Artur Didyk/iStock through Getty Photographs

Thesis

Devon Vitality (NYSE:DVN) has had it tough recently, down 8% to begin the yr after being down over 30% in 2023. I’ve written several bullish articles on DVN over the course of 2023 and the stark distinction in worth efficiency between it and friends is puzzling. To problem my convictions, I made a decision to do a comparability with Diamondback Vitality (NASDAQ:FANG), one other firm I’ve previously covered, and Devon Vitality to find out if I ought to take into account a shake-up of my portfolio.

On this article I’ll examine, head-to-head, two center weight firms of the Permian Basin. The winner might be based mostly on the next metrics for each Devon Vitality Company and Diamondback Vitality.

- Grime – a measure of the bodily asset we’re investing in. Whoever has the very best acreage ought to (over the lengthy haul) present the very best returns.

- Debt – a measure of total administration efficiency and ahead flexibility.

- Dividends – which firm has the very best shareholder return mannequin.

- {Dollars} – a measure of total valuation

A Fast Look

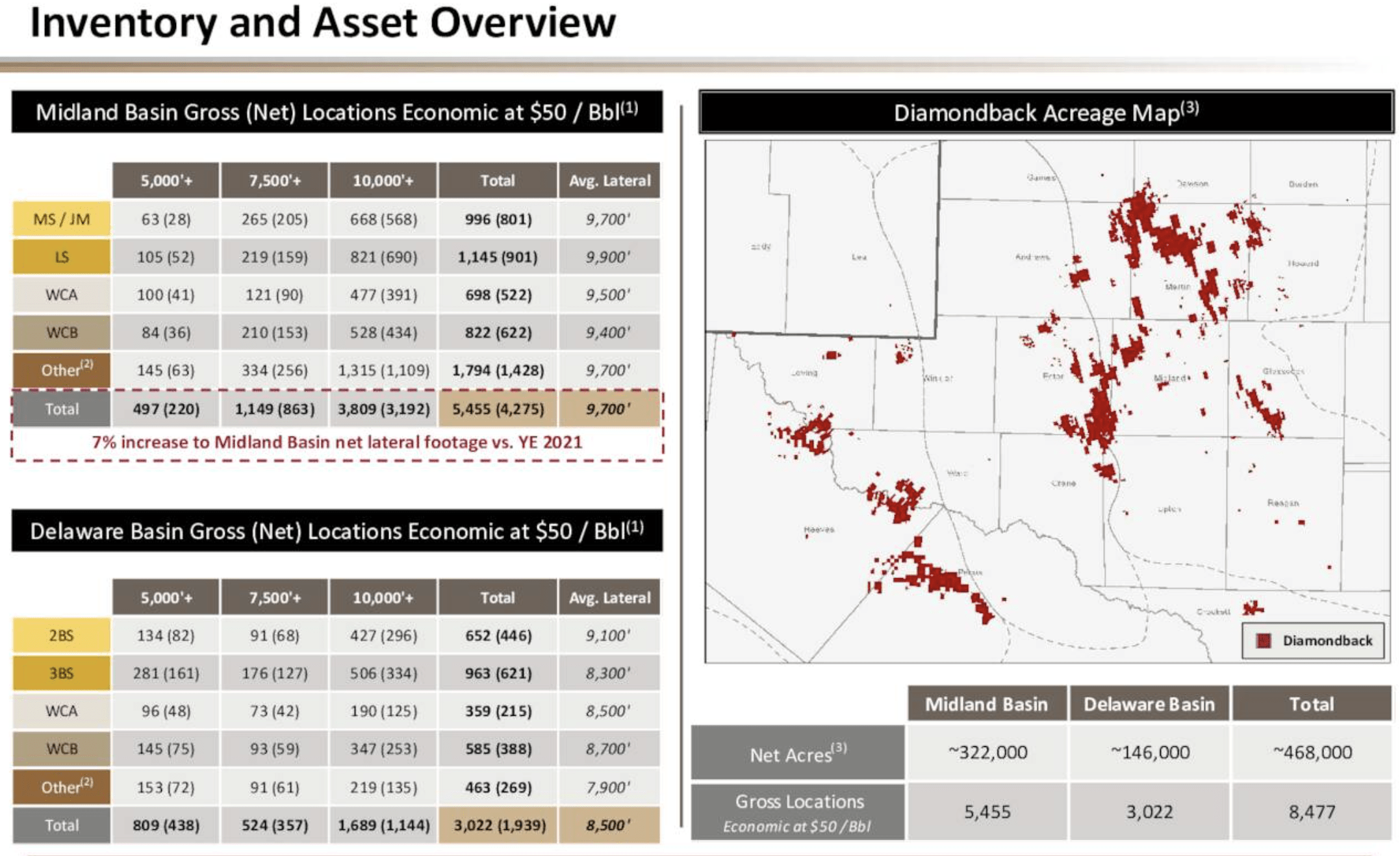

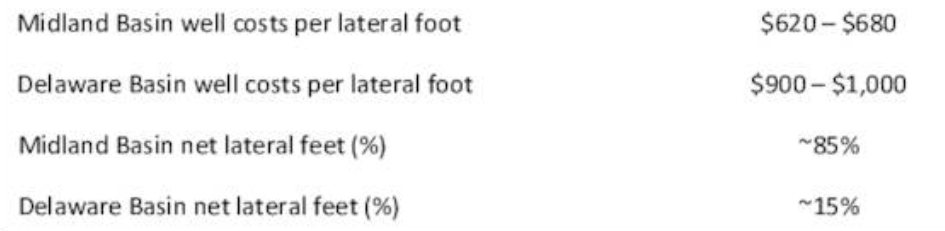

Earlier than we get began, let’s check out every firm. Each DVN and FANG have comparable enterprise fashions as unbiased oil and gasoline producers. Diamondback operates largely within the Midland Basin with 85% of manufacturing coming from this space and 15% coming from the neighboring Delaware Basin.

FANG Acreage Map (Q3 Investor Presentation)

