Monty Rakusen/DigitalVision through Getty Pictures

In mid-2022, I revealed a bullish outlook on the oil and fuel producer Diamondback Power (NASDAQ:FANG) in “Diamondback Energy: Oil Producers To Profit From Substantial Decline In Crude Reserve.” At the moment, I believed that crude oil costs would inevitably rebound because of the important decline in whole US storage ranges and tepid manufacturing development. Mixed with rising exports to Europe, offsetting Russia, it appears probably that oil costs wouldn’t stay as little as they had been then.

Since that article was revealed, FANG has risen by round 73%, delivering a strong whole return of about 80%. As anticipated, the US authorities has been unable to refill the SPR reserve, and international provides have continued to pressure. That stated, the availability and demand imbalance is decrease than anticipated, as US manufacturing ranges have risen markedly in latest months. Nevertheless, as was the case in 2022, most of that manufacturing development comes from pre-drilled wells, indicating it’s unsustainable and not using a rise in capital expenditure spending. For probably the most half, major producers are nonetheless unwilling to extend their CapEx ranges and proceed to shift away from development towards dividends.

Whereas your gasoline spending won’t profit from this variation, Diamondback and its friends are. The corporate has seen dramatic revenue and valuation development, notably in latest months, as oil rose to ~$90 per barrel. In latest weeks, oil reversed most of these good points, following the inventory market in what seems to be a correction. The oil market has benefited from report demand over the previous yr, so if a slowdown causes that to vary, we might even see oil producers like FANG observe go well with. That stated, with Diamondback’s administration and its monetary and operational place, I should still think about shopping for the inventory if it declines.

FANG’s Operational and Monetary Outlook

Diamondback’s major revenue driver is the value of crude oil. Oil accounts for round 80% to 90% of its total sales, with the rest break up between pure fuel and NGLs. That determine declined since 2022 because it shifted away from pure fuel because of the huge value decline in that commodity. From its annual report (pg. 9), we will see its whole money prices per BOE is $10.9 whereas its non-cash prices (together with curiosity) are $12.15 (most of which is depreciation). Thus, its whole manufacturing value is round $23 per BOE, which is extremely low.

The corporate is targeted on the Permian Basin, which is notoriously low cost for hydraulic fracturing. It produces round 163M BOE per yr, with ~2.18M BOE in whole proved reserves, of which ~1.5M BOE are developed. That’s essential to contemplate, as whereas the Permian permits for affordable manufacturing, it’s not essentially an infinite useful resource. Technological progress has prompted reserve estimates to rise sooner than depletion for years, however that ought to not proceed eternally. Certainly, good proof means that effectively effectivity is falling sooner than anticipated, implying the first provide supply will not stay so profitable years into the longer term.

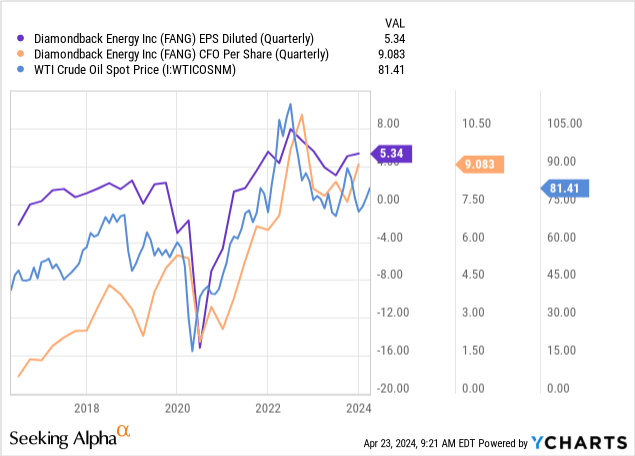

Assuming the agency continues to see reserves develop barely, it might have 10-15 years of worthwhile working situations, which we should account for in its valuation. For my part, this isn’t a big situation as a result of, by 2040, I imagine it’s probably that EVs will change most standard autos, making 80%+ of petroleum ineffective. Realistically, as expertise stands, electrical automobiles are fueled by pure fuel (the first US electrical energy supply), so the corporate nonetheless has revenue potential past that time. The approaching 5-10 years needs to be probably the most essential for Diamondback. Certainly, the corporate is seeing large earnings and money flows in the present day, notably with greater oil costs:

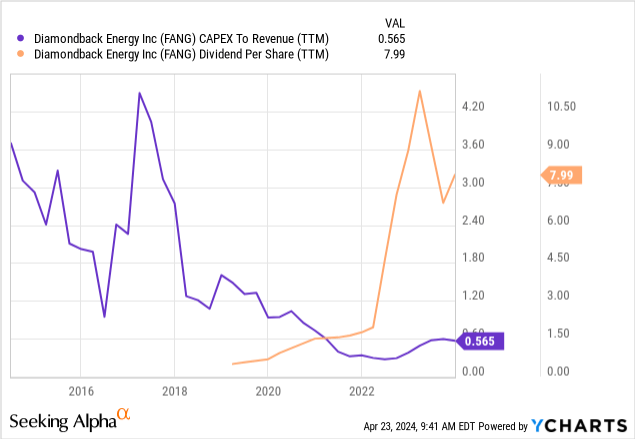

Like nearly all oil exploration and growth corporations, Diamondback is transferring away from exploration and growth. The 2010s had been a shock growth for that market because the Permian was explored and developed, inflicting a large enhance in US output that prompted international oil costs to break down. Accordingly, the 2020s are a decade of oil market maturation. E&Ps are avoiding CapEx spending and as a substitute shifting towards paying greater dividends and decreasing debt. In contrast to a few of its friends, FANG has not centered an excessive amount of on debt discount, although its debt-to-EBITDA is simply round 1X, so it is simply manageable. Nevertheless, it is shifting its money flows away from capital growth spending to dividends. See beneath:

Relying on how the determine is calculated, Diamondback’s web revenue per share has not risen dramatically since I final lined it. Nevertheless, its dividend has elevated considerably. Its yield is simply 1.8% in the present day however sharply rises because it transitions towards paying the next yield, encouraging a brand new wave of dividend development funding.

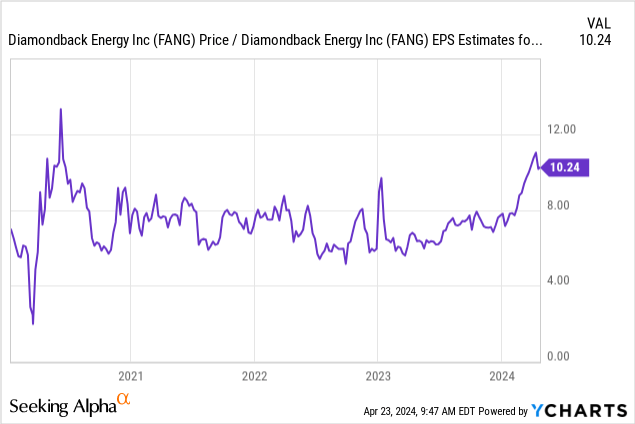

Nonetheless, this leaves FANG’s ahead valuation a lot greater in the present day than earlier than. Utilizing two-year-out anticipated EPS, which accounts for latest adjustments in oil costs, its ahead “P/E” a number of is 10.2X. See beneath:

Whereas that determine could not appear excessive, it’s elevated in comparison with different E&Ps with large financial value sensitivity to grease. Nevertheless, Diamondback’s revenue sensitivity is decrease than most of its smaller friends since its manufacturing prices are so low. That stated, its present valuation can also not account for the inevitable depletion of its reserves and may solely be affordable if we assume oil will proceed to rise.

The Oil Scarcity Ought to Develop By 2026

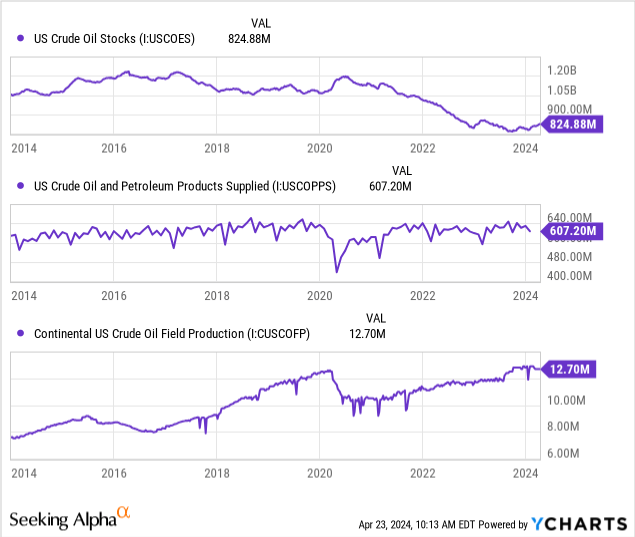

US oil storage ranges are low in the present day following the mass launch of the federal government’s Strategic Petroleum Reserve. Traditionally, low oil storage ranges are related to greater costs. US whole oil demand (merchandise provided) stays close to its peak stage and is unlikely to say no and not using a important international recession. Complete US oil manufacturing did bump greater over the autumn of 2023 however has stagnated. See beneath:

Total, these figures level to stability within the US oil market. Provide and demand usually are not transferring considerably, whereas whole storage isn’t trending upward or downward. Nevertheless, whole storage is low, so if a provide and demand imbalance happens, the potential upside in oil is probably going very asymmetrical. It’s uncertain we are going to see a large decline in oil costs or damaging costs as each OPEC+ and the US authorities SPR are prone to take price-supportive measures if oil crosses beneath $70 and stays within the $60s, both by reducing output (OPEC) or increasing demand (strategic reserve).

