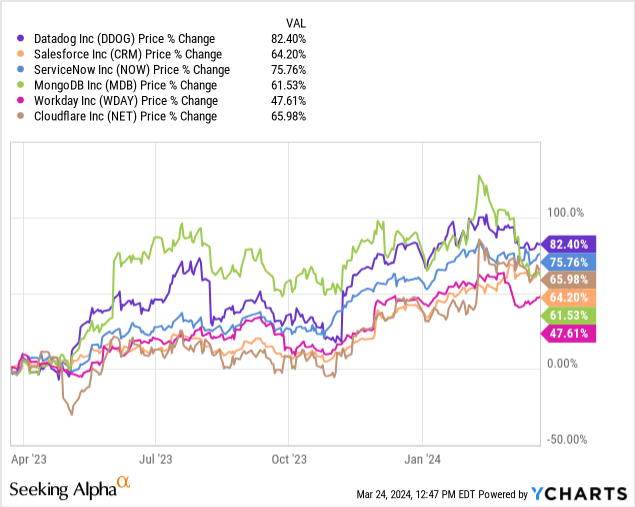

Datadog (NASDAQ:DDOG) is among the largest beneficiaries of digital transformation and corporations shifting to the cloud. Moreover, the proliferation of the Web of Issues (“IoT”) and edge computing is driving an enormous improve in machine-generated knowledge, a secular development that might probably drive vital future income development for the corporate’s observability platform. The corporate displayed its upside potential final yr when, regardless of heavy cloud optimization developments in 2023, it launched a third-quarter earnings report crushing analysts’ earnings estimates for the quarter and included a full-year 2023 steerage elevate. JPMorgan upgraded the inventory to overweight. The inventory rose 28.50%, serving to it outperform many Software program-as-a-Service (“SaaS”) corporations during the last yr, as proven within the chart under.

Nonetheless, this firm has a number of dangers that some worried about even earlier than final yr’s third-quarter earnings. These dangers by no means actually disappeared and made some traders assume twice after Datadog reported fourth quarter 2023 earnings earlier than the bell on February 13, 2024. The corporate forecasted income of between $2.555 billion and $2.575 billion for the complete yr 2024, under analysts’ estimates of $2.586 billion.

Administration additionally issued the primary quarter of 2024 adjusted web earnings per share between $0.33 and $0.35, nicely under analysts’ estimates of $0.39. The corporate’s steerage for the complete yr 2024 adjusted web earnings per share was $1.38 and $1.44, once more lacking consensus analyst estimates of $1.78. By failing to satisfy or exceed analysts’ forecasts, with the dangers factored in, the market started to query Datadog’s valuation. Consequently, as of March 22, 2024, the inventory is down 7% for the reason that firm reported fourth quarter 2023 earnings.

This text will focus on Datadog’s enterprise and its excessive potential upside. It can additionally briefly focus on its fourth-quarter earnings, a couple of dangers, the inventory’s valuation, and why, regardless of the corporate’s potential upside, I believe the inventory is a Maintain at present costs.

Why the corporate’s platform has excessive potential upside

Over a decade in the past, Marc Andreessen, co-founder of enterprise capital agency Andreessen-Horowitz, gained fame for stating that “software is eating the world.” What he meant by that’s that software program is more and more creating many of the worth in companies in all sectors of the economic system. Suppose what Andreessen said is true; whichever firm is the primary to provide the best and environment friendly software program functions can probably create aggressive benefits of their trade.

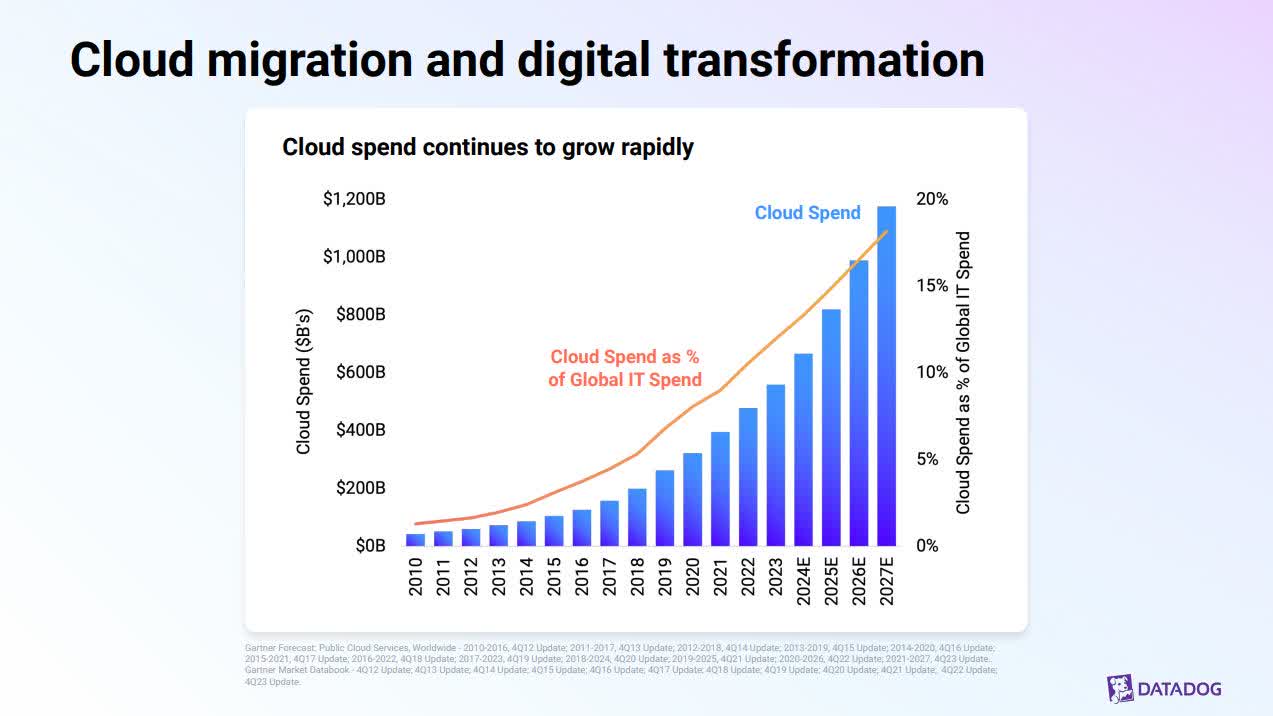

Organizations are beginning to flock in the direction of cloud computing as a result of it permits improvement groups to collaborate with Data Expertise (“IT”) operation groups to hurry up software program improvement, create higher software program, and handle functions extra effectively. The chart under from its 2024 investor presentation reveals that cloud spending and cloud spending as a proportion of worldwide IT spending are rising quickly.

Datadog 2024 Investor Day.