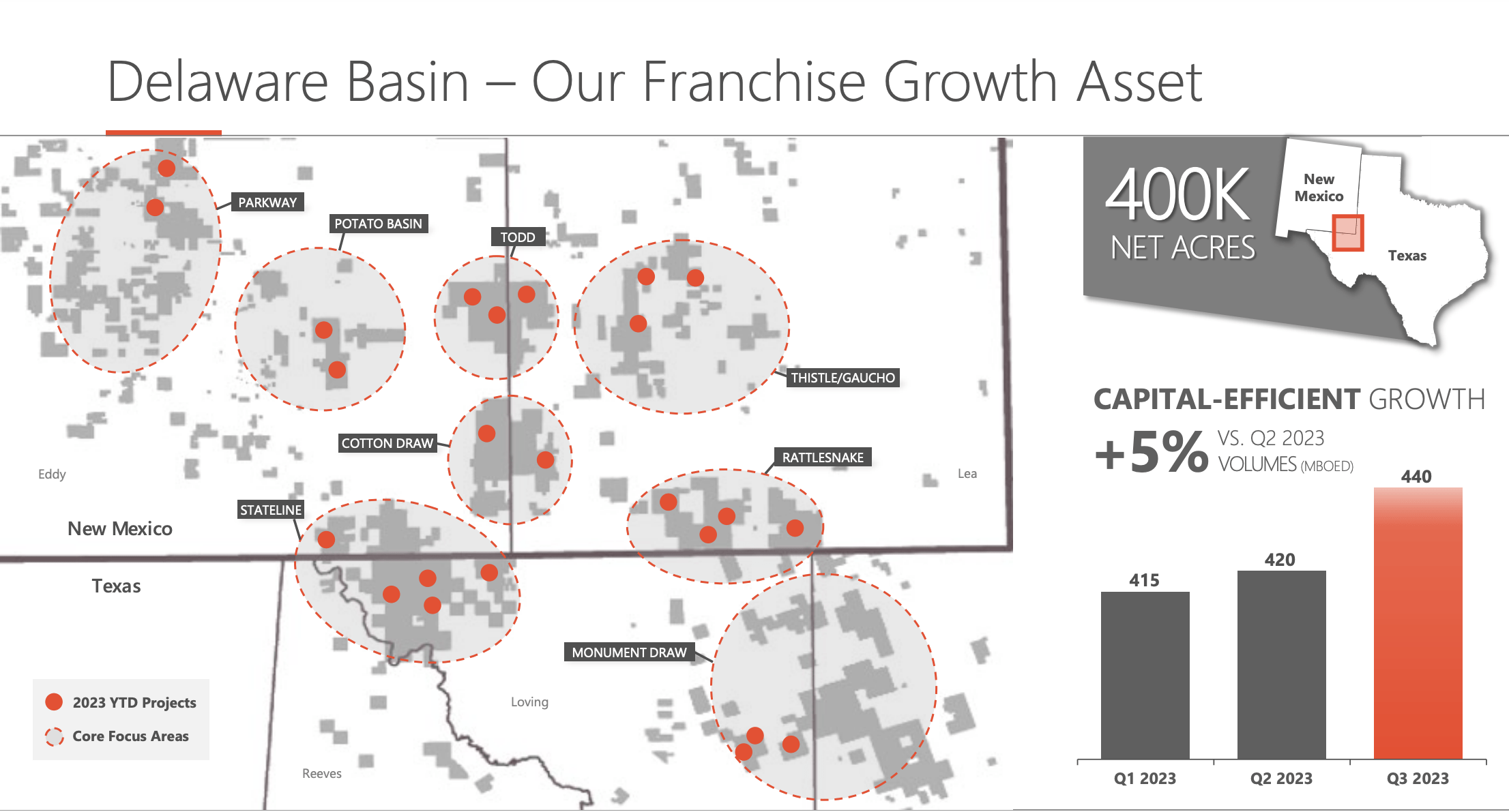

Devon is barely extra various pulling manufacturing from a number of basins. Devon produces roughly 67% of its output from the Delaware Basin The remainder of its manufacturing is sprinkled amongst the Eagle Ford, Anadarko, Powder River, and Williston Basins.

Devon Vitality’s Delaware Acreage (DVN Q3 Earnings Presentation)

Each firms’ money flows are derived from commodity costs. Because of the volatility this will create, each firms have created a variable shareholder return mannequin. Each firms are practically an identical by way of market cap ($26 billion) and Permian manufacturing. DVN produces 440 MBOE/d out of the Permian whereas FANG tips the scale at 453 MBOE/d. After accounting for all of its belongings, DVN is the largest producer at roughly 665 MBOE/d.

