Kokkai Ng/iStock Unreleased via Getty Images

Overview of Delivery Hero

Delivery Hero (OTCPK:DLVHF) (OTCPK:DELHY) (“DH”) is a multinational food delivery company that operates 5 different businesses:

-

Asia: DH is operating in Southeast Asia (SEA) via its Foodpanda platform, which is the second-largest delivery platform in the region; and in South Korea via its Baemin/Baedal Minjok platform, Korea’s number 1 food delivery app, and others including Bangladesh, Pakistan, accounting for a smaller portion.

-

Middle East and North Africa (MENA): DH has multiple brands under its umbrella, including Instashop, Hungerstation, and notably Talabat, the leading food delivery platform in the region, with little competition.

-

Europe: Similarly, DH owns multiple brands, consisting primarily of Foodora, rebranded from “Foodpanda” in Mar-23, a leading delivery app in Sweden; Glovo, acquired by DH on Dec-23, the leading delivery app in Spain as of 2022; and other brands including efood and foody.

-

Americas/Latin America (LatAm): Via its PedidosYa brand, DH operates in various markets including Argentina and Chile, where it is the leading food delivery app as of 2022.

-

Integrated Verticals: DH’s integrated vertical, primarily consisting of Dmarts is the companies-owned small warehouses holding thousands of in stocks and inventories. Dmarts promised quick deliveries of goods, such as groceries. This is part of the company’s quick-commerce strategy.

Investment Thesis

Delivery Hero owns an exceptional portfolio of brands across Europe, MENA, LatAm, and Asia that possess a strong competitive edge in terms of market leadership. These include Baemin in Asia (South Korea), Talabat in MENA, Foodora in Europe, and PedidosYa in LatAm. This can be attributed to the management’s strategic expansion into markets with lesser competition, which is more peculiar in regions like Europe and LatAm, where they avoid mature markets such as the UK, Germany, Brazil, and Mexico where competition is high. This has continued to drive strong orders growth, and top-line growth for the company, which in some cases, has surpassed the growth rates of competitors operating in similar regions. This, coupled with a focus on cost efficiency, has helped the company to achieve positive adjusted EBITDA, and FCF breakeven, with further improvements expected in FY24. Considering these positive developments, I will rate Delivery Hero as a buy.

Thoughts on 1Q24 Results & Discussion

Note: I will be evaluating the performance of DH’s business on a constant currency basis, which removes the impact of FX movements.

1) Europe

Northern Europe (Austria, Belgium, Denmark, Germany, Luxembourg, Poland, Slovakia, Switzerland, and the Netherlands), United Kingdom and Ireland, and Southern Europe and ANZ (Australia, Bulgaria, France, Israel, Italy, New Zealand, and Spain).

In the Europe segment, the Group is represented in Armenia, Austria, Bosnia, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Finland, Georgia, Greece, Hungary, Italy, Moldova, Monaco, Montenegro, Norway, Poland, Portugal, Romania, Serbia, Slovakia, Slovenia, Spain, Sweden and Ukraine under local brands which include Glovo, efood, foodora and foody. In addition, Glovo’s operations located in Africa (Ghana, Ivory Coast, Kenya, Morocco, Nigeria, Tunisia, and Uganda) and Central Asia (Kazakhstan and Kyrgyzstan) are also included in the Europe segment.

