GlobalStock

After a brutal begin to the yr, Devon Power (NYSE:DVN) has lastly bounced following strong earnings. The home power firm has turn out to be a money stream machine returning a lot of capital to shareholders, making the inventory interesting to purchase on weak spot contemplating the risky power sector. My investment thesis is extremely Bullish on the power firm at this valuation.

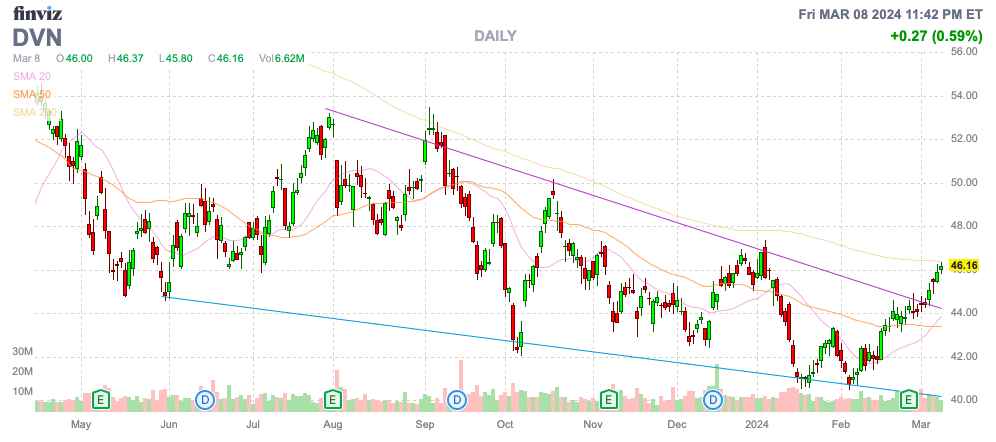

Supply: Finviz

Improved Effectivity

Whereas Devon Power grew oil volumes 8% in 2023 to 317 m/bod, the corporate truly lower capital spending plans for 2024 by 10%. The objective is to maintain oil volumes at 315 m/bod with capital spending dipping to $3.45 billion.

The corporate is not chasing the market with aggressive spending as a way to seize extra market share even with OPEC+ sustaining production cuts of two m/bod. Devon Power will permit manufacturing volumes to presumably even dip in 2024 to solely 650,000 m/boed in comparison with the 662,000 m/boed produced final yr.