DIRT

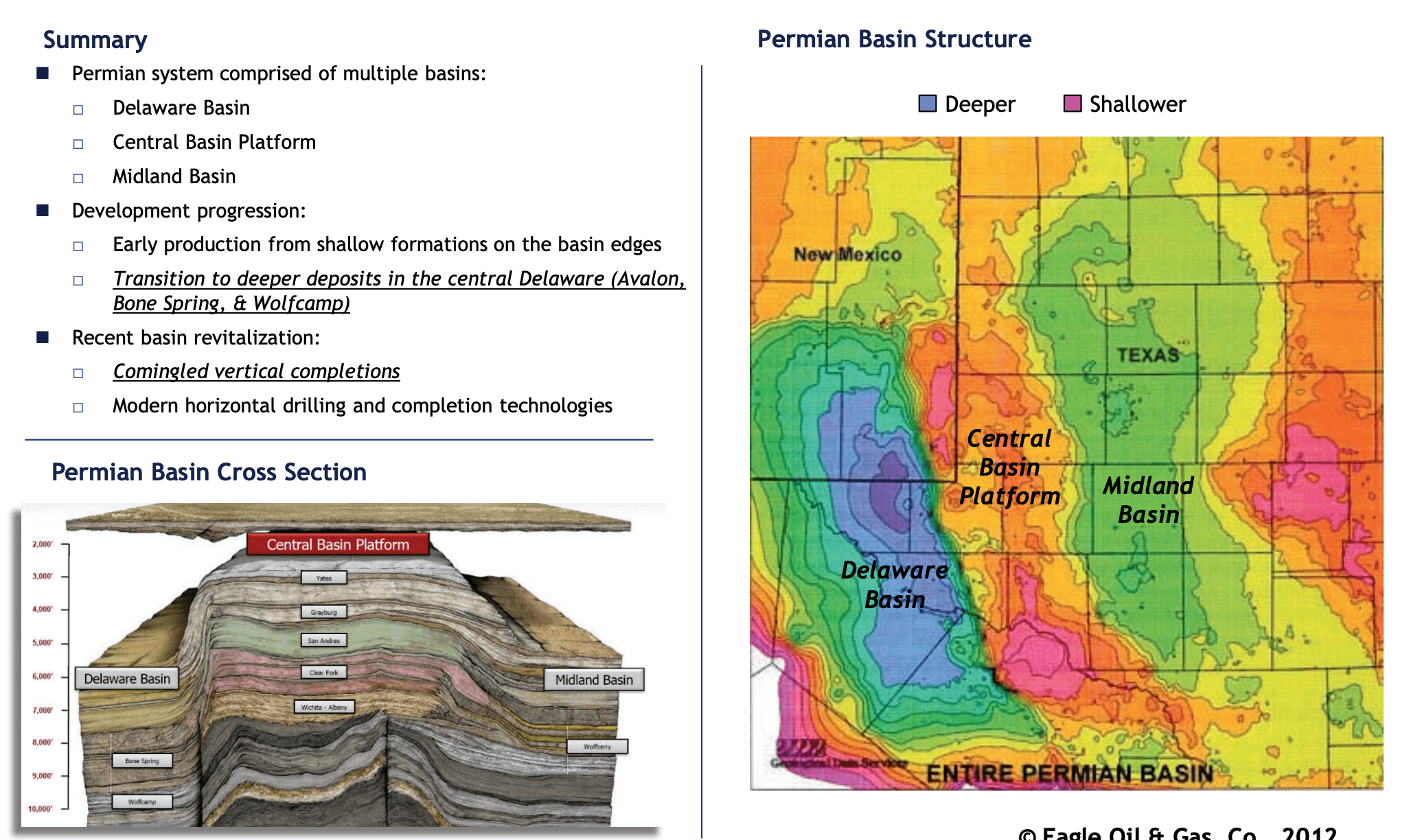

In the end when investing in an oil/gasoline producing entity, we should keep in mind that the standard of property they personal would be the limitation to their success. Poor high quality wells will produce poor monetary returns. The primary focus of this dialogue will examine and distinction the Midland Basin and the Delaware Basin, each of that are positioned in West Texas and Southern New Mexico.

Depth Profile of the Midland and Delaware Basins (Search and Discovery Article #10412)

Midland Basin

The Midland Basin is Diamondback’s bread and butter and has been capable of produce wonderful outcomes. The Midland Basin is positioned simply east of the Delaware Basin. Certainly one of completely different bodily points of the Midland versus the Delaware is that the Midland Basin is within the ballpark of two,000 ft shallower to the oil producing layers of the basin such because the Wolfberry or the Wolfcamp.

This provides Diamondback a definite price benefit, having to drill by 2,000 much less ft of rock to succeed in their product. Diamondback makes use of this benefit to yield one of many lowest manufacturing prices per BOE within the trade. Since FANG additionally produces within the Delaware basin, the corporate is ready to produce price figures for each basins. As you possibly can see within the picture beneath, a properly within the Delaware basin price over $300/lateral foot extra to finish. With an over 10,000 ft lateral properly, this price distinction will be important, to the tune of $3 million per properly.