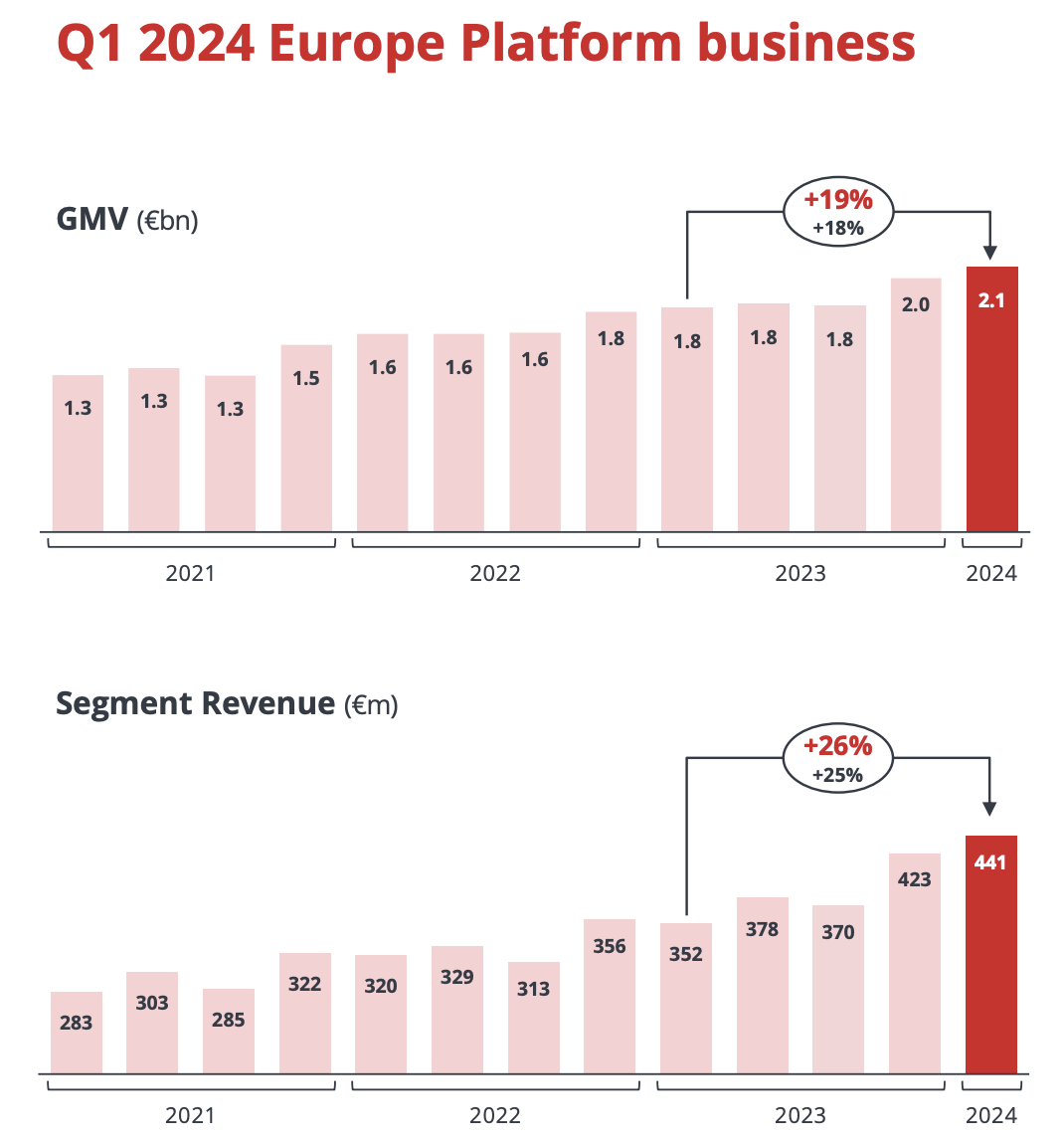

Europe GMV and Revenue

In 1Q24, its Europe platform business grew GMV by 19% YOY, while revenue grew 26% YOY, primarily driven by double-digit order growth and increasing spending from existing customers, and this is an increase from the 17.5% growth in FY23. According to the management, this was driven by double-digit order growth, and increased revenue from Foodora’s subscription plan. Specifically, management states that Glovo demonstrated “outstanding GMV growth” across all countries, and it is expected to achieve positive adjusted EBITDA by 2H24.

Since DH and Just Eat have overlaps in multiple countries, we can compare the two. In 1Q24, Just Eat saw its total order, excluding North America, decline 2.9% YOY, versus DH’s double-digit order growth, highlighting the difference in execution. Note that DH does not compete with its rivals in mature and competitive markets like the UK and Germany, and instead operates in less competitive markets, such as Greece, Finland, Spain (in which Glova is the market leader), Croatia, and many others.

2) Middle East and North Africa (MENA)

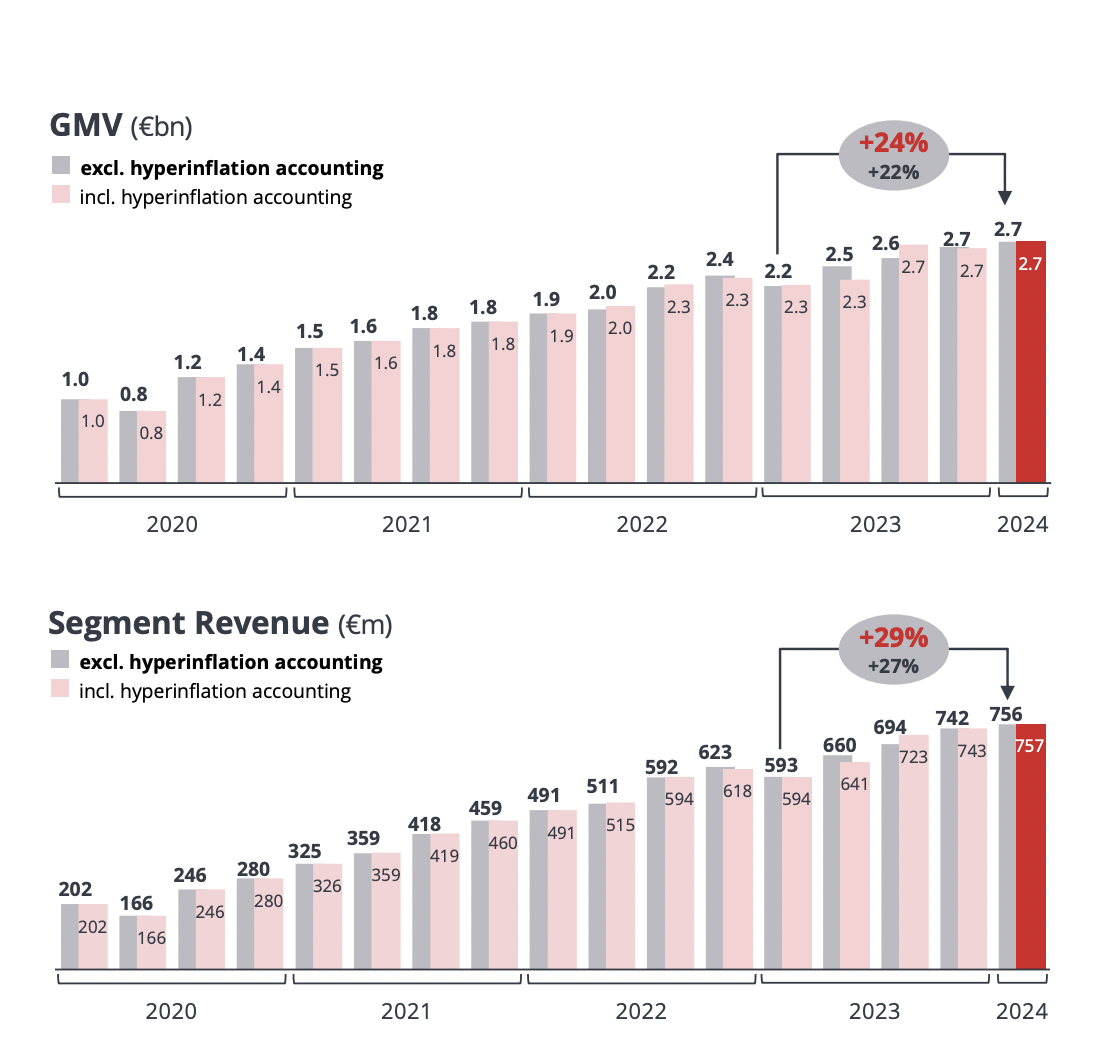

MENA GMV and Revenue

In the same quarter, its MENA platform business’s GMV grew 24% YOY, while segment revenue grew 29% YOY, which is an increase from the 22.7% GMV growth and 27.1% YOY revenue growth in FY23. According to the management, this was attributed to “relentless focus on enhancing their customer experience with product offerings like Dmart, the grocery subscriptions, the royalty programs, kitchen operations, but also credit cards and much more”, which drove healthy orders growth.