Datadog defines itself in its 2023 10-Ok as “the observability and security platform for cloud applications,” providers which might be important as cloud computing can vastly improve the complexity for IT operation professionals inside corporations utilizing cloud computing and different digital transformation applied sciences to compete.

Consequently, as cloud computing grows, demand for Datadog’s providers grows. Cloud computing and different digital applied sciences can turn into so advanced that it has turn into vastly more difficult and would require hiring extra folks to resolve points with software program functions with out the corporate’s observability platform.

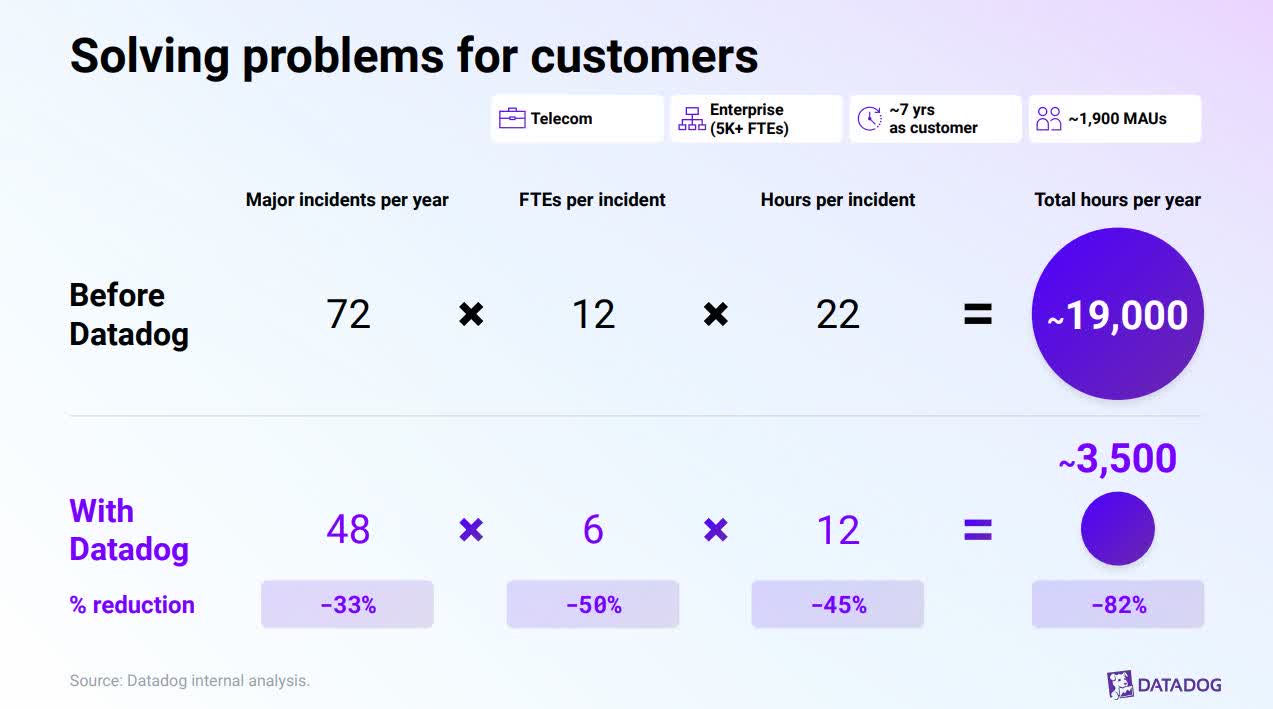

The corporate’s platform can considerably scale back the scale of the group of builders wanted to construct an software and the scale of an IT group responding to incidents. Throughout the firm’s 2024 Investor Day, Vice President of Product Yrieix Garnier explained how its platform helped a telecom firm save money and time responding to main incidents.

Datadog 2024 Investor Day.

The picture above reveals that Datadog decreased that firm’s main incidents by 33% yearly. FTEs imply the typical variety of folks engaged per incident. So, the platform cuts in half the variety of people who want to answer a serious incident and reduces the time it takes to resolve an incident by 45%. The result’s decreasing the corporate’s annual person-hours it devotes to incidents by 82%, permitting personnel to interact in different duties.

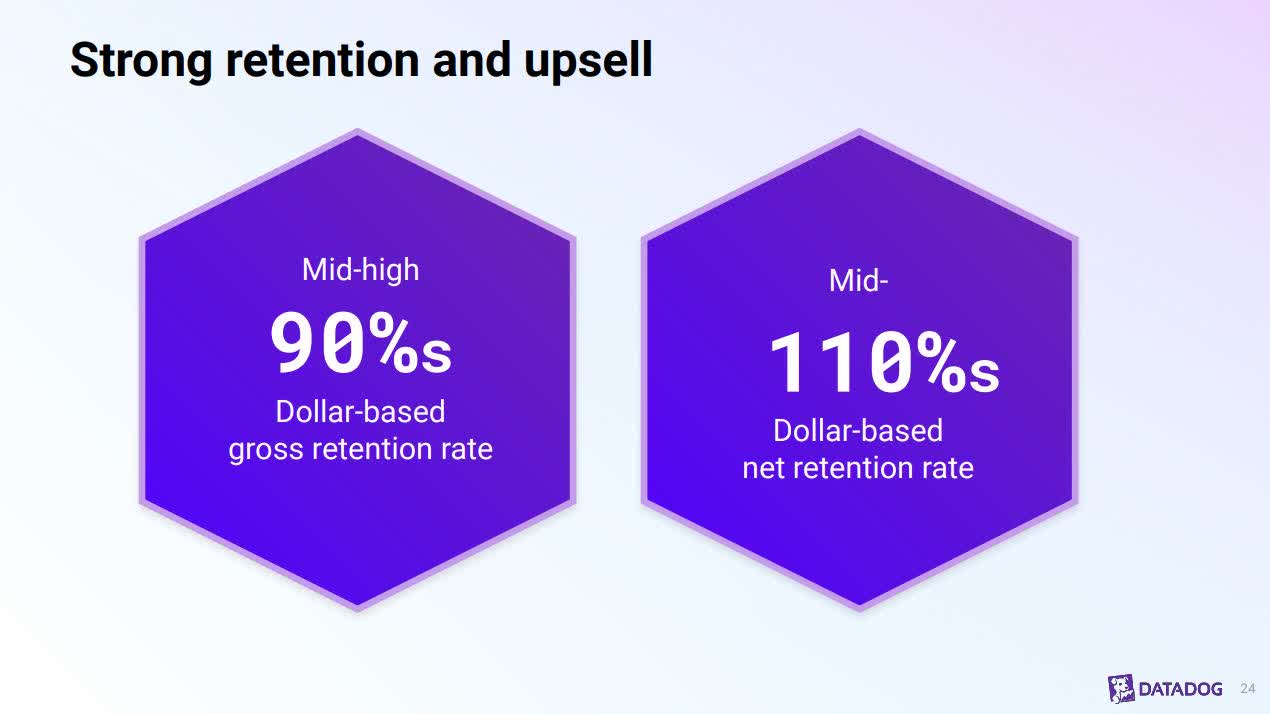

This potential to avoid wasting organizations money and time is an element of their potential to retain and upsell most of their buyer base regardless of the cloud optimization developments during the last yr. The corporate’s fourth quarter 2023 gross retention ratio (“GRR”) is within the mid-90s, a superb quantity for a SaaS firm, that means it has efficiently retained over 90% of its current buyer’s income. Moreover, its web retention ratio (“NRR”) got here in above 110%, one other respectable quantity for a SaaS firm, indicating it’s retaining current prospects and upselling these prospects by 10% over the earlier interval.