FANG drilling prices (Q3 Investor Presentation)

Delaware Basin

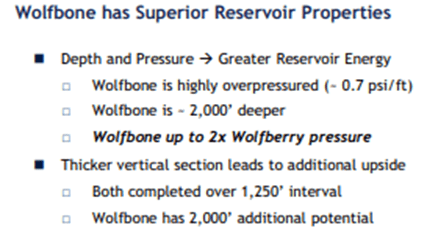

If it is simpler to get to the oil and gasoline merchandise within the Midland Basin, why on earth would somebody hassle drilling within the Delaware Basin? Being 2,000 ft deeper is not essentially ALL dangerous. The extra rock overhead creates extra strain and thus extra oil will be extracted per properly. This does create the potential for increased ROIs if the wells are drilled and executed appropriately. The juice must be definitely worth the squeeze.

Delaware Vs. Midland Basin Properties (Search and Discovery Article #10412)

Devon has famous some operational impacts because of infrastructure constrains within the underdeveloped parts of the Delaware basin.

Our plan will shift the next mixture of exercise to multizone Wolfcamp developments in New Mexico, which is the core of the play as infrastructure constraints have eased over the previous and can proceed over the approaching months. With this refined capital allocation, we anticipate to enhance properly productiveness by 5% to 10% in 2024

The 2023 infrastructure constraints resulted in a shifting a portion of our capital to much less prolific areas within the basin and at instances, constrained peak charges throughout a subset of our new wells.