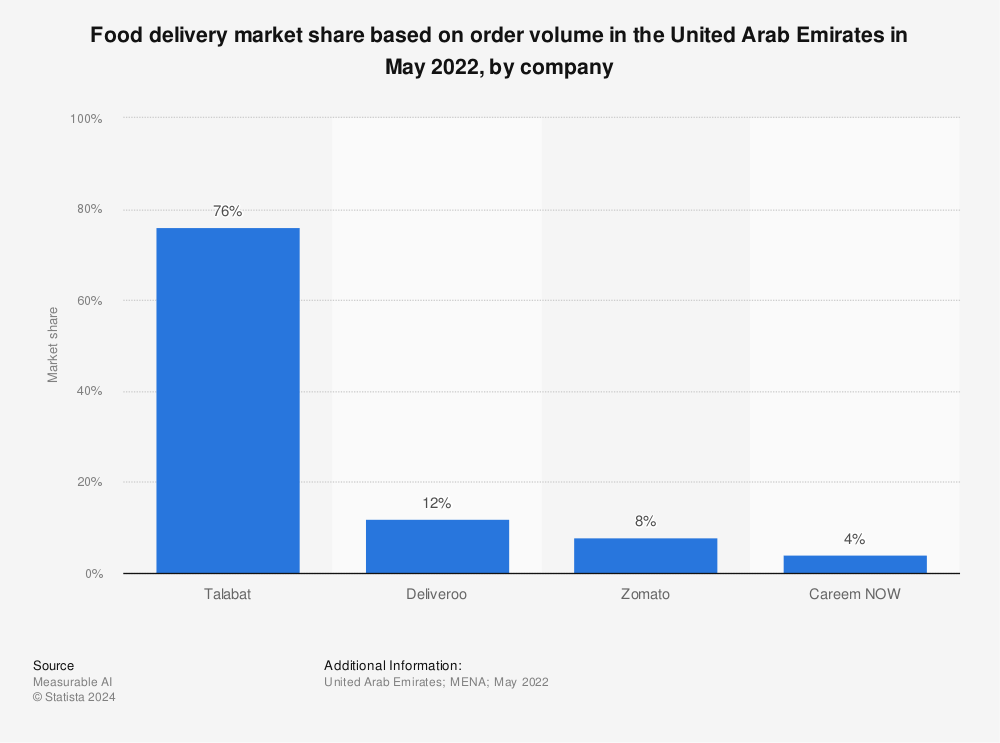

Market Share in UAE as of 2022

It is also worth noting that DH’s Talabat is the leading food delivery platform in the region, commanding a massive market share of 76% as of May 2022, which contributed to the continued strong growth of this business.

3) Americas/Latin America

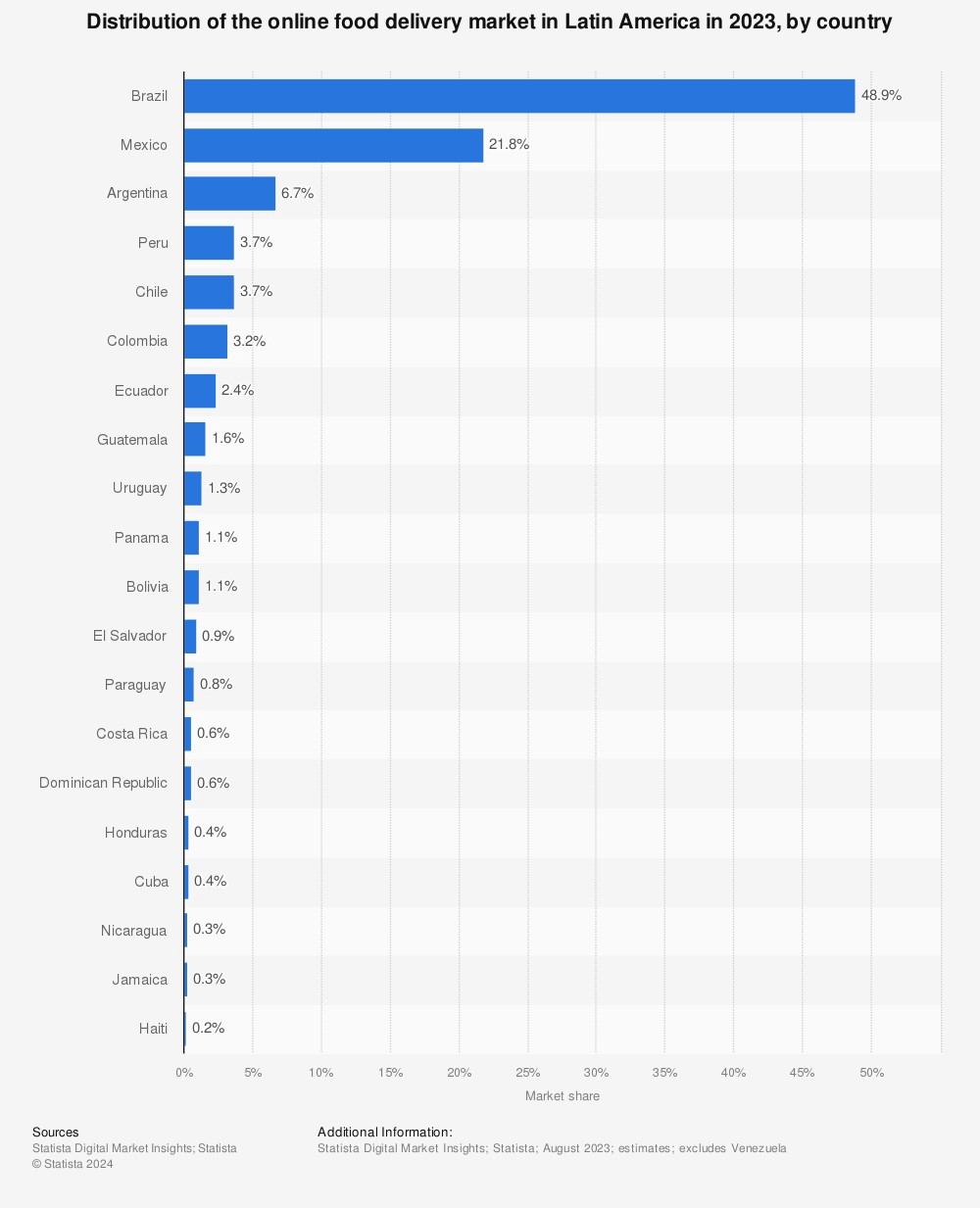

Distribution of food delivery market in LatAm in 2023

Before diving into its results, I thought I’d dive into the competitive landscape in Latin America (LatAm) to highlight how DH differentiates itself from its competitors. According to Statista, competitors in the region include:

-

Movile’s iFood: Leading food delivery app in Brazil, and the top app overall in LatAm. Brazil is LatAm’s largest market.

