Watcom

At first of the yr, I wrote a cautious article on the Western Asset/Claymore Inflation-Linked Alternatives & Revenue Fund (WIW), warning {that a} ‘increased for longer’ Federal Reserve could show to be a headwind for the duration-heavy WIW fund. I additionally warned that the WIW fund will seemingly retest its October 2022 lows, primarily based on the technical image on the time.

Since my article, the WIW fund has carried out poorly, delivering 4.0% in whole returns and justifying my warning (Determine 1).

Determine 1 – WIW has carried out poorly in 2023 (Looking for Alpha)

As we wrap up 2023, allow us to evaluation my predictions on the WIW fund and refresh my thesis.

Temporary Fund Overview

The Western Asset/Claymore Inflation-Linked Alternatives & Revenue Fund is a sizeable closed-end fund (“CEF”) specializing in inflation linked securities, with over $600 million in web belongings.

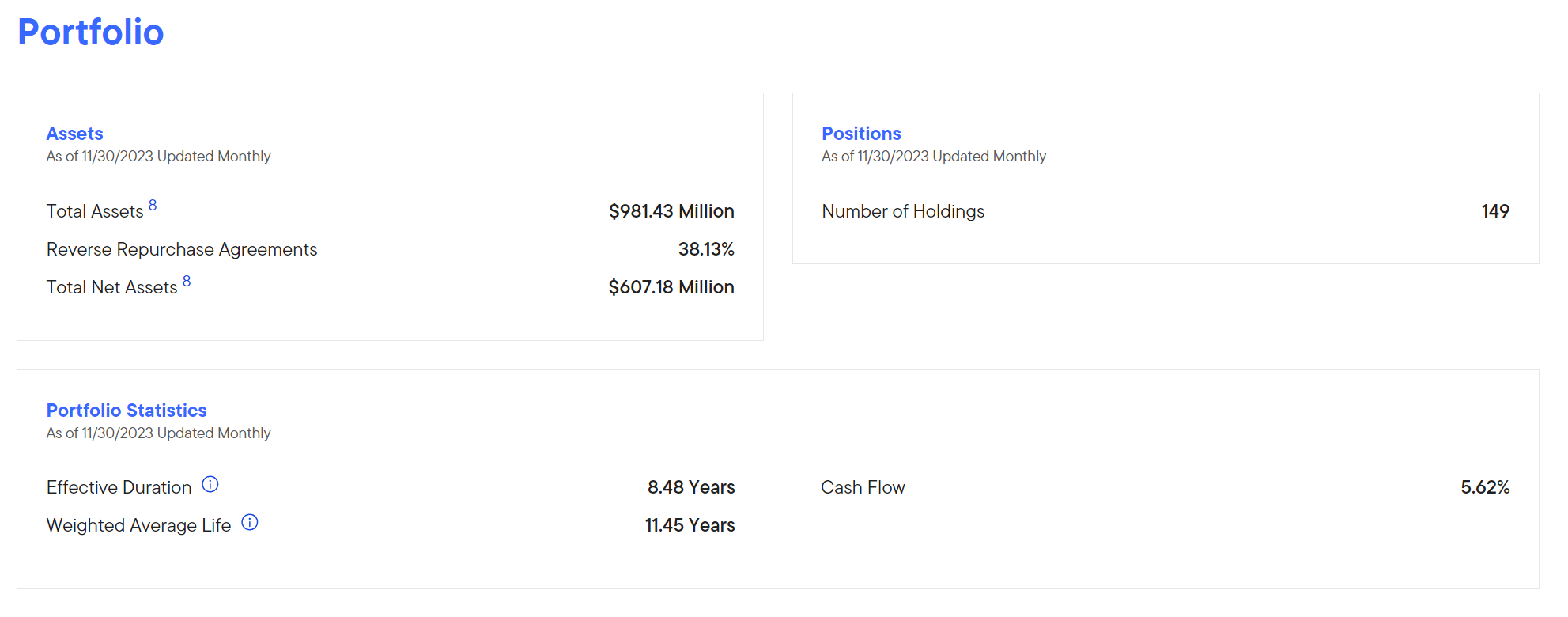

WIW’s portfolio at the moment comprises 149 securities with an efficient period of 8.5 years, basically unchanged from 8.4 years after I final reviewed the fund (Determine 2).

