DaLiu

Deutsche Telekom (OTCQX:DTEGY) has good fundamentals within the European telecom sector, however this appears to be presently mirrored in its valuation and its shares are subsequently a ‘Maintain’.

As I’ve lined in a previous article, Deutsche Telekom has higher progress prospects than most of its friends, as a result of its sturdy massive publicity to the U.S., by way of its stake in T-Cellular US (TMUS). As I’m an income-oriented investor, I used to be not a lot attracted by its below-average dividend yield, however its shares have outperformed most of its closest friends since my final article, exhibiting that Deutsche Telekom’s funding case is principally geared to progress somewhat than revenue.

On this article, I replace the corporate’s most up-to-date monetary efficiency and its funding case, to see whether it is presently a great progress decide within the European telecom sector or not.

Monetary Overview

Deutsche Telekom has reported a constructive working atmosphere over the previous few quarters, supported by its a number of enterprise items, though T-Cellular continues to be its main progress engine. The corporate continues to profit from its technique to spend money on infrastructure, specifically in its 5G community within the U.S., which has been a particular issue over its opponents Verizon (VZ) and AT&T (T). This has enabled T-Cellular to report sturdy buyer progress and market share good points over the previous couple of years, a pattern that has not reversed in latest quarters.

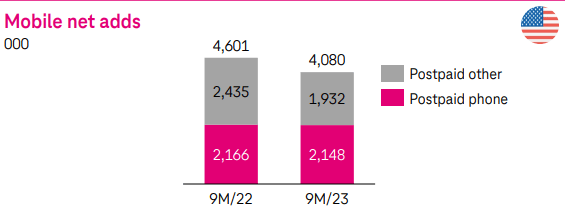

This backdrop explains why Deutsche Telekom continues to report sturdy progress within the U.S., as T-Cellular was in a position to develop its web buyer rely by greater than 4 million within the cellular phase, throughout the first nine months of 2023, nonetheless an excellent consequence though its progress has slowed down in comparison with the identical interval of the earlier yr.

Internet provides (Deutsche Telekom)

This was a powerful help for service income progress, which was up by 3.6% YoY in Q3 2023, however this was not sufficient to offset decrease income from gear income. Certainly, gross sales of smartphones have been weak over the previous few quarters throughout the trade, justified by rising rates of interest and better value of dwelling, resulting in general T-Cellular revenues of $19.2 billion within the final quarter, a decline of 1.3% YoY.

In different geographies, Deutsche Telekom additionally reported constructive buyer progress, particularly in broadband and TV, resulting in group service income progress of three.3% throughout 9M 2023. Nevertheless, as a result of decrease gear gross sales, general group income was €82.6 billion within the first 9 months of the yr, a decline of two.4% YoY.

Regardless of decrease reported income, its profitability elevated a bit of bit as a result of decrease prices, additionally impacted by the deconsolidation of GD Towers its tower enterprise in Germany and Austria, by which Deutsche Telekom bought 51% of its possession to DigitalBridge and Brookfield. Its adjusted EBITDA in 9M 2023 was almost €30.5 billion, a rise of 0.8% YoY, boosting its EBITDA margin to 36.9%.

As a result of sale of GD Towers and its Dutch enterprise, which impacted its web revenue by €11 billion, its reported revenue was almost €19 billion in 9M 2023 (vs. €7 billion in 9M 2022), however adjusted for this impact, its web revenue amounted to €6.1 billion (-13.8% YoY). This drop is principally defined by constructive one-off results within the earlier yr, which boosted its web revenue, making annual comparisons harder for the corporate. Relating to its money circulation era, Deutsche Telekom has determined to scale back its capital expenditures, which amounted to €13.4 billion in 9M 2023, a decline of 13% YoY, being a decisive issue for greater free money circulation throughout the interval to €11.8 billion (+25% YoY).

Given this sturdy backdrop throughout its companies, Deutsche Telekom raised once more its steering for the total yr, anticipating to realize an adjusted EBITDA of about €41.1 billion in 2023 and its free money circulation to be above €16.1 billion, barely up from its earlier steering as proven within the subsequent graph, exhibiting that its constructive working momentum is anticipated to proceed in This fall.

Key monetary metrics (Deutsche Telekom)

Relating to its stability sheet, Deutsche Telekom’s web debt was €137 billion on the finish of final September, down by greater than €5 billion throughout 9M 2023, primarily as a result of its web proceeds from the sale of its stake in GD Towers. The mixture of barely greater EBITDA and decrease web debt, led to a declining leverage place, reporting a web debt-to-EBITDA ratio (together with leases) of two.94x on the finish of final quarter. That is nonetheless considerably above the sector’s common and the corporate’s personal desired vary of between 2.25-2.75x over the medium time period however contemplating its good money circulation era capability and progress prospects, I feel Deutsche Telekom will be capable to scale back leverage organically to its desired vary over the following few years.

This implies Deutsche Telekom doesn’t must retain a lot money to strengthen its stability sheet, enabling it to distribute a great a part of its earnings and money flows to shareholders. Certainly, this has been its coverage in latest quarter, each at its T-Cellular unit and on the group stage. On account of share buybacks, its stake in T-Cellular has elevated in latest quarters and the corporate has now reached a majority stake within the U.S. enterprise, holding a 52.1% stake on the finish of final September. This was a strategic purpose for Deutsche Telekom and one thing it has been working for throughout the previous three years, from its 43% stake in 2020 when T-Cellular US merged with Dash.

T-Cellular US additionally began to distribute dividends within the final quarter, anticipating to distribute some €3.75 billion between This fall 2023 and the tip of 2024. Deutsche Telekom subsequently expects to obtain some €1.8 billion in dividends after tax throughout this era, which is a vital help for its personal dividend and stability sheet deleveraging efforts.

Associated to its 2023 earnings, Deutsche Telekom has already introduced that it intends to distribute an annual dividend of €0.77 per share, a rise of 10% in comparison with the earlier yr, anticipated to be paid subsequent April. At its present share worth, Deutsche Telekom’s ahead dividend yield is about 3.4%, which stays decrease than its closest friends, thus its revenue attraction shouldn’t be implausible proper now in comparison with different telecom corporations and different fixed-income options, equivalent to bonds or banking deposits.

Conclusion

Deutsche Telekom has maintained a constructive working efficiency throughout the group in latest quarters, with the U.S. remaining its important progress engine. This profile shouldn’t be anticipated to alter a lot within the close to future, contemplating that present avenue estimates anticipate Deutsche Telekom to take care of a single-digit income and earnings progress path within the coming years.

Which means within the telecoms sector, Deutsche Telekom presents above-average progress prospects, as most of its friends wrestle to develop their companies. On account of this totally different profile, Deutsche Telekom doesn’t provide the identical revenue attraction as a few of its friends, making its funding case principally geared for progress.

Relating to its valuation, Deutsche Telekom is presently trading at some 12.2x ahead earnings, virtually according to its historic valuation over the previous 5 years of 12.8x. Thus, though it has higher progress prospects than most telecom corporations, its shares don’t look like undervalued proper now and are a ‘Hold’ in the interim.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.