-

DiDi’s DiDi Food: The leading app in Mexico, the region’s second-largest market

-

Rappi: The Leading delivery app in Colombia, which is the sixth-largest market in the region

On the contrary, DH does not compete in mature and competitive markets like Brazil and Mexico. Instead, it operates in other markets where competition is less intense, including Argentina and Chile, where it established itself as the leading food delivery app. According to the table above, Argentina and Chile are the third and fifth-largest markets in the region.

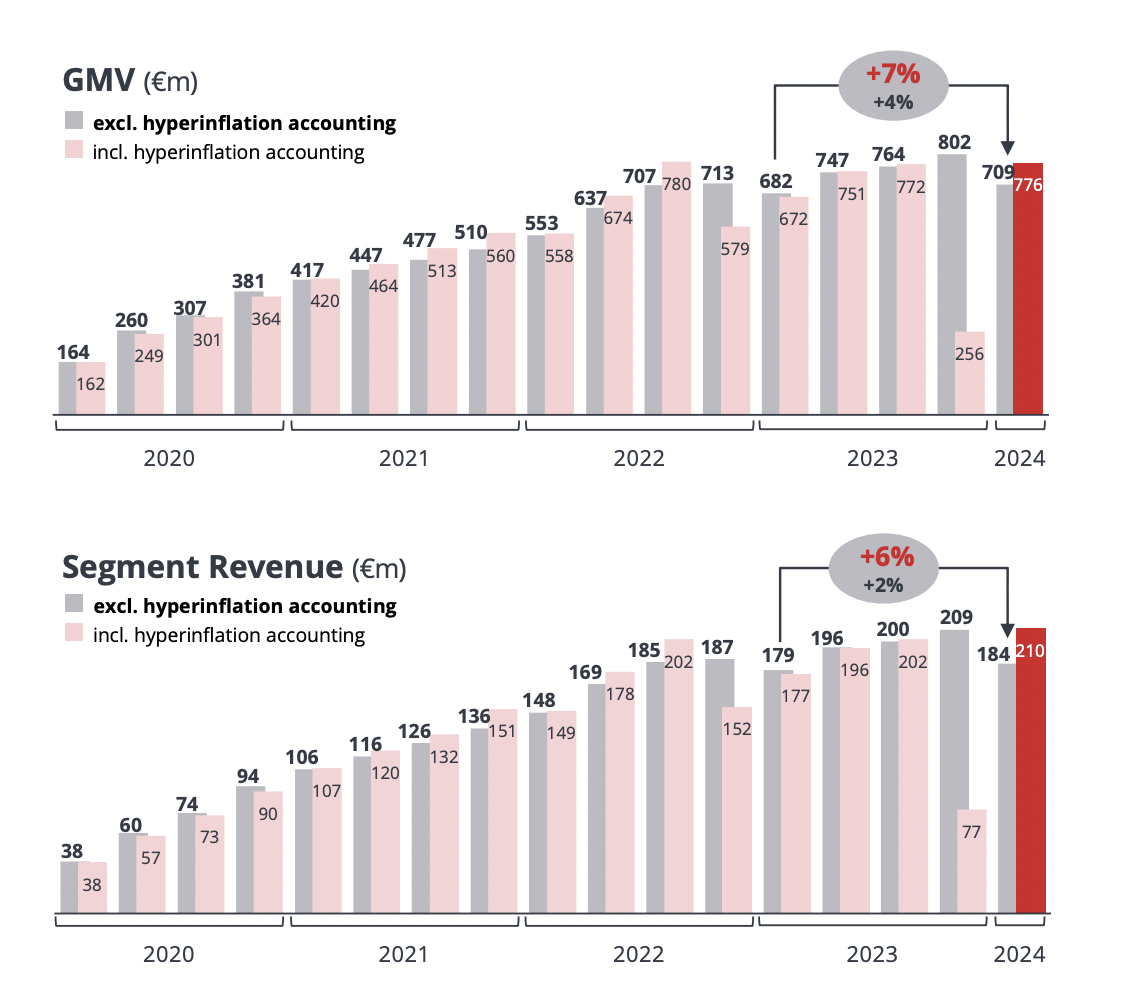

Latin America GMV and Revenue

During the quarter, DH delivered GMV growth of 7% YOY, while revenue grew 6% YOY. While this seemed like an underperformance, the business has delivered double-digit growth in 12 out of the 15 countries it operates in, and partially, its high-margin advertising business. However, this was offset by the poor performance of the Argentina market which is suffering from severe macro headwinds, characterized by high inflation rates that have led to extreme surges in the cost of goods and services, negatively impacting consumers’ spending power and driving up poverty. During the 1Q24 earnings call, management noted that while Argentina’s basket size remained muted, they did notice a slight recovery in order volume. Since Argentina is the region’s third-largest market, this also explains the material impact on its growth.