Notably, a senior White House official just lately talked about releasing much more oil from the reserve (at its 40-year low stage) if oil costs rise once more. Though that may be an unwise transfer from the “strategic reserve” standpoint, I really feel there’s a political aim to keep gasoline costs low earlier than the election.

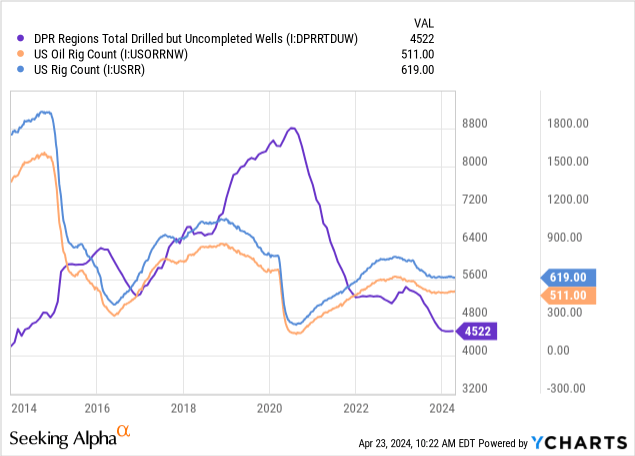

Additional, it’s unlikely that the present US oil output stage can be sustained with out elevated capital funding. Like its friends, Diamondback is avoiding making important CapEx investments, probably as a result of the long-term payoff of such investments is lowered as international oil demand permanently peaks. Current output development has come from the utilization of oil wells that had been drilled earlier than 2020. The US and international rig counts stay very low, signaling minimal general oil output capability enlargement. See beneath:

There are fewer drilled-but-uncompleted wells in the present day than up to now, which means the rig rely might want to rise for oil output to extend and even be sustained, provided that fracked wells see huge output declines throughout their first yr or two. Which means oil output shouldn’t rise with out a rise in CapEx spending, which we’re not seeing regardless of excessive earnings for many E&P’s.

This factors to a long-term oil scarcity, as oil producers like Diamondback have no real interest in increasing and are as a substitute centered on profitability and accretive mergers, such as its $26B acquisition plan of the non-public Endeavor. If the deal passes the extremely scrutinizing FTC, then Diamondback could be a behemoth of the Permian Basin. That stated, I don’t anticipate it to dramatically change its earnings past the accretive advantage of the funding.

The company recently launched a $5.5B bond sale to partially fund the $26B takeover of Endeavor. The providing has a 40-year safety yielding 142bps above the Treasury charge, so round 5-6%. Whereas this may double the agency’s excellent debt, the added cash-flow is expected to maintain its leverage ratio round 1.1X by year-end. The deal is predicted to extend its output by round 76% (~460K BOEd to ~812K BOEd). Assuming its CFO rises equally, the online change in each the corporate’s post-merger valuation and leverage is small.

I believe the merger deal is a profit as a result of it limits the danger that Endeavor will enhance manufacturing to compete with it. Such competitors could enhance the prices of transportation within the area, particularly. Therefore, it’s seen as unhealthy information for Permian midstream firms. Nevertheless, for that cause, and given the FTC’s sturdy antitrust positioning today, I believe there’s a materials danger that the deal will fail.

The Backside Line

I imagine FANG could also be an honest funding in the present day, however I am downgrading my outlook to impartial on concern that it’s overvalued. Sure, its earnings are important in the present day and will proceed to rise because it focuses on mergers and capital effectivity. Nevertheless, the inventory’s value has elevated dramatically since 2022, whereas oil costs haven’t. Basically, I anticipate FANG to rise in worth solely as a result of I imagine crude oil will stay over $150 within the coming years, dramatically growing its revenue potential. That stated, I really feel the inventory has moved too quick in comparison with oil in latest months, placing it liable to a correction. If its ahead “P/E” falls beneath 8-9X, I would probably flip bullish. In different phrases, I would solely purchase FANG at round $170 or beneath, given in the present day’s market dynamic.

Direct oil futures ETFs like (USO) is a greater guess. Oil has corrected to round $82 from over $90, making for a sexy correction shopping for alternative. Oil will rise in worth because of power underinvestment from major producers, with nearly no long-term output development investments since 2020. A possible recession would undoubtedly upset USO or FANG, however I imagine USO’s draw back is especially restricted as a result of the federal government will probably refill the SPR if it declines beneath $70. I do not get USO to rise too shortly by November, because the Biden administration has talked about releasing much more SPR reserves ought to fuel costs rise too quick. Nevertheless, there stays materials potential that key oil provide strains from the Center East will break as that area’s conflicts proceed. In that state of affairs, I might not be shocked to see oil rise effectively over $150, doubtlessly creating an emergency because of the lack of SPR storage in the present day.