Datadog Fourth Quarter 2023 Earnings Name Presentation.

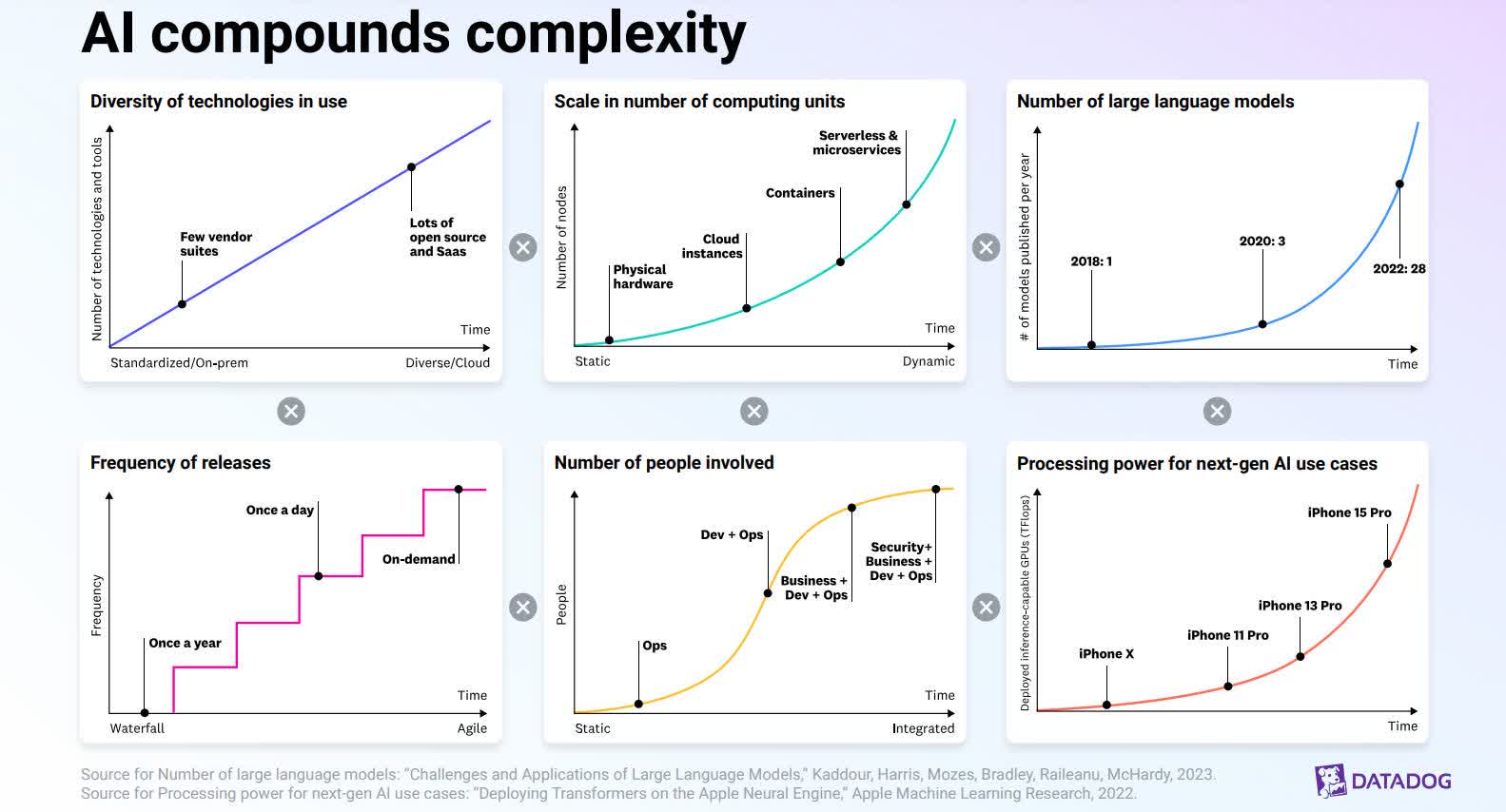

Whereas software program could also be consuming the world, NVIDIA’s (NVDA) Chief Government Officer (“CEO”) Jensen Huang predicted in 2017 that “AI eats software.” The proliferation of generative AI is quickly making Jensen’s prediction come true, and the enlargement of this new AI know-how has solely elevated the complexity that organizations have to cope with.

Datadog 2024 Investor Day.