4) Asia/APAC

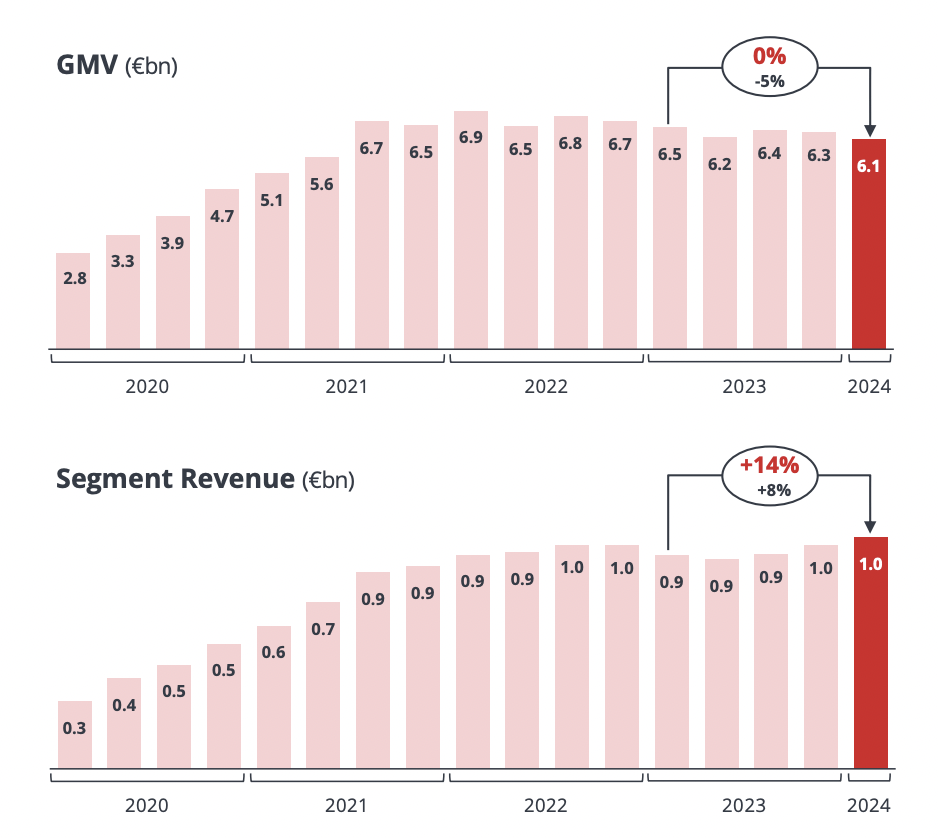

Asia GMV and Revenue

As of 1Q24, despite delivering a flat GMV growth of 0% from 1Q23, its revenue grew 14% YOY to $1 billion. According to 1Q24 earnings call, this is driven primarily by its growing, high-margin advertising business, which currently makes up 3.4% of its total APAC’s GMV, up from 2.7% in 1Q23, as well as its increased usage in DH’s delivery system (their own fleet of riders). In comparison, Asia is a region they have struggled with as the competitive landscape, especially in South Korea, has been heating up.

In Korea, there are three main players: Baemin/Baedal Minjok platform, the market’s leading food delivery platform, followed by Coupang Eats and Yogiyo. According to Pulse by Maeil Business News Korea, these three platforms are competing for market share through their offerings of free delivery services. Management in their 1Q24 earnings call stated that this move harmed their category position and growth, although they had taken steps to mitigate these losses. This competition is expected to intensify and prolong further, as Coupang Eats does not seem to be resting on its laurels. As Coupang, its parent company, owns the largest e-commerce logistic infrastructure in Korea, it is important for DH’s management to not underestimate the threat of Coupang.

Meanwhile, in Southeast Asia, Grab (GRAB) is a market leader (which I have covered extensively in my recent article) that is growing its food delivery revenue at a higher rate than DH’s Asia GMV growth, suggesting that DH is losing market share to Grab. Furthermore, they have also previously explored the sale of its Foodpanda units in SEA, which was terminated in Feb 2024. However, they remain open for sale if only they can create value for shareholders. In my opinion, this suggests their willingness to exit the market to concentrate on regions where they are more established. This can be seen in May 2024 as DH sold its Foodpanda unit in Taiwan to Uber for a total consideration of $950 million, of which the proceeds will be used to pay off its debt. However, this also supports my theory that DH is trying to exit markets where it lacks a significant presence.

