Slaven Vlasic/Getty Photographs Leisure

There’s a sign that the worst for Disney (NYSE:DIS) is probably going behind it as its CEO Bob Iger is lastly turning the enterprise round. The newest comparatively profitable earnings outcomes together with different latest developments level to the truth that Disney is on observe to restoration and its streaming enterprise might lastly attain profitability subsequent yr. Whereas some dangers stay, the momentum that the corporate has going for it might doubtless assist Disney’s shares to a minimum of commerce on the present ranges within the foreseeable future.

Streaming Profitability In Sight?

Again in September, I said that Disney could possibly be a worth entice because the disappointing efficiency of the streaming enterprise has negatively affected the corporate’s efficiency in latest quarters and pushed the shares to their 8-year lows. I’m glad to say that I’ve been fallacious to this point, as the newest earnings report for This fall that was launched final month pointed to the truth that the advance of the corporate’s general enterprise could possibly be on the horizon. In This fall, Disney managed to extend its revenues by 5.7% Y/Y to $21.24 billion, whereas its non-GAAP EPS of $0.82 was above the estimates by $0.11. What’s extra, is that the expansion of the experiences enterprise has accelerated as its revenues through the interval elevated by 13% Y/Y to $8.16 billion.

On the similar time, the leisure enterprise has lastly managed to develop in addition to its revenues in This fall have been up 2% Y/Y to $9.52 billion. Partly it was attainable due to the profitable debuts of Disney’s new theatrical titles and partially due to the expansion of the streaming enterprise. In This fall alone, Disney has managed to extend its subscriber rely by practically 7 million to 150.2 million subscribers, above the estimates of over 147 million subscribers. This might point out that after losing practically $11 billion because the launch of Disney+ in 2019, the corporate’s flagship streaming service is lastly catching up momentum and will turn into worthwhile by the tip of 2024. This could possibly be achieved by the discharge of recent content material within the following quarters, the higher advertising of the ad-supported plan of Disney+, and the implementation of stricter requirements round account sharing in 2025. The latter has helped Disney’s competitor Netflix (NFLX) expertise a rise in subscribers and revenues within the latest quarter.

All of these development catalysts ought to assist Disney maintain the momentum going sooner or later and assist the shares to rebound farther from the 8-year lows. On high of that, a shift in strategy in 2024, together with the upcoming deal to promote the bulk stake in its Indian operations might additionally be sure that the worst for Disney is lastly behind it after years of struggles.