Determine 2 – WIW portfolio overview (franklintempleton.com)

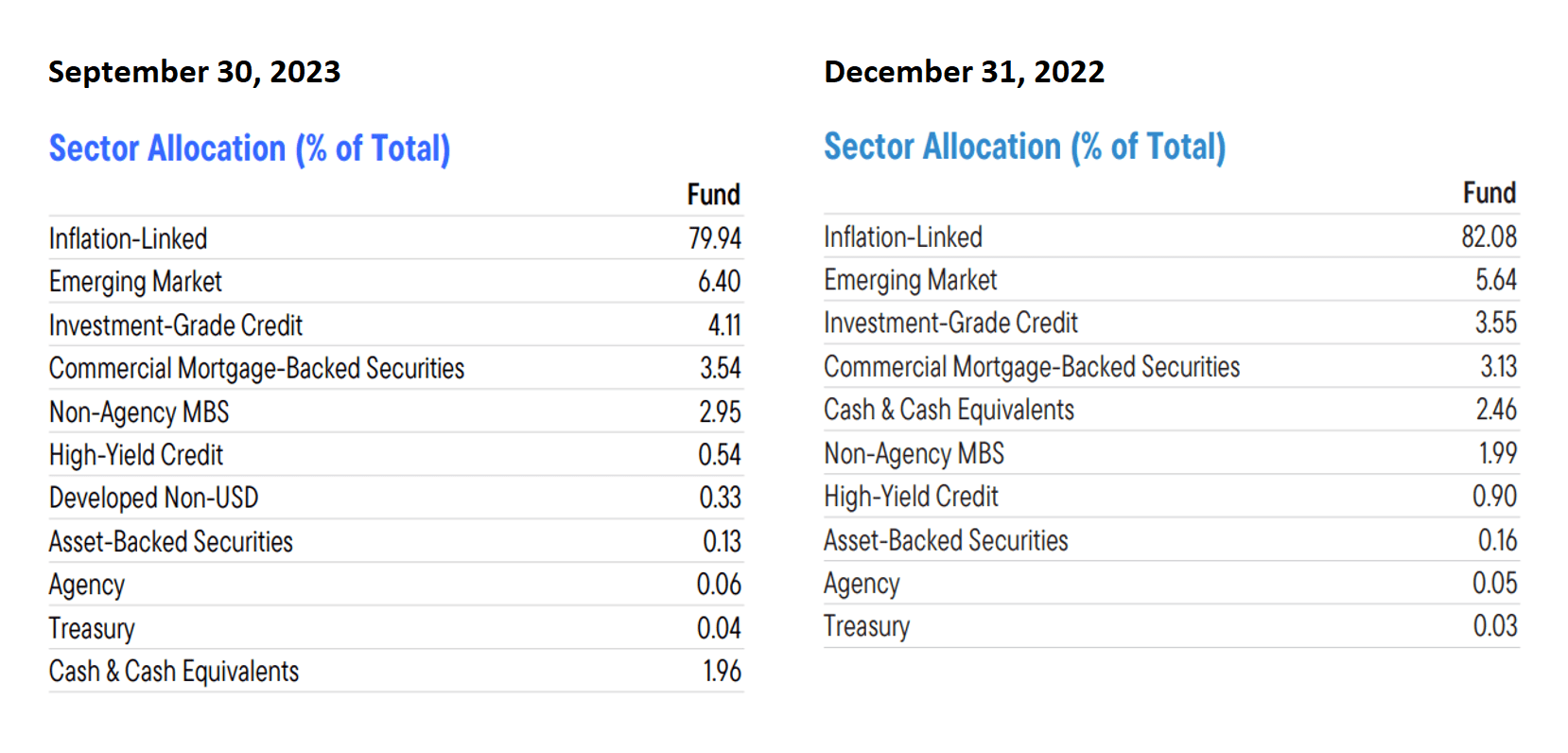

The fund’s sector allocations are additionally little modified, with inflation-linked securities nonetheless accounting for the lion’s share of the portfolio at 79.9% (Determine 3).