5) Integrated Verticals

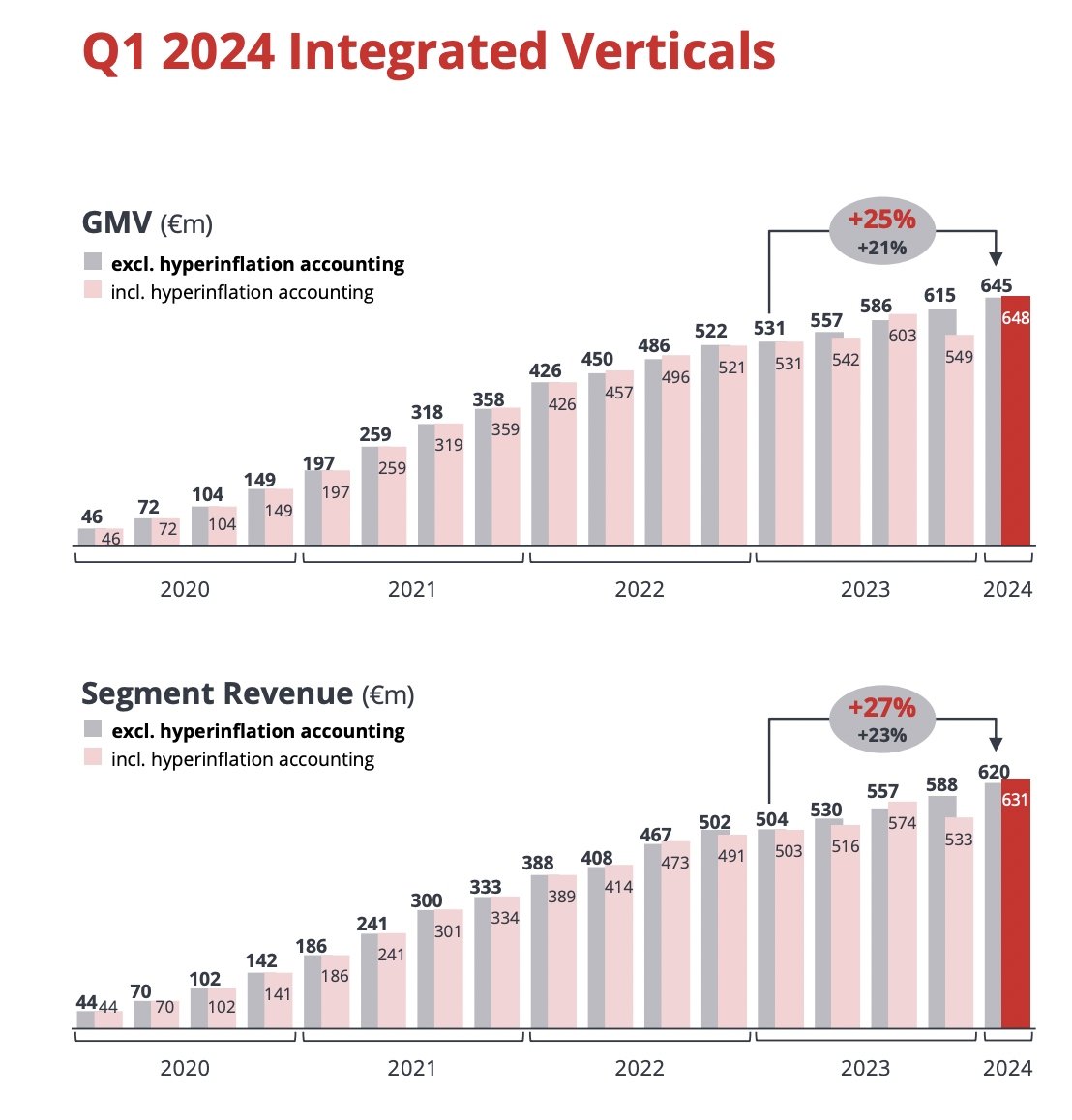

Integrated Vertical GMV and Revenue

In 1Q24, its GMV and revenue grew 25% and 27%, respectively, on a YOY basis. This is an increase from 17% GMV growth and 20% revenue growth in FY23. According to the management, they have made a conscious effort to downsize their operations by closing down 200 unprofitable stores in the last 12 months. As of 1Q24, they have 895 Dmarts. This tells me they have been more efficient in running Dmarts as they generate higher growth despite the drop in the number of stores. This was driven by increased customers’ spendings, smarter pricing on products and service fees, more SKUs, and reduced picking time. This improved sales efficiency has led to Dmart achieving a positive gross profit margin by 1H23, and now, they are on track to reach EBITDA breakeven by the end of FY24. This contributed to the company’s overall gross profit and EBITDA, which I will discuss next.

Profitability

Non-GAAP Profitability

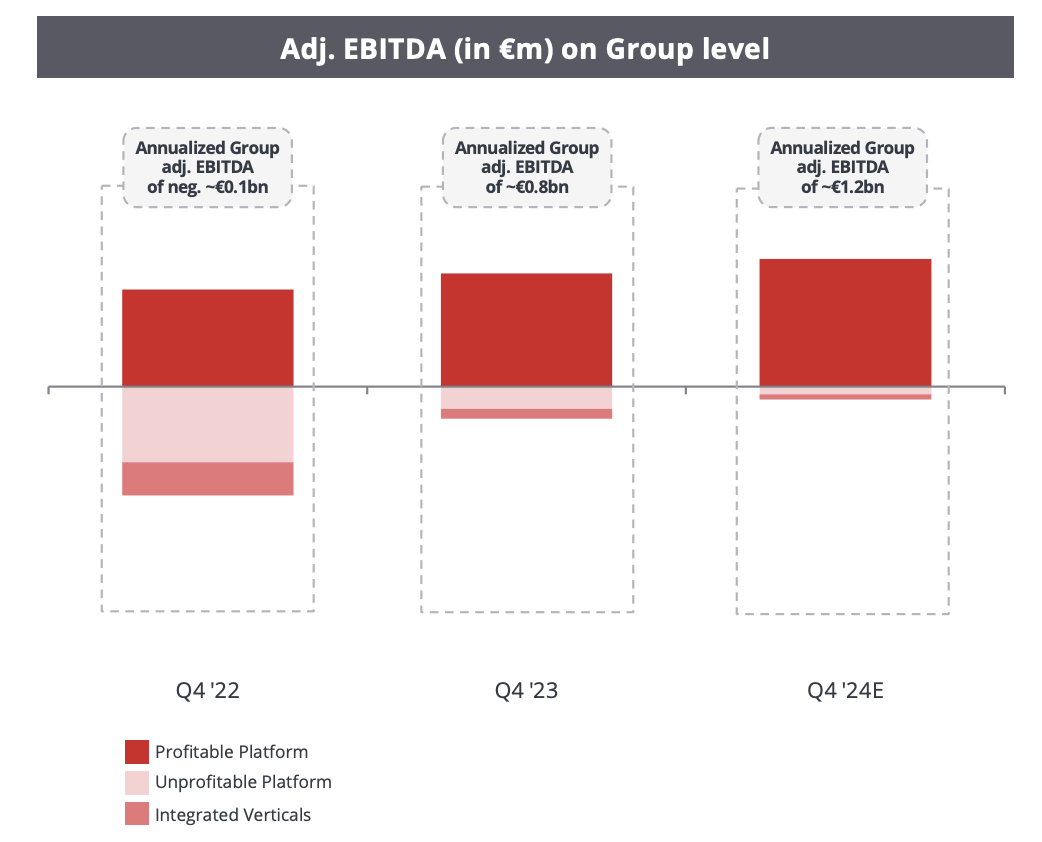

Note that the management did not disclose its adjusted EBITDA for 1Q24.

As of 4Q23, its annualized adjusted EBITDA has reached a total of $0.8 billion, a massive improvement from -$0.1 billion last year. These adjusted EBITDA improvements were driven by several factors, which apart from the improved sales efficiencies, and higher gross margins of its integrated vertical business, the increase in high-margin advertising revenue in its Asia and Americas platform businesses, as well as the strong top-line growth across all of platform businesses, this is also primarily attributed to the improved G&A expenses, which as a proportion of GMV, has declined from 4.4% in FY22 to 4% in FY23. This is expected to further decline in FY24, and according to management, this was driven by reduced headcounts, the closure of tech hubs in Turkey and Taiwan, and the streamlining of business teams.

