fullvalue

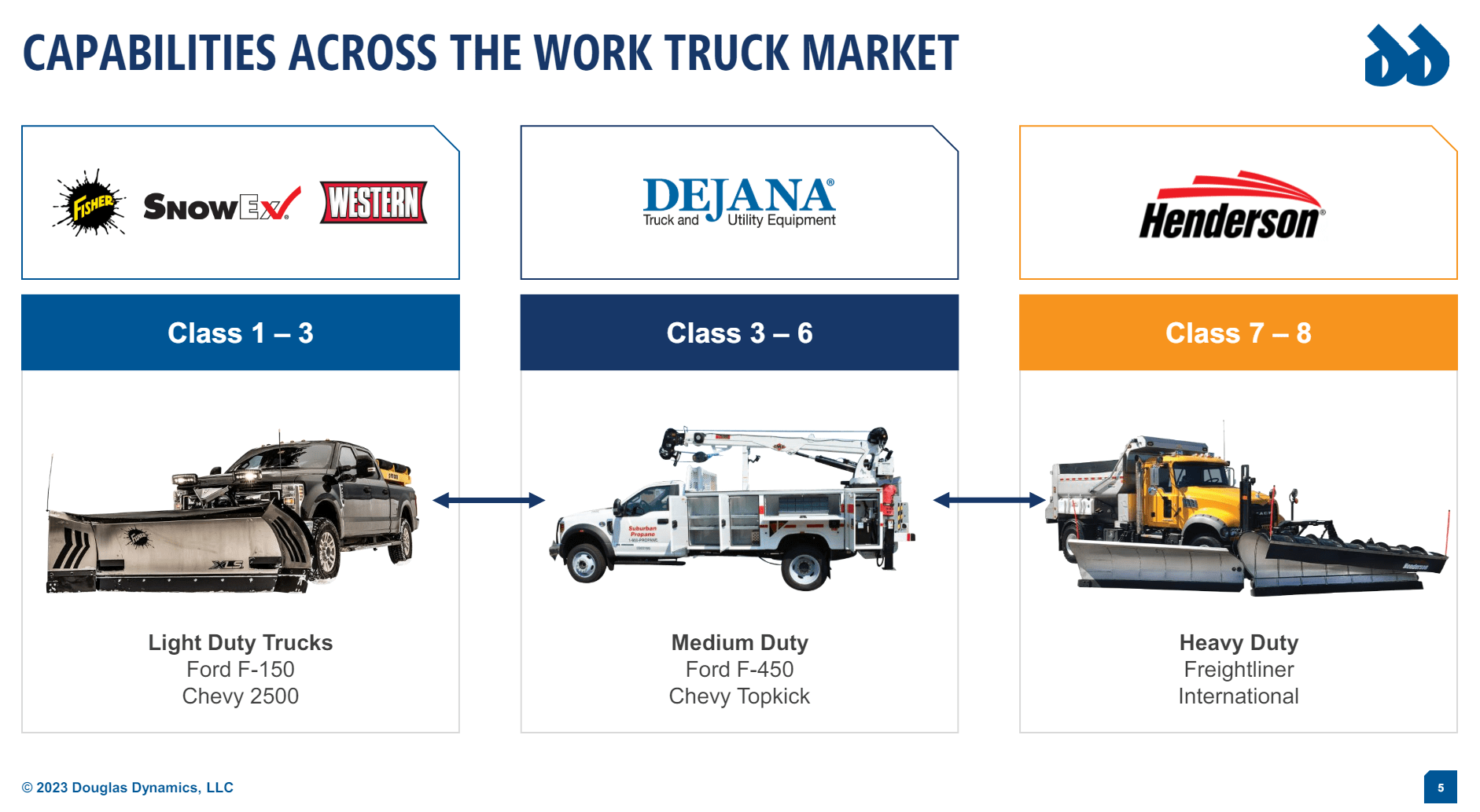

Douglas Dynamics, Inc. (NYSE:PLOW) is the market leader in snow and ice control equipment for light trucks, owning 50-60% of the market share for these products. It is a premium provider and commands premium prices. Distributors and end users pay up for these products because these products, under the Fisher, Henderson, SnowEx, and Western brands, are known to be high quality and trusted. These operations encompass PLOW’s Work Truck Attachments segment.