Determine 3 – WIW portfolio allocation is little modified (Creator created with information from WIW factsheets)

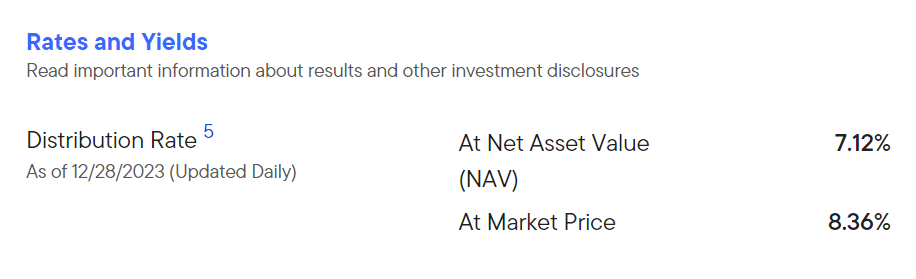

The WIW fund pays a pretty $0.0605 / month distribution that annualizes to a 7.1% yield on NAV and eight.4% yield on market worth (Determine 4). WIW’s distribution is funded from web funding revenue (“NII”) and realized positive aspects.

Determine 4 – WIW pays a pretty 8.4% yield (franklintempleton.com)

‘Larger For Longer’ Proved To Be A Headwind

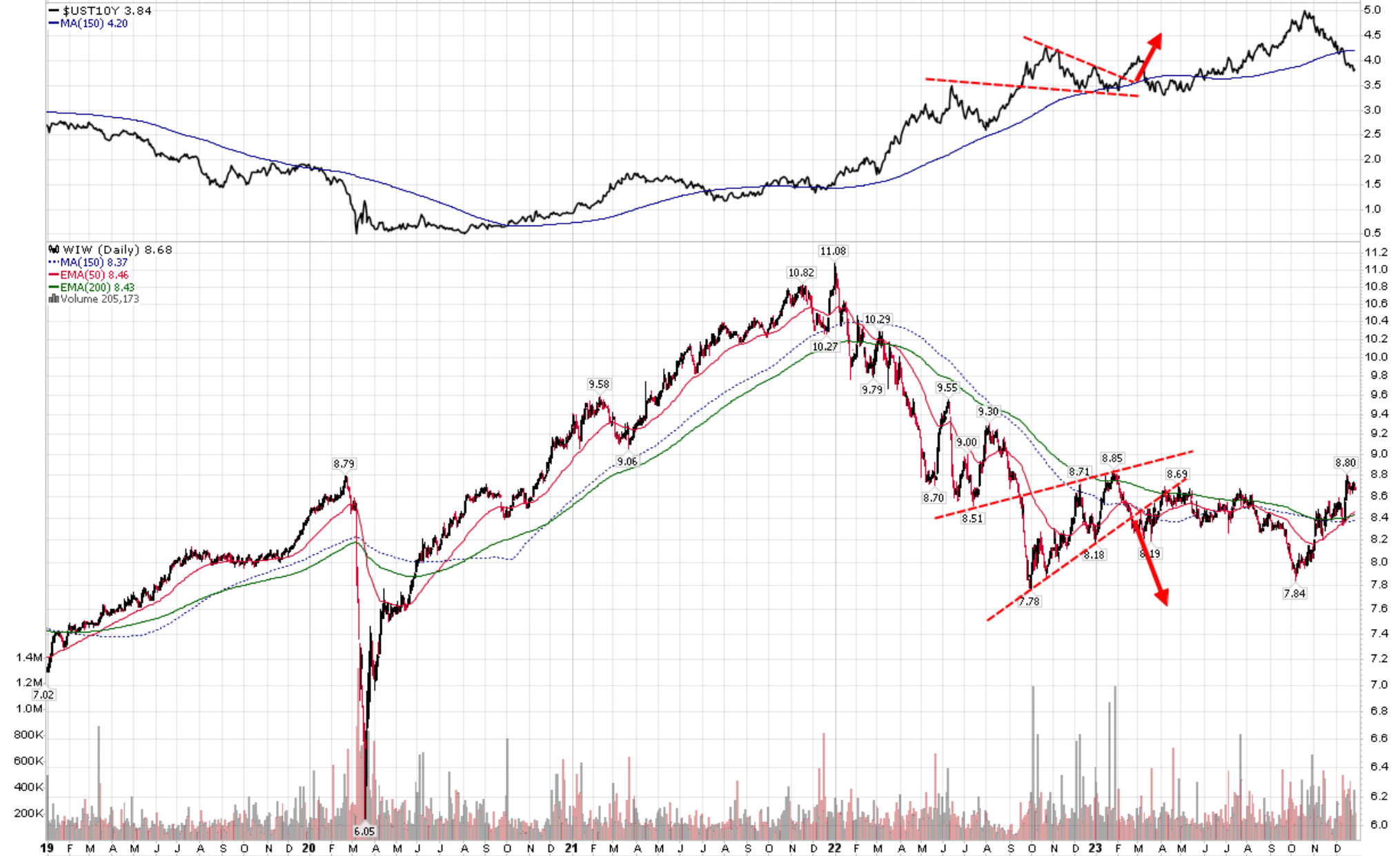

As I predicted, the Federal Reserve stayed on its ‘increased for longer’ message for many of 2023, retaining financial restrictive and performing as a headwind for top period bond funds just like the WIW. The truth is, the WIW fund reached a low of $7.84 in early October, fulfilling my prediction of a re-test of October 2022 lows (Determine 5).

Determine 6 – WIW re-tested October 2022 lows (Creator created with worth chart from stockcharts.com)

Fed Pivot Giving WIW Respite