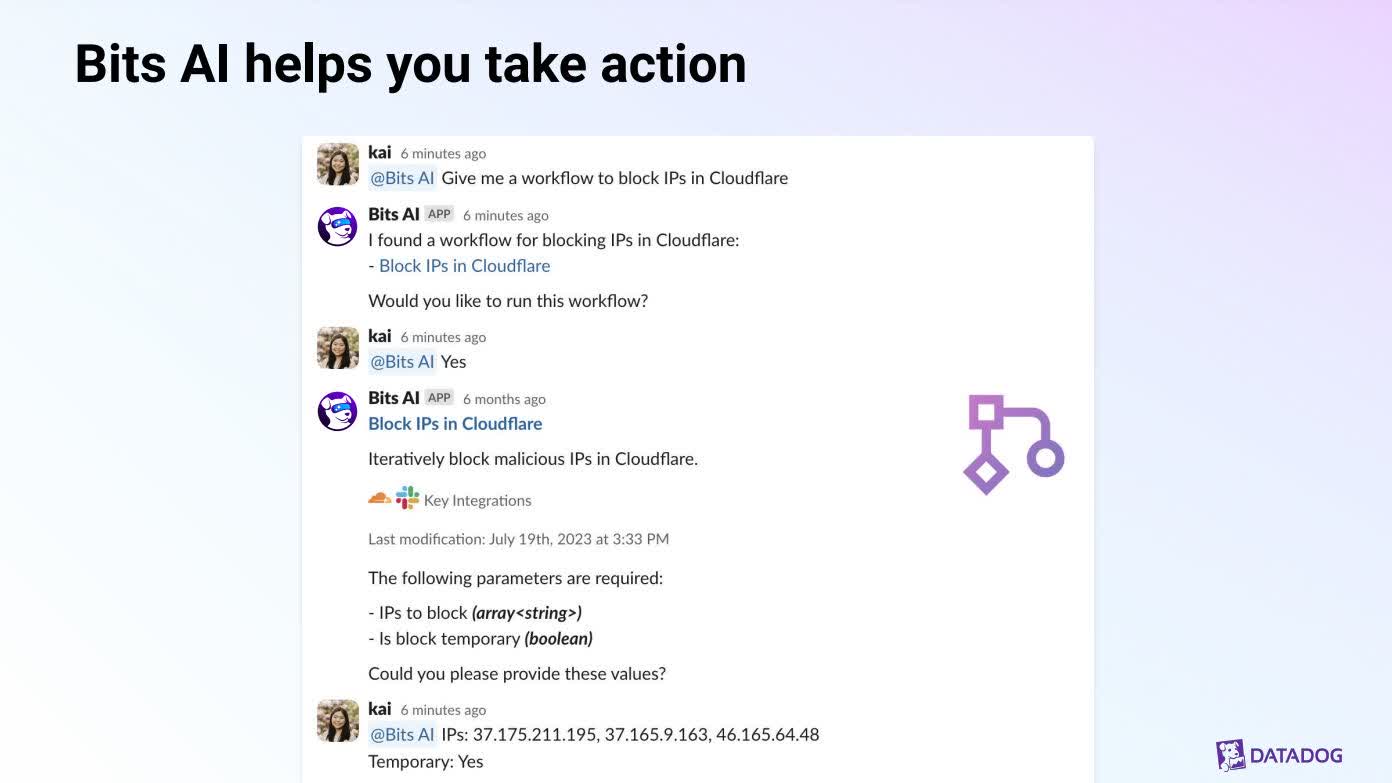

Datadog makes use of generative AI in two methods. It improves many distinct features of its platform with the know-how, and the corporate has created a generative AI chatbot known as Bits AI for patrons.

Datadog 2024 Investor Day.

Since cloud computing and generative AI are within the early levels, Datadog has a protracted potential income development runway. Let’s study how demand for Datadog’s observability, safety, and different performance the corporate has on its platform interprets to income development, earnings, and free money circulate (“FCF”).

A superb fourth quarter 2023 earnings report

The excellent news is that cloud optimization developments which have held many cloud service suppliers again during the last yr are starting to say no. Chief Monetary Officer (“CFO”) David Obstler stated throughout the firm’s fourth-quarter earnings name (Emphasis added):

Final quarter, we talked about that the bigger and extra intense optimizers had begun to point out indicators of stabilization. In This fall, we noticed these developments proceed and the big optimizers start to develop once more. Whereas we should still be in a cost-conscious atmosphere general, we imagine that the upper depth of optimization has dissipated and shoppers are persevering with to spend money on new digital functions.

Supply: Datadog Fourth Quarter 2023 Earnings Name

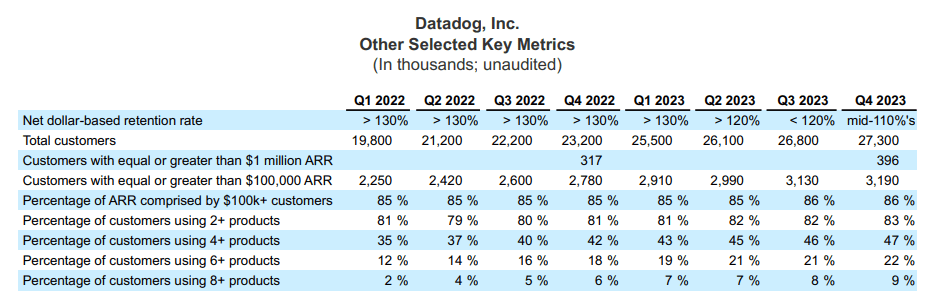

If that assertion is true, it may result in elevated cloud spending for Datadog’s providers over the subsequent a number of quarters. In that case, administration’s steerage might show conservative, and the corporate might even exceed analysts’ estimates. The desk under from Datadog’s fourth quarter 2023 investor relations monetary statement package reveals a number of important metrics traders ought to monitor to find out whether or not the corporate is certainly bouncing again from slowing cloud spending.

Datadog’s Fourth Quarter 2023 Investor Relations Monetary Assertion Bundle

Though Datadog produced mid-110% NRR within the fourth quarter, this quantity is down considerably from roughly 130% within the fourth quarter of 2022. NRR rising to 120% or larger may point out that cloud spending by prospects has resumed. A rising NRR may additionally elevate investor confidence that income development may rise larger sooner or later.

Alternatively, if NRR begins trending right down to 100 or under, traders might turn into anxious in regards to the firm dropping prospects or having problem upselling prospects to new merchandise. If that occurs, Wall Road might turn into disenchanted about Datadog’s future income development potential.

Complete prospects rose 15% yr over yr to three,190. Extra prospects improve the dimensions and effectivity of Datadog’s SaaS enterprise, which is crucial for increasing the corporate’s margins.

Prospects with equal or larger than $1 million Annual Recurring Income (“ARR”) grew 25% yr over yr to 396. Prospects with an ARR of $100,000 or extra rose 15% yr over yr to three,190. ARR represents the gross sales enlargement to the prevailing buyer base over one yr. Datadog defines ARR in its 2023 10-Ok: “The annual run-rate revenue of subscription agreements from all customers at a point in time.“

An increase in these numbers reveals the corporate is efficiently upgrading and cross-selling merchandise to its current giant enterprise prospects, ensuing within the buyer’s lifetime worth (“LTV”) rising and buyer acquisition prices (“CAC”) declining. When an organization raises its LTV and lowers its CAC, traders typically turn into extra assured that it might probably enhance its profitability. These are essential numbers for traders to comply with as a result of traders’ confidence in future income development and profitability may rise or fall relying on what they present. Improved profitability typically interprets to larger FCF if an organization can hold its capital bills (“CapEx”) down. An growing FCF is often engaging to traders for a lot of causes.

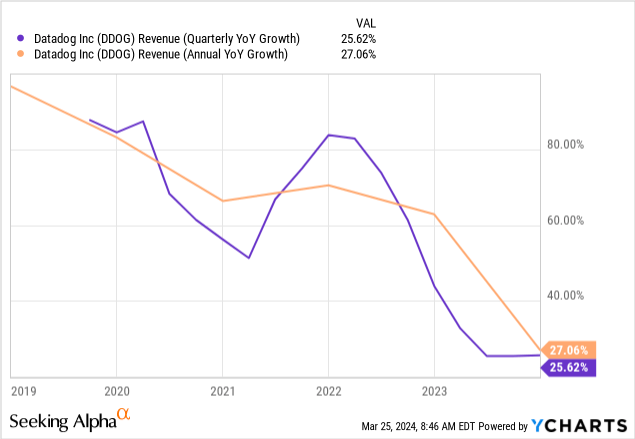

Not proven within the above desk, however an especially essential metric, remaining efficiency obligations (“RPO”), rose 74% over the earlier yr’s quarter to $1.84 billion. When an organization’s RPO grows sooner than income development, it signifies a strong gross sales pipeline and the potential for sooner income development. The corporate grew fourth-quarter income by 25.66% and seven.69% sequentially to $589.64 million, above analyst estimates of $568.23 and administration’s steerage of $566 million. As you possibly can see on the chart under, income development has taken a considerable dive during the last two years.