PLOW Products (May 2024 Presentation)

In its Work Truck Solutions Segment, PLOW manufactures snow and ice equipment for heavier duty trucks used by municipalities, and upfits class 3-8 commercial work vehicles involved in snow and ice control and other general vocational purposes. This segment was created with the acquisitions of Henderson and Dejana in 2014 and 2016. This segment is considered the higher growth segment by management due to the fact that PLOW’s high market share in snow and ice control equipment and the mature market, make it difficult to grow at a pace much higher than nominal GDP.

The investment thesis is relatively simple. PLOW is currently trading at a near-trough multiple on depressed earnings due to back years of well-below average snowfall in the East Coast and Midwest areas of the US. In fact, according to PLOW’s management, this has been the worst year in terms of snowfall in the over 75-year history of the business. I think that investors have grown impatient with the level of earnings over the past two years, especially after management publicized an EPS target of $3.00 by 2025. When snowfall reverts to the long-term average, which it will, PLOW’s earnings will rise and the stock’s multiple should expand.

Additionally, I believe investors are underestimating the potential margin expansion that could come with a rise in demand. PLOW has been aggressively cutting costs due to the current environment and once this demand comes back, the company should benefit greatly from operating leverage.

With these factors in mind, I see a credible case for PLOW to trade between $35-$40 in 12–18 months as FCF rises. This would provide 40-50% upside from current prices.

Q1 Earnings

Q1 2024 earnings were much improved when compared to the prior year period. The improvements were primarily due to continued positive momentum in the Work Truck Solutions segment, better snow conditions which led to improved volume in the Work Truck Attachments segment, and cost savings initiatives. Consolidated sales grew by 16% led by growth of 23% in the Attachments segment and growth of 23% in the Solutions segment. PLOW’s adjusted EBITDA margin also expanded over 10% year over year led once again by the Attachments segment that had adjusted EBITDA margin expansion of a staggering 34.5%, followed by the Solutions segment that had adjusted EBITDA margin expansion of 4%. The results from the Attachments segment demonstrate how poor the snow conditions were in the prior year period.

Commentary from management was largely positive except for discussions on weather conditions. Regarding the Solutions segment, management noted that the backlog was still at historically high levels despite supply chain improvements which is leading to improved ability to work through its backlog.

Work Truck Solutions Industry Commentary

The general slowdown in heavy-duty and medium duty truck production may seem worrisome for PLOW’s Solutions segment, but PLOW is an upfitter that works on custom requests. Even though class 3-8 truck production is falling and is expected to continue falling as pent-up demand has largely been met, and the freight industry works through the deep recession it is currently in, PLOW only needs strength in pockets of the truck market.

For example, Rush Enterprises. Inc. (RUSHA), an operator of truck dealerships in the US, in its Q1 earnings press release, called out expected strength from vocational truck customers in its aftermarket parts and service segment in CY2024. Most of PLOW’s customers for its Solutions segment are likely vocational customers, as they need specific upfitted trucks for their specific jobs, unlike freight fleets that purchase generic class 3–8 trucks directly from OEMs or dealers. The relevant section in the press release said the following:

As we look ahead, over-the-road carriers continue to be plagued by challenging economic factors and the current freight recession, which we currently believe will extend into at least late 2024. In the second quarter, we expect that new Class 8 and new Class 4-7 truck sales will improve compared to the first quarter, primarily due to the timing of deliveries to certain of our larger customers, and we believe that demand should remain steady for new Class 4-7 trucks for the remainder of the year. In the aftermarket, difficult operating conditions are likely to continue, but we expect some normal seasonal lift in the warmer months, as well as strong demand from vocational customers throughout the year.

This relative end market strength, along with PLOW’s ability to grow organically and gain market share, bodes well for investors. For reference, revenue in the Solutions segment has grown from $137mm in FY2017, to $276mm in FY2023, for a CAGR of about 12%. FY2023 was also negatively impacted by reduced chassis availability from OEMs, which makes this growth even more impressive.

Given continued strong demand from vocational truck customers, along with PLOW’s history of impressive growth in the Solutions segment, investors should be confident that this segment will continue to hum for the foreseeable future. Weather conditions, while an uncontrollable factor, should be the main focus. Longer-term focused investors should see the impatience of those investors that are not waiting for the weather to turn as an opportunity to invest in market leading and growing businesses at a price that reflects depressed earnings and a near trough multiple.