Nonetheless, in the previous couple of months, with continued progress on the inflation entrance, the Federal Reserve has subtly shifted its place, selecting to carry coverage charges regular since September and messaging that coverage charge cuts could also be within the playing cards for 2024. Chair Powell even mentioned lately that rates of interest “are likely at or near the peak rate for this cycle” throughout his December FOMC press convention.

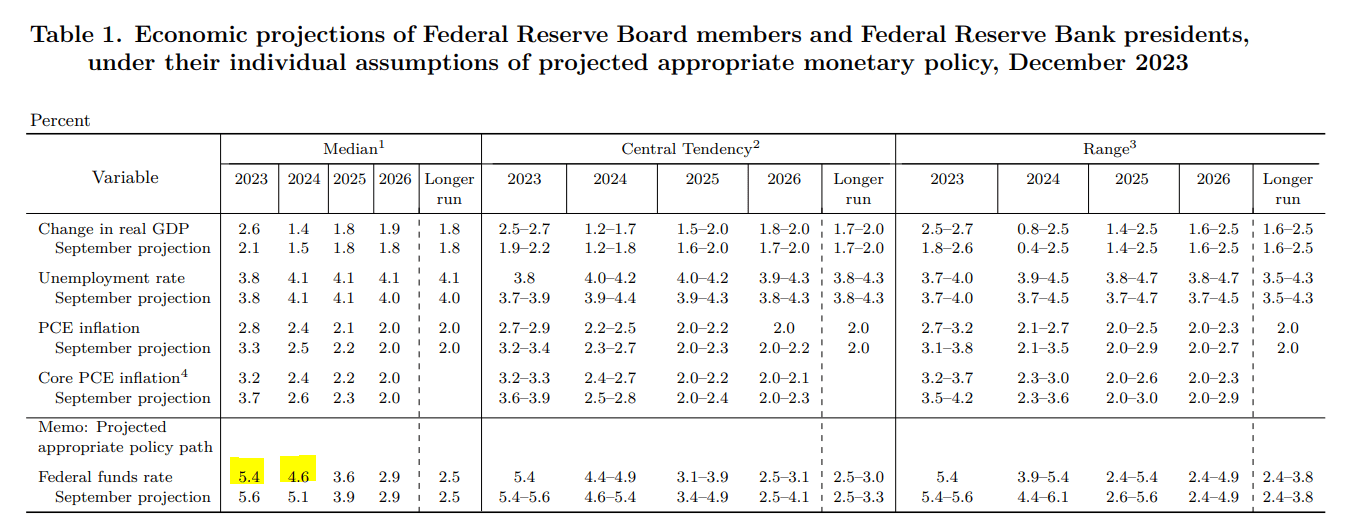

Trying on the Fed’s latest Abstract of Financial Projections (“SEP”), the FOMC committee expects to deliver coverage charges down from the present 5.25%-5.5% stage to 4.5%-4.75% by the top of 2024 (Determine 6).

Determine 6 – FED is forecasting charge cuts in 2024 (Fed Abstract of Financial Projections)

Based on Fed officers, potential coverage charge cuts in 2024 is a pure response to falling inflation, as a result of if the Fed maintain coverage charges regular whereas inflation fell, then actual rates of interest will rise, probably over-tightening the economic system right into a recession.