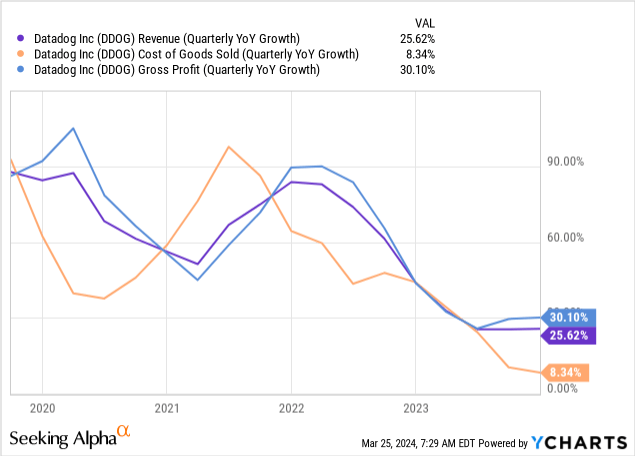

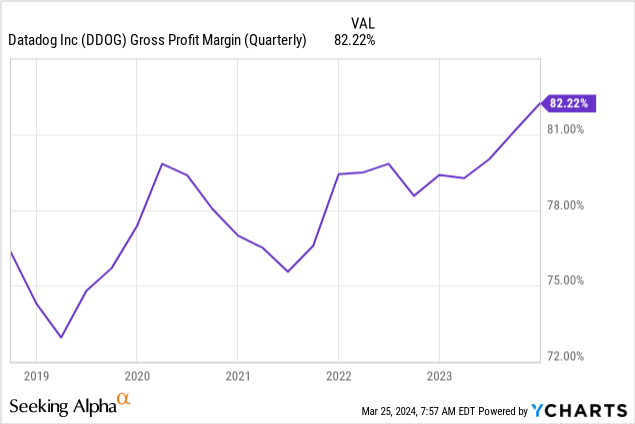

In the meantime, the price of items bought (COGS) solely grew 8.34% throughout the fourth quarter, which has the impact of accelerating GAAP (Typically Accepted Accounting Ideas) gross earnings sooner than income development, which the chart under reveals. Moreover, it helped GAAP gross margins develop 281 foundation factors (“bps”) year-over-year to 82.2%.

CFO David Obstler stated in regards to the gross margin enchancment on the fourth quarter 2023 earnings name, “We continue to experience efficiencies in cloud costs reflected in our cost of goods sold as our engineering teams pursue cost savings and efficiency products — projects.“

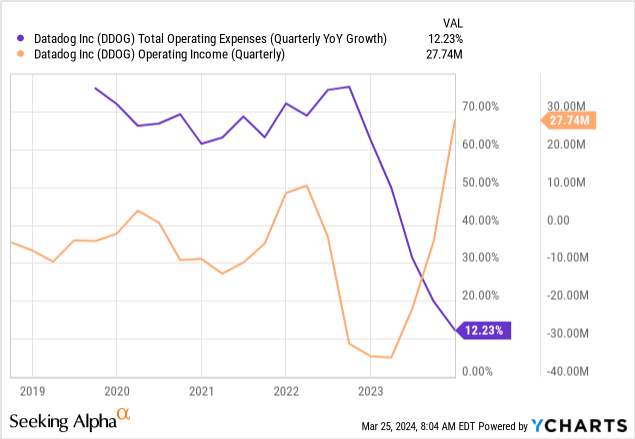

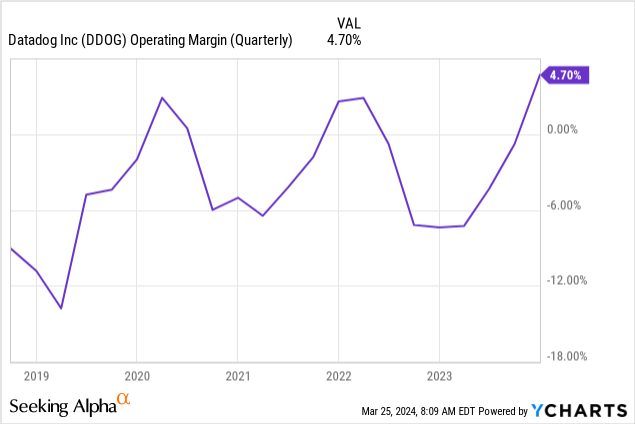

Equally, Datadog’s GAAP working bills (OpEx) solely grew 12.23%, boosting GAAP working earnings from a $34.62 million loss within the earlier yr’s comparable quarter to a acquire of $27.74 million within the fourth quarter of 2023. GAAP working margin was a constructive 4.70%.

The discount in OpEx and the rise in working margin and working earnings resulted from optimization and value administration efforts. Nonetheless, traders shouldn’t count on the identical substantial enhancements shifting ahead. David Obstler indicated that the corporate was extra cautious about investing in 2023 as a result of worries in regards to the world economic system and plans to ramp up funding in 2024. Traders ought to count on that the working margin will recede shifting ahead. The corporate emphasizes non-GAAP numbers in its working margin steerage. It forecasts a first-quarter 2024 non-GAAP working margin of twenty-two%, in comparison with a 28% working margin reported within the fourth quarter of 2023.

Among the many causes that the inventory worth has stalled is as a result of administration is telling the market that they’re going to improve funding, which can decrease profitability. Nonetheless, administration didn’t forecast the elevated income development analysts had anticipated for the primary quarter and the yr. Whereas Datadog’s elevated investments might rejuvenate income development in the long run, traders won’t see the bang for the funding buck within the close to time period. An alternate rationalization is that administration has deliberately made conservative income forecasts that they internally imagine they’ll beat. In both case, the market could also be unwilling to push the inventory a lot larger than it’s till it sees the corporate’s growing income development.