Transitioning to increased high quality wells ought to enable DVN to revenue from decrease working price per BOE in 2024.

The Verdict

There are apparent execs and cons between the 2 basins, nonetheless all this comes all the way down to which firm can flip the very best return on funding. The desk beneath represents the typical realized worth per BOE for each firms in addition to their working prices bases on Q3 efficiency. All information is obtained from every firm’s Q3 10-Q reviews.

Diamondback scores the purpose for the very best acreage due to the next realized worth and decrease total working price construction to ship a sizeable enhance in working margin. The rating is 1-0 FANG.

Buyers ought to word that I anticipate the hole in working bills to slim going ahead. As beforehand talked about, DVN’s prices ought to decline by shifting to increased high quality wells. Moreover, FANG will incur increased working prices following the divesture of its stake in its water infrastructure, Deep Blue JV. This may end in working bills rising approximately $0.50/BOE going ahead.

| % Oil Manufacturing | Realized Worth per BOE | Working Expense | Working Margin | |

| Devon Vitality (DVN) | 48.3% | $46.92/BOE | $12.19/BOE | $34.73/BOE |

| Diamondback Vitality (FANG) | 58.8% | $54.37/BOE | $10.51/BOE | $43.86/BOE |

Debt

To measure the work of the administration group, we should consider the monetary situation the corporate is working underneath. We’ll examine the debt profiles of each firms for out subsequent metric.

Two distinct variations will be seen right here.