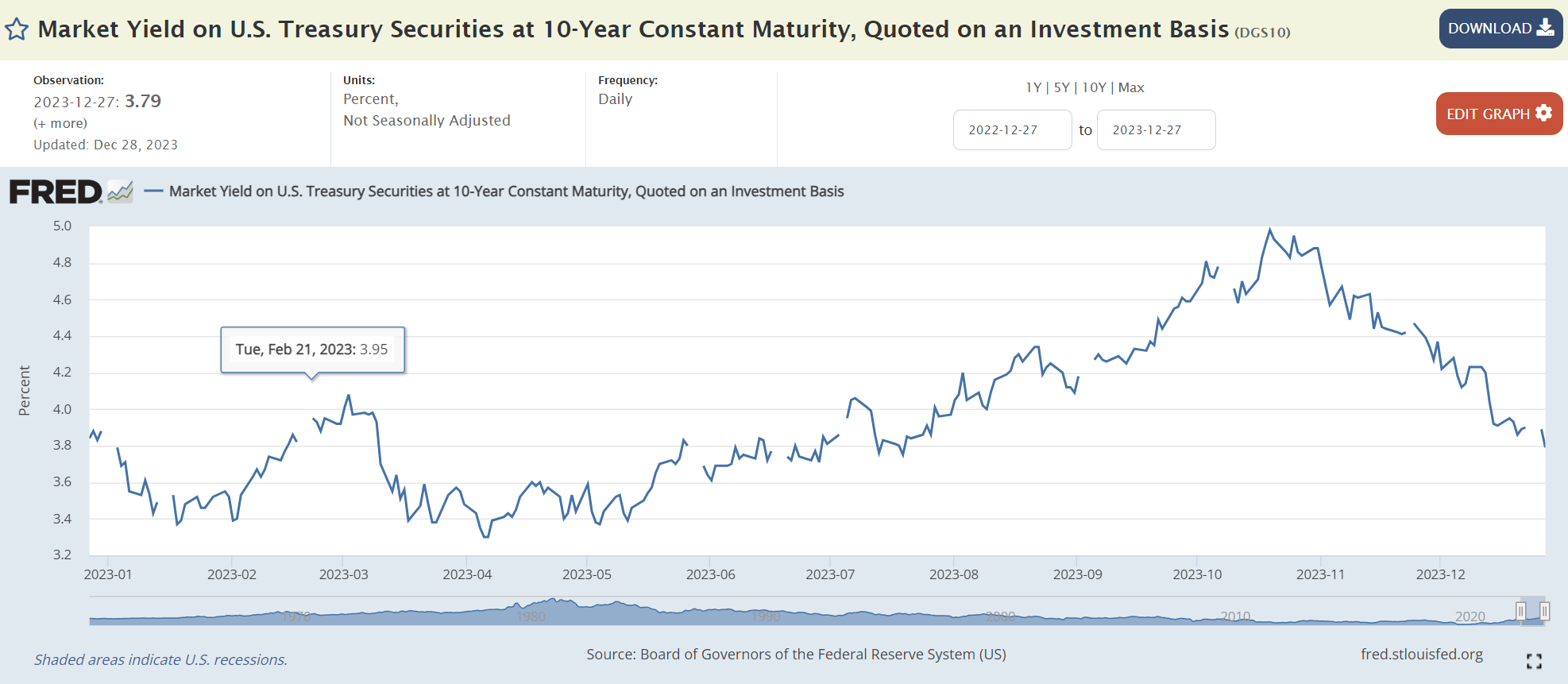

With the Fed formally altering its stance from ‘increased for longer’ to ‘comfortable touchdown’, markets have introduced down long-term rates of interest, with the 10-year treasury yield declining from close to 5.0% to three.8% lately (Determine 7).