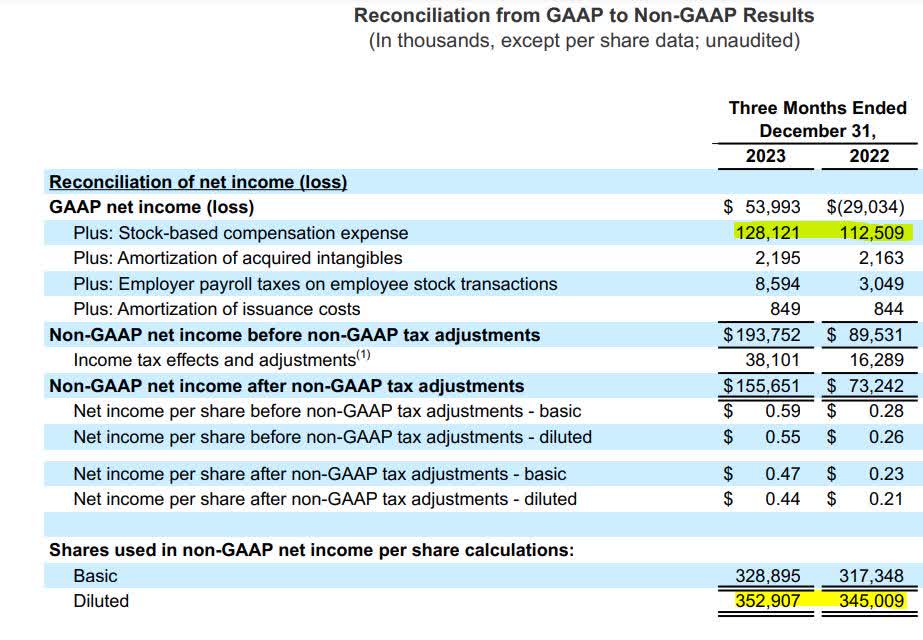

Let’s transfer down the earnings assertion to the underside line. Datadog generated a diluted GAAP web income-per-share of $0.16, up from a lack of $0.09 within the earlier yr’s quarter. The non-GAAP web income-per-share of $0.44 aligned with analysts’ consensus earnings however beat the corporate’s steerage of $0.41.

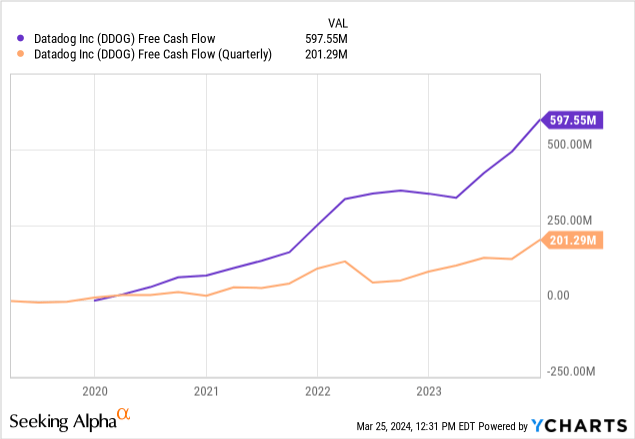

Datadog spends comparatively little on CapEx as a cloud firm: $18.94 million, which is simply 3.21% of its income. Suppose the corporate retains the CapEx-to-revenue ratio on the present low degree whereas rising web earnings extra quickly; this may bode nicely for growing FCF development. The corporate generated a fourth-quarter FCF of $201.29 million and a trailing 12-month FCF of $597.55.

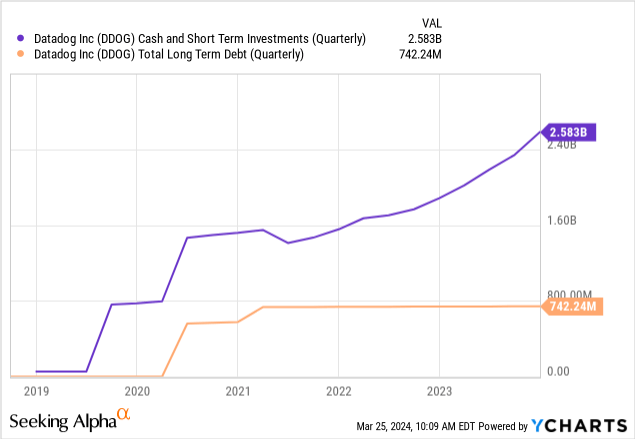

Datadog ended 2023 with $2.58 billion in money and short-term investments towards $742.24 million in convertible debt due in 2025. The corporate’s money and debt-to-EBITDA (earnings earlier than curiosity, taxes, depreciation, and amortization) ratio of three.09 signifies that it has loads of cash to pay down its long-term debt. On the finish of the fourth quarter, its fast ratio was 1.24. A quantity above 1.0 means the corporate has sufficient property to pay its short-term obligations.

Let’s check out a couple of dangers.