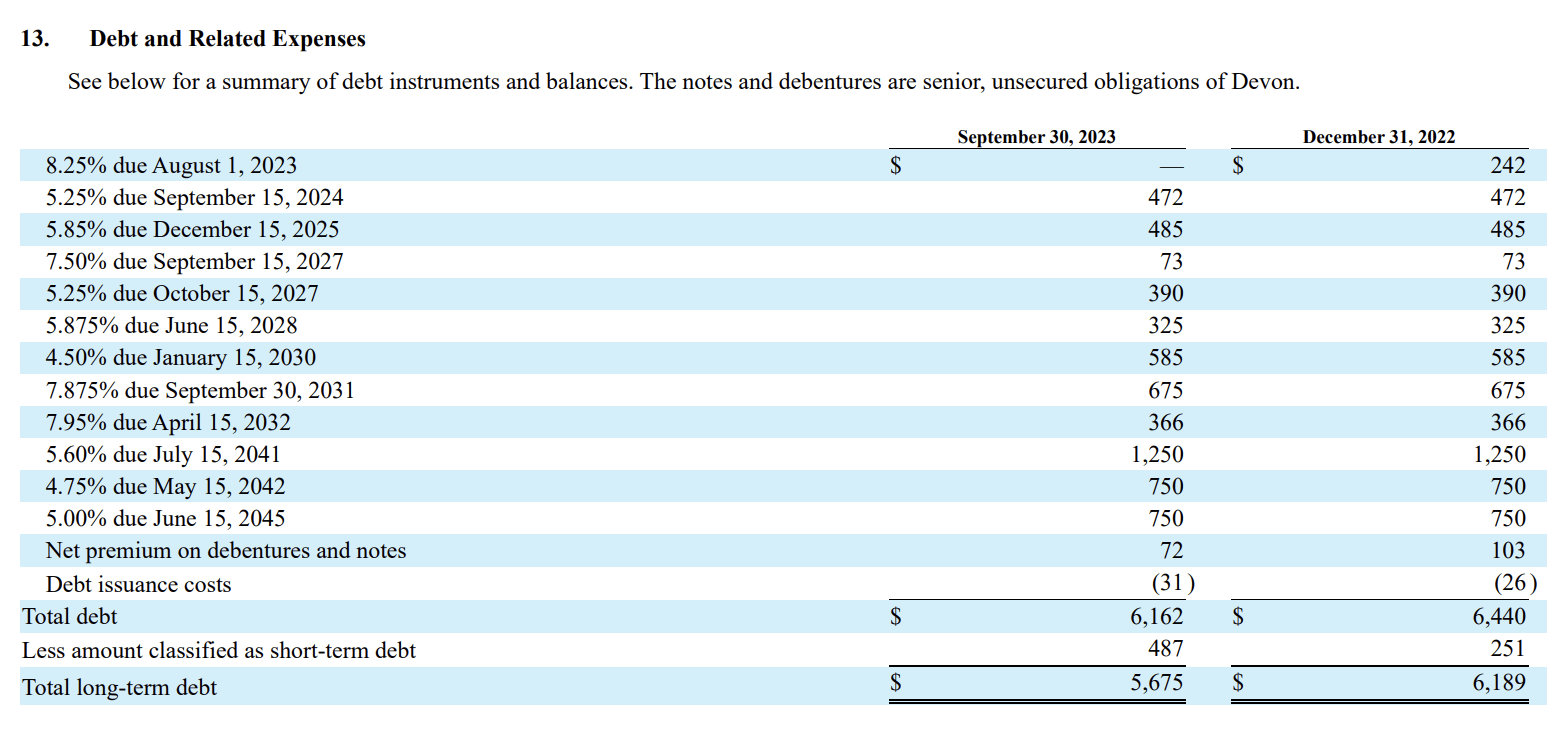

1. The typical price of debt for FANG is 4.57% vs 5.72% for DVN.

2. DVN has $957 million in debt due between each 2024 and 2025. In the meantime, FANG has no maturities due till 2026.

The full debt due over the following 5 years is actually the identical between the 2 firms however DVN’s has a steadier cadence. FANG traders will profit from increased returns in 2024 and 2025 that aren’t impeded by debt maturities.

Nonetheless, this may enable DVN to have a extra structurally sound steadiness sheet coming into 2026 as the corporate plans to repay the debt because it comes due as an alternative of pursuing refinancing choices. Devon’s CFO, Jeff Ritenour, laid out the businesses plan within the Q3 conference call.

In August, we paid off $242 million of maturing debt, and we bolstered liquidity with money balances rising by 56% to $761 million.

With these actions, Devon exited the quarter with a web debt-to-EBITDA ratio of simply over 0.5 flip. Shifting ahead, we plan so as to add to our monetary power in every quarter by committing round 30% of our free money circulation again to the steadiness sheet. This may enable us to additional pare down our absolute debt steadiness with reimbursement of roughly $1 billion of maturities coming due in 2024 and 2025 and keep a minimal money steadiness in extra of $500 million.

With a decrease price of debt and two years of zero debt obligations the purpose for debt goes to Diamondback. The rating is now 2-0.