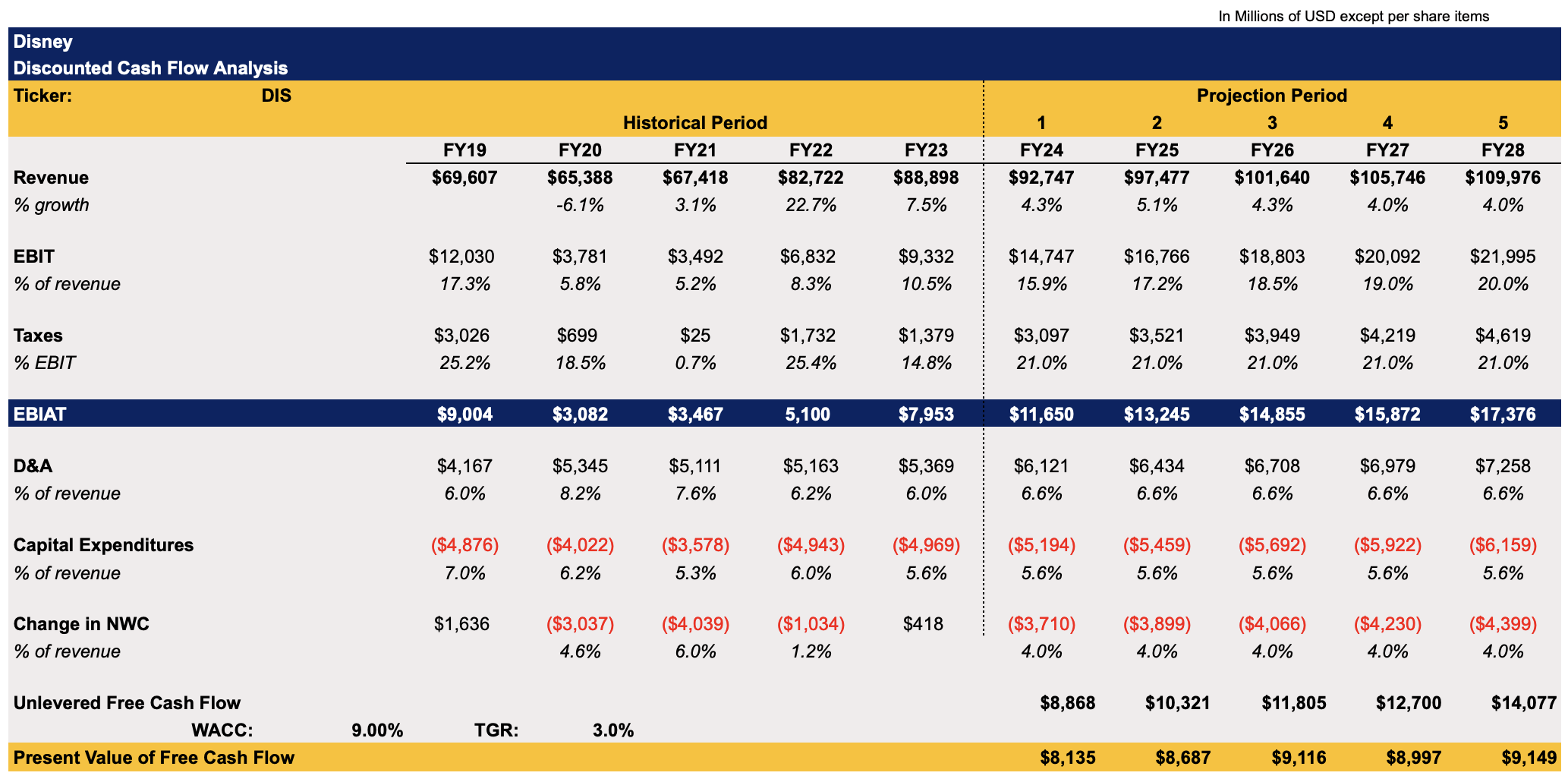

To determine how massive is Disney’s upside, I’ve created a DCF mannequin that may be seen beneath. A lot of the assumptions within the mannequin for the next years are both near the historic efficiency or in-line with the street estimates. The weighted common value of capital within the mannequin is 9%, whereas the terminal development price is 3%.

Disney’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Writer)

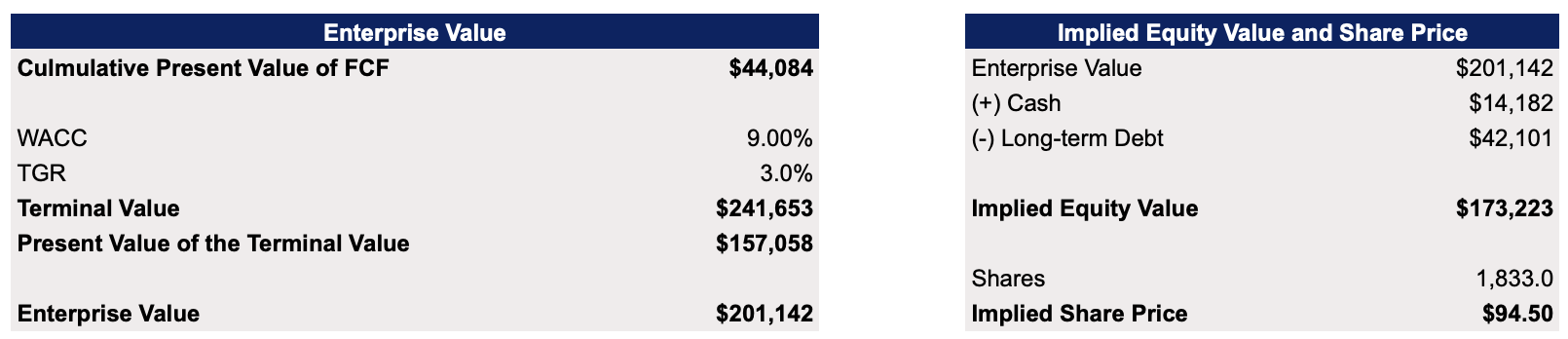

This mannequin reveals that Disney’s enterprise worth is $201 billion, whereas its honest worth is $94.50 per share, which represents an upside of ~5% from the present market worth.

Disney’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Writer)

Main Dangers To Take into account

Regardless of all the optimistic developments in latest months, there’s nonetheless no assure that Disney will have the ability to maintain the momentum going within the following quarters. It’s vital to grasp that so as to maintain any streaming service related there must be a relentless provide of recent and fascinating content material. Whereas to this point, Disney has been profitable in producing such content material in latest quarters – there’s at all times a danger {that a} weak launch of a brand new film or a sequence would end in a weaker development of subscribers and kill the momentum that the corporate has at the moment going for it.

What’s extra is that the long run development of Disney’s streaming enterprise is in massive depending on the efficiency of the general financial system that has a direct affect on the streaming business. Earlier this yr it was reported {that a} quarter of adults in the US have unsubscribed from streaming providers on account of a excessive inflation that has negatively affected the broader shopper confidence. Whereas we’re at the moment in a disinflationary setting and on observe to attain a smooth touchdown, there’s at all times a danger that inflation might as soon as once more get uncontrolled and have a direct affect on the streaming business sooner or later.

One other factor that must be talked about is that even when we obtain a smooth touchdown, the Federal Reserve might determine to maintain the charges greater for longer and reduce them later than we at the moment anticipate. If that’s going to be the case, then Disney’s curiosity funds might proceed to rise within the foreseeable future. Only a yr in the past, Disney paid $434 million in curiosity bills in This fall’22, whereas in This fall’23 the curiosity bills reached $501 million. Subsequently, it is smart to imagine that even when Disney is on the trail to restoration, such a restoration is unlikely to be fast and easy.

The Backside Line

There’s no denying that Disney is in a a lot better place now than even half a yr in the past. Regardless of all of the dangers which can be related to its enterprise, the corporate has momentum going for it and if Disney+ continues to extend its person rely and reaches profitability subsequent yr, then the shares might rally within the following quarters as they’re not overvalued on the present worth. Nonetheless, Disney had a historical past of overpromising and underdelivering prior to now, so the advance of the streaming enterprise within the following quarters just isn’t assured at this stage. That’s why I follow my HOLD score for now.