Dangers

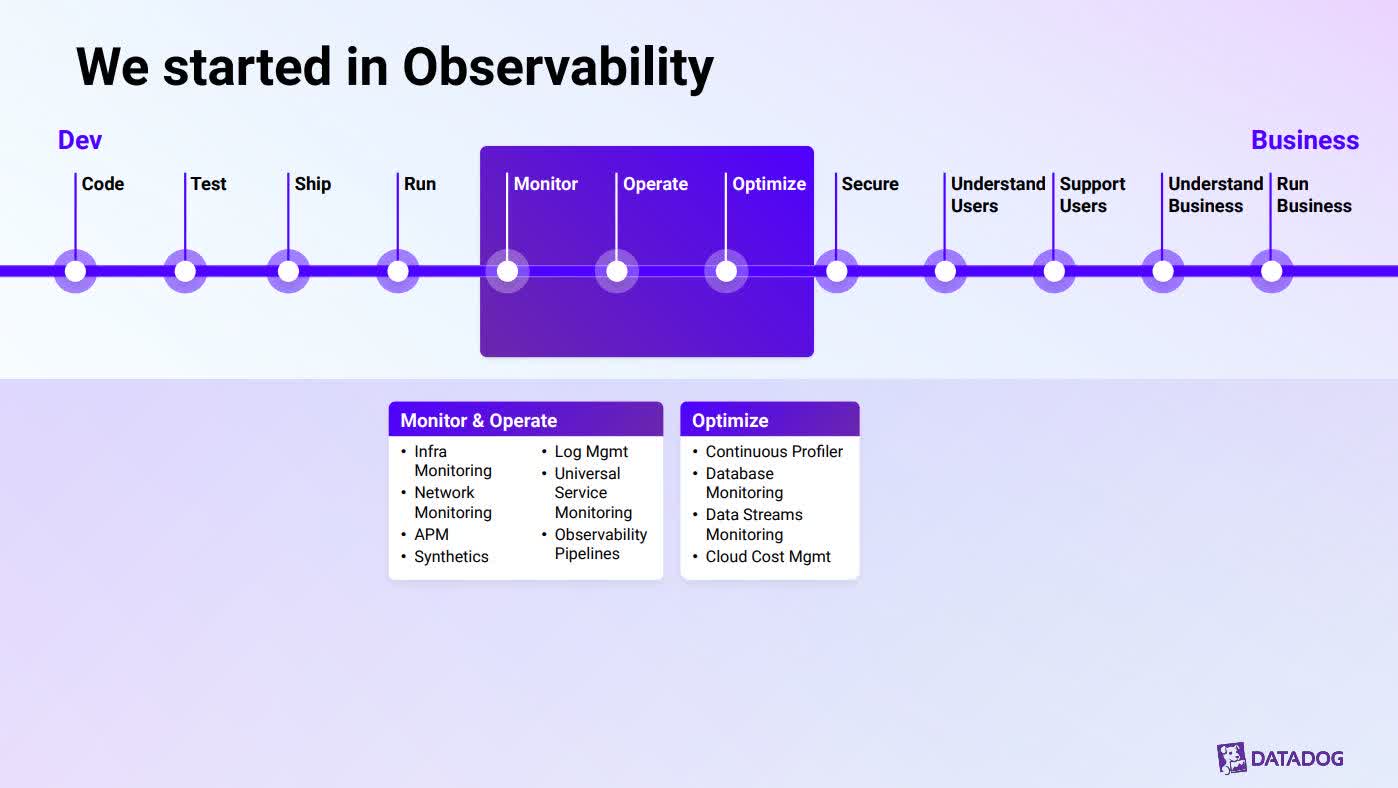

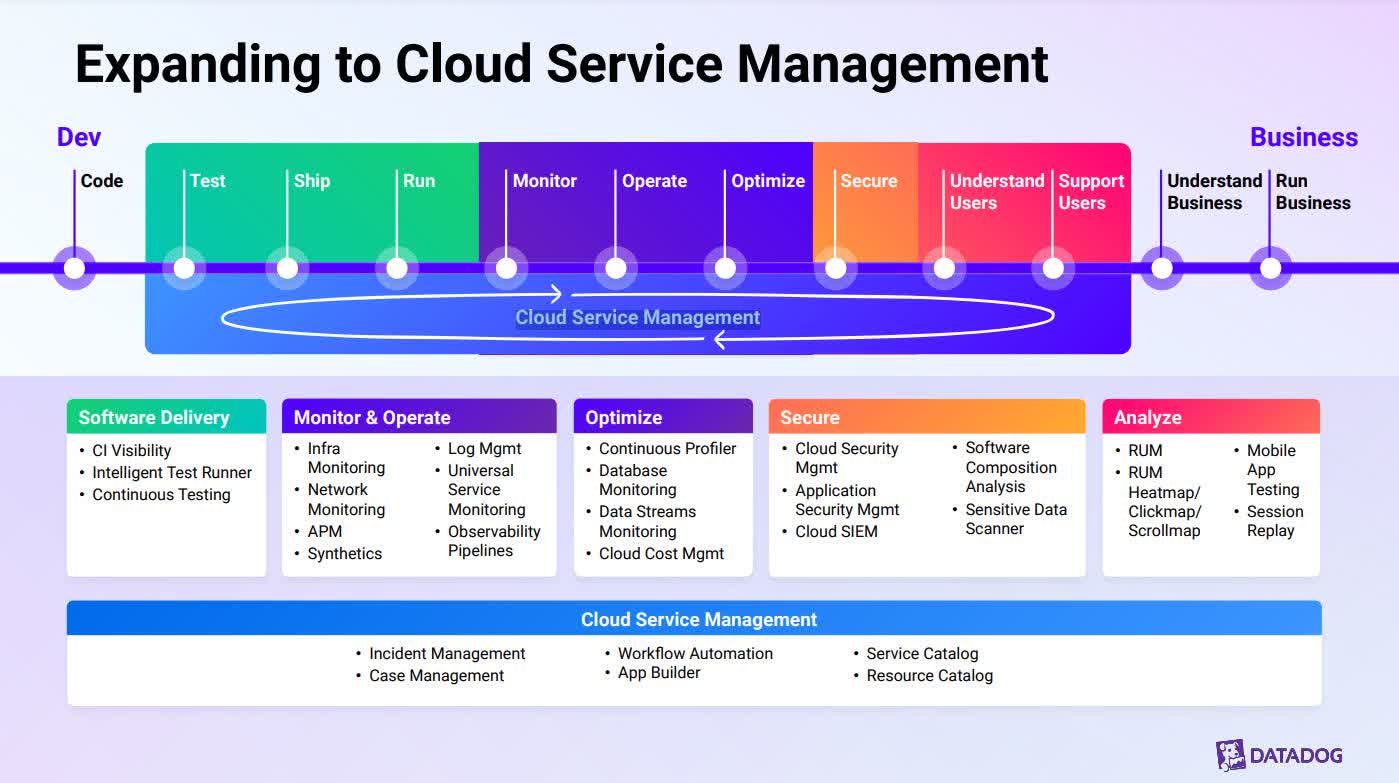

One danger that traders ought to be keenly conscious of is intensifying competitors. One of many causes competitors is intensifying is that Datadog is increasing into adjoining markets from its unique enterprise and encroaching on the turf of increasingly more potential rivals. The primary picture reveals Datadog’s unique space of focus, observability.

Datadog 2024 Investor Day.

Throughout its 2024 Investor Day, administration defined how the corporate first moved into safety, the place a few of its options, like cloud Safety Data and Occasion Administration (SIEM), compete with CrowdStrike’s (CRWD) Falcon SIEM, SolarWinds’ (SWI) SIEM device, and Splunk’s SIEM options. As a reminder, Cisco Techniques (CSCO) lately acquired Splunk. Datadog later created merchandise addressing must the precise and the left of its core observability product to assist improvement and operations groups collaborate throughout its new Cloud Service Administration platform. This enlargement in capabilities may put it into extra direct competitors with cloud heavyweights reminiscent of Amazon’s (AMZN) AWS, Alphabet’s (GOOGL) (GOOG) GCP, and Microsoft’s (MSFT) Azure for cloud monitoring providers.

Datadog 2024 Investor Day.

Datadog additionally has rivals like New Relic (personal) and Dynatrace (DT) in its unique observability enterprise. As well as, different companies like CrowdStrike are increasing into adjoining areas that compete towards Datadog’s core merchandise. As an example, CrowdStrike purchased an organization known as Humio in 2021, which owned an observability platform that competes with Datadog. Individuals who resolve to spend money on Datadog should monitor the ever-shifting aggressive panorama for acquisitions, new know-how, and new entrants to all areas the place the corporate competes. The corporate’s 2023 10-Ok states:

With the introduction of latest applied sciences and market entrants, we count on that the aggressive atmosphere will stay intense going ahead. A few of our precise and potential rivals have been acquired by different bigger enterprises and have made or might make acquisitions or might enter into partnerships or different strategic relationships which will present extra complete choices than they individually had supplied or obtain larger economies of scale than us. As well as, new entrants not at present thought-about to be rivals might enter the market by means of acquisitions, partnerships or strategic relationships.