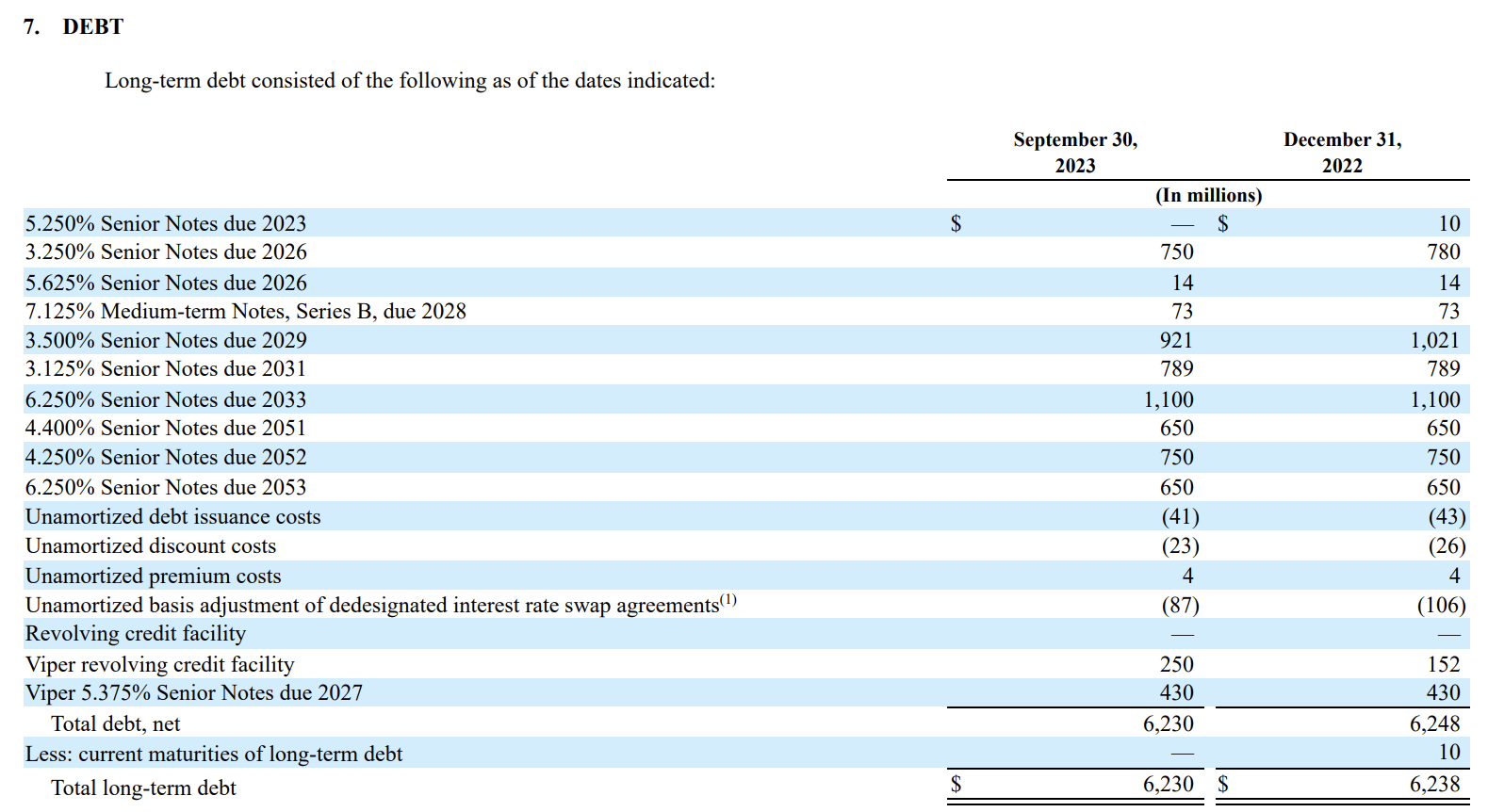

DVN Lengthy Time period Debt (10-Q)

FANG Lengthy Time period Debt (10-Q)

Dividends

Each firms’ return profile is break up into two components. A base dividend and a variable part. The variable part will be both within the type of a variable dividend or share repurchases, or some mixture of each. The variable part is meant to match the variability of power costs.

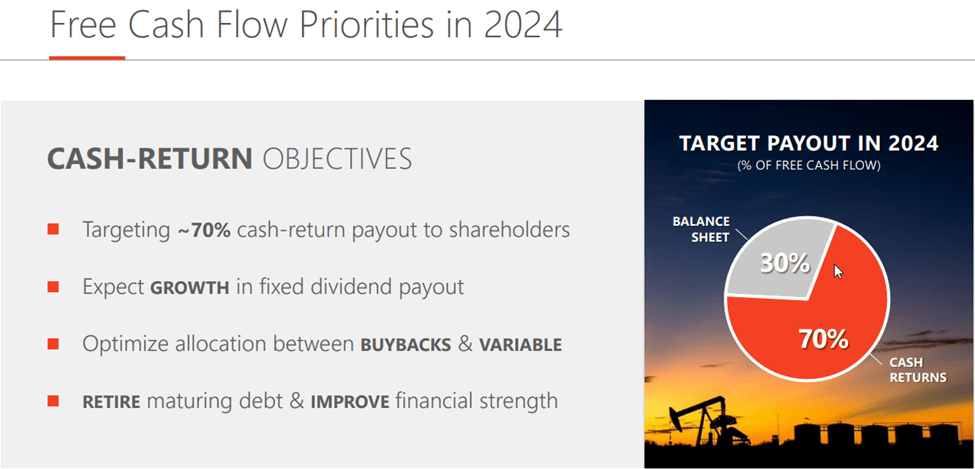

DVN targets to allocate 70% of FCF to shareholder returns whereas devoting the remaining 30% to the steadiness sheet. This 30% will primarily be used to handle the 2024 and 2025 maturities talked about earlier. FANG follows an analogous mannequin however allocates a minimal of 75% of FCF to shareholders underneath its program.

DVN Shareholder Returns (DVN Q3 Earnings Presentation)

Regardless of the decrease goal, DVN has returned 102% of FCF over the primary three quarters of 2023 because of heavy share repurchases in Q1. FANG additionally exceeded its goal by paying out roughly 81% over the identical timeframe. Nonetheless, with superior working margins and the next minimal payout, FANG shareholders ought to obtain the next total compensation in the long term. The rating is now 3-0 in favor of Diamondback Vitality.