By the end of FY24, management is targeting an EBITDA of $1.2 billion, up 50% from $0.8 billion in FY23. Based on their FY24 midpoint guidance of 8% GMV growth, this should generate a GMV of $48.9 billion by FY24, implying an EBITDA margin of ~2.5% by FY24.

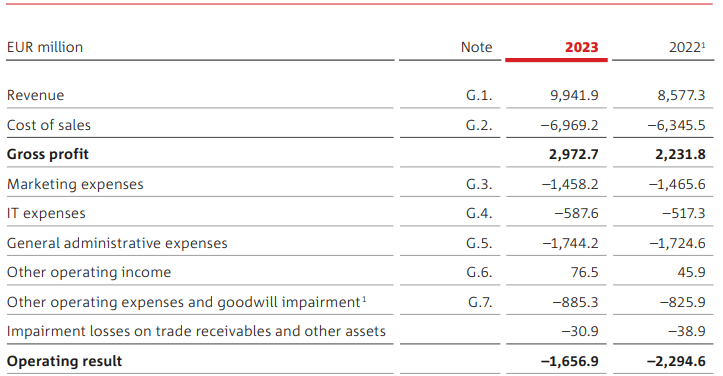

FY23 Income Statement

However, DH is still unprofitable on a GAAP profitability basis. In FY23, its EBIT margin is -16.7%, down from -26.8% in FY22.

Balance Sheet and Cash Flow

Debt Profile

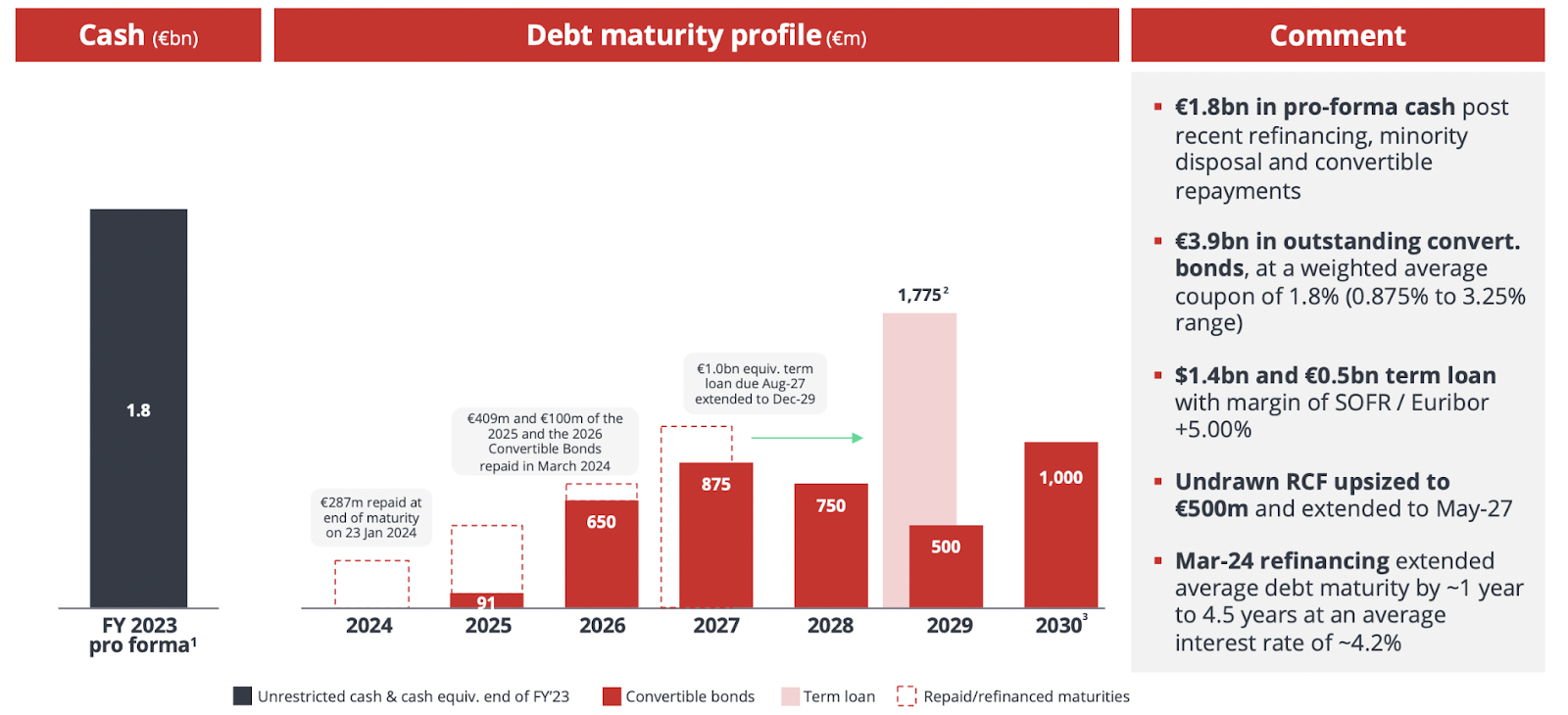

DH’s management has taken steps to improve its balance sheet. In Mar 2024, management successfully optimized its capital structure, and these are the following key events:

-

There is an existing EUR 1.1 billion term loan, and this is broken down into USD 813 million term facility (existing US term facility), and EUR 300 million term facility (existing EUR term facility). Specifically, the existing USD 813 million term facility’s interest rate is reduced from 5.75% to 5%, and the existing EUR 300 million term facility will be replaced by a new EUR 550 million term facility. Additionally, their maturity date has been extended from Aug 2027 to Dec 2029.

-

They raised an additional EUR 500 million term facility. Of this, 300 million is used to purchase its convertible bonds due in 2025 and 2026. According to the slide, they have successfully repaid EUR 409 million for the 2025 bond and $100 million for the 2026 bond.