Supply: Datadog 2023 10-Ok

Subsequent, traders ought to monitor Datadog’s share dilution. Its fourth quarter 2023 diluted weighted common shares had been up 11.2% year-over-year to 352,907; the inventory has a comparatively excessive stock-based compensation (“SBC”) at 21.7% of income. So long as an organization outperforms, the market has been forgiving of shares with excessive SBC. Nonetheless, if an organization with excessive SBC underperforms analysts’ and traders’ expectations, the inventory may speed up to the draw back. Up till now, SBC has but to be a difficulty for Datadog. Nonetheless, if Datadog regularly misses future income or earnings expectations, the market might begin discovering points with its excessive SBC.

Datadog 2023 10-Ok

For those who resolve to spend money on Datadog, bear in mind that the corporate’s non-GAAP numbers include SBC. Though utilizing non-GAAP numbers to light up an organization’s core profitability is handy, traders ought to all the time study them alongside GAAP numbers, as SBC can damage shareholders by diluting their possession. SBC can also be a non-cash cost that may distort FCF. In case you are an investor who makes use of FCF to worth a inventory, SBC may probably throw off your valuation.

Lastly, though the corporate’s convertible notes are usually not a right away danger, the debt may create unexpected issues if, for any cause, Datadog is unable to provide sufficient money circulate to repay the principal and curiosity, which can power the corporate to lift capital or restructure debt on unfavorable phrases. Potential causes that might scale back money circulate embrace a poor macro economic system, sudden enterprise developments, or the aggressive atmosphere. Administration highlighted an extra danger from its convertible notes in its 2023 10-Ok:

Within the occasion the conditional conversion characteristic of the 2025 Notes is triggered, because it was throughout the quarter ended March 31, 2022, holders of the 2025 Notes are entitled to transform the notes at any time throughout specified intervals at their choice. If a number of holders elect to transform their 2025 Notes, until we elect to fulfill our conversion obligation by delivering solely shares of our Class A standard inventory (apart from paying money in lieu of delivering any fractional share), we might be required to settle a portion or all of our conversion obligation by means of the fee of money, which may adversely have an effect on our liquidity. As well as, even when holders don’t elect to transform their 2025 Notes when these conversion triggers are happy, we could possibly be required below relevant accounting guidelines to reclassify all or a portion of the excellent principal of the 2025 Notes as a present quite than long-term legal responsibility, which might lead to a fabric discount of our web working capital.

Supply: Datadog 2023 10-Ok.

For those who resolve to spend money on Datadog, monitoring the corporate’s convertible debt scenario could also be in your finest curiosity. Though the chance of one thing going mistaken could also be low, the potential detrimental affect on the corporate’s funds is critical.

Valuation

By most conventional valuation metrics, Datadog’s inventory seems to be overvalued. Searching for Alpha’s quant charges the inventory’s valuation an F. The corporate hasn’t produced GAAP earnings lengthy sufficient to present a legitimate conclusion primarily based on a GAAP price-to-earnings (P/E) ratio. Nonetheless, the corporate’s non-GAAP P/E ratio of 80.41 is nicely above the sector median of 23.17, signaling that the market might overvalue the inventory.

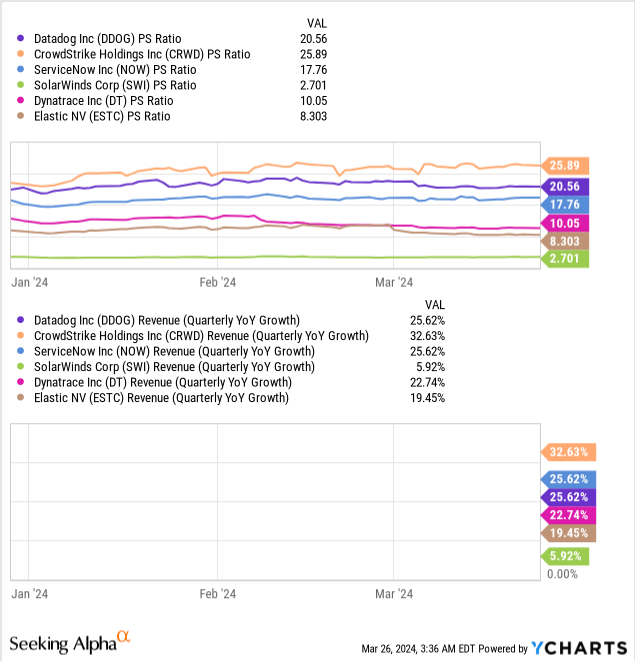

The next chart compares Datadog’s price-to-sales (P/S) ratio to that of a number of different corporations that present an observability product. Curiously, ServiceNow and Datadog have the identical year-over-year quarterly development charges, but the market values Datadog larger on a P/S ratio foundation.

The next reverse DCF reveals the implied FCF development charges over the subsequent ten years for Datadog’s closing worth of $123.45 on March 26, 2024.

Reverse DCF

|

The primary quarter of FY 2025 reported Free Money Stream TTM (Trailing 12 months in thousands and thousands) |

$598 |

| Terminal development fee | 3% |

| Low cost Fee | 10% |

| Years 1 – 10 development fee | 23.9% |

| Inventory Value (March 26, 2024, closing worth) | $123.45 |

| Terminal FCF worth | $5.251 billion |

| Discounted Terminal Worth | $28.922 billion |

| FCF margin | 28% |

Datadog’s potential to realize an FCF of 23.9% could also be a tall order. In keeping with one analyst estimate, its income development ought to have a compound annual development fee of 20.78% over the subsequent ten years, which may make it difficult for the corporate to develop FCF as quick because the assumptions that go into the above reverse DCF recommend.

Nonetheless, since Datadog has but to completely scale its enterprise, the FCF margin will seemingly proceed to broaden. How a lot can it develop? Two comparable cloud SaaS corporations, CrowdStrike and ServiceNow, have FCF margins of 30%. If Datadog can broaden its FCF margins to 30%, it might solely want to realize an FCF development fee of twenty-two.9%, which remains to be a tricky ask.

One cause the market could also be delicate to Datadog’s newest fourth-quarter 2023 income and earnings miss is that, on the present worth, the market assumes lots of top-line and profitability enlargement. Except the corporate can develop its income by 25% to 26% or broaden its FCF margin to 34% over the subsequent ten years, the present inventory worth could also be a stretch. Though the corporate could also be totally able to doing so, with the quantity of competitors that Datadog has in its market, I want to see extra proof that the corporate’s downward development in income for the reason that starting of 2022 has hit backside and whether or not it might probably proceed increasing margins over the long term towards rising competitors.

Why I take into account Datadog a maintain

The market might have gotten just a little forward of itself in driving Datadog as much as the present valuation. In case you are a price investor, you might wish to keep away from Datadog for now. Even development traders ought to stay cautious of this firm at its present valuation. Nonetheless, suppose you’re a long-term investor who already owns the inventory. In that case, you might wish to proceed to carry as the corporate nonetheless has a excessive potential upside from cloud adoption, digital transformation, and generative AI over the subsequent 5 to 10 years. I fee Datadog a Maintain.