Determine 7 – Lengthy-term treasury yields have declined considerably since October (St. Louis Fed)

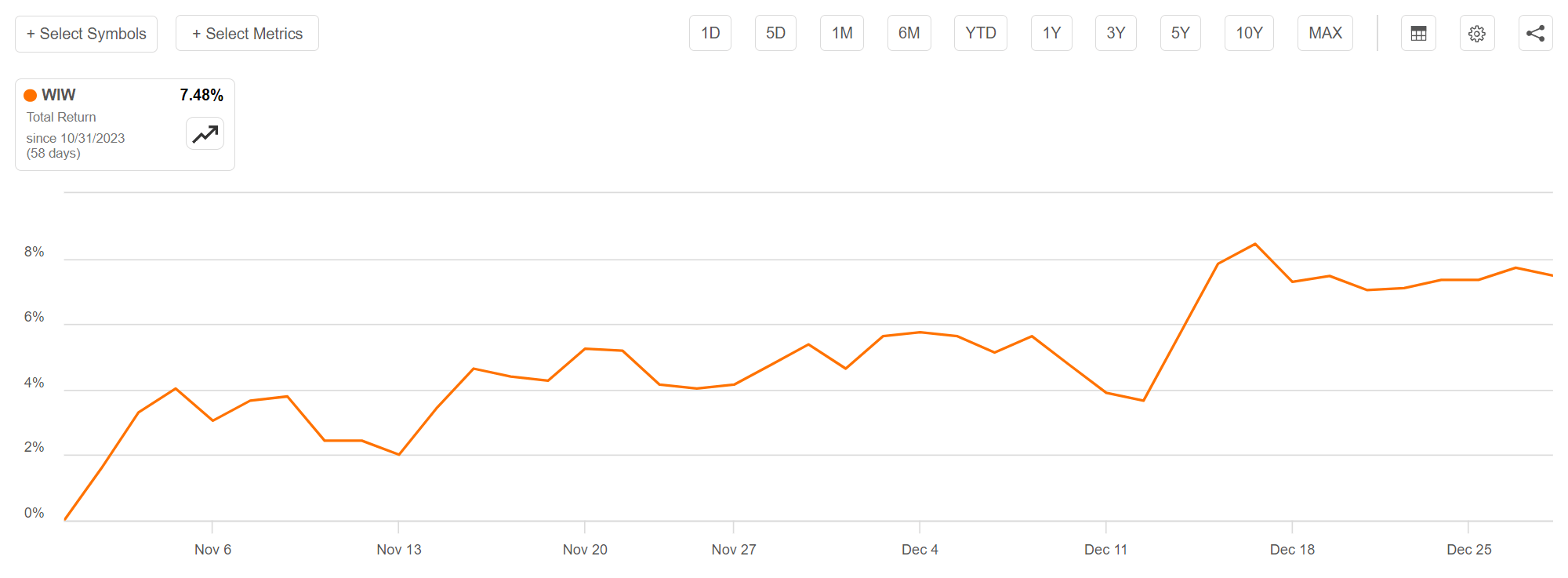

As I wrote in my prior article, a ‘comfortable touchdown’ state of affairs might be goldilocks for the WIW fund, as moderating however nonetheless excessive inflation retains curiosity funds excessive on WIW’s funding portfolio whereas decrease long-term rates of interest increase WIW’s long-duration belongings. Because the finish of October, the WIW fund has rallied 7.5% (Determine 8).

Determine 8 – WIW has rallied on account of the decline in long-term rates of interest (Looking for Alpha)

Bonds Overbought In The Quick-Time period

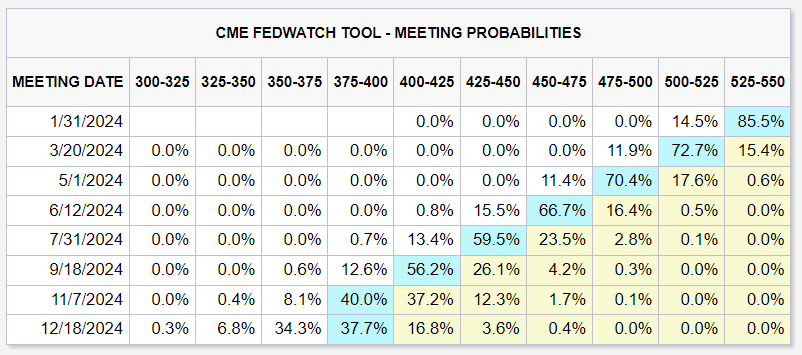

Within the short-term, merchants could have gotten too aggressive, with Fed Funds futures now anticipating the Federal Reserve to chop coverage charges 6-7 occasions in 2024 vs. Fed officers’ estimate of three cuts (Determine 9).