Of the total outstanding loan of EUR 3.9 billion, the next payment date is due in July 2025, which amounts to EUR 91 million, followed by EUR 650 million in 2026. After the successful refinancing, disposal of its Foodpanda unit in Taiwan, and bond repayments, they have a pro forma of $1.8 billion of cash, as of FY23, which is sufficient to repay its upcoming 2025 and 2026 bonds. Management states that they are “in the comfortable position to repay all of our debt maturities organically over the coming years through our own cash flow”.

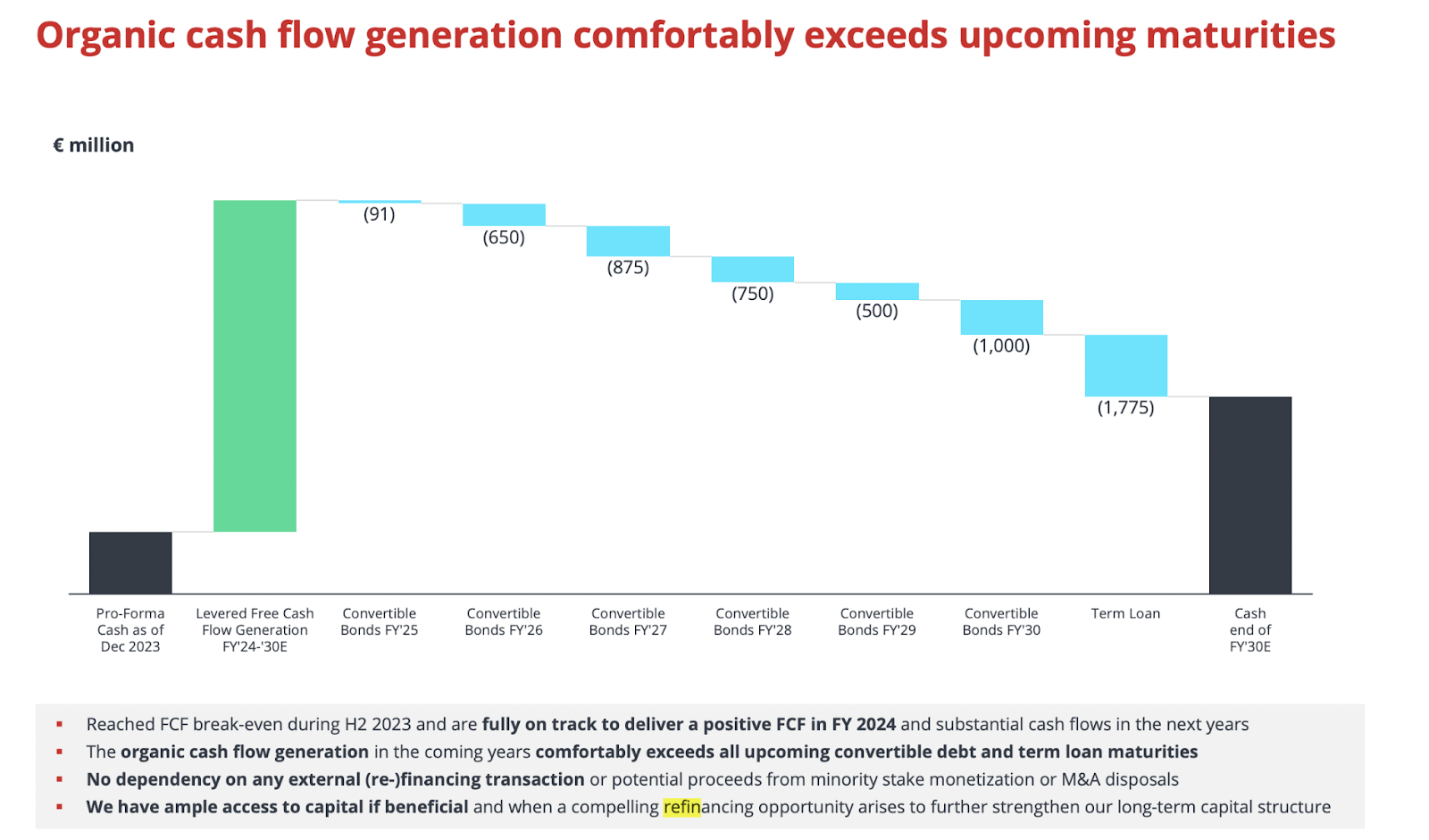

Long term Cash Flow

Shifting to cash flow, the company has attained positive FCF during 2H23 and is on track to deliver FCF positive for FY24. They are confident in generating ample FCF from FY24 to FY30 to repay their convertible bonds and improve their liquidity position. Furthermore, this is not dependent on further refinancing or proceeds from its disposal of business units, and it will continue to explore potential refinancing opportunities to optimize its capital structure.

Relative Valuation

Relative Valuation

These are the list of companies I’ve picked that share the same business model, and operate in similar industries. Do note that while Uber and Grab are not direct comparisons, as they own multiple businesses that operate in different industries, such as ride-hailing, I do think that they still serve as a good benchmark on where DH’s valuation stands.

Based on DH’s TTM EV/Sales of 1.2x, this is priced at a significant discount below DoorDash, Uber, and Grab, while trading at a multiple above Just Eat. In my opinion, these could be attributed to a few reasons:

-

Markets like MENA and LatAm have higher default risks and risk premiums, which is especially pronounced in countries like Argentina, investors have likely priced this in when valuing DH.

-

Intense competition in Asia, particularly in SEA and South Korea, and the lack of clear market leadership in SEA.

-

Lower GAAP profitability than most of its peers

-

More robust execution than Just Eat in terms of order growth and profitability

-

The market has factored in balance sheet risk, as poor execution or unpredictable events like increased competition may slow down its growth and profitability, which may hinder its ability to generate sufficient FCF to repay its debt.

Conclusion

In conclusion, DH executed well in 1Q24, delivering robust top-line growth, except for its Asia business platform, and EBITDA improvements across the company. This is a testament of management’s execution, a strong portfolio of brands, and strategic expansion into less competitive markets. Moreover, they have successfully executed their refinancing to improve their balance sheets, and are on track to deliver positive FCF by FY24. However, investing in the company is not without risks such as the intense competition in South Korea, and balance sheet risk. Taking into account all of these, I am rating DH as a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.