Financial Model and Valuation

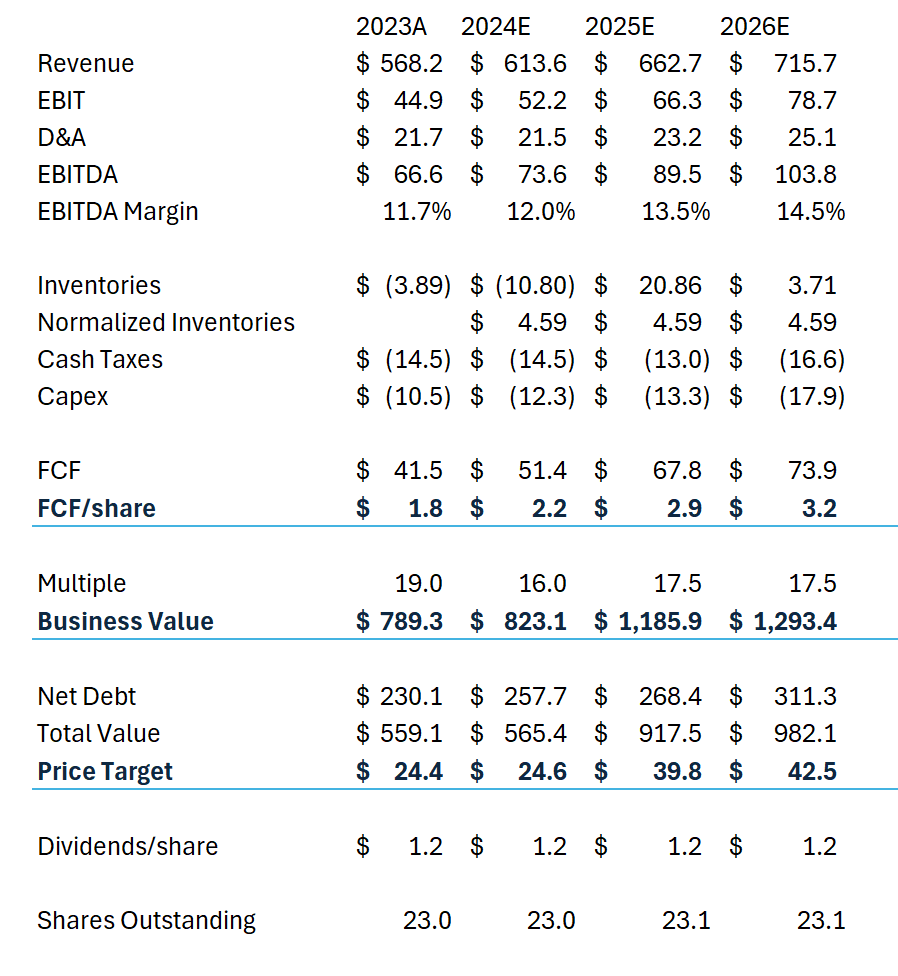

Below is a financial model that reflects what I believe are credible expectations for PLOW over the next few years. Of course, it’s impossible at this point to predict what snowfall will look like next winter, but I can say with high confidence that the current low snowfall trend will move back up towards its long-term average eventually. When this happens, PLOW’s earnings will be a coiled spring, especially as the current cost cuts should lead to extra operating leverage when demand returns. As a note, I use the normalized inventory change number in the model when calculating free cash flow. I am doing this as I believe the market will view the current inventory build-up as non-recurring, which is currently caused by unsustainably low demand.

PLOW Financial Model (Created by Author)

Based on my estimate of FY2025 and FY2026 FCF per share and a 15-20x multiple, I believe the stock may trade between $35 and $40 over the next 12–18 months. A 15-20x multiple seems fair due to the stock’s historic multiple, and due to the fact that PLOW operates a market leading, and highly cash generative business in its Attachments segment, and a growth business in its Solutions segment that has a long-term history of steady growth.

The primary risk with the stock is the uncertainty of weather, as demonstrated by the recent, historically poor past few seasons of weather. Not only does this reduce earnings, but it leads to a longer sales cycle and a build-up of inventory, which affects FCF in the next year on top of the current year. If this streak of poor weather continues, PLOW’s elevated inventory may become more obsolete and more costly to hold.

Another risk is that the company’s CEO, Robert McCormick, recently retired. While this doesn’t seem like it has to do with operational issues, there is a possibility that he saw upcoming difficulties in the business or that the business suffers from operational issues during the CEO transition period.