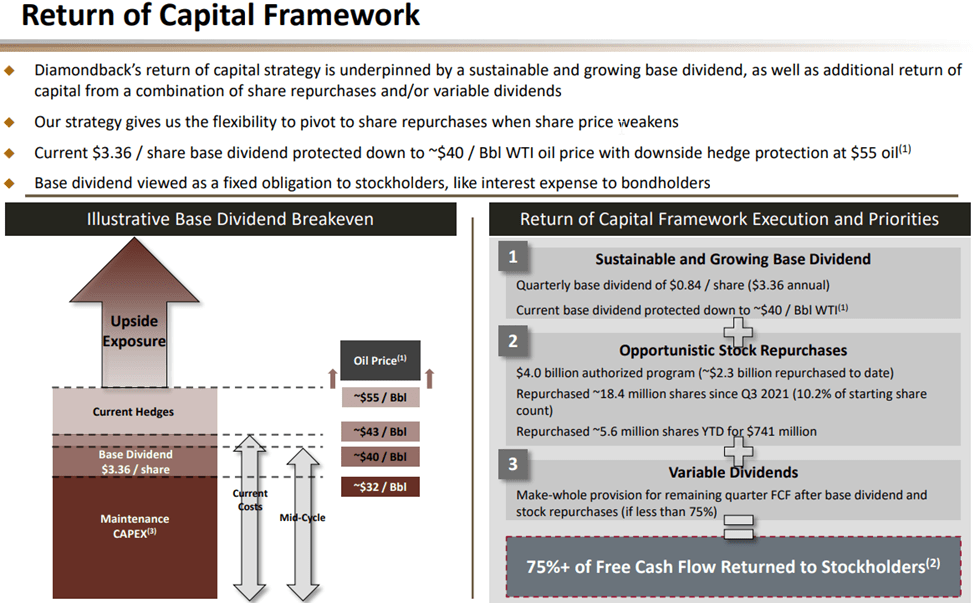

FANG Shareholder Returns (Investor Presentation)

{Dollars}

To date, FANG is knocking it out of the park. The last word objective for shareholders is to optimize FCF per share as this may decide the payout to shareholders. We additionally need to pay as little as potential for that FCF with a low Worth/FCF a number of.

I annualized Q3 manufacturing information to offer a tough estimate of money technology over a full yr. This may clearly change with power and share costs however the relative distinction between the 2 firms is what’s necessary. As proven beneath, each DVN and FANG commerce at primarily the identical Worth to FCF ratio.

This is able to point out that each firms are valued practically the identical. Nonetheless, the route of working bills for each firms are heading in reverse instructions. FANG is projecting for barely increased OPEX following the Deep Blue divesture, whereas DVN is projecting for decrease OPEX by concentrating on increased high quality wells. In consequence, I’ve given the ultimate level to DVN by a slight margin.

Abstract

The “official” rating has Diamondback Vitality (FANG) for the win with a ultimate rating of 3-1. Listed below are the highlights of every dialogue.

- The Delaware and Midland basins have contrasting qualities between price and oil manufacturing. Diamondback is ready to get hold of the next working margin as a consequence of the next share of oil manufacturing and decrease working prices. FANG was awarded the purpose for that motive.

- Each firms have practically an identical quantities of debt. Diamondback has a decrease price of debt with no maturities due over the following 2 years. This creates a really clear path for optimized shareholder returns over the medium time period. FANG was awarded the purpose on this class.

- Diamondback has a 75% return mannequin versus 70% for DVN. The mixture of a better share of returns, increased margins and decrease debt prices will produce superior shareholder returns. FANG was awarded the purpose on this class.

- Each firms commerce at equal worth to FCF multiples. The purpose was awarded to DVN for reducing working bills going ahead whereas FANG’s are projected to barely enhance.

General, the variations in every class are small, making each firms viable investments. Given these outcomes, FANG ought to show to be the extra profitable funding based mostly on the present efficiency. Nonetheless, DVN is taking actions that will very properly shut the hole between the 2 firms by the top of 2024. In my view, these actions warrant holding DVN for a two quarter analysis interval previous to deciding to reallocate my DVN place.

For traders seeking to provoke a place, FANG is a transparent winner on this head-to-head. I charge each firms as a purchase at present costs.