Yauhen Akulich

Introduction

The opposite day, I used to be trying into ICE Midland WTI futures as a part of my analysis into Intercontinental Change (ICE), the proprietor of those futures and one among my favourite monetary dividend progress shares – that’s not but part of my portfolio.

So, I believed, why not begin this text with a micro lecture on this futures contract?

I consider that the majority will likely be conversant in the NYMEX WTI future, which is owned by the CME Group (CME). Subsequent to ICE Brent, it is the largest oil future on this planet.

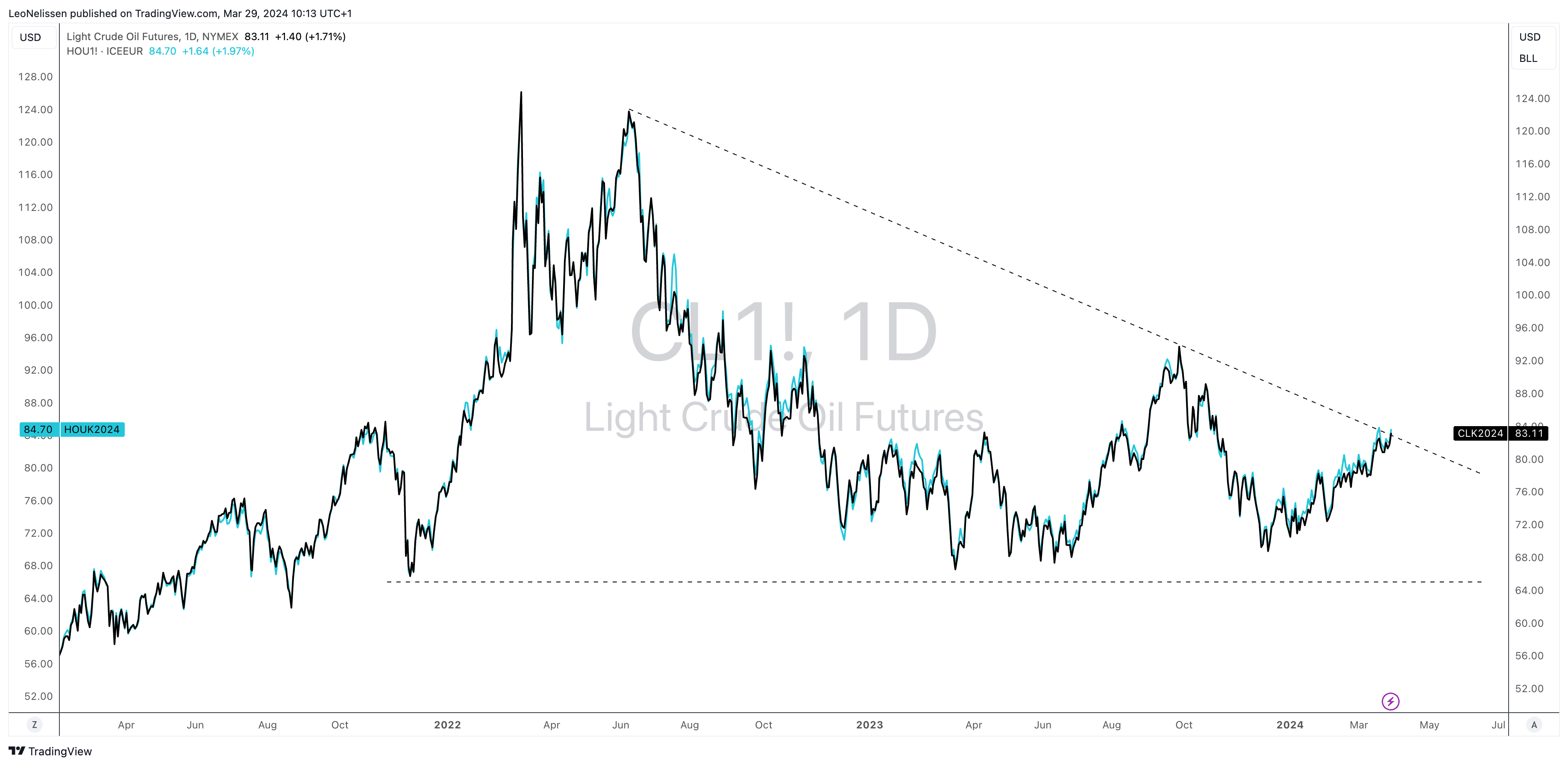

As we are able to see beneath, ICE Midland WTI and NYMEX WTI have an ideal correlation. The correlation is so excessive that it is exhausting to see the blue line behind the black line.

TradingView (NYMEX WTI, ICE Midland WTI)

Nonetheless, a fast have a look at the x-axis exhibits that there is one distinction: pricing.

Normally, ICE Midland is roughly $1.50 per barrel costlier than NYMEX WTI.

What makes ICE Midland so particular is its concentrate on America’s highest-quality oil from the Midland Basin (part of the mighty Permian Basin). The oil is deliverable into the Brent advanced and can be utilized in American, European, and Asian refineries.

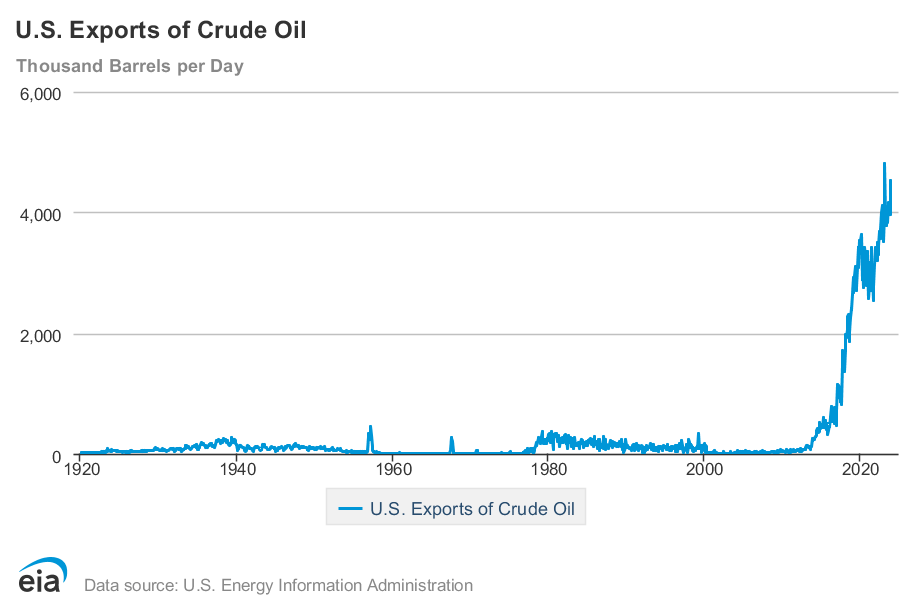

Because the U.S. has turn into an power powerhouse, exporting greater than 4.5 million barrels of oil per day, new strategies to purchase oil and hedge dangers are wanted.