Determine 9 – Merchants getting too aggressive on charge reduce expectations (CME)

Nonetheless, the change within the Fed’s stance is simple and may present a tailwind to long-duration belongings within the coming yr, offered inflation doesn’t make a shock return.

Inflation Is The Wildcard

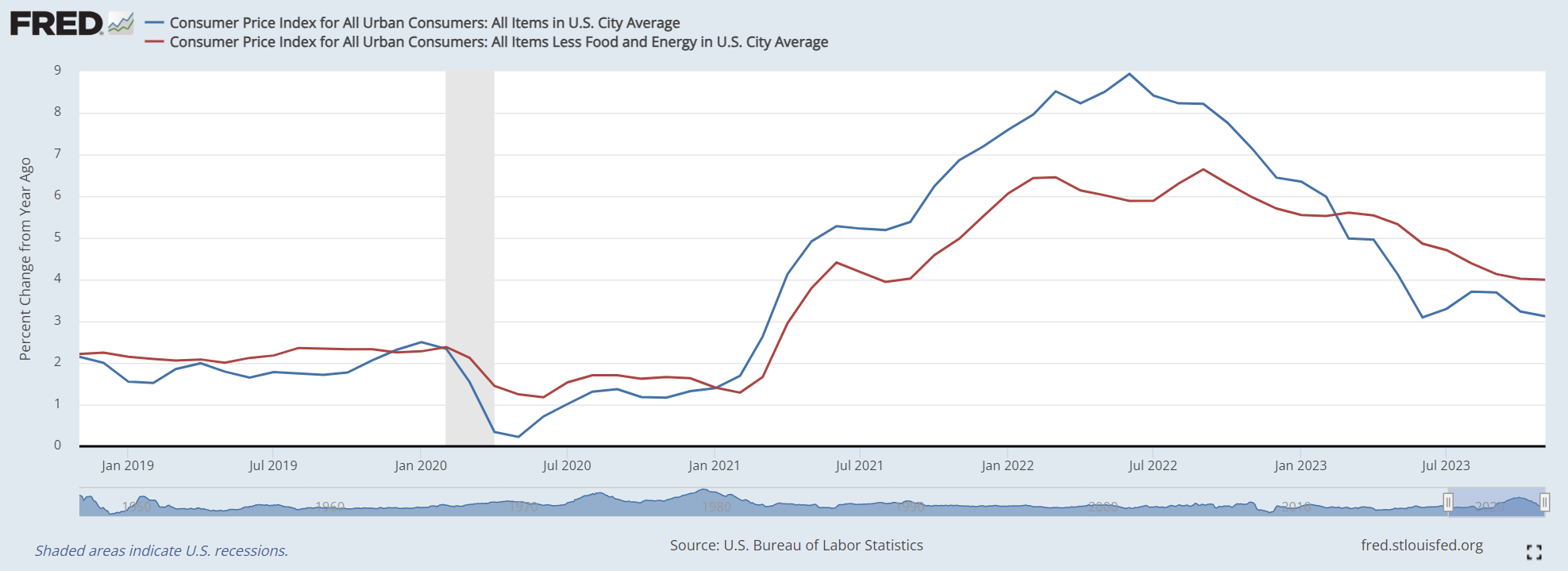

To date, headline CPI inflation has declined properly, trending right down to a 3.1% YoY charge in November and on tempo for the Fed’s 2% goal in late 2024. Nonetheless, the stickier core CPI measure has been far tougher to scale back, with the newest studying nonetheless stubbornly excessive at 4.0% YoY (Determine 10).

Determine 10 – Core vs. Headline CPI (St. Louis Fed)