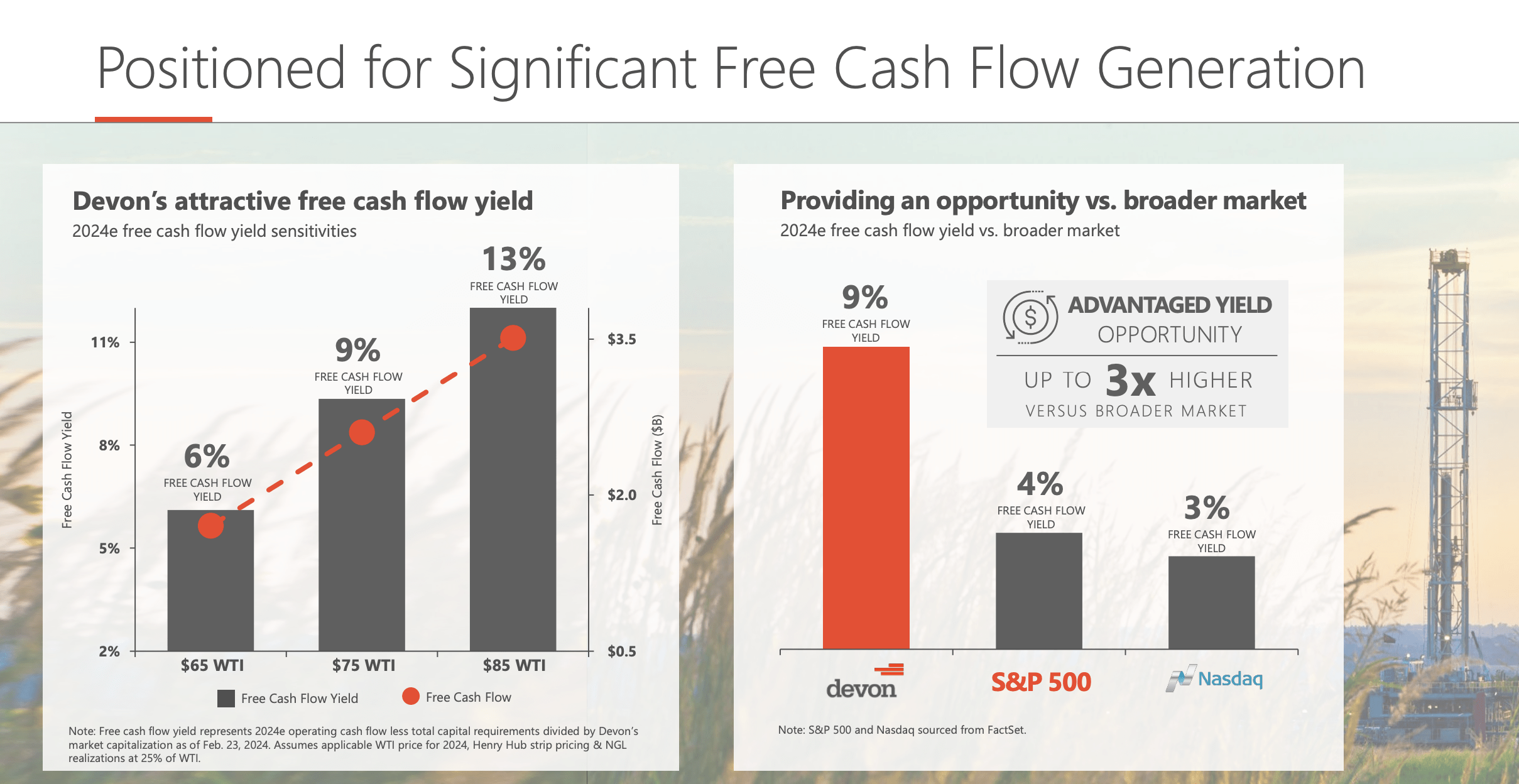

Devon Power suggests breakeven funding at ~$40 per barrel of oil at WTI costs. Resulting from this low breakeven stage, the corporate is ready to generate substantial free money stream, providing a virtually 10% yield on the present market cap with WTI costs round $80/bbl.

Supply: Devon Power This fall’23 presentation

Because of the constant money flows from the upper capital effectivity from specializing in the Delaware Basin whereas producing higher ends in the Williston Basin and Eagle Ford, the corporate simply hiked the fastened dividend by 10% to $0.22. The full Q1’24 dividend payout will likely be $0.44 for an annual payout of $1.76. Devon Power solely ensures the fastened dividend with a yield of 1.9%, however buyers are nearly assured greater payouts on present oil costs together with inventory buybacks.

The hiked fastened dividend solely quantities to ~$600 million in annual payouts. Devon Power produced $2.7 billion in free money stream in 2023 and decrease capital spending ought to increase money flows in 2024 whereas the corporate forecast returning 70% of capital to shareholders.

The inventory might positively fall again to the lows at $40, however Devon produced sturdy outcomes again in This fall’23 when oil costs had been decrease. The power firm had realized oil costs of practically $77/bbl in This fall, whereas the corporate survived solely $72/bbl again in Q2’23 when pure gasoline costs had been $1.66/mcf.

Devon was nonetheless capable of generated $1.4 billion in working money flows again within the June quarter. The corporate might nonetheless soak up far decrease power costs, although pure gasoline costs could not maintain decrease costs and WTI is not more likely to keep beneath $70/bbl for lengthy with OPEC+ cuts.

The inventory solely has a market cap of $29 billion for an organization with $6+ billion in working money flows and a $5+ EPS. By each metric, Devon Power is reasonable and power costs are nearer to the lows than a premium stage the place dangers to the draw back are extreme.

An investor can construct a strong place on the present low cost ranges and get a dividend usually working at double the present fastened fee. Again after the weaker Q2 outcomes because of decrease oil costs, Devon Power truly paid a variable dividend of $0.29 on prime of the fastened fee of $0.20.

The mixed $0.49 quarterly dividend would equate to a 4.2% dividend yield. Lately, administration has proclaimed a need to prioritize the share buybacks program on the present inventory valuation.

Devon Power purchased 5.2 million shares for $234 million through the December quarter. The corporate has decreased the diluted share rely from 677 million on the finish of Q3’21 to solely 636 million on the finish of 2023. Devon has decreased the share rely by 6% throughout a interval the place the corporate was extra targeted on dividend payouts, providing perception to the potential for a bigger discount within the excellent share rely.

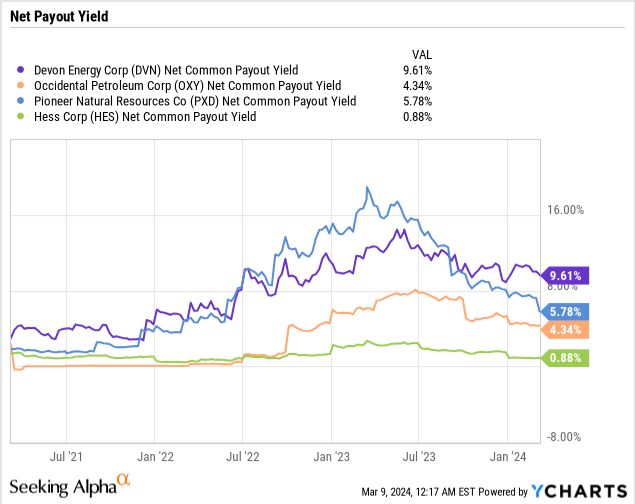

Yielding The Most

Over the previous couple of years, Devon Power has persistently provided shareholders among the best internet payout yields. The present yield is almost 10% whereas Occidental Petroleum (OXY), Pioneer Pure Assets (PXD) and Hess Corp. (HES) all grew to become acquisition targets with decrease yields of the mixed internet buyback yield and the dividend yield.

The market is clearly lacking the chance to personal a premier power firm on a budget. Whereas oil might positively commerce decrease, the percentages are that pure gasoline rallies ultimately and oil is probably going cut up on whether or not the subsequent transfer is greater or decrease.

Warren Buffett and Berkshire Hathaway (BRK.B) continues loading up on Occidental, although Devon Power presents the higher internet payout yield and the cheaper inventory.

Takeaway

The important thing investor takeaway is that buyers ought to proceed loading up on Devon Power, buying and selling close to multi-year lows whereas providing buyers sturdy capital returns from optimistic money flows by way of disciplined capital investments. At these costs, the inventory presents some safety from decrease oil costs, although the upside potential happens with a rally in each oil or pure gasoline costs.