Vitality Data Administration

The rationale I am bringing this up is as a result of ICE Midland oil is not delivered through Cushing, Oklahoma, like NYMEX WTI.

ICE Midland WTI is deliverable to each the Enterprise Crude Houston and ONEOK Magellan East Houston (“MEH”) terminals.

S&P World

This brings me to ONEOK Inc. (NYSE:OKE), which owns the MEH terminal after merging with Magellan, making it an much more necessary participant within the U.S./world power trade.

With regards to long-term investments, I need to personal the very best corporations which can be so necessary that, with out them, we’d run into hassle.

Whereas an environment friendly power infrastructure might really feel like one thing we take as a right within the West, latest developments present that power infrastructure is important to our on a regular basis lives.

It additionally explains why, in a warfare, power infrastructure is a core goal.

Google Information

With that mentioned, my most up-to-date article on ONEOK was written on December 29, titled “5.4% Yield And Up to 10% Annual Return Potential – Buying Top-Tier Income With ONEOK.”

Since then, OKE shares have returned 16%, beating the S&P 500 by roughly 6 factors!

On this article, I am going to revisit the inventory to clarify why it is such a robust midstream firm and what to make of the chance/reward after such a powerful rally.

On a facet notice, OKE is a C-Corp. It isn’t taxed as a Restricted Partnership like lots of its midstream friends.

So, let’s get to it!

Shopping for Diversified Vitality Infrastructure

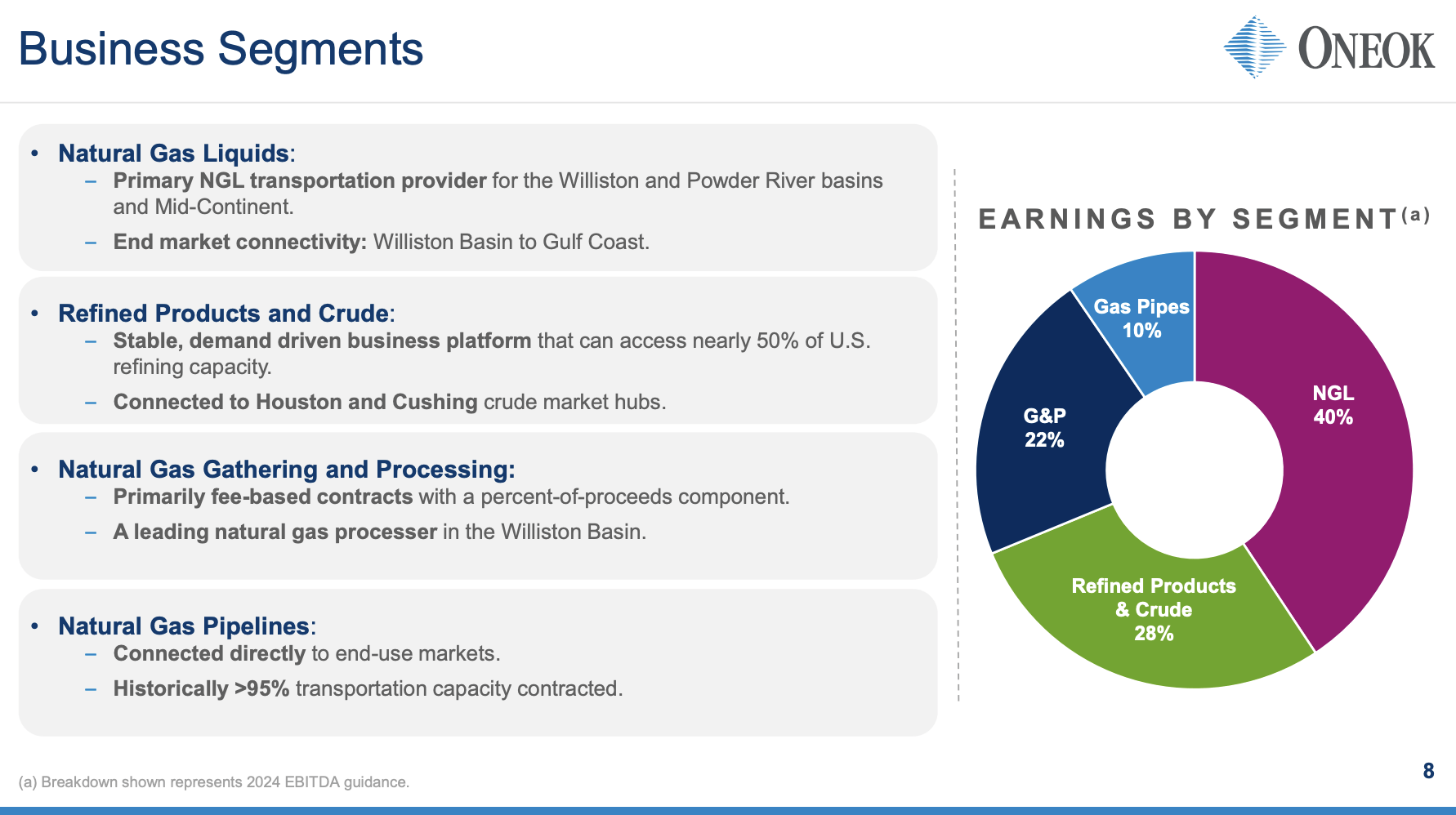

Initially, OKE was a pure fuel and pure fuel liquids (“NGL”) participant. Nonetheless, after a variety of main offers, together with the merger with Magellan, it’s now a extremely diversified midstream firm.

- As we are able to see beneath, near 70% of its earnings come from NGL and refined/crude oil operations.

- 22% of its earnings come from gathering and processing operations, that are primarily fee-based operations. Within the Williston Basin, the corporate is a number one pure fuel processor.

- 10% of its earnings come from pure fuel pipelines that straight join provide to end-use markets.

ONEOK Inc.

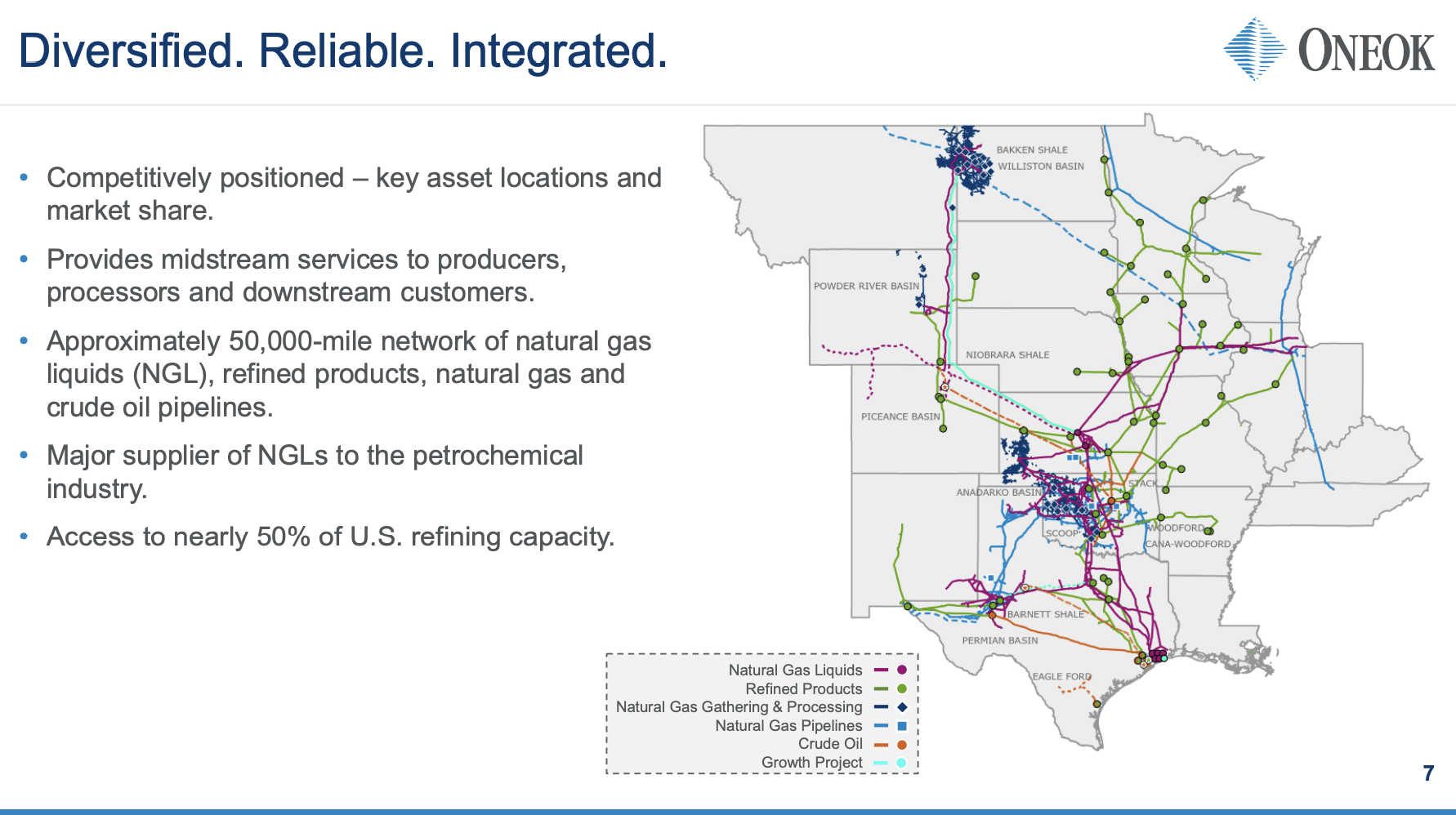

The corporate has roughly 50 thousand miles of pipelines and entry to half of the refining capability within the U.S.

ONEOK Inc.

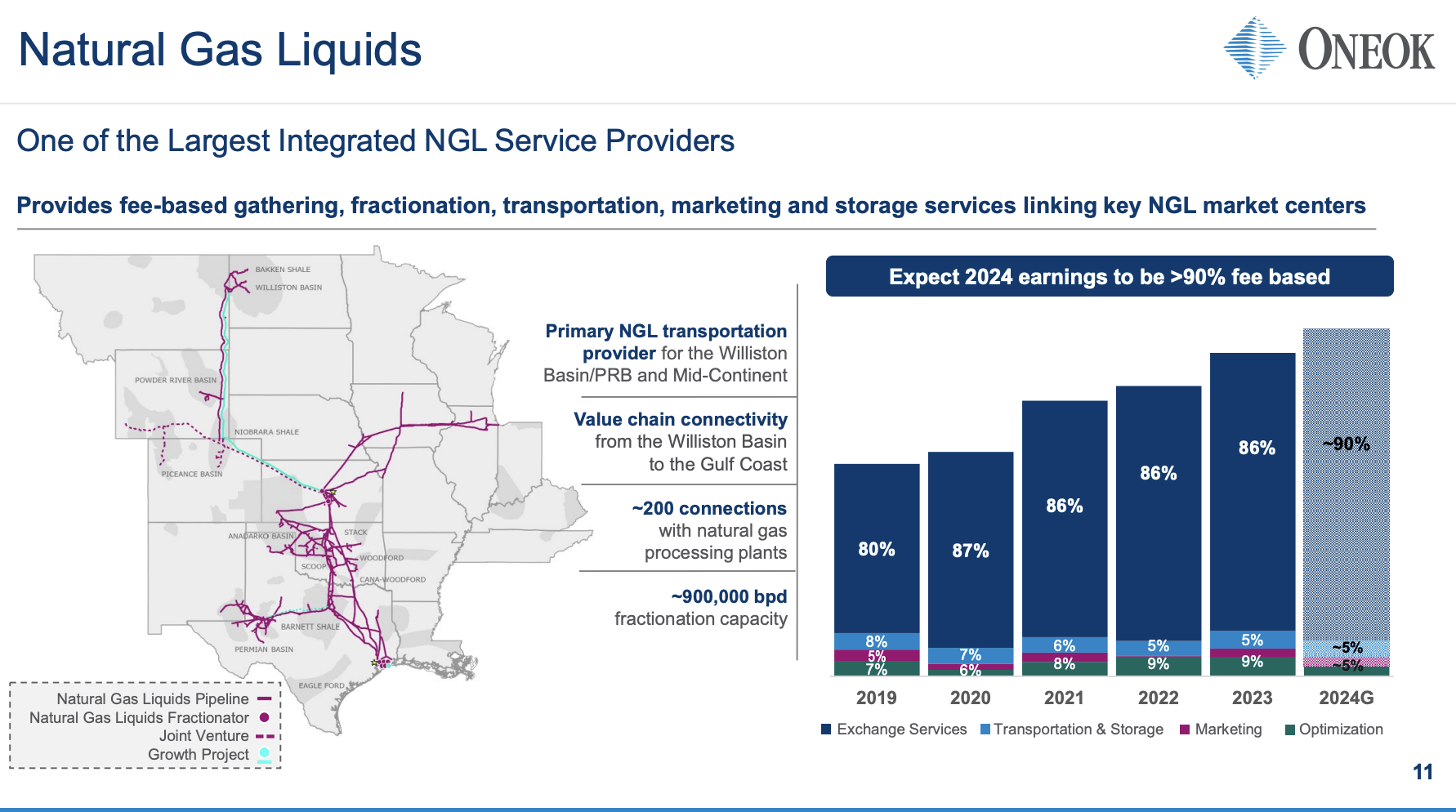

Even higher, the corporate additionally advantages from more and more favorable contracts. As we are able to see beneath, this yr, greater than 90% of its NGL earnings are anticipated to be fee-based. That might be up from 80% in 2019.

ONEOK Inc.

In truth, over the previous decade, the corporate has remodeled from an ultra-high unstable midstream firm to a dependable big with a constantly rising dividend, subdued capital necessities, and an more and more wholesome stability sheet.

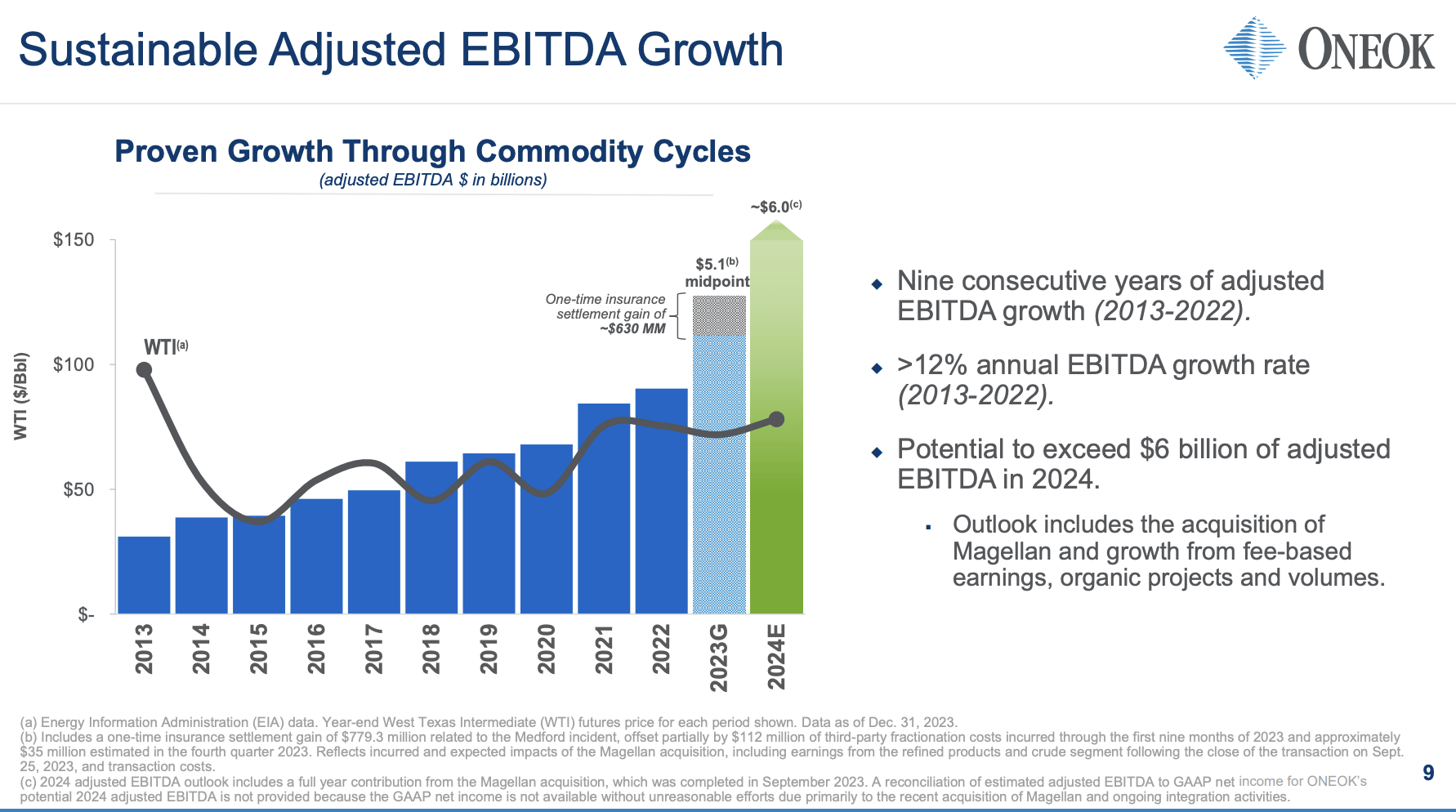

Over the previous decade, the corporate has maintained a powerful streak of adjusted EBITDA progress, which proves its resilience by way of many commodity cycles, together with the 2014/2015 oil value crash and the pandemic.

As we are able to see beneath, the corporate hasn’t seen a decline in adjusted EBITDA since a minimum of 2013, rising its adjusted EBITDA by 12% per yr in the course of the 2013-2022 interval.

ONEOK Inc.

That is the facility of midstream corporations. They profit from throughput volumes. They’re considerably immune in opposition to low commodity costs until costs are so low that producers scale back output.

Nonetheless, please remember that buyers eager to guess on greater commodity costs could also be higher off shopping for oil and fuel producers.

Personally, I am doing each. I am shopping for upstream for particular dividends and probably outsized positive aspects if oil continues to rally and midstream for constant revenue progress and security.

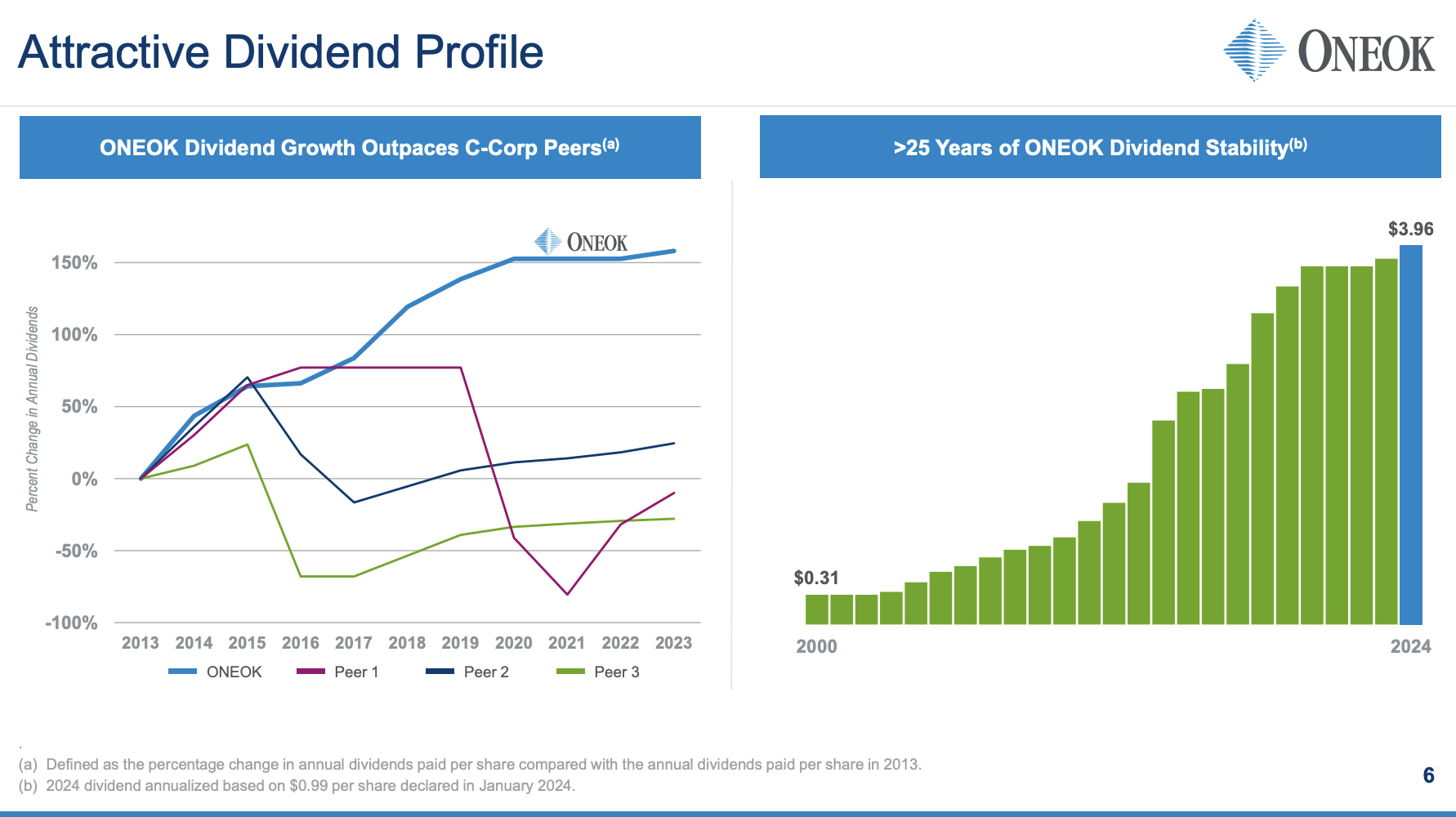

Going again to OKE’s monitor file, dividends paid to shareholders have additionally elevated considerably. In 2000, the corporate paid $0.31 per share. After mountain climbing its dividend by 3.7% on January 17, it has an annualized 2024 dividend of $3.96. This interprets to a yield of 4.9%.

ONEOK Inc.

The very best information for the dividend is that OKE is more and more flushed with money.

See, one of many largest issues midstream corporations confronted up to now ten years (and earlier than that) is elevated capital expenditures (“CapEx”). In spite of everything, constructing a large pipeline community may be very costly!

Now, these corporations are seeing decrease bills as tasks have been completed and are actually bringing in money.

For instance, in 2019, OKE spent $3.8 billion on CapEx. This yr, that quantity is anticipated to be $1.8 billion, probably adopted by a decline to $1.5 billion in 2026.

In the meantime, free money stream is anticipated to rise from -$1.9 billion in 2019 to $2.9 billion in 2024 and $4.0 billion in 2026.

As OKE has a $46.8 billion market cap, it implies a 2024E free money stream yield of 6.2%.

In different phrases, the corporate has sufficient free money stream to cowl its dividend 1.3x! In 2026, that quantity may rise to eight.5% (1.7x its present dividend).

Even higher, the corporate has an investment-grade credit standing of BBB and a long-term internet leverage goal of three.5x EBITDA. This yr, internet leverage is anticipated to be 3.5x.

ONEOK Inc.

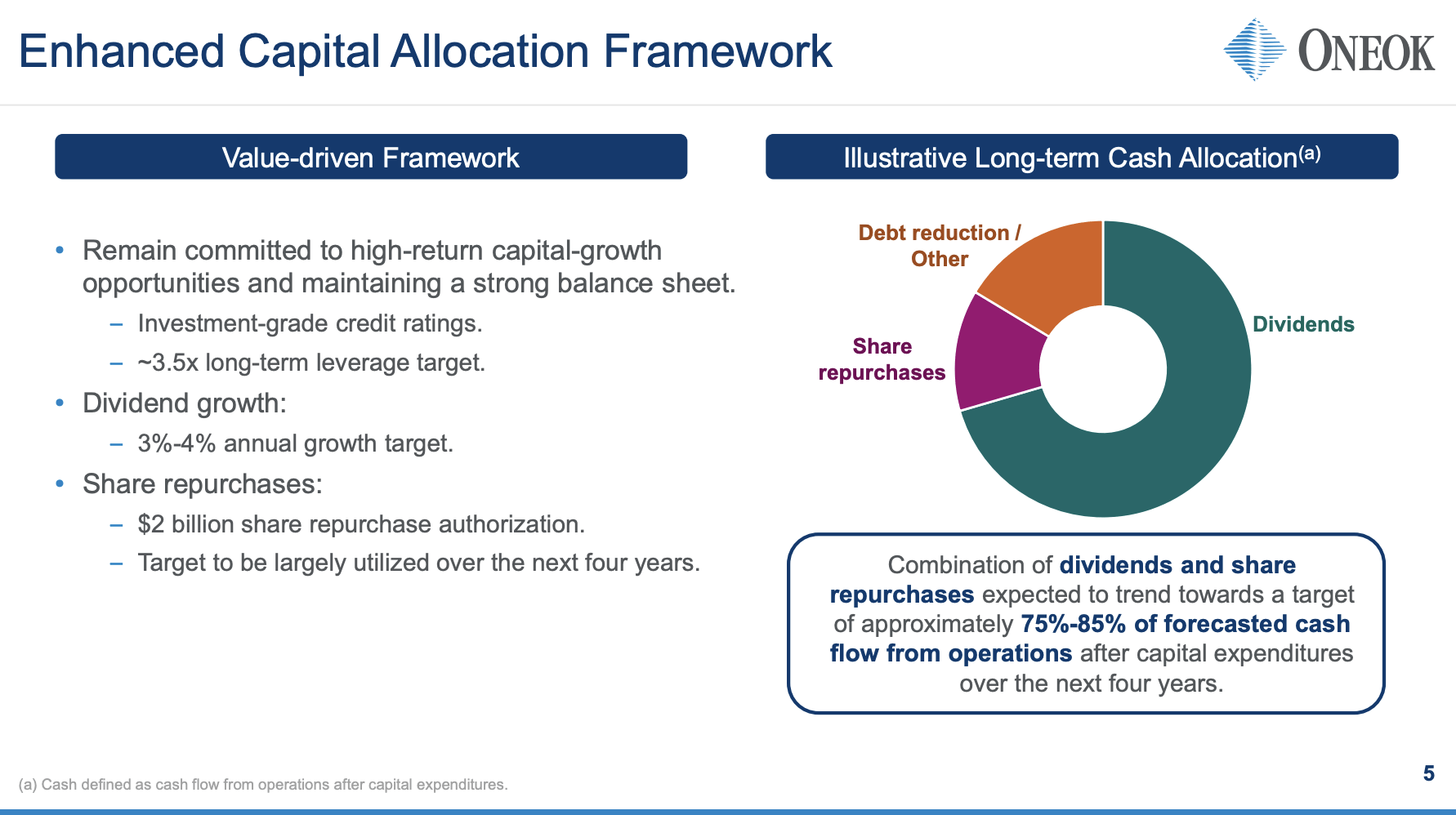

Consequently, the corporate stays dedicated to constant dividend progress and buybacks.

- It targets annual dividend progress between 3-4%.

- It introduced a $2 billion buyback program.

- Over the following 4 years, the corporate goals to distribute as much as 85% of post-CapEx working money stream.

In January, we elevated our quarterly dividend 3.7% to $0.99 per share, or $3.96 per share on an annualized foundation. Going ahead, ONEOK expects to focus on an annual dividend progress fee ranging between 3% to 4%.

We additionally introduced a $2 billion share repurchase authorization, which we goal to largely use over the following 4 years. This program is complementary to the dividend progress fee when eager about shareholder return sooner or later.

Over the following 4 years, ONEOK’s mixture of dividends and share repurchases is anticipated to development in direction of a goal of roughly 75% to 85% of forecasted money stream from operations after recognized capital expenditures. – OKE 4Q23 Earnings Call

I consider these numbers make OKE – and lots of of its friends – incredible long-term investments, as we’re coping with an organization able to constant earnings progress used to reward shareholders in ways in which had been unimaginable a couple of years in the past.

Constant Progress & A Good Valuation

Along with having an more and more favorable free money stream profile, there’s loads of progress left.

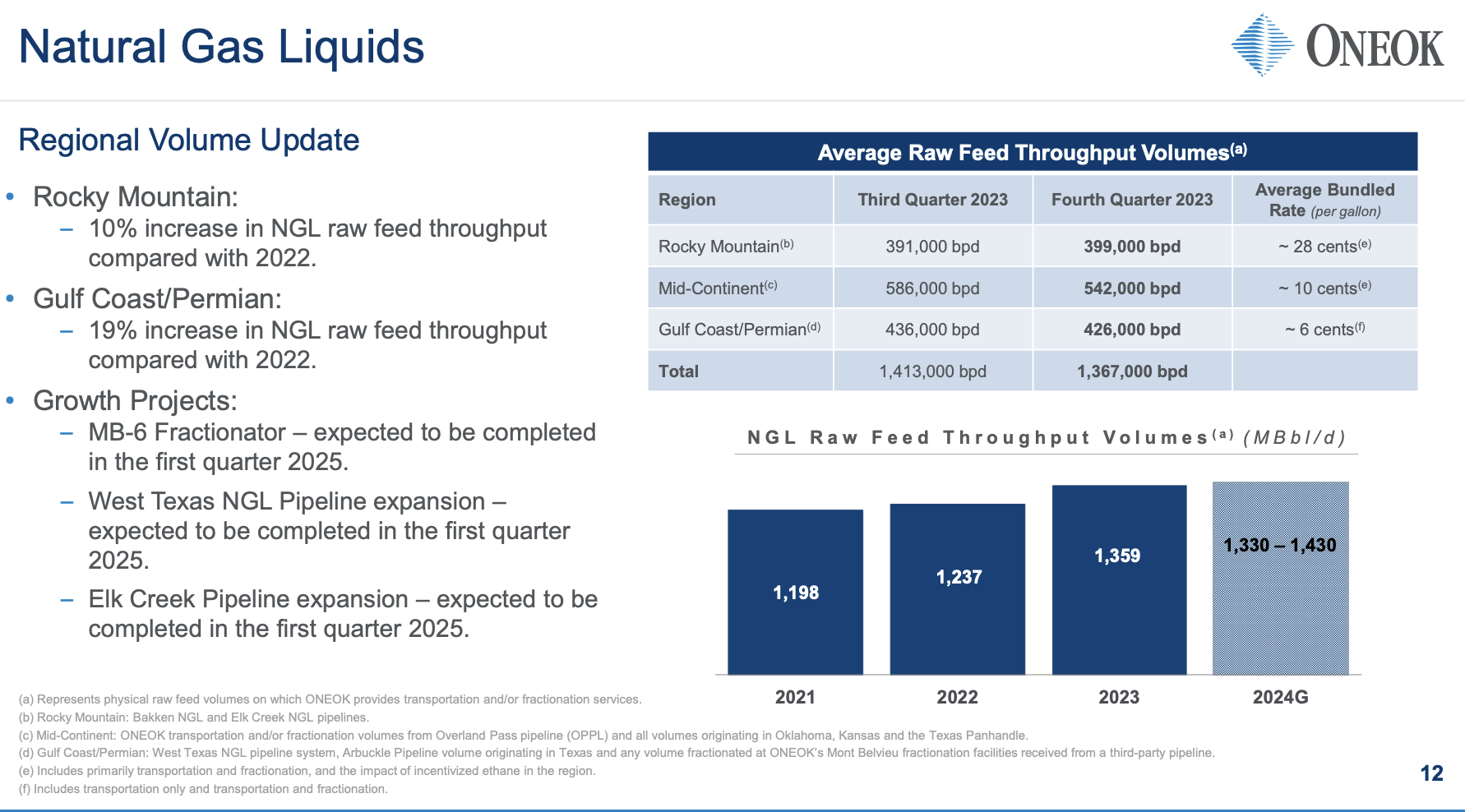

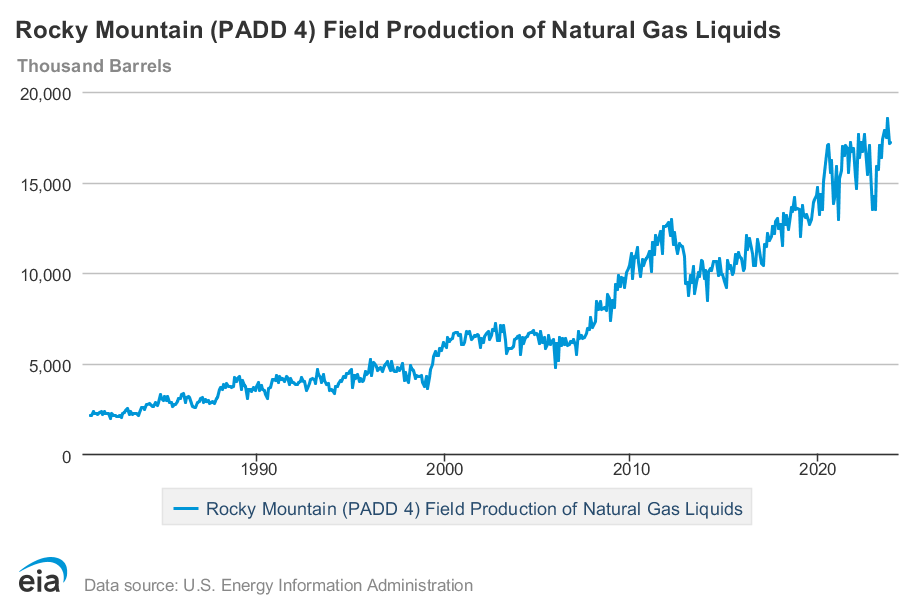

For instance, the Rocky Mountain area has seen important progress.

NGL volumes from the area have surged at an annual fee of greater than 20% over the previous 5 years, whereas pure fuel processing volumes have grown at a gentle 10% annual fee throughout the identical interval.

In 4Q23, the corporate reported 14% greater pure fuel processing volumes. NGL volumes rose by 10%.

Furthermore, OKE is formally transferring ahead with increasing the Elk Creek pipeline to 435,000 barrels per day, rising whole NGL capability out of the Rocky Mountain area to 575,000 barrels per day.

ONEOK Inc.

Even higher, expectations for quantity progress within the Rocky Mountain and Mid-Continent areas stay robust, pushed by higher-than-expected effectively connections in 2023 and constant producer exercise ranges anticipated in 2024.

Vitality Data Administration

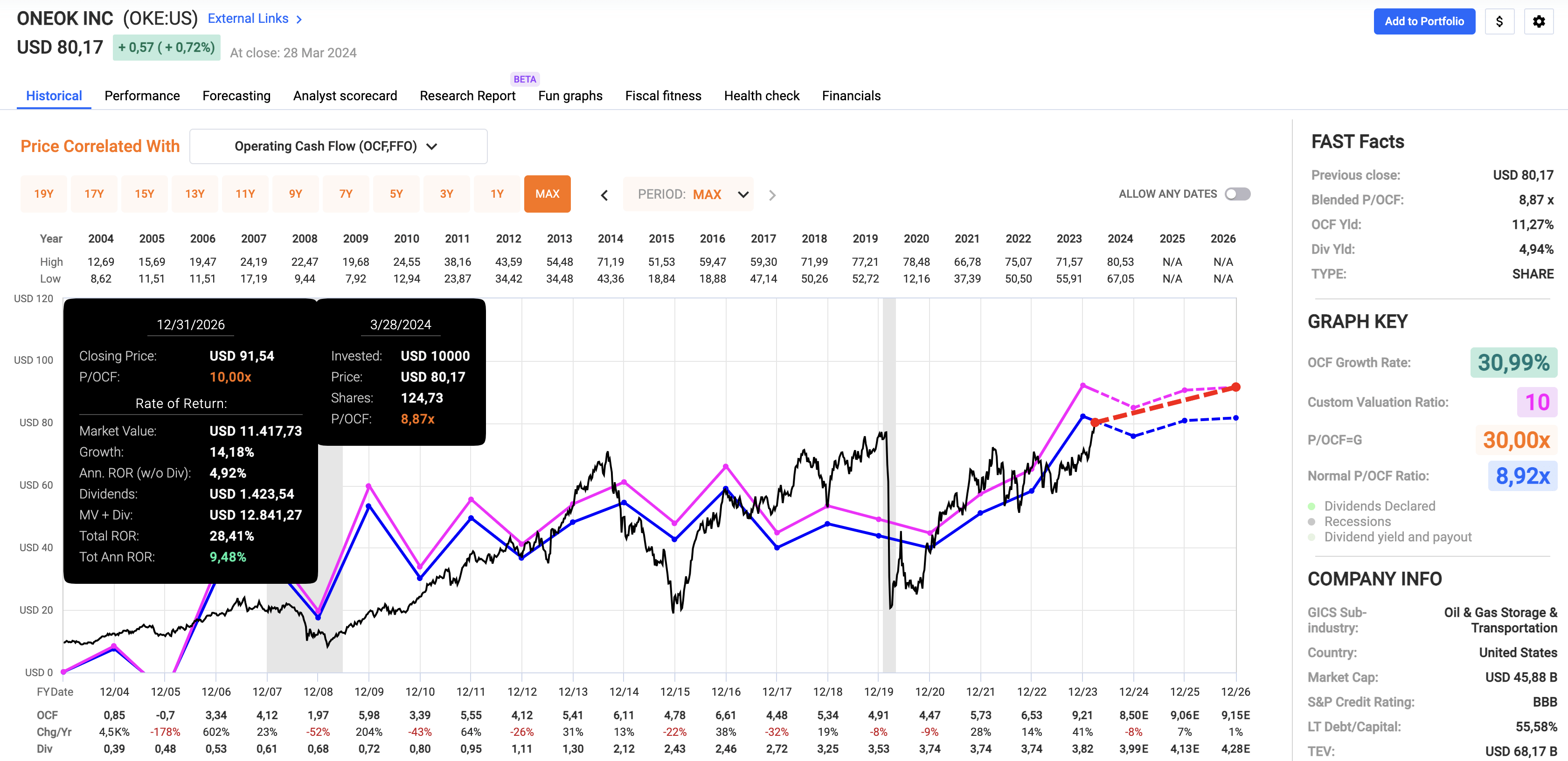

Transferring over to its valuation, regardless of returning 16% since December 29, the inventory nonetheless presents potential for brand spanking new buyers and buyers trying so as to add to their positions.

At present, OKE trades at a blended P/OCF (working money stream) ratio of 8.9x.

Traditionally, the corporate has traded at an 8.9x a number of. Nonetheless, as a result of the corporate has turn into extra mature, I count on {that a} 10x a number of may be very acceptable. I might not even rule out an 11x a number of within the years forward if the market shifts from progress to worth shares.

FAST Graphs

Furthermore, the corporate is anticipated to develop its OCF by 7% in 2025 after a possible 8% decline in 2024. 2026 is anticipated to see 1% progress.

My private opinion is that each one of those progress charges will possible find yourself being greater than anticipated, as I am very bullish on NGL manufacturing and since I see greater related fuel manufacturing – particularly if crude oil manufacturing in key basins continues to extend.

Combining a 10x OCF a number of with anticipated EPS progress and its 4.9% yield, we get a possible annual return of 9.5-10.0%.

I consider the corporate will possible exceed that quantity on a chronic foundation.

Consequently, I stay bullish and consider that OKE stays a incredible funding for everybody in search of high-quality revenue – particularly in an atmosphere the place we may see a rotation from progress to worth, as I mentioned in this article (amongst many others).

Takeaway

Investing in power infrastructure giants like ONEOK presents not simply constant revenue progress but additionally the potential for substantial long-term returns.

With its diversified operations, resilient earnings, and dedication to shareholder rewards by way of dividends and buybacks, ONEOK stands out as a promising participant in its sector.

Its more and more favorable free money stream profile, mixed with growth tasks and robust quantity progress expectations, make it a horny inventory for each income-focused buyers and people looking for capital appreciation.

Execs & Cons

Execs:

- Constant Revenue Progress: OKE has a diversified portfolio and a monitor file of steadily rising dividends, making it a dependable revenue generator.

- Resilient Earnings: Regardless of market fluctuations, OKE has proven resilience with its constantly rising adjusted EBITDA over the previous decade.

- Favorable Free Money Movement Profile: The corporate’s enhancing free money stream place, coupled with diminished capital expenditures, bodes effectively for sustained dividend progress.

- Progress Alternatives: The Rocky Mountains and different areas present constant progress alternatives.

- Cheap Valuation: Regardless of latest positive aspects, OKE’s valuation stays affordable.

Cons:

- Demand Dependency: Though OKE’s dependence on commodity costs is restricted, commodity demand dangers may rise in a recession.

- Potential Regulatory Dangers: Modifications in rules or environmental insurance policies may have an effect on the corporate’s operations and profitability.

- Aggressive Panorama: OKE operates in a aggressive trade, dealing with competitors from different midstream corporations. Nonetheless, typically, the main midstream corporations have a tendency to come back with vast moats.

- Market Volatility: Like every inventory, OKE is topic to market volatility, which may result in short-term fluctuations in its share value.