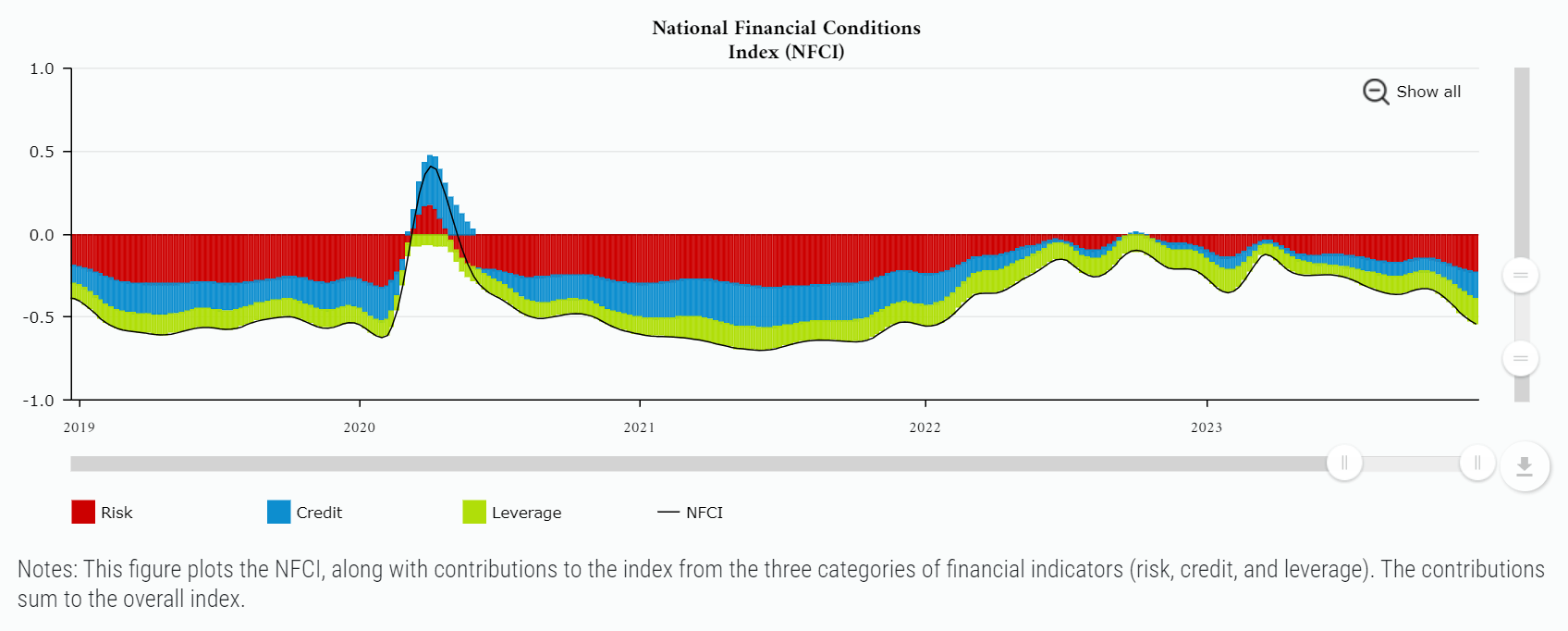

Judging by core CPI, the Federal Reserve could also be untimely in declaring victory and altering its stance, since financial conditions have eased to early 2022 ranges due to the Fed’s dovish pivot (Determine 11).

Determine 11 – Monetary circumstances have eased considerably because of Fed’s pivot (Chicago Fed)

The chance is that loosening monetary circumstances could reignite ‘animal spirits’ and create a second wave of inflation in 2024, throwing a wrench in ‘comfortable touchdown’ narrative and forcing the Fed to restart coverage charge hikes.

Already, we’re seeing indicators of froth, with cryptocurrencies making new 52-week highs and unprofitable idea shares staging spectacular year-end rallies. Bond traders ought to carefully monitor monetary circumstances and inflation indices to ensure inflation isn’t staging a comeback, which would require further financial coverage actions to resolve.

Conclusion

With the Fed lately shifting to a ‘comfortable touchdown’ coverage stance and guiding to charge cuts in 2024, I imagine long-duration bond funds just like the WIW ought to stand to learn. Though bonds are overbought within the short-term, financial coverage tailwinds are undeniably supportive.

The present ‘comfortable touchdown’ state of affairs could also be goldilocks for the WIW fund, as moderating however nonetheless excessive inflation retains WIW’s curiosity revenue excessive, whereas declining long-term rates of interest present capital positive aspects.

The important thing danger for the WIW fund and bond traders on the whole is whether or not the Federal Reserve has declared victory prematurely, loosening monetary circumstances too quickly and permitting inflation to stage a comeback in 2024. If that occurs, we could rue the present bond respite as it can require further financial coverage actions, above and past what has already been enacted, to resolve.

I’m elevating the WIW fund to a